LIFTING-THE-BARRIERS REPORT 2015 | TOURISM

Published date: August 2015

TABLE OF CONTENT

(Click any topic to read the related section)

- 1. Tourism in the Global and ASEAN Landscape

- 2. Milestones Achieved Through the ATSP 2011 – 2015

- 3. Key Factors Impacting the Integration of Tourism into the ASEAN Economy

- 4. Recommendations for Accelerating Reductions in Key Barriers

1. Tourism in the Global and ASEAN Landscape

Oftentimes when we say “tourism”, it’s linked to vacations, plane rides, hotel stays, recreational activities, and the like. What most do not realize is that it is an ecosystem that encompasses a broad spectrum of different industries. We are all too familiar with client facing entities such as tourist transportation services – air, land, and sea transport, accommodation facilities, natural, cultural, and man-made tourist attractions, meeting-incentive-conventions-event facilities, tourist merchandising, entertainment and recreation, travel and tour operators, among others. What we often overlook are support service providers like financial services (credit card companies, banks, and investment organizations), souvenir shop suppliers, water, energy and waste management system operators, in rural areas – fishermen, boatmen, local tour guides, local communities supplying food products, materials and other services, etc. that contribute to the overall success of the industry’s operations. This is what makes tourism an avenue to channel inclusive growth.

It is well recognized that the tourism sector is a valuable contributor to global economic growth. The industry is becoming one of the fastest-growing economic sectors in the world (UNWTO Tourism Highlights, 2014). The number of international tourists have grown from 25 million in 1950 to 1,087 million in 2013 – more than a 4,200% increase – accounting for 9% of global GDP, 10.1% of global employment, and 29% of global services exports.

Tourism has the potential to bring socio-economic growth opportunities to less developed areas and their people. In ASEAN for example, a significant proportion of total tourism activity occurs in destinations outside the capital cities making it one of the few economic sectors able to bring income opportunities to less economically advantaged local communities in these destinations. Thus, the combined impacts of tourist activity makes a significant contribution towards strengthening local economies.

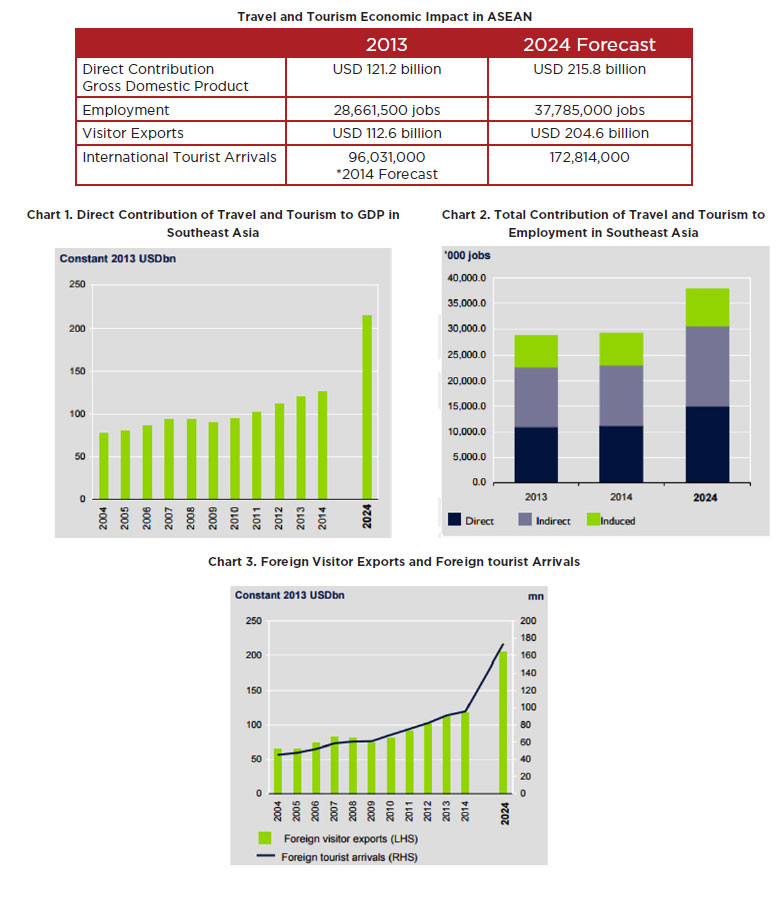

According to the World Travel and Tourism Council (WTTC 2) 2014 Travel and Tourism Economic Impact Report, in 2013, the ASEAN tourism sector contributed USD 121.2 billion to ASEAN GDP, employed around 28.7 million people, and generated USD 112.6 billion in visitor exports.

