ASEAN Economic Progress: Prospects

Published on 23 October 2019

How conceivable is aspiration 2030?

Southeast Asia is expected to be one of the world’s fastest growing consumer markets over the next decade, with ASEAN members’ GDP forecasted to rise to US$10 trillion by 2030.1 The International Labour Organization (ILO) projected that ASEAN would see the second-largest labour force growth by 2030 (behind India); with the entry of some 59 million people to the workforce.

Along with this development, the middle-class is expected to increase from 29% of the population in 2010 to around two thirds by 2030.2 Expansion in the workforce and middle-class is expected to further drive private domestic consumption.

The question then arises as to what do current developments reveal about the nature of the “gap” between the vulnerabilities identified in the previous section and this vision.

Prospect 1: Riding generational and demographic challenges

Prospect 1: Riding generational and demographic challenges

As ASEAN pushes past 50 years, the option for ASEAN—especially the ASEAN-5—to be a low-cost, mass manufacturing merchandise producer is increasingly a distant past. Demographic trends present challenges. On the one hand, 60% of ASEAN’s population is under 35 along with a growing sizable middle class and educated workforce.

On the one hand, 60% of ASEAN’s population is under 35 along with a growing sizable middle class and educated workforce. On the other hand, it has been observed that some key working populations are “ageing” as birth rates decline and better healthcare increases life expectancy. The number of people who are 65 years or older are forecasted to more than triple by 2050 (Figure 7.1).3

Any effort to “future-proof” the workforce must cater to both the needs of ageing economies in Singapore and Thailand as well as Indonesia’s very sizeable young workforce.

Impediments to workforce participation, mobility, education and training must be removed. Job market-sensitive strategies and business models must develop both technology and “technology-proof” skills such as creativity and entrepreneurship. We see these trends in the decentralised business models of automotive and medical services sectors, as well as partnership models involving cross-sectoral alliances and industry disruptors such as Fintech in the financial services sector.

Prospect 2: Bridging the infrastructure gap

Prospect 2: Bridging the infrastructure gap

Increasing the “seamlessness” of connectivity among physical entities (people and goods) is one critical aspect of enhancing access challenges, thus contributing to production growth.

- According to the Asian Development Bank (ADB), a 10% increase in paved roads is expected to result in a more than 5% improvement in economic growth across Asia.4 With increased prosperity, each US$1,000 increase in GDP per capita could result in 15 more cars per 1,000 residents, thus leading to congestion and greater economic inefficiencies if road networks are not upgraded.

Given the multiplier effect, government spending on transportation infrastructure are expected to increase. Indonesia, Malaysia, Thailand, Vietnam, and the Philippines have already announced multiple initiatives to push infrastructure development, especially for transportation.5 The ADB recently suggested that from 2016 to 2030, ASEAN needs infrastructure investment of around US$2.8 trillion, thus indicating an annual investment requirement of US$184 billion, i.e., equivalent to 5% of ASEAN’s GDP.6

These are just baseline estimates. Climate change mitigation and adaptation would require infrastructure investment to increase to US$3.15 trillion for the same period, with an annual investment requirement of US$210 billion, equivalent to 5.7% of ASEAN’s GDP.

The multiple G2G infrastructure collaborations, especially those involving the Belt and Road Initiative (BRI), would certainly play an important role in meeting ASEAN’s future infrastructure needs, with Indonesia, Vietnam, and Cambodia accounting for the top three recipients of BRI-related capital as of end-2018 (Figure 7.2).

- Estimates for BRI projects in 88 countries point to some US$330 billion worth of investment flowing into the transport and logistics sectors, as well as US$266 billion flowing into the energy and utilities sectors, according to a joint study by LSE IDEAS and CARI.7

As mentioned in the Vulnerabilities section, the various regional infrastructure projects including BRI-related projects, face material, political, implementation and governance challenges.

- Malaysia’s government temporarily suspended the East Coast Rail Link (ECRL) project in 2018 due to costing concerns. The government renegotiated the project and reached a new deal on April 12, 2019 after cutting a third of the original cost of US$16 billion. Construction works on the project resumed on July 25 this year.8

- Indonesia’s US$5.5 billion Jakarta-Bandung Railway project, on the other hand, has been plagued by delays since inception over complexities involving land acquisition and financing, according to LSE IDEAS and CARI.9

These challenges notwithstanding, successful implementation of the BRI is deemed to yield extensive indirect advantages and is also expected to mobilise greater global FDI and trade flows into ASEAN.

