LIFTING-THE-BARRIERS REPORT 2014 | FINANCIAL SERVICES & CAPITAL MARKETS

Published date: December 2014

TABLE OF CONTENT

(Click any topic to read the related section)

- 1. Introduction

- 2. Why is an integrated financial and capital market important to ASEAN?

- 3. AEC initiatives lay the foundation for financial and capital market integration

- 4. What can we learn from the EU experience?

- 5. What are the key challenges to the financial and capital market integration?

- 6. So what can we do in light of these challenges?

- 7. Final Thoughts

- 8. Post Roundtable Considerations

1. INTRODUCTION

Financial and capital markets have an important role in sustaining growth in an emerging economy, especially one like ASEAN. While bank lending is important to finance the economic activities across all types of enterprises, capital market provides a more diverse source of long-term finance for investments and infrastructure development with strong socio-economic benefits such as roads, public transport or energy. And while well-functioning domestic capital markets are a good starting point, an integrated ASEAN financial and capital market would bring more significant benefits for its members by improving the efficiency of capital allocation and helping to attract foreign investment.

The ASEAN member states recognised the importance and laid out a foundation for capital market integration in the ASEAN Economic Community (AEC) Blueprint 2015 and the Implementation Plan 2015, as well as the ASEAN Financial Integration Framework (AFIF). The intention is to achieve significant progress in building a regionally integrated market where companies or governments can raise capital across ASEAN markets, investors are able to invest freely across borders, and banks can enter and operate across the region. On the surface these stated goals are an excellent objective, though the actual implementation is difficult considering complexities such as a multi-currency environment, significant disparity in development standards, and disparate fiscal & monetary policies among the ASEAN nations.

While modest achievements toward the integration of financial and capital markets have been made, a number of challenges remain to be addressed. This includes policy and regulation alignment, pan-ASEAN supervision and dispute resolution, as well as the underlying market infrastructure, just to name a few. It is imperative that policy makers come together to work towards the common vision, execute in an orderly fashion, install adequate safeguards and ensure benefits are shared. In addition, the industry could step forward with specific industry-led initiatives – such as a shared market utility – to help progress the agenda.

2. Why is an integrated financial and capital market important to ASEAN?

ASEAN, a region with a population of more than 600 million, represents one of the most vibrant economies in the world. By GDP it is one of the largest economies globally, and a significant trading bloc with exports of US$1.27 trillion in 2013, not too far behind China at $ US$2.21 trillion, the EU at US$2.17 trillion and the US at US$1.58 trillion. The region’s total trade, at over US$2.5 trillion, is equally impressive.

Large corporates, as well as small and medium enterprises (SMEs) are the region’s growth engine. Prioritising their development is critical for promoting inclusive economic growth. They create domestic demand through jobs, bring innovation through competition, and drive international trade. The rapid growth of the private sector translates into rising funding needs and requires robust financial and capital markets to provide the required growth capital.

Access to an efficient capital market is necessary to support growing ASEAN financing needs

Bank lending to date remains the main source of financing, especially among smaller, less developed economies. However, there is already a supply-demand gap today, and it will only grow with Basel III further constraining banks’ ability to lend in the future.

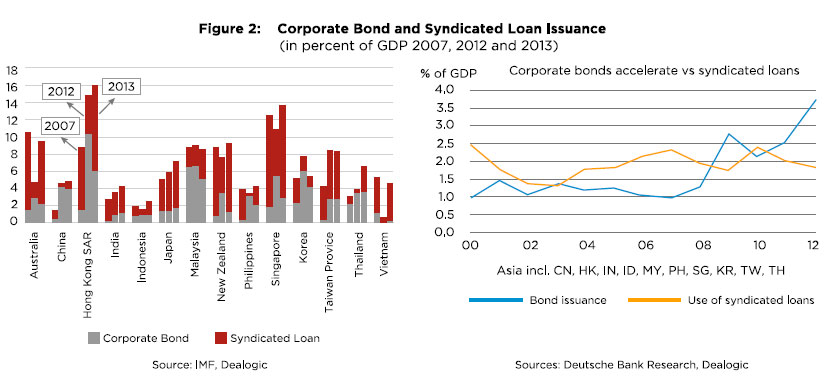

The capital market is a good alternative source of funding, particularly for corporates. Corporate bond demand across ASEAN is on the rise, as shown for instance in the graphs below comparing corporate bond vs syndicated loan issuance.