As noted by the WTTC’s report, by 2024, the sector is forecast to increase its GDP contribution by 78% to USD 215.8 billion, employment by 31% to 27.8 million and visitor exports by 82% to USD 204.6 billion. Over this period, total international arrivals within ASEAN are forecast to increase from around 96.03 million in 2013 to 172.8 million by 2024. Visitors from East Asia alone comprises roughly 25% of the total arrivals in the region. Based on 2013 ASEAN data, Japan accounts for 4.72 million arrivals, China for 12.64 million, South Korea for 4.87 million and India for 2.92 million.

The composition, size and scale, and importance of the tourism sector in ASEAN has been recognized by the ASEAN member states which have prioritized the tourism sector as a catalyst for contributing towards the goal of building the ASEAN Economic Community. A key cross cutting concern of regional plans for the development of the tourism sector in ASEAN is how to create more sustainable and inclusive outcomes for the more than 200 million ASEAN residents living below USD 2 per day.

2. Milestones Achieved Through the ASEAN Tourism Strategic Plan (ATSP) 2011 – 2015

The ATSP 2011 – 2015, directed towards optimizing the quality of ASEAN’s tourism industry through sustainable, responsible, and inclusive development, was formulated to address existing constraints in the tourism sector. The figure below illustrates how the plan laid out directions and actions in achieving its vision:

In the scorecard prepared by the ASEAN Tourism Integration and Budget Committee in 2015, it was noted that 82% of all activities under the ATSP had been completed or are still ongoing. Some of the notable milestones are in the aspects of regional marketing, product development of experiential regional products, and standards development and certification procedures for key tourist facilities, destinations, and for climate change adaptation and mitigation, and for hospitality services under the Mutual Recognition Agreements (MRA) as shown below:

While significant improvements have been made in the abovementioned areas, the absence of quantitative links and measures between these improvements and the expected outcomes anticipated in the vision for 2015 makes it difficult to assess whether these were the result of the strategy or some other factors unrelated to it. Nevertheless, granted that a substantial impact has been made, a number of major barriers remain to be dealt with that have a profound impact on the capacity of the private sector to be an effective partner in achieving a borderless ASEAN and to contribute towards ASEAN economic integration. The impact of these barriers is further discussed below.

3. Key Barriers Impacting the Integration of Tourism into the ASEAN Economy

The future integration and growth and of the ASEAN tourism sector is contingent upon developments in a number of key policy areas controlled by the member states that act either as barriers or facilitators to the integration of tourism in the ASEAN economy. Of these, the most important are: (a) removing residual barriers to trade in tourism services, investment and consumer protection; (b) removing barriers to cross border transportation services, (c) adopting a more effective approach to regional destination and product development and marketing; (d) further developing and implementing the harmonization of standards for tourist facilities and services, tourism human resources and approach to environmental protection; (e) removing unecessary restiriction on the movement of tourists across ASEAN borders and strengthening and harmonizing pproaches to tourist safety and security. The salient features of each are reviewed below.

-

A. Trade in Tourism Services, Investment, and Consumer Protection

Although much progress has been achieved to remove restrictions on trade in tourism services between the member states, key areas remain on the negative list including establishment of competing tourism businesses, tour guiding services, business set up and regulatory procedures, and other procedural requirements that in effect reduce barriers to entry of tourism enterprises between ASEAN countries. Investment regulations and support policies differ significantly between ASEAN countries making it time consuming and expensive to deploy an ASEAN-wide tourism business strategy. If ASEAN is to be marketed as a single destination like Europe for example, then existing consumer protection regulation of the meber states will need to be strengthened and harmonized.

