Economic Snapshot: ASEAN Focus December 2017 | Economic & Currency Outlook

Published on 20 December 2017

by Michelle Chia & Lim Yee Ping, Economists, CIMB Equities & Economic Research

Economics Focus

2018 Outlook: Making hay while the sun shines

- Global growth to sustain in 2018. This may be as good as it gets though, given the ageing recovery, and the reduced scope for upside growth surprises.

- As the global economy becomes self-sustaining, policymakers are likely to accelerate the removal of monetary accommodation.

- ASEAN economies stand in good stead to weather the transition, having built up buffers against the risk of tightening global financial conditions.

- Exports lent a crucial crutch to growth in 2017 but internal sources of growth are expected to pull their weight in 2018.

Global: As good as it gets?

Tailwinds driving global economic momentum this year look set to extend to 2018, driven by improvements in household and business confidence. As the global recovery becomes entrenched and navigates the late-stage of the cycle, monetary policy is set to turn hawkish, not just among the advanced economies but also selectively in the emerging markets. The key risk here is if monetary policymakers misjudge the strength of the economy and over-tighten as a result, or inflationary pressures and financial imbalances emerge more intensely than expected.

ASEAN: Leaning against the wind

The good news is that ASEAN economies have worked on improving their buffers against external vulnerabilities through the accumulation of foreign exchange reserves, well-capitalised banking systems, macro-prudential curbs to contain the build-up of financial imbalances as well as fiscal and structural reforms. Expect 2018 to be a year of transition for ASEAN, as domestic engines of growth take the reins from external drivers.

Malaysia: Shifting gears in 2018

After a dip in form, Malaysia’s economy has rebounded strongly in 2017, driven by brighter prospects in commodities, external demand for manufactured goods, and a reversal in domestic consumption and investment. With the low-hanging fruits harvested this year, it’s time to apply the elbow grease in 2018, with a renewed focus on improving domestic growth engines and external macro buffers. Nonetheless, there is no need to fret about the moderation as it takes GDP growth back to trend, to 5.2% in 2018 from 5.9% in 2017. Against this backdrop, the policy interest rate is set to rise by 25bp in 1Q18.

Indonesia: Firmer recovery in GDP growth

Expect economic growth to accelerate mildly in 2018, from a growth rate that has hovered around 5% per annum over the past four years impacted by fiscal reforms and tight monetary policy post-taper tantrum and sharp declines in commodity prices. A gradual recovery in private consumption could be in sight, amid firmer commodity prices, higher minimum wage growth, a low inflation environment and falling lending rates. Investment growth should continue to ride on the improved investment climate and infrastructure spending. Nonetheless, tax revenue collection will likely remain the key constraint to government spending.

Singapore: Canary in the coalmine to continue singing

Singapore’s GDP growth will accelerate to 3.6% in 2018 from 3.5% in 2017, aided by a broadening out of gains from the external sector and manufacturing to domestic demand, services and construction. Expect the improving growth picture, the uptick in core inflation and monetary policy tightening in advanced economies to nudge the Monetary Authority of Singapore into tightening policy by strengthening the S$NEER in Apr 2018.

Thailand: Don’t count Teflon Thailand out

Staying true to its moniker, Thailand has weathered near-term challenges, despite political uncertainties and the year-long mourning for the late king. A strong uplift in global demand and recovering commodity prices filtered through to higher exports and tourism receipts. Going forward, the transition to a self-sustained recovery will have to rope in households and businesses. A turnaround in farm and non-farm incomes portends further gains in private consumption, while key public investments projects are poised to take off. Thailand’s real GDP growth is forecast to quicken to 4.0% in 2018 from 3.9% in 2017.

GLOBAL OUTLOOK IN 2018

Healthy expansion even as recovery gets long in the tooth

Base case: Cyclical pick-up in the global economy to sustain into 2018 as recovery extends into the late stages of the economic cycle. This may be as good as it gets though, as the scope for upside surprises has reduced. Global trade growth is expected to moderate from a cyclical peak in 2017 but remain supportive of export-driven economies. Prospects in advanced economies are still positive next year, especially in the US and Eurozone, while developing economies pass the baton from export-led expansion to domestic sources of growth.

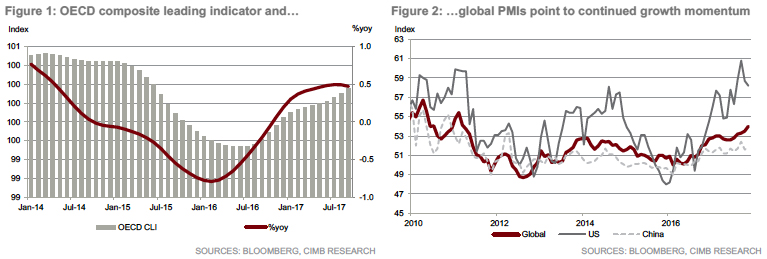

The global recovery this year has been noticeable in its breadth and synchronisation, with both advanced and developing economies gaining momentum. Forward-looking data like the OECD composite leading indicators and global purchasing managers’ indices suggest that the near-term outlook for the global economy remains positive. Heeding the recent data outturn, it is believed that the global recovery has further to run as the calendar flips over to 2018, driven by continued growth in investments, trade and industrial activity. The IMF is projecting global GDP growth to inch higher from 3.6% in 2017 to 3.7% in 2018 as consumer and business confidence turns more upbeat, generating greater capacity to consume and invest after years of pent-up demand during the recovery from the global financial crisis and the Eurozone sovereign debt crisis.