At the same time, capital flows to corporate bonds are currently constrained by a lack of pan-ASEAN lending standards, coordinated reporting standards, and central credit agencies. If addressed, investor trust in the ASEAN markets would increase and open the market to a broader set of global institutional investors.

For SMEs the challenge to secure adequate financing is even greater. A survey of SMEs in Malaysia1 shows that financing demand (of approx. US$2.54m on average) significantly outstrips the actual funds raised (approx. US$0.64m on average). It also shows hesitation towards the use of capital markets instruments such as bonds or equity. Key reasons include complexity and cost.

Lenders generally have been hesitant to extend credit to SMEs due to poor consistency of financial/credit reporting standards, lack of credit ratings and concerns related to cross border ownership rights.

Adequate market structures are required to support the requirements for growth capital. Access to a larger pool of finance, ideally at a lower cost of funds, would go a long way to support the sustained growth of the industry. An integrated, efficient capital market would facilitate this, while offering numerous other benefits to market participants as laid out below.

3. AEC initiatives lay the foundation for financial and capital market integration

AEC 2015 Blueprint for Capital Markets Integration

The AEC 2015 Blueprint was adopted in 2007 with the goal of establishing ASEAN as a single market and production base, with free flow of goods, services, investments and skilled labour, and freer flow of capital. It also sets out a broad general framework to strengthen ASEAN capital market development and integration by 2015. Specifically the blueprint calls for freer movement of capital, easier capital raising and open opportunities for portfolio investment across ASEAN, allowing for greater cross border access to investors and issuers, and helping to broaden the investor base and range of products.

The ASEAN Capital Markets Forum (ACMF) which comprises of capital market regulators from all ASEAN member states developed an implementation plan to achieve the above objectives. Key initiatives include:

- A mutual recognition framework for fund raising, product distribution, investment and market access

- An ASEAN exchange alliance and governance framework

- New products and ASEAN as an asset class

- The strengthening of the bond markets

- Alignment of domestic capital markets development plans to support regional integration

- Reinforcement of ASEAN working processes

A number of achievements have been made, such as the ASEAN Trading Link or the ASEAN framework for cross-border offering of collective investment schemes (CIS) which allows retail investors to buy and sell funds issued in Singapore, Malaysia and Thailand.

However, the liberalisation of financial services has been constrained by concerns regarding financial stability and perceived risks related to financial policies & sovereignty of individual countries. There are significant differences in the levels of development of financial and capital markets, as well as the extent to which global standards are observed. Individual nations try to find the right balance between national interests versus shared goals and collective benefits.

ASEAN Financial Integration Framework

The ASEAN Financial Integration Framework was established to provide a general approach to financial liberalisation and integration. It calls for instance for ‘Qualified ASEAN Banks’ (QABs) to be able to enter and operate in banking markets across ASEAN, and for the elimination of discrimination against foreign banks.

While aiming for financial liberalisation by 2020, the process is contentious and gradual. Guiding principles and frameworks are in place, but implementation plans are yet to be defined. A study from the Asian Development Bank (ADB) projected that only a semi-integrated market will be achievable with some compromises:

- Only a small number of QABs will gain access to the banking markets of all member states

- Some market restrictions still remain at the discretion of the host country

- Progress in the sub-dimension of regulatory harmonisation will be slow

Slow progress is still better than no progress and the benefits of an integrated financial and capital market should provide sufficient reason to push beyond individual countries’ interests.

4. What can we learn from the EU experience?

A great number of economists and politicians have drawn the analogy of the ASEAN Blueprint for financial integration with the experience of the European Union (EU) in hope of learning from both the positive outcomes as well as mistakes that may be avoided. While EU integration is still a work in progress, the general consensus is that pan-regional integration creates a number of benefits for all members of the Union that far outweigh the potential negatives, when properly executed.