- Singapore, for instance, stands to strengthen its position as the regional infrastructure hub given that Singapore-based banks manage up to 60% of ASEAN’s project finance transactions, according to Enterprise Singapore.10

Prospect 3: Region’s digital preparedness

Prospect 3: Region’s digital preparedness

a) Region’s digital preparedness is an advantage

The seamless connectivity of physical infrastructure can smoothen the flow of people and goods and the same can be said of internet infrastructure and its ability to connect ideas and processes.

- Digital technology bridges production gaps by linking producers and buyers directly (disintermediation), thus strengthening and shortening supply chains.

- The World Bank also estimated that by widening the spectrum of sharing through the dematerialisation process, digital tools allow for more efficient use of assets. A 10% rise in fixed broadband penetration could boost GDP growth by 1.4% in developing economies worldwide.11

- A recent study also found that Southeast Asia appears to be on the right side of the digital divide.In 2018, there were 350 million internet users in Malaysia, Singapore, Indonesia, Philippines, Vietnam and Thailand—about 35% more than in 2015.12

- As of January 2019, Southeast Asia’s internet penetration rate was 63%, above the global rate of 57%, while its mobile social media penetration rate was 61% (a total of 402 million users) which is significantly above the global average of 45% (Figure 8.1).

- Internet usage and time spent on social media daily in ASEAN countries is currently higher than more developed economies such as the US or Japan.13 Such high penetration rates is unsurprising considering around 90% of the region’s internet users access the worldwide web via smartphones.14

- Amidst this landscape, Southeast Asia’s internet economy is expected to generate gross merchandise volume (GMV) of US$300 billion by 2025 driven by sectors such as e-commerce, ride-hailing, online media and online travel.15

b) Meeting the 4IR challenge

Is ASEAN ready for the Fourth Industrial Revolution (4IR) given that the region is among the fastest growing internet regions in the world? One sobering perspective is that the exuberance may be somewhat premature when much of ASEAN is “pre-industrial on an industrial scale”. 16

