Captures has widened its scope to include news related to all the members of the Regional Comprehensive Economic Partnership (RCEP) agreement which was signed towards the end of 2020. Besides the ASEAN Member States, this includes Australia, New Zealand, China, Japan, and South Korea. The other weekly newsletters under CARI, China-ASEAN Monitor and Mekong Monitor will also be consolidated into the Captures newsletter. We hope this new version of Captures will serve you better and look forward to providing a curation of stories relevant to ASEAN and its trading partners.

VIET NAM, THAILAND

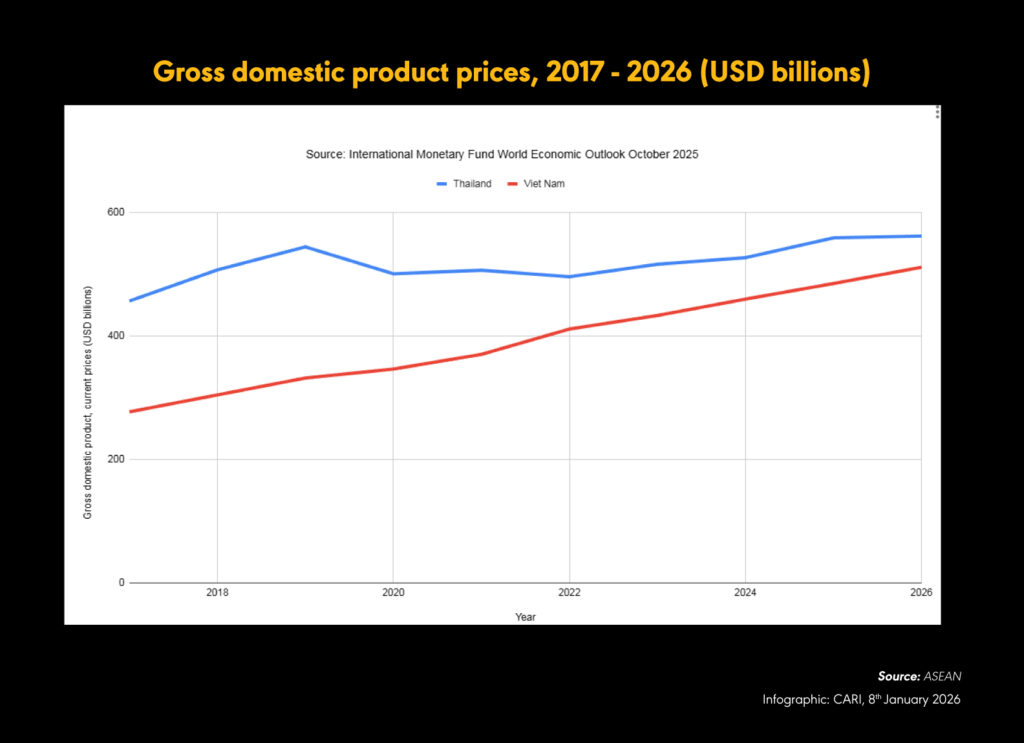

Viet Nam projected to overtake Thailand in nominal GDP as early as 2026

(05 January 2026) Viet Nam is projected to overtake Thailand in nominal GDP as early as 2025, driven by accelerated public works spending and higher growth, while Thailand’s economy is slowing amid domestic political instability and its border conflict with Cambodia. Viet Nam’s real GDP is estimated to have grown about 8% in 2025, and the government targets growth above 10% from 2026. If realised, Viet Nam’s nominal GDP could reach the mid-USD 500 billion range by 2026 or 2027, surpassing Thailand and ranking third in Southeast Asia after Indonesia and Singapore, with per capita GDP exceeding USD 5,000. Public investment is a key driver, with 2026 infrastructure spending plans set to rise about 26%, potentially lifting growth by 1.6 percentage points versus 2025. Major projects include a new airport near Ho Chi Minh City scheduled to open in 2026 and a Chinese-backed railway under construction in northern Viet Nam. However, legal reforms and administrative streamlining remain constraints, with more than 2,000 investment projects facing obstacles. In contrast, the OECD forecasts Thailand’s real GDP growth at 1.5% in 2026, down 0.5 percentage point year on year, citing high household debt, weak consumption, a slow tourism recovery, and pressure on manufacturing from U.S. tariffs. The OECD warns Thailand risks being overtaken not only by Viet Nam but also by the Philippines. Geopolitical risks have increased following intensified Thailand–Cambodia border clashes since May, reducing bilateral trade and tourism and raising investor concerns. The OECD projects Viet Nam’s GDP growth at 6.2% in 2026, below Hanoi’s target, citing potential export slowdowns amid U.S. tariffs of around 20% on Southeast Asian countries, while Vietnamese economists highlight the need to diversify exports beyond the U.S. to markets in the Middle East, Africa and South America.