Benefits of the EU financial and capital market integration

While the single currency provided a major impetus to the integration of financial markets, benefits go well beyond currency integration. A 2014 study2 by the Bertelsmann Stiftung in Germany found that increasing European integration within the EU single market has had a positive impact on economic growth in all founding countries. The single market’s impact on growth varies considerably from country to country and depends for example on how well trade relations are developed, or how well the national economy has been able to adapt to economic developments within the EU. As a general rule, the deeper and tighter the integration, the more economic benefits are realised.

Other benefits include

- A level playing field for financial services providers across member states through mutual recognition of banks through a “single passport”

- More efficient allocation of credit, aided by lower cross border spreads through free flow of information and capital

- A Single Rulebook which creates a unified regulatory framework for the EU financial sector, such as Basel III, the Single Supervisory Mechanism (SSM), the Single Resolution Mechanism (SRM) including the Single Resolution Fund (SRF)

The strong rule of law and good governance helped the EU significantly by building trust in the banking system and capital markets.

Integration flaws surfaced during the financial crisis of 2008

Despite the long journey toward EU integration, not everything was perfect and the financial crisis of 2008 created significant challenges. The EU created a currency union without fiscal union or sufficient monetary policy coordination. Smaller, peripheral nation states adopted lenient policies to attract foreign investment which inflated the banking sector beyond supporting fundamentals. A lack of coordination by Eurozone governments created macroeconomic imbalances of divergent wages and prices, and there were serious failings in the cooperation, coordination, consistency, and trust between national supervisors. Nationally-based supervisory models have lagged behind the integrated and interconnected reality of European financial markets in which many financial firms operate across borders, and existing supervisory arrangements have not been able to prevent, manage or resolve crises.

What can ASEAN learn from this?

Any integration brings challenges, but putting a robust framework in place from the start helps avoid future problems. So what should ASEAN take away from the EU experience?

- Disparities between ASEAN members are even larger than those faced by the EU

ASEAN needs to consider how to best address individual sovereign interests vs. common goals of the integration, and how to share benefits. Weaker ASEAN members may opt to focus on capability building before opening their financial systems if the perception prevails that developed nations have more to gain. A two speed approach may be adopted, with the stronger ASEAN-53 moving towards integration at a faster pace than the less developed BCMLV4 - Adequate safeguards need to be put in place

Safeguards will need to be clearly defined to protect against macro-economic instability and systematic risks, especially for countries in the earlier stages of financial markets maturity which may face challenges of capital outflows and competitive pressures. The rule of law should be strengthened across member nations and investor protection be tightened, e.g. through robust foreclosure, seizure, and bondholder protection laws and a binding arbitration dispute mechanism to create confidence. Centralised infrastructure can also contribute to managing risk, e.g. through central clearing counterparties (CCPs) which may mitigate systemic risks. - Regulatory and policy harmonisation is imperative

ASEAN should strive for policy and regulatory alignment regarding capital controls, economic policies, tax regimes, and banking regulations. Cross border resolution mechanisms should be put in place, e.g. through a dedicated court system and/or binding arbitration system. Also a pan-regional supervisory system will be required to coordinate initiatives and centrally deal with crisis situations.

5. What are the key challenges to the financial and capital market integration?

To reap the benefits of an integrated financial and capital market, a number of barriers need to be addressed.

Policy & Regulation

Regulatory misalignment

- Capital controls and exchange restrictions

- Differences in regulations – economic policies, tax regimes, banking regulations

- Portfolio restrictions on institutional investors

Sovereign interests vs ASEAN benefits

- No supra-national legal power or system to coordinate alignment

- Risk that centralised financial policy disproportionately benefits developed nations

- Individual countries may first focus on capacity building, then open up

Safeguard measures to be defined

- Safeguards against macro-economic instability and systemic risks

- Investor protection – current foreclosure laws, bondholder protection weak

- Protection of less developed countries – capital outflows, competitive pressures

The harmonisation of policies and legislative frameworks among member countries is key to a successful integration.

Considerations for ASEAN include: alleviating concerns regarding loss of sovereignty on macroeconomic, monetary and fiscal policy, achieving close alignment without a common currency, protecting and fostering relatively less developed economies, and mitigating system risks.