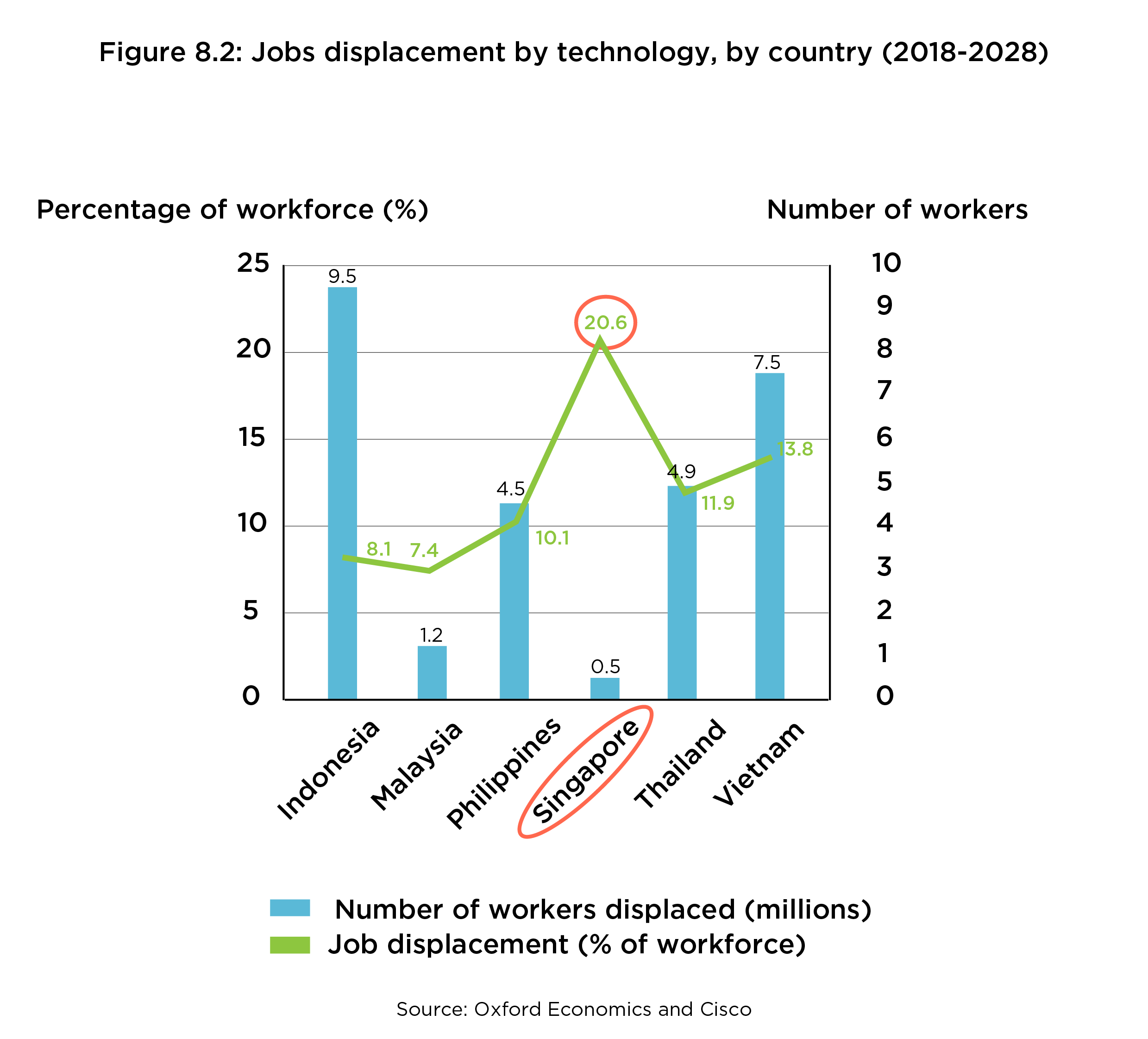

- The exception is Singapore, which is predicted to face the highest rate of job displacement in the region due to technological disruption at 20.6% of the workforce according to a report by Oxford Economics and Cisco in 2018.17 (Figure 8.2).