MALAYSIA

Malaysia expected to rely more on domestic demand in 2026 as external growth weakens

(06 January 2026) Malaysia is expected to rely more on domestic demand in 2026 as external growth weakens due to US tariffs, while the official forecast projects GDP expansion of 4.0%–4.5%, slightly slower than in 2025 and driven mainly by private consumption, investment and tourism. The Socio-Economic Research Centre said the key uncertainty is whether private consumption can continue to sustain growth amid spillover effects from US tariffs. Household spending is supported by a tight labour market, government cash assistance and a scheduled civil service salary increase, while inflation remains contained due to subdued commodity prices. Business investment growth may moderate as the wave of data centre investments reaches its later stage. Bank Muamalat Malaysia Bhd said downside risks include a heavier-than-expected impact from the US tariff regime, uncertainty over sector-specific trade measures, geopolitical disruptions to trade and energy flows, and continued global market volatility. Bank Negara Malaysia is widely expected to keep the overnight policy rate unchanged, supported by steady growth and benign inflation. The ringgit strengthened more than 10% against the US dollar in 2025 to around 4.06 and is forecast to appreciate further to as strong as 3.95 by end-2026, supported by looser US monetary policy, sustained foreign direct investment and tourist inflows linked to the Visit Malaysia Year campaign.

INDONESIA

Government bond market records net foreign inflow in 2025 after investors returned in December

(06 January 2026) Indonesia’s government bond market recorded a small net foreign inflow in 2025 after overseas investors returned in December, offsetting earlier outflows linked to political unrest and leadership changes. Finance ministry data compiled by Bloomberg show net foreign buying of USD 388 million in December, the first monthly inflow since August, resulting in a full-year net inflow of USD 337 million and extending annual foreign buying to a third consecutive year. From September to November, global funds sold about USD 4.6 billion of Indonesian bonds following unrest in several cities and the dismissal of long-serving finance minister Sri Mulyani Indrawati, alongside concerns over wider fiscal deficits under the new finance minister and potential pressure on Bank Indonesia’s independence. PT Mandiri Sekuritas said foreign positioning had become very light, making the market sensitive to even modest improvements in sentiment. They attributed the December inflows to a weaker US dollar and manageable domestic debt issuance. Bank Indonesia kept its policy rate unchanged in December to support rupiah stability while signalling it would continue to look for scope to cut rates, easing concerns about aggressive monetary easing to support government growth policies. Analysts state that foreign inflows could continue in 2026 if the US dollar and Treasury yields decline, but warned that risks remain from possible state revenue shortfalls amid plans for higher government spending.

INDONESIA

Headline inflation increases to 2.92% year-on-year in December

(06 January 2026) Indonesia’s headline inflation increased to 2.92% year on year in December from 2.72% in November, exceeding market expectations of 2.73% but remaining within Bank Indonesia’s 1.5%–3.5% target range, according to Kenanga Research. Full-year inflation averaged 1.9% in 2025, down from 2.3% in 2024 and in line with Kenanga’s forecast. Month-on-month inflation accelerated to 0.64% in December from 0.17% in November, the highest in eight months, mainly due to rising food prices. Core inflation edged up to 2.38% year on year from 2.36%, a seven-month high, indicating steady domestic demand. Inflation in food, beverages and tobacco rose to 4.58% from 4.25%, driven by higher prices of red chilies, fresh fish, chicken meat and onions. Transportation inflation increased to 1.23% from 0.71%, the highest in 16 months, reflecting rising vehicle prices. Inflation in personal care and other services surged to a record 13.33%, pointing to higher personal care-related costs. Kenanga maintained its 2026 inflation forecast for Indonesia at 2.5%, compared with an estimated 1.9% in 2025, citing fading low base effects, festive demand and potential weather-related food price volatility. The firm said near-term monetary easing is constrained by inflation risks and a fragile rupiah amid global uncertainty and geopolitical tensions. However, Indonesia’s 5.4% growth target for 2026 supports further accommodation, with Kenanga expecting two rate cuts in the first half of 2026, subject to rupiah stabilisation.

