ASEAN Economic Progress: Drivers

Published on 30 September 2019

Introduction

ASEAN was formed in 1967 with five members namely Indonesia, Malaysia, the Philippines, Singapore, and Thailand with a combined GDP of US$23 billion. In 2016, ASEAN’s GDP was estimated to be US$2.6 trillion, making the region the sixth largest economy in the world if ASEAN was a country. In half a century, ASEAN’s membership has doubled, total population has increased by 3.5 times, while its GDP has expanded by 120-fold.1

Wealth has also increased. GDP per capita of Indonesia, Malaysia, Singapore, and Thailand grew by at least 3.5% annually from 1965 to 2015.2 Cambodia, Laos, Myanmar, and Vietnam (CLMV) recorded even higher rates of GDP per capita growth i.e., at least 5% from 1996 to 2016.3

Diverse economic growth patterns

The diversity of the region’s economies is best captured by the difference in their GDP levels. The three largest ASEAN economies of Indonesia, Thailand and Malaysia collectively made up more than 64% of the region’s total GDP in 2018 (Figure 1.1).

However, Singapore and Brunei rank the highest when it comes to the region’s GDP per capita as the countries lead the group by 5 and 3 times the regional average respectively in 2018 (Figure 1.2).

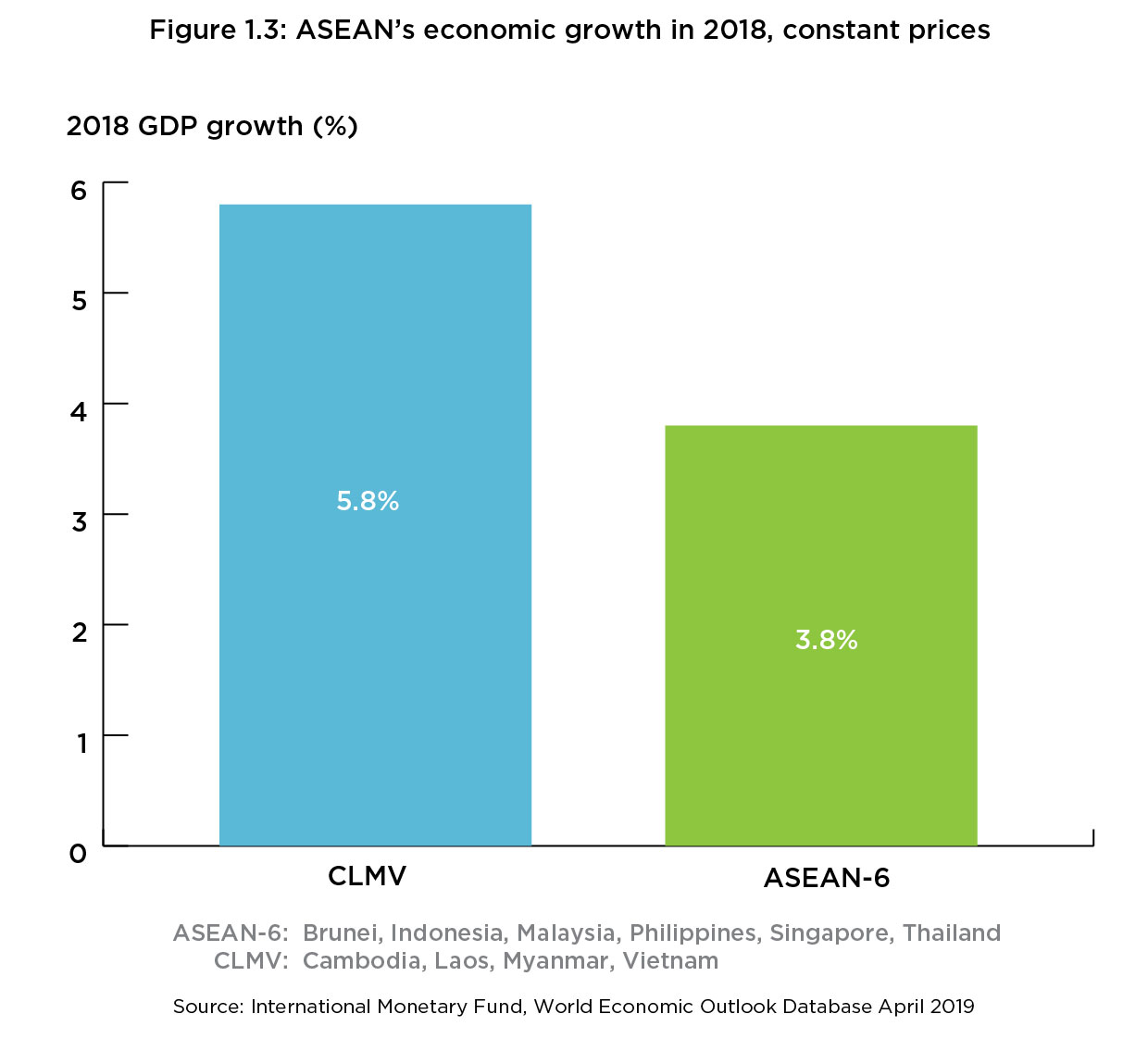

Although CLMV economies have among the lowest GDP per capita in ASEAN, these countries are also the fastest growing, with an average GDP growth rate of 5.8% in 2018 compared to 3.8% for the ASEAN-6 economies (Figure 1.3).4

Driver 1: Impressive growth in the labour force

Driver 1: Impressive growth in the labour force

Sufficient resources and an efficient capital transformation machinery gave rise to a large labour force in ASEAN which further propelled the region’s growth. In the span of 20 years (from 1995 to 2015), ASEAN’s labour force grew from 224 million to 326 million, a staggering rate of close to 46%, in part due to the inclusion of the CLMV (Cambodia, Laos, Myanmar and Vietnam) countries5 (Figure 2.1).

According to projections, ASEAN’s labour market is expected to expand considerably, i.e., become the third largest labour force worldwide behind China and India by 2030.6