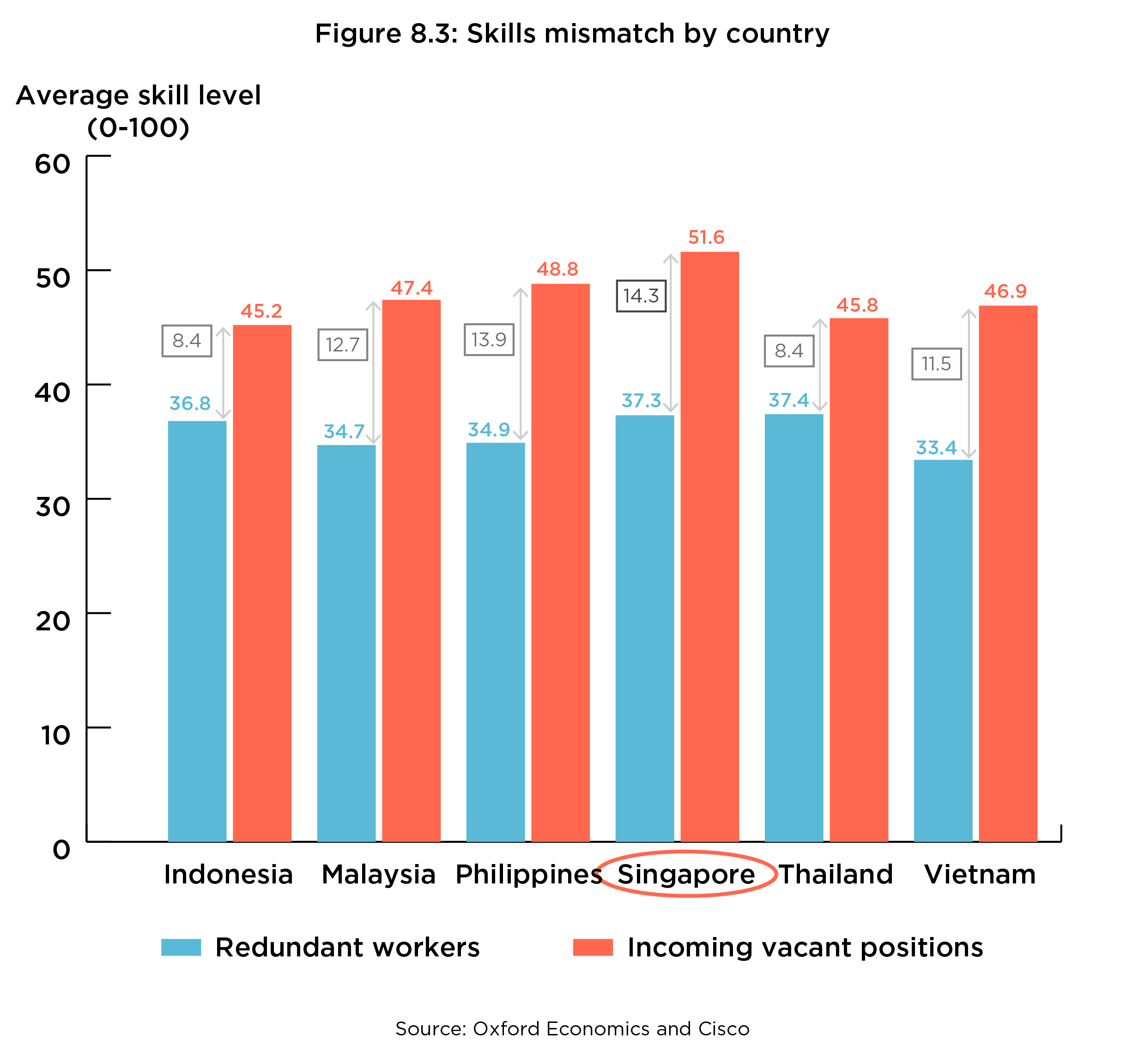

- The problem of job displacement could be attributed to the large skills mismatch as Singapore also accounts for the largest skills mismatch between the projected workforce to be made redundant and the projected incoming vacant positions with a score of 14.3 (Figure 8.3).

- However, the Singaporean government has taken note of the problem and is introducing job retraining schemes in industries threatened by technological changes such as the wholesale and maritime industries.18

Irrespective of technological readiness, ASEAN must come to terms with 4IR. It has been estimated that given ASEAN’s manufacturing sector-dependent economies, successful adoption of 4IR could potentially bring about productivity gains amounting from US$216 billion to US$627 billion by 2025.19

The onus is now on ASEAN governments to deliver customised and agile policymaking in business ecosystems characterised by greater technological adoption, more fluid labour markets and entrepreneurial behaviour that favours the establishment of start-ups.20

- Long-term strategies to mitigate the negative consequences of job displacement will require collective stakeholder efforts involving governments, businesses, educational institutions, technology providers and workers’ groups. Nimble policymaking would also involve multi-sectoral and public-private sector teams and the testing of prototype programmes in an iterative and evidence-based way.

- Pilots and experiments should be attempted, before scaling up policies that work. There are already instances of the Monetary Authority of Singapore and Bank of Thailand taking on these approaches.21

- Just as important, regulatory innovation needs to be accompanied by governance and enforcement competency, transparency and accountability at all levels to maintain business confidence in such a climate.

Prospect 4: Current impacts of global economic volatility

Prospect 4: Current impacts of global economic volatility

a) Global economic consolidation

As the previous section on Vulnerabilities shows, the region’s high dependence on extra-regional trade and investment poses a risk to its economic resilience. In addition, the current global economic consolidation phase also raises some concerns.

- The region’s export sector is likely to be strongly affected by normalisation policies—in particular China’s ongoing policy adjustment to its growth trajectory as well as previous monetary tightening policies by developed economies.

- The US Federal Reserve lowered their interest rates on July 31, 2019 for the first time since the Global Financial Crisis in 2008, to between 2.00% and 2.25%.22 In reaction to this announcement, both stocks in the US and Asia fell, signaling investor anxiety in the equity markets. However, the interest rate cut may bring greater opportunity to Asian markets. Investors in the US who may see reduced returns in their own market may shift their investment to other markets that are doing well.23 The Federal Reserve cut interest rates further in September by lowering the target range for its key interest rate by 25 basis points to between 1.75% and 2.00%,24 and again in October to a range of between 1.50% to 1.75%.25

Having said that, ASEAN’s projected 2019 growth rates of 4.8%-4.9% are higher than the projected growth rate for the global economy which was estimated to be 3.0% (Table 9.1).