THE PHILIPPINES

Bangko Sentral ng Pilipinas signals one final policy rate cut in 2026

(06 January 2026) The Bangko Sentral ng Pilipinas signalled that it may deliver one final policy rate cut this year, possibly in February, to conclude its easing cycle. The central bank said the policy rate is “very close” to the desired level and that any additional easing would be limited and dependent on incoming data, a view echoed by the Monetary Board in a separate statement. The guidance follows a rise in headline inflation to 1.8% year on year in December, above the Bloomberg median estimate of 1.4%, driven by typhoon-related disruptions that lifted vegetable and fish prices, according to the Economic Planning department. The central bank expects inflation to edge up this year but remain within the 2%–4% target range. The BSP said the economic outlook has weakened, but domestic demand is expected to recover gradually as lower interest rates take effect and public spending improves. The central bank estimates GDP growth at 4.6% in 2025, improving to 5.4% in 2026. The central bank added that if growth in 2026 falls below 5%, there may be justification for an additional rate cut beyond the 25 basis points currently priced in by markets.

SINGAPORE

Economy grows 4.8% in 2025 in strongest performance since 2021

(06 January 2026) Singapore’s economy grew 4.8% in 2025, exceeding the government’s 4% forecast and marking its strongest performance since 2021, supported by AI-driven electronics demand and trade front-loading amid US tariff uncertainty. The World Trade Organization revised its 2025 global merchandise trade growth estimate up to 2.4% from an earlier forecast of contraction, while Singapore recorded growth of 4% and above for a second consecutive year. Fourth-quarter 2025 GDP expanded 5.7% year-on-year, up from 4.3% in the third quarter. Non-oil domestic exports rose 11.6% year-on-year in November, beating the 6.8% consensus forecast and marking a second month of double-digit growth. For 2026, the WTO forecasts global goods trade growth of 0.5%, reflecting the delayed impact of US tariffs agreed and implemented in the second half of last year, while the IMF projects global growth of 3.1% versus 3.2% previously. Singapore’s government has set a 2026 growth forecast of 1% to 3%, with HSBC and OCBC projecting 2%, Oxford Economics 3.8%, and Nomura 3.7%. HSBC said electronics manufacturing led growth in the third quarter while pharmaceuticals were subdued, supported by diversification including double-digit growth in transport engineering. Singapore’s exposure to a 10% baseline US reciprocal tariff, lower than most Asian peers, is expected to attract trade diversion and foreign investment, with Asean-6 accounting for 14.5% of global FDI and 65% of that flowing to Singapore. Maybank cited continued deepening of Singapore’s AI supply chain in 2026 with the opening of Micron’s SGD 8.9 billion advanced packaging facility and UMC’s SGD 6.5 billion wafer plant. Analysts expect AI investment momentum to moderate but persist, supporting exports, infocomm services, and investment inflows, alongside construction and modern services, to underpin economic resilience despite slower global trade growth.

LAO PDR

Lao PDR records year-on-year inflation rate of 5.6% in December 2025

(05 January 2026) Lao PDR recorded a year-on-year inflation rate of 5.6% in December 2025, according to the Consumer Price Index released by the Ministry of Finance’s Lao Statistics Bureau, with prices falling 0.3% month-on-month for a second consecutive month. Housing, water, electricity and cooking fuel prices rose 18.1% over 2025, led by a 105.0% increase in electricity tariffs and a 40.1% rise in water charges. Healthcare inflation reached 14.4%, with hospital services up 26.4% and pharmaceutical products up 13.8%, while education prices increased 11.4%, including a 19.2% rise in supplementary tutoring fees. Clothing and footwear prices rose 8.1%, with women’s clothing increasing 25.2%, partly linked to appreciation of the Thai baht affecting imported goods. Miscellaneous goods and services recorded the largest annual increase at 29.2%, driven by a 58.8% surge in jewellery and gold accessory prices. In December, food and non-alcoholic beverage prices declined 0.8% month-on-month, led by sharp falls in vegetable prices, including shallots down 35.4%, coriander down 29.6% and cucumbers down 16.4%. Transport costs eased 0.6% month-on-month as fuel prices fell 3.7%, while housing-related costs rose 0.6% and electricity bills increased 1.6% during the month. Core inflation for 2025 was reported at 6.9%, compared with non-core inflation of 4.2%. Prices of domestically produced goods increased 6.5% year-on-year, outpacing a 3.8% rise in imported goods. The LSB noted that although inflation moderated from levels above 15% earlier in 2025, elevated utility costs remain a significant burden on households and businesses.