Driver 2: Rising productivity

Driver 2: Rising productivity

Accompanying labour force growth has been the rising labour productivity. From 2000 to 2016, ASEAN’s annual labour productivity has increased by about 69.1%, significantly higher than the global average growth of around 20%7 (Figure 2.2).

However, while the growth in ASEAN’s labour productivity has been impressive, it is prudent to note that global labour productivity levels were 3.6 times ASEAN levels in 2016 based on the right vertical axis in Figure 2.2. As we will see in the next section, ASEAN’s lower labour productivity level will be an area of concern going forward if it continues to persist.

Driver 3: High gross savings

Driver 3: High gross savings

ASEAN, in particular the ASEAN-5 countries,8 has benefitted from consistent high gross national savings rates as compared to the global average. This trend can be observed when comparing the ASEAN-5 and the global average gross national savings rates from 2000 to 2018 (Figure 2.3).

At a national level, as a percentage of GDP, Singapore saved 51% between 2000 to 2015, with equally impressive rates for Malaysia (40%), Indonesia (32%), and Thailand (30%) in the same period (Figure 2.4). According to McKinsey Global Institute, even as far back as during the late 1990s, Malaysia’s Employees Provident Fund accounted for 8% of domestic disposable income, while Singapore’s Central Provident Fund accounted for 15% respectively. 9

Driver 4: Low government debt

Driver 4: Low government debt

Some aspects of the macroeconomic environment have also been especially supportive for the ASEAN-5 countries in the post-1997 Asian Financial Crisis era10.

- In the decade since 2000, government debt as a percentage of GDP in the ASEAN-5 showed a general decline. The rates were also generally below that of emerging markets and much lower than those of developed economies11 (Figure 3.1).

- In 2016, for example, the ASEAN-5 markets enjoyed government debt of 39.4% to GDP, lower than emerging markets (averaging 46.8%) and an even starker contrast to the G7 nations (averaging around 119.4%).