B. Developments in Transportation Infrastructure and Connectivity

The intricacies of the topic on transportation infrastructure is already picked up by the other sector discussions. On that note, we would like to support the view of the aviation sector pertaining to creating a single aviation authority and regulatory body for ASEAN. This will also be beneficial to the tourism industry as it will facilitate the movement of tourists within the region.

What we want to further emphasize is how vital transportation is to the growth and development of the tourism sector. Several pillars of the Travel and Tourism Competitiveness Index Report by the World Economic Forum (WEF) are dedicated solely to infrastructure. The development of convenient, safe, secure and affordable intra-ASEAN travel either by air, sea, or land will make it easier to attract higher spending international visitors and distribute the benefits as widely as possible to promote more inclusive socio-economic development in the region.

Transportation infrastructure is not just limited to airports and seaports. It also involves the quality of thoroughfares leading to the airport, available modes of transportation to places of interests, road signages, and all the other accessories in making travel seamless, convenient, and easy to undertake. Except in cities such as Singapore and Kuala Lumpur, a comprehensive transportation system continues to be a need in the region. Most cities do not yet have a transportation hub. Nor do they have mass transportation systems that allow tourists to conveniently transfer between ports of entry, such as the airport, and the city center. Improvements in soft infrastructure are also equally important.

The development of a more convenient, safe, secure and affordable intra-ASEAN multi-modal travel system will make it easier to create multi-country packages. One example is how easily tourists can go from Singapore to Malaysia and vice versa. A 5 hour bus ride can already get you to the heart of Kuala Lumpur. Flight options are also available. Hence, creating twin city tours featuring these two destinations is a breeze. Ideally, this arrangement should be replicated for the rest of the region.

C. Harmonization of Cross Border Formalities – Customs, Immigration, and Quarantine and Security

Under the current visa policies, some nationalities require visas to enter the ASEAN region. It is estimated by WTTC studies that the ASEAN region stands to gain 6 to 10 million international tourist arrivals by 2016 if appropriate improvements are made 1. 1Based on 2013 data, this would provide between USD 7 billion and USD 11.7 billion in additional visitor exports within ASEAN at 2013 prices. Similarly, improvements to ease customs, immigration and security processes and procedures would further boost market demand and induce further investment on the supply side.

While in principle, ASEAN residents can travel to any other ASEAN country without visa requirements, much has yet to be done to fully implement this long standing agreement. In practice, some countries continue to require additional formalities similar for visa requirements for ASEAN residents moving across their borders. Moreover, as the largest potential high-yield markets for ASEAN comprises non-ASEAN residents – East Asians, Europeans, Middle Easteners, North Americans, and South Asians (e.g. India) – that generate at least two to three country arrivals per visit. The confusing mix of visa requirements and visa prices, notwithstanding visa exemptions applied to some countries by some member states, is a major barrier to expanding these high-yield markets. In this context, it is noted that the concept of a Single ASEAN visa has been promoted within the ASEAN economic cooperation fremework. This would be similar to the Schengen visa wherein a visitor would only need to secure an entry visa from one of the 10 member states which in turn grants him/her access to the entire region. This would substantially ease mobility of intra-ASEAN travel as well as inter-regional travel by high-yield non-ASEAN residents and make significant contributions to ASEAN’s integration and socio-economic development – particularly inclusive economic development. However, because of security, procedural, and financial concerns, in spite of the enormous benefit relative to the cost, there has been little enthusiasm on the part of the member states to forward this initiative.

The challenge now is to formulate and implement policies designed to move ASEAN towards becoming a border-free region. It goes without saying that needing to acquire a visa will limit the goals of the development of tourism which is to ensure the increase of tourist arrivals and tourist spending for it to be a major industry in ASEAN especially in promoting inclusive growth. In this context, there is a need to hold a high level summit to address cross border barriers in tourism and to develop new strategies and programs to facilitating the movement of high-value non-ASEAN tourists to and within the region.

D. Alignment of Standards and Mutual Recognition of Certification for Tourism Products and Human Resources

A key component of the AEC is for mutual recognition of the certification of product and human resource standards across ASEAN. In this context, there is a need to introduce mutual recognition of certification for tourism product standards, and to implement and expand the coverage of the existing MRAs to include qualified manpower and other new occupations within the ASEAN region.