RCEP Monitor

AUSTRALIA

Consumer prices rise 3.4% year-on-year in November 2025, down from 3.8% in October

(07 January 2026) Australian consumer prices rose 3.4% year on year in November, below the 3.6% market expectation and down from 3.8% in October, according to Australian Bureau of Statistics data. The lower reading reduced near-term expectations of a Reserve Bank of Australia rate hike, with markets pricing a two-thirds probability of rates remaining on hold at the February meeting. Following the release, the Australian dollar weakened from 67.38 US cents to 67.24, while the ASX200 rose from 8,700 to 8,734 points. Despite the moderation, NAB economists maintained forecasts for rate increases in February and May, while markets continue to expect a first hike by June and potentially a second before December. Deloitte Access Economics said a February hike would be premature given uncertainty over the recent inflation resurgence. ANZ economists described the February decision as finely balanced, citing easing prices in some categories. Clothing and footwear prices fell 3.1% month on month in November, while furniture prices declined 4.6% amid Black Friday discounting. Domestic holiday prices dropped 4.1% and international holiday prices fell 0.6%, while health costs declined 0.5% following expanded bulk-billing incentives from 01 November 2025. Housing costs increased 1.1% month on month and 5.2% year on year, driven by higher rents, new home construction costs and a 19.7% rise in electricity prices as rebates expired. Food prices rose 3.3% annually, with meals out and takeaway up 3.5% and meat and seafood up 3.9%. EY said inflation is likely to remain elevated in forthcoming December quarter data and that interest rates will need to be lifted in the first half of 2026 to return inflation towards the target midpoint.

JAPAN

Japanese equities show resilience despite rising geopolitical tensions with China

(07 January 2025) Japanese equities showed resilience despite rising geopolitical tensions with China, with the Topix index falling about 1% after China imposed export controls on items with potential military use and signalled possible tighter restrictions on rare earth sales, while more than half of Topix constituents advanced. The decline followed a strong start to the year, with the Topix and Nikkei 225 rising for two consecutive sessions and both reaching record highs on 06 January, according to Bloomberg-compiled data. Market participants characterised the sell-off as a buying opportunity, with Rayliant Global Advisors stating expectations that tensions would not escalate into a broader market risk. Sector performance diverged, as the Topix Transport Equipment Index fell up to 2.5%, reflecting concerns over supply chain disruption given China’s dominance in rare earths critical for electric vehicles. H Capital warned of continued pricing volatility in electronics and automotive sectors reliant on rare earth inputs. In contrast, Toyo Engineering Corp surged 20% on expectations of increased demand for technologies enabling rare earth recovery and supply chain diversification. Japanese brokerage chief executives continue to forecast a strong year for equities following a more than 20% gain in the Topix in 2025. Goldman Sachs strategists lowered their rating on Japan while maintaining a constructive view on alpha opportunities. Pepperstone Group described the market reaction as a short-term disruption rather than a structural shift, citing supportive global liquidity and relatively attractive valuations.

CHINA, JAPAN

China mulls tightening licensing controls on rare earth exports to Japan

(07 January 2026) China is considering tighter licensing controls on rare earth exports to Japan, according to a China Daily report citing an unidentified source, as bilateral tensions escalate following remarks by Japan’s Prime Minister on Taiwan. The potential measures would cover the same seven rare earth elements that China restricted in April in response to the US-led trade conflict. The report followed an official Chinese announcement banning sales of more than 800 dual-use items to the Japanese military or end-users supporting military capabilities, a category that typically includes rare earths. Heavy rare earths such as dysprosium and terbium remain a key vulnerability for Japan, as they are essential for high-performance magnets and supply is still almost entirely dependent on China. Japan has reduced overall reliance on China for the full suite of 17 rare earths to about 60% in 2024 from 80–90%, supported by government and industry backing for Australia’s Lynas Rare Earths Ltd. Lynas began shipping limited volumes of heavy rare earths to Japanese customers late last year. Shares in Lynas rose as much as 16% in Sydney following the report. Despite progress since China’s 2010 export ban, the episode highlights ongoing exposure in sectors reliant on rare-earth magnets, although Japan has expanded domestic magnet production, encouraged stockpiling and pursued material substitution to mitigate disruption risks.

|

15 participating countries |

20 chapters |

2.2 billion |

US$26.2 trillion |

28% |

| ASEAN member states, Australia, China, Japan, South Korea, New Zealand | trade in goods and services, investment, intellectual property, e-commerce, competition, SMEs, economic and technical cooperation, and government procurement | combined population, 30% world’s population | combined GDP, 30% global GDP | global trade (based on 2019 figures) |