Infrastructure

A currently disjointed ASEAN infrastructure needs to be harmonised to facilitate efficient financial and capital markets. Key challenges include:

- Disparate standards that prevent efficient cross border payment and settlement; adopting common best practices and standards is time consuming

- Lack of a centralised clearing services establishment to enable efficient post-trade clearing and settlement

- Existing infrastructure capability in member countries need to be enhanced to accommodate high-speed inter-connections among all national information infrastructures

- Efforts required to ensure security measures are in place to build trust and confidence in the use of the internet and exchange of electronic transactions, payments and settlements

- Due to substantial financing needs to develop the regional architecture, ASEAN needs to explore various funding mechanisms and sources, as well as governance models for regional infrastructure

The EU offers a number of examples of regional infrastructure initiatives that help address these challenges:

European Markets and Infrastructure Regulation (EMIR)

- Mitigates risks posed to the financial system by OTC derivatives transactions (trade reporting, CCP clearing)

- Increases transparency of the derivatives market

Directive on Payment Services (PSD)

- Provides the legal framework for a single comprehensive system of pan-EU rules for payment services

- Makes cross-border payments easy, efficient and as secure as ‘national’ payments within a member state

- Improves competition and thus efficiency and cost-reduction. The Directive also provides the necessary legal platform for the Single Euro Payments Area (SEPA).

While a number of questions need to be addressed, a key consideration is the appropriate common infrastructure for a multi-currency environment.

Capital Flows

Even if capital is substantially allowed to move across borders, capital mobility is still considered not free as subject to control. The process to address current challenges with regards to capital account liberalisation is time consuming and looks to delay significant progress towards the freer flow of capital. Key challenges include:

- Cross border capital flows are subjected to control in form of permission, ex ante reporting, and quantity restrictions

- Differing currencies and lack of interest rates integration hinders the seamlessness and cost-effectiveness of FX flows

- Potential high costs for cross border transaction processing due to its complex nature

- Caution to open up due to a variety of risks and lack of measures to safeguard against instability

- Macroeconomic risks – credit growth due to capital inflows – appreciation of real exchange rate, inflationary pressure, possible affect on other macroeconomic variables such as price stability, exchange rate stability, export

- Financial stability risks – capital inflows inflating asset prices; capital outflows depleting foreign exchange reserves or currency depreciation

- Small, segmented financial markets are vulnerable to shocks and require management of reserves outside the region instead of financing the region’s development needs

- Difficulties in establishing a universal capital account liberalisation that is consistent with national agendas and economic readiness of all member countries

The EU achieved free and seamless cross border capital flows through the establishment of a common currency which was preceded by an Economic & Monetary Union (EMU) and an Exchange Rate Mechanism (ERM), requiring member states to give up monetary sovereignty.

Since an ASEAN currency union is not in sight, the question is what the next best alternative is for the region.

Cross border banking

Though cross border banking promotes regional financial stability, economic growth and capacity to withstand external shocks, it is still fragmented and hindered by regulation. Challenges include:

Significant gaps in the banking system, especially between ASEAN-5 and BCLMV

- Less developed capabilities in BCLMV; lack of competitiveness

- Risk of fund outflow from less-developed countries with poorer institutional qualities causing winner-loser scenario

Regulation preventing regionalisation

- National laws differentiating between foreign and local banks, impacting ability of foreign banks to obtain bank licenses or buy stakes in local firms

Financial stability frameworks

- Absence of sufficient financial safety nets

- Lack of integrated crisis management in the definition of macro-prudential policy

- No single cross border banking supervision and deposit guarantee system

Trade-off between national interests and ASEAN benefits

- Threats from the entry of foreign banks and being dominated

- Local banks too small to compete with regional or global peers – priority on protecting local players

The EU accomplished the liberalisation of cross border banking through a “single passport” system. It allows financial services operators that are legally established in one member state to establish and provide services in the other member states without further authorisation requirements.

Key considerations for ASEAN will be what safeguards to put in place to protect weaker members while achieving non-discrimination and get to a ‘single passport’ system.