In effect, facilities in all ASEAN destinations – restrooms, hotels, attractions, etc. should be at par with each other. The same approach should apply to manpower. A front office operator in Myanmar who has acquired certification can work the same job elsewhere within ASEAN. Having skilled employees across the board subsequently aids in achieving the AEC goals of the free flow of skilled labor and help raise the competitiveness of ASEAN as an economic region.

E. Approach to Destination and Product Development and Marketing of ASEAN As A Single Destination

As indicated earlier, through the ATSP, product development and promotion plans and programs designed to promote ASEAN as a single destination among ASEAN residents and non-ASEAN markets are being implemented. The objective is to tie destination and product development, investment and promotion together and to equally market and sell all the destinations and products in the region. It is considered best to bundle multi-country tour products/destinations based on themes (i.e. nature based, culture, heritage, cruise, adventure, meetings and events, etc.). However, existing subregional destinations such as the Mekong sunregion have not been integrated into the ASEAN tourism framework and only a handful of tour operators are involved in developing, marketing and operating multi-country destinations and products even as a large volume of medium and long haul tourists organize their own multi-country tour programs. Ideally, given the size of this business opportunity, much greater paticipation and cooperation needs to be given to developing, marketing and operating multi-country destinations and products.

Moreover, as what transpired from the roundtable discussion, there is little or no awareness about the campaign “Feel The Warmth” for Southeast Asia”. It has been identified that there is a lack of marketing, per se, in both online and offline platforms. The identity of each country is more profound compared to the region as a whole even though most international visitors – especially those from medium and long haul markets are visitong two or more countries in the region.

These are some of the key barriers that need to be removed or reduced in order to realize the goal of the economic integration of tourism in the ASEAN economy. As indicated in the WTTC study, the impact of reducing these barriers could be substantial in terms of visitor exports and employment generation, especially in the less economically developed destinations of the region such as the Mekong Subregion and the Brunei-Indonesia-Malaysia-Philippine subregion in East ASEAN that together account for most of ASEAN’s poorer population.

4. Recommendations for Accelerating Reduction in Key Barriers

These are some of the key barriers that need to be removed or reduced in order to realize the goal of the economic integration of tourism in the ASEAN economy. As indicated in the WTTC study, the impact of reducing these barriers could be substantial in terms of visitor exports and employment generation, especially in the less economically developed destinations of the region such as the Mekong Subregion and the Brunei-Indonesia-Malaysia-Philippine subregion in East ASEAN that together account for most of ASEAN’s poorer population.

It was noted during the Roundtable Discussion that the participants had little, if any knowledge about the ATSP 2011-2015 or its successor currently being crafted for the period 2016 – 2015. It was noted that in the formulation of the first ATSP 2011 – 2015, the private sector’s participation was only partial and the inputs were only taken into account midway through the formulation process rather than at the beginning of the process. In other words, the private sector is regarded as an actor in the tourism sector and not a key driver of its development.

This situation has been repeated in the case of the formulation of the ATSP 2016 – 2025 and reflects the weakness of tourism private sector to organize and deal with regional issues. As a result, the public sector organized under the ASEAN Secretariat has taken the lead. Strengthening the private sector’s capacity to organize, advocate, and finance its stance to removing key barriers to the integration of tourism within the ASEAN economy and full participation as a driver of tourism economic integration in the ATSP 2016 – 2025 formulation and implementation process is thus a primary recommendation of this report.

Private sector involvement in the formulation and implementation of strategies, programs and projects to address key barriers and to help fast track implementation is discussed below.

-

Research and advocacy on the need for further reductions in barriers affecting transportation, cross border, and mutual recognition of certification standards

It is within the private sector’s purview to introduce concepts, programs, and ways to improve the status of tourism related undertakings. With all the barriers in mind, there is a need to mobilize the full range of private sector organizations operating in ASEAN including all major carrier groups, major hotel chains, travel operations firms, shopping, entertainment and leisure facility operators, financial institutions, and tourism real estate developers to come together as one to resolve the pertinent issues.