However, this is not the time for complacency as almost all growth projections for ASEAN forecast a dip in 2019, before rebounding slightly in 2020.

b) US-China trade war

The US-China trade war has thrown a spanner in the works and could potentially be a game-changer for ASEAN as well as global trade and investment in the medium to longer term.26 Both the US and China are significant trading and investment partners for ASEAN. For instance, in 2017, China was the largest external market for ASEAN exports accounting for 14.1% of ASEAN’s total export value.27

In the earlier stages of the trade conflict, the concerns were about shorter-term disruptions to ASEAN’s export demand, supply chains and production networks. There were also fears that ASEAN markets could be flooded with redirected Chinese goods which could not find its way into the US due to tariff hikes. Then, as time progressed, there were some optimistic predictions.

- For example, import substitution could benefit Malaysia’s manufacturing of electronic integrated circuits, liquefied natural gas and communication apparatus.28

- Some analysts have also argued that there could be significant relocation of manufacturing bases to ASEAN from mainland China, with Vietnam as a likely top beneficiary. Earlier reports also noted that manufacturing inflows into Vietnam jumped 18% in the first nine months of 2018.29

- The same reports noted that Thailand’s net FDI rose 53% from January to July 2018 compared to a year earlier.30

- In the Philippines, net FDI into manufacturing reportedly rose from US$144 million to US$861 million for the same period.31

Pending win-win solutions that would satisfy both China and the US, the script arising from this conflict is still being written as we head into 2020. Prior to the onset of the trade conflict, some business sentiment surveys appeared to support the ASEAN economic engine.

- Based on an early 2018 ASEAN-EU business survey, 99% of respondents were expected to either expand or maintain current levels of trade and investment in ASEAN in the next 5 years, while another 51% saw ASEAN as the region with the best economic opportunity.32

- According to a survey conducted by the US Chamber of Commerce in Singapore, a good percentage of businesses indicated economic growth (67% of respondents) and the rise in the middle/consumer class (44% of respondents) as the top reasons for expanding trade and investment in the region.33

It is hard to know to what extent these survey sentiments have changed owing to the US-China trade conflict, especially in view of recent developments.

- According to an article by a consultancy,34 total US tariffs applied exclusively to Chinese goods amounted to US$550 billion, while Chinese tariffs applied exclusively to US goods amounted to US$185 billion.

- On October 11, President Trump announced that negotiations between the US and China had reached a Phase 1 agreement to be finalised in weeks. As part of the Phase 1 agreement, China agreed to purchase US$40-50 billion in US agricultural products annually, as well as strengthen intellectual property provisions and issue new guidelines on how it manages its currency. The US, in turn, agreed to delay a tariff increase originally scheduled to go into effect on October 15. The tariffs were originally set to increase to 30% on US$250 billion worth of Chinese goods.35

As it is, the trade war has already impacted the region’s 2019 growth projections, with every country having recorded slower growth for the first quarter of 2019 compared to the previous quarter. The impact of the trade war along with the identification of a slowdown in global trade ‘triggered by US-China tensions’ was ranked as the biggest risk facing ASEAN major economies based on an April 2019 study by the Japan Center for Economic Research.36

Summary

Analysts deem that ASEAN will be one of the fastest growing consumer markets in the world over the next decade and its GDP is projected to triple to US$10 trillion by 2030. The prospects of meeting such an aspiration would require addressing among other structural vulnerabilities, connectivity-related infrastructure challenges.

- It can be observed that, to a larger extent, current internal growth momentum arising from expanding economies, vibrant workforce and disruptive technologies can address some of these challenges, as would skillful means comprising multi-sectoral and multi-level solutions involving digital, logistics and regulatory solutions.

- It is also evident that the current tepid global economic climate clearly reveals the vulnerabilities of ASEAN’s very high and increasing degree of dependence on extra-regional trade and investment flows. In the next section, we further explore this dependency within the context of ASEAN economic cooperation efforts to establish an integrated regional market.

1 ASEAN, Investing in ASEAN 2013/2014.

2 McKinsey & Company, “Understanding ASEAN: Seven things you need to know”, May 2014 and PwC, The Future of ASEAN: Time to Act, May 2018. Note: Middle class is defined as the capacity to expand US$10 to US$100 in daily expenditure.

3 PwC, The Future of ASEAN: Time to Act, May 2018, and International Monetary Fund, Regional Economic Outlook, Asia and Pacific: Preparing for Choppy Seas, May 2017.