Driver 5: Healthy levels of foreign reserves

Driver 5: Healthy levels of foreign reserves

Additionally, healthy foreign reserve levels in ASEAN economies provided the necessary buffer to weather exchange rate and capital account uncertainties, especially in recent years.12

At over 80% of GDP (2017), Singapore enjoyed the highest levels of foreign reserves in the region (Figure 3.2).

In comparison to Thailand that had healthy foreign reserves at 62% compared to GDP, Indonesia, with a much lower foreign reserves of 12% against GDP, showed stronger growth with Indonesia managing to catch up with Thailand’s 18% growth between 2014 and 2017 (Figure 3.3).

Driver 6: Global FDI magnet

Driver 6: Global FDI magnet

With growing economies, large and conducive labour market conditions, greater domestic capacities to pay for goods and services, increasing local consumption and supportive macroeconomic conditions, ASEAN has attracted significant FDI flows over the years.

- Total FDI inflows into ASEAN countries totalled US$135.6 billion in 2017, marking a 54.7% increase since 2011 (Figure 3.4). Such a trend is the result of yearly increases with the exception of 2014-15.

- ASEAN’s appeal as an FDI destination is further cemented by the fact that In 2018, ASEAN’s FDI inflows even surpassed China by a staggering US$15 billion (Figure 3.5).

The fact that ASEAN’s FDI inflows increased by 4.96% to US$154 billion in 2018 is impressive given that global FDI flows actually declined by 13% in the same year (Figure 3.6).

- However, FDI into ASEAN appeared to be highly concentrated in a few economies. Using 2017 data as an example, Singapore, Indonesia and Vietnam received some 73% of total ASEAN FDI inflows that year (Figure 3.7).

- At 46% of total FDI inflows, Singapore was the region’s largest FDI recipient in 2017, despite a decline to US$62 billion that year from US$77 billion in 2016. FDI into CLMV (Cambodia, Laos, Myanmar and Vietnam) economies rose by 21% to reach US$23 billion in 2017, making it the third consecutive year of growth in CLMV’s share of FDI inflows into ASEAN. Vietnam alone received over 60% of inflows to the CLMV countries.13

Summary

A virtuous cycle of savings, foreign investment and labour productivity have helped feed the domestic mechanisms that supported the growth of many ASEAN economies. Macroeconomic conditions such as healthy levels of government debt and high foreign reserve levels have also been supportive. These conditions have provided a fertile platform for the region to attract global FDI. Nonetheless, as the next section shows, accompanying such growth momentum are emerging vulnerabilities that would need to be addressed to sustain further growth.

1 PwC, The Future of ASEAN: Time to act, May 2018; ASEAN Secretariat, Celebrating ASEAN: 50 Years of Evolution and Progress, A Statistical Publication, July 2017

2 Since 1965

3 McKinsey Global Institute, Outperformers maintaining ASEAN countries’ exceptional growth, September 2018

4 PwC, The Future of ASEAN: Time to Act, May 2018 and ASEAN Secretariat, ASEAN Statistical Highlights 2018, October 2018

5 PwC, The Future of ASEAN: Time to Act, May 2018

6 PwC, The Future of ASEAN: Time to Act, May 2018

7 Ibid

8 The ASEAN 5 countries comprise Indonesia, Malaysia, the Philippines, Singapore, and Thailand

9 McKinsey Global Institute, Outperformers maintaining ASEAN countries’ exceptional growth, September 2018

10 ASEAN-5 comprises Indonesia, Malaysia, Philippines, Singapore, Thailand

11 With the exception of Singapore, many ASEAN economies especially those from the emerging economies recorded low and declining levels of government debt since 2001

12 Ibid

13 UNCTAD, ASEAN Investment Report 2018. Note: Generally, FDI into CLMV flowed into infrastructure, manufacturing, real estate, and finance.

(Note: The term “ASEAN” can refer to either the collection of economies in this region or the intergovernmental institution which was established through the ASEAN Charter of 1967 or both.)

Research Director: Hong Jukhee

Editorial Team: Kwong Mook Shian, Mohd Imran Said Mohd Shamsunahar, Gan Bo Ren, Nor Amirah Mohd Aminuddin, Aznita Ahmad Pharmy