Talent

Thanks to changing demographics and worker attitudes, digital enablement and strong growth, the workplace in ASEAN today is scarcely recognisable from what it was a decade ago. ASEAN has the fastest-growing working age population in Asia and it will add an estimated 50M people between 2010 and 2020, creating a workforce that is:

- More culturally and demographically diverse

- Highly mobile and digital-savvy

- Different in perspectives on what constitutes a fulfilling career

This complexity requires business leaders, policy makers and educational institutions to think about how to respond to the rapid changes in work, and what needs to be done in the short and long term to harness potential and not fall behind. Access to skilled talent across the region is a cornerstone of the AEC, though national interests still often take precedence.

Some of the current talent related challenges are:

Movement of labour not yet free

- Within countries, nationalistic restrictive legislation prevents organisations from being agile in their talent strategy and policies

Talent gaps

- Markets across ASEAN are struggling to get the right amount of quality talent to fuel growth

Technology gaps

- Technology and competency gaps in the workplace hinder organisations from growing with the digital revolution

Mind-set change

- Hierarchical leadership styles will need to evolve to be in line with changing Millennial expectations and technology trends

ASEAN diversity

- The political, social, cultural and economic diversity of ASEAN makes it difficult to bridge talent gaps regionally

The EU launched a number of initiatives to promote talent development and mobility, such as “Youth on the move” which provides funded study programmes, learning projects and training programmes to help young people in developing the skills needed to enter or stay within the labour market, or EURES, an EU-wide job placement and recruitment tool which centrally provides job information, advices and job-matching services to workers, employers as well as citizens who want to move and work abroad.

ASEAN businesses and political leaders need to think about how to address the business community’s increasing need for talent.

6. So what can we do in light of these challenges?

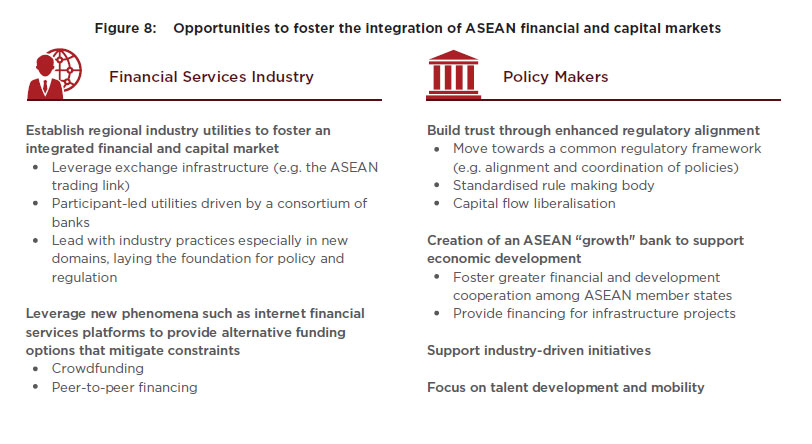

The integration of ASEAN financial and capital markets is best addressed with a two pronged approach, involving policy makers on the one hand and the financial services business community on the other.

Policy makers have an opportunity to create a greater sense of trust in the financial markets through enhanced regulatory alignment and policy harmonisation. To address major financing needs, they also could consider the creation of a pan-ASEAN “growth” bank that supports economic development similar to the recently announced New Development Bank set up by the BRICS nations.

Industry participants could come together and establish regional industry utilities that help foster an integrated capital market. This allows the market to lead with industry best practices, laying the foundation for policy and regulation enhancements. Furthermore, new phenomena such as internet financial services and alternative funding platforms could be promoted to provide funding options while mitigating existing constraints.

While an entity shared and operated by many different interest groups may prove to be daunting and inefficient, financial market utilities can turn these challenges into opportunity by creating a centralised, shared & distributed infrastructure to collectively perform a set of non-differentiating functions, using a common technology employed across multiple enterprises and thereby creating efficiencies. What makes ASEAN unique is that the existing infrastructure is less developed compared to other economies. While this may be seen as a weakness, it in fact presents an opportunity to build new infrastructures without having to cope with interoperability challenges of legacy system integration faced by more mature markets. Building a cohesive utility based infrastructure now will save time and money.