Strengthening the Capability of the Industry in ASEAN Regional Affairs

In order to echo a stronger voice, there is also a need to strengthen the representation and role of existing regional private sector organizations like the ASEAN Tourism Association (ASEANTA) in the affairs of the region. ASEANTA is a non-profit tourism association comprising both public and private tourism sector organizations from within ASEAN. This was formed more than 40 years ago with the goal of helping shape tourism development growth and policies. However, despite its decades of presence, the association is not yet where it hoped to be. Its representation remains narrow and ideally should be expanded to include more transportation providers in the air, sea and ground arena including new online service providers, major theme attractions, parks and entertainment, MICE and gaming operators, financial institutions such as the major banks, investment houses with large tourism portfolios and credit card firms, real estate developers and tourism management companies, online travel agencies and booking firms, etc.

The private sector is potentially a strong partner to the public sector tourism organizations in ASEAN to help develop strategies and implement breakthrough projects through its representation and lobbying capabilities. The strengthening of private sector representation and regional presence and capability will propel the industry to that of a viable partner with the public sector in developing and implementing strategies to reduce the barriers to the integration and growth of ASEAN tourism.

Inter and Intra-regional Transportation

One of the key barriers is transportation. Much greater attention needs to be given to the harmonization of safety and security policies and regulations and moving to a single international transportation market. The private sector, as the main provider of transportation services in the region, given its ability to lobby the political process, can play a crucial role in working to remove barriers in this area. In fact, the “Pathfinder Initiative” to bring about specific policy changes at the member state level in line with regional priorities for integration is a good example of how the private sector can work to help reduce barriers.

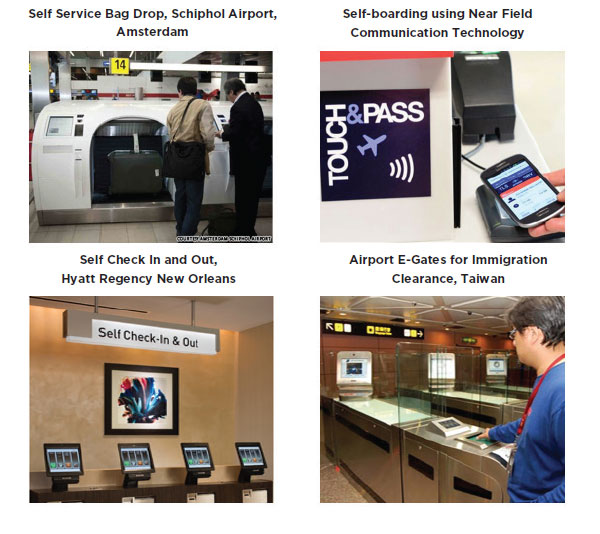

As indicated below, there have been numerous technological advancements pioneered by the private sector that are already in use in the different parts of the world to make it easier and more convenient for tourist to move travel and move across borders.

Ideally, an ASEAN Single Visa must be made available for tourists, starting with the nationals of ASEAN Dialogue Partners China, Japan, South Korea, and India. As previously mentioned, 25% of arrivals in ASEAN comes from these countries. In 2014, the four countries had 157 million outbound travelers combined with China now ranking as the biggest international tourism spender in the world. With this, the region stands to gain tremendously from an influx of tourists from these neighboring markets.

Moreover, if the Single ASEAN visa cannot come into fruition just yet, countries are moving into visa-free access. As an example, Indonesia has just recently waived visa requirements for tourists from 30 more countries including United States, Germany, New Zealand, United Kingdom, among others, allowing them to stay in the country for up to 30 days. It is with the objective of welcoming more tourist traffic and activity that is beneficial to its economy. This is one approach that the private sector can lobby to their respective government agencies to achieve border-free travel. By improving international openness, the rankings of the member countries will fare better in the WEF Competitiveness Index.

In line with this, the private sector can also lobby for the introduction of technological advancements such as the Advance Passenger Information System (APIS).

This should help to resolve the area of security as it allows the border control to pre-process arrival and departure manifest data on all passengers and crew members. The information can then be checked against warning lists and used for immigration processing, security, and customs processes. It also inadvertently fast tracks passenger processing upon arrival.

Quality Standards

As it is, there is a great disparity in terms of the standards of goods and services in the region especially in less developed member states. The MRAs need to be fully implemented to ensure supply of a quality pool of manpower in the region. The qualifications and skill set required can be best identified by the private sector. Later on, training and monitoring of the level of accomplishment can be undertaken by the same body.