Fears that the global economy was on a slippery slope towards trade protectionism following the election of US President Donald Trump proved unfounded as global trade volumes flourished in 9M17 (+4.4% vs. +1.4% in 2016) on the back of recovering ‘animal spirits’ and still-accommodative global financial conditions. A year that began with legitimate concerns of escalating trade tensions could end with global trade growth outpacing global real GDP growth (3.6%) for the first time since 2011. Industrial activity has been a beneficiary of the global reflation as global industrial output rose to 3.0% yoy in 9M17 (+1.9% in 2016), driven by strong demand for electronics, especially from the US, where demand surged 32% in 2017. The World Semiconductor Trade Statistics estimates that global semiconductor sales increased 20.6% to US$409bn in 2017 but that growth is expected to moderate to 7% in 2018 as inventory shortages for memory components ease and the smartphone product launch cycle tapers off after several blockbuster releases this year, including the iPhone X. The swell in manufacturing extended to autos, machinery and equipment and industrial capital goods.

The recovery in commodity prices also bolstered trade and the economies of resource-based producers. Overall commodity prices are expected to stabilise in 2018, with the World Bank projecting price increases of 4.1% for energy (+23.6% in 2017) and 1.2% for agriculture (-0.6% in 2017) but reductions for metals (-0.7% vs. +22.4% in 2017).

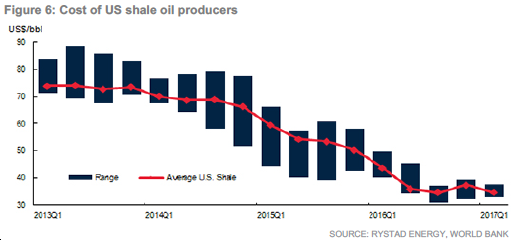

The oil and gas (O&G) sector, which was a key source of capital-intensive investments when oil prices were high, is estimated to have boosted capex for exploration and production by 8% in 2017, after sharp declines of almost 40% in 2015-16. With oil prices stabilising amid an extension of production cuts by Opec and non-Opec producers until Dec 2018, O&G capital commitments are forecast to rise 4% in 2018. The International Energy Agency projects production to result in a narrow excess supply of 200k bpd in 1H18, before reverting to a deficit of 200k bpd in 2H18, driven by rising US crude production. Oil prices are likely to remain range-bound between US$50/bbl and US$60/bbl as the cost of production for US shale producers, which increasingly influence global marginal supply, continues to fall.

While the trade environment has turned more constructive, trade protectionism remains a credible threat. Conditions or election promises that underpin US President Donald Trump’s rhetorically aggressive stance on trade remain unaddressed: 1) the stark gap between the US’s trade position, which recorded a wider deficit of US$463bn in 10M17 (vs. a deficit of US$414bn in 10M16) and its trade partners, 2) renegotiating terms in existing trade agreements (like NAFTA and South-Korea-US Free Trade Agreement), and 3) tariff and anti-dumping disputes.

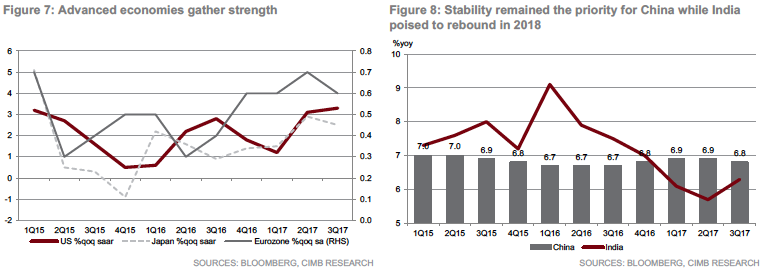

The recovery from the global financial crisis is starting to get long in the tooth. As of Dec 2017, the current expansion in the US economy is the third-longest on record at 102 months, with only the cycles that peaked in Mar 2001 (120 months) and Dec 1969 (106 months) faring better. The US economy is on track to expand 2.2% in 2017 and 2.3% in 2018, according to IMF estimates. The growth outlook for 2018 is bolstered by the stimulus that comes with the potential passage of the tax reform legislation, and quickens the passing of the torch from monetary policy to fiscal policy. Slack in the US economy has dissipated, with the unemployment rate dipping to 4.1% in Nov, below the 2007 trough of 4.4%. Meanwhile, capacity utilisation climbed to 77.1% in Nov, supported by increased demand in the manufacturing and O&G sectors. As the economy reaches full employment, wage and inflation pressures – still nascent as of now – may re-surface.

Among the advanced economies, the Eurozone has emerged as the dark horse as the IMF envisages the 19-country bloc to expand at the quickest pace since 2007 at 2.1% in 2017, before moderating to 1.9% in 2018. Updated forecasts by the European Central Bank (ECB) in Dec are even more optimistic, indicating that the collective members of the euro currency union experienced a late spurt that is set to spread into next year. The ECB projects GDP growth of 2.4% in 2017 (revised from 2.2%) and 2.3% (revised from 1.8%). A potent combination of healthier household consumption driven by stabilising labour markets, a boost in export demand and the materialisation of pent-up investments by the private sector have steered the Eurozone on a more robust growth trajectory.

The global trade recovery and a dose of fiscal stimulus are expected to lift Japan’s GDP growth from 1.