So what is a market utility? Broadly speaking, a true utility would be an industry or exchange led initiative which is member or consortium owned, and can be a for-profit or not for-profit entity. Such a service would entail shared governance, investment, cost savings, profits/losses (if applicable), and fees for data paid by members and non-members alike. Examples of financial services utilities include those related to post trade processing and/or data including reference data, client data & documentation, client on-boarding, corporate actions, LEI, etc.

Benefits of Utilities

There are several benefits of a shared utility, with the most obvious being cost savings as non-differentiated functions are shared through a single shared data or processing centre with positive implications for manpower, storage, and computing power economics. Another less obvious benefit is the “golden source” nature of the shared data. Because all participants are using the same sets of data, the number of failures and amount of human intervention is decreased. Additionally, this also affords the industry to lead the creation of best practices for regulatory reporting requirements for items such as KYC, anti-money laundering, and client record retention rather than responding to sometimes confusing and misguided regulatory mandates.

The concept of market utilities is not new and has been in existence for over half a decade. The overarching theme among the examples below is that significant opportunities exist for utility led initiatives across a broad spectrum of financial services that would serve a multitude of purposes from interconnectivity to regulation, and beyond.

Other market led initiatives often arise from a perceived need or unmet demand in the market. For example, the Intercontinental Exchange (ICE) was originally created as an internet based platform for energy trading, fostering transparency, efficiency, and lower cost in what was at the time a highly inefficient market. Over time the ICE expanded both in terms of membership and products, today comprising 11 exchanges, 5 clearing houses, and over 12,000 listed contracts and securities. The question for ASEAN policy makers is if they are open to fostering innovative market-driven solutions and create regulatory guidelines for such enterprises that are beneficial for all, or hinder efforts over concerns related to national interests or oversight.

Purely from a policy (or government) led perspective ASEAN could look at the recent announcement made by the BRICS5 countries which launched the New Development Bank, formerly known as the BRICS Development Bank, as an alternative to the Western-dominated World Bank and International Monetary Fund (IMF). Unlike the Asian Development Bank’s initiatives that focus on infrastructure financing, the New Development Bank will also include a US$100 billion Contingent Reserve Arrangement (CRA) as a cushion against balance of payments and/or liquidity crises through swaps agreements among member countries.

ASEAN could consider options such as these as part of a holistic approach to financial market integration. Thereby minority interest would have to be protected and benefits for lesser developed countries ensured. In addition it needs to be discussed how oversight is provided and what boundaries need to be established.

Internet financial services platforms as alternative source of funding

Platforms for alternative funding, such as peer-to-peer lending and crowdfunding, can facilitate access to capital for smaller, less established firms or in less developed markets.

They can provide a positive economic impact through the rebalancing of investible assets (i.e. local investment rather than savings which often are channelled into reserves invested outside of the region), and may drive a greater participation of retail and institutional investors by offering new investment opportunities.

To allow such platforms to flourish, access to common reliable credit ratings will be an important factor for investors to judge the risk they take. Furthermore it is imperative to create a framework and standards which are clearly articulated and backed by the rule of law across boundaries, avoiding differing rules by jurisdiction. For example, access to crowdfunding was meant to be enhanced in the U.S. by the Jumpstart Our Business Startup (JOBS) Act by easing certain securities regulations related to capital raising without the need for meeting costly listing requirements.

ASEAN policy makers should discuss if alternative financing options should be allowed to thrive, and if they feel comfortable bringing non-financial services providers into the system. ASEAN banks should consider creating such platforms in conjunction with policy makers as there is no doubt regarding the long term trends for alternative funding platforms gaining acceptance. The question is what level of disintermediation risk banks are willing to accept.

What can the policy makers do to support the regional integration?

In an “ideal” world, the ASEAN member states would standardise macroeconomic policies, align legal & supervisory regimes, create a framework for bank and investor dispute resolution, create a central governing body with a ‘single passport’ system for cross-border operations, and institute safeguards against macroeconomic stability and systematic risk issues. While this is not feasible in the near/medium term, steps can be taken to demonstrate a resolve toward ASEAN financial integration.