Marketing ASEAN as a Single Destination

As mentioned, there is a greater need to involve the private sector in the formulation and implementation of plans and programs for ASEAN tourism. Thus, there is a need for the private sector to take a stronger position going forward. This can be effected through creation of public private sector working groups at the national and ASEAN level and private sector participation in rapid assessment task forces, working group meetings, surveys, and facilitation of required focused group discussions, among others.

In terms of travel services, the private sector is best placed to contribute as it is at the front line of product packaging, pricing, promotion, distribution, and operation. The private sector knows what is happening on the ground as it comes face to face with the tourist at all points of the tourism supply chain. The value that the private sector can add will be important in setting realistic long term strategic directions, action plans and programs.

ASEAN brand awareness is a prerequisite to the successful marketing of ASEAN as a single tourism destination. The tourism players in the region – both public and private – need to work together for an aggressive and sustainable branding campaign, including clear brand messaging and the aid of publicity tools such as TV, radio, print, and social media. Given that the “Southeast Asia: Feel the Warmth” is not well-known, there is a need to boost marketing efforts in all areas. Ideally, there should be an easily accessible market orientated website that will be a database of all the regional destinations and places to visit, possible activities, basic information, and the like on all the 10 member states of ASEAN. All the multi-country itineraries and packages should also be available there. In principle, it should like the European Union’s counterpart, be a “one-stop-shop” for everything there is to know about ASEAN tourism for potential visitors. The content will be derived from consolidated inputs of both public and private sectors in the region, linked to booking search engines and social networking platforms and managed by a professional website manager. This way, all destinations – even from the lesser known countries, have an equal chance of being promoted. The web site should also be easily accessible to the market by keying in familiar phrases such as “visit southeast asia”, “travel in southeast asia”, “vacations in southeast asia”, “exploring southeast asia”, etc. At present, however, the market would need to know about “ASEAN” in order to key “visit ASEAN” or “explore ASEAN”, knowledge that most of the market does not have and that would require changing the world’s perception of ‘Southeast Asia’ to ‘ASEAN’ – a very costly and needless exercise. Europe promotes itself on a website called “visiteurope.com” not “visitEC.com” or as in the case of ASEAN.

Based on 2013 data from UNWTO, the combined number of international tourist arrivals from the ten countries will put the region on the top and will be the most visited destination in the world. At the same time, ASEAN will fare second next to the United States in terms of generated international tourism receipts should this be the case. This recognition will only be possible if the region will be marketed as a single destination.

As private sector, we should be at the forefront of tourism planning initiative. There should be a level of trust between the public and private sector to make this work.

One feasible scheme to get this done is to create a Public-Private Sector ASEAN Tourism Working Group to discuss, agree, jointly implement where appropriate and monitor and evaluate strategies, plans and, programs designed to reduce barriers and promote ASEAN as a single destination.

Further Identify What Is Needed From the Public Sector To Raise the Competitiveness of ASEAN as a Global Destination

We have already highlighted the importance of public and private partnerships in policy making and implementation. Again, the private sector being in the forefront of the tourism industry, there are some concerns and issues that can only be dealt with in cooperation with the public sector. Regulations, taxation, and infrastructure are just some of the matters that are mainly under the government’s purview. If the direction of both sectors are in coordinated, it will be easier to actualize plans that would benefit the economic integration of the ASEAN tourism industry. Through effective collaboration in the formulation of the ATSP, this is possible.

These are just some of the recommendations on how barriers in the tourism industry can be lifted and its integration within the ASEAN economy enhanced. In the dawn of the ASEAN Integration, it is but timely to address these hindrances and fully realize what it means to have a united region.

Sources

• United Nations World Tourism Organization. (2014). Tourism Highlights.

• World Travel and Tourism Council. (2014). Travel and Tourism Economic Impact.

• World Travel and Tourism Council. (2014). The Impact of Visa Facilitation in ASEAN Member States.

• World Economic Forum. (2014). Travel and Tourism Competitiveness Index Report.

• ASEAN Tourism Strategic Plan. (2011).

• International Civil Aviation Organization and International Air Transport Association. (2014).

![]()

RELATED REPORTS