4 Asian Development Bank, “The Impact of Infrastructure in Asia: 12 Things to Know”, December 2015.

5 PwC, Understanding infrastructure opportunities in ASEAN, September 2017.

6 ADB, Meeting Asia’s infrastructure needs, 2017, and PwC, Understanding infrastructure opportunities in ASEAN, September 2017. Note: This is based on 2016 GDP estimates. ADB’s estimates cover transport, power, telecommunications, and water supply and sanitation.

7 LSE IDEAS and CARI, China’s Belt and Road Initiative (BRI) and Southeast Asia, October 2018.

8 Bloomberg, “Malaysia restarts ECRL project after cost cut,” July 25, 2019.

9 LSE IDEAS and CARI, China’s Belt and Road Initiative (BRI) and Southeast Asia, October 2018, The Straits Times, “Malaysia’s East Coast Rail Link back on track after government signs $14.5b deal with China,” April 2019, and Benar News, “Indonesia Seeks More Chinese Investment in Infrastructure Projects,” December 2018.

10 Enterprise Singapore, How Singapore companies can be a part of BRI.

11 World Bank, “Exploring the Relationship Between Broadband and Economic Growth”, 2016.

12 Google and Temasek, e-Conomy SEA Spotlight 2017 (December 2017), and 2018 (December 2018). Note: The region’s internet economy is predicted to be valued at around US$72 billion at the end of 2018—up 37% from 2017—as measured by gross merchandise value. Indonesia is the largest and fastest-growing economy in the region, with an estimated value of US$100 billion by 2025 and accounting for 40% of the region’s spending.

13 Hootsuite and We Are Social, ‘Global Digital 2019’, January 2019.

14 Google and Temasek, e-Conomy SEA Spotlight 2017 (December 2017), and 2018 (December 2018).

15 Google, Temasek and Bain, e-Conomy SEA 2019, October 2019.

16 CARI, “The potential gains from IR4.0 lie in basic needs, not the tech echo-chamber”, November 2018.

17 Oxford Economics and Cisco, Technology and the future of ASEAN jobs: The impact of AI on workers in ASEAN’s six largest economies, September 2018. Note: A displaced worker is defined as a full time equivalent (FTE) unit of labour displaced by technology under the study’s 2028 scenario assumptions, based on their occupational task profile.

18 Nikkei Asian Review, “Singapore faces biggest reskilling challenge in Southeast Asia”, December 2018.

19 McKinsey, Industry 4.0: Reinvigorating ASEAN manufacturing for the future, November 2018.

20 Nikkei Asian Review, “Southeast Asian tech hubs race to become the next Silicon Valley”, October 2018.

21 McKinsey Global Institute, Outperformers maintaining ASEAN countries’ exceptional growth, November 2018.

22 CNN Business, “The Fed cut rates for the first time since 2008,” July 31, 2019.

23 CNA, “Commentary: After the Fed’s rate cut, the impact on Singapore and growth,” August 21, 2019.

24 BBC, “US Fed cuts interest rates for second time since 2008,” September 18, 2019.

25 CNBC, “Fed cuts interest rates, but indicates a pause is ahead,” October 30, 2019.

26 Reuters, “Global growth outlook for 2019 dims for first time: Reuters polls”, October 2018.

27 ASEAN Secretariat, ASEAN Statistical Yearbook 2018, December 2018.

28 Financial Times, “Malaysia best placed to benefit from China-US trade war: Nomura”, November 2018.

29 Bloomberg, “Southeast Asia Has an Investment Boom, Thanks to the Trade War”, October 2018.

30 Ibid.

31 Ibid.

32 EU-ASEAN Business Council, 2018 EU-ASEAN Business Sentiment Survey.

33 AmCham Singapore, ASEAN Business Outlook Survey 2018.

34 Dezan Shira & Associates, “The US-China Trade War: A Timeline”, October 2019.

35 Ibid.

36 Japan Center for Economic Research, “Outlook Down Again as Trade War Impact Spreads,” April 2019.

(Note: The term “ASEAN” can refer to either the collection of economies in this region or the intergovernmental institution which was established through the ASEAN Charter of 1967 or both.)

Editorial Team: Kwong Mook Shian, Mohd Imran Said Mohd Shamsunahar, Gan Bo Ren, Nor Amirah Mohd Aminuddin, Aznita Ahmad Pharmy, Janet Leong