Opportunities for harmonisation and coordination of regional regulations exist in areas of mutual interest that would benefit all ASEN members, including:

- Creation of a working committee to draft rules to be adopted across ASEAN

- To develop and agree on a framework for a governing body for professional licensing

- Standardised central bank reporting of interest rates, account balances, capital accounts, and currency targets

- Creation of a regulatory authority, or regulatory framework, similar to that of the U.S. Securities and Exchange Commission (SEC) to harmonise standards for financial disclosure and reporting among companies seeking access to the capital markets

- Creation of a binding arbitration board for cross-border dispute resolution with each ASEAN nation represented in an equal manner

7. Final Thoughts

While the ASEAN vision of integrated financial and capital markets is courageous and ambitious, political opposition and inadequate institutional infrastructure hinders the effective implementation. The “ASEAN way” of consensus building, while having its strengths, makes the 2015 Blueprint deadline for a more robust capital market integration challenging. However, the direction is the right one and considerable progress has been made. Policy makers and business leaders should continue to strive for the realisation of the ASEAN vision and work tirelessly to build an integrated financial and capital market.

8. Post Roundtable Considerations

On the 8th September 2014, a select group of ASEAN financial services professionals met to discuss next steps to advance the integration of financial and capital markets. As a result of a productive discussion, a two-pronged approach was suggested:

- Industry-led initiatives where industry participants come together to define and drive specific industry agenda through the application of best practices, especially in areas where there is no clear regulation, such as cross interaction and arbitration. Examples may include a reference data utility, KYC/AML, or similar common functions that are jointly set up.

- Initiatives driven by policy makers, such as a dedicated working group to drive financial and capital markets integration, with focus on expedited implementation.

Industry-led initiatives

An industry-led initiative would entail a number of market participants from across ASEAN coming together and jointly create or share a specific common function or utility to collectively perform non-differentiating functions. Possible examples may include a common reference data utility (e.g. for securities reference data or client reference data), a joint approach for determining credit ratings for SMEs, or a utility covering KYC and client onboarding. Such initiatives, or utilities, could facilitate the integration of ASEAN through the creation of best practices and cross border solutions, which in turn can help shape regulation. Additional benefits may include cost savings, standardisation, improved efficiency and automation.

Policy makers can contribute by recognising such initiatives as a potential foundation for the enhancement of policies and regulations, and should establish an environment in which such cross border transformation can thrive.

Initiatives driven by policy makers

The roundtable participants took the view that integration progress could be significantly improved through the establishment of a small, dedicated team within the government machinery with the sole purpose of achieving integration goals. This team could be part of the ASEAN Secretariat, may pair up government agencies and regulators with industry participants, and proactively drive integration based on an agreed agenda and action plan. It should also recommend and implement quick-wins expediently without waiting for any pre-set schedule. As outlined in this report, a number of opportunities for quick wins exist which can be addressed and implemented without having to address fundamental differences between ASEAN member states. This includes standardised reporting, the creation of an arbitration board for cross-border dispute resolution, or the development of a framework for professional licensing.

In contrast to the pursuit of a broad agenda by each individual member country, such an approach – especially when clearly showing initial success – has the potential to instil much needed confidence within the industry that the AEC 2015 and 2020 goals will be met on time.

In conclusion we believe that such a two-pronged approach – with industry and policy maker participation – must be pursued to realise the vision of the ASEAN Economic Community Blueprint.

Endnotes

1 ADB, Capital Market Financing for SMEs: A Growing Need in Emerging Asia, Jan 2014

2 Bertelsmann Stiftung

3 Indonesia, Malaysia, the Philippines, Singapore and Thailand

4 Brunei, Cambodia, Laos, Myanmar, Vietnam

5 Brazil, Russia, India, China, South Africa

![]()

RELATED REPORTS

- AN ANALYSIS OF THE ASEAN PRIORITIES ON IMPROVING GOOD GOVERNANCE

- LIFTING-THE-BARRIER REPORT 2013 FINANCIAL SERVICES

- LIFTING-THE-BARRIER REPORT 2013 CAPITAL MARKETS

- LIFTING-THE-BARRIER REPORT 2015 FINANCIAL SERVICES & CAPITAL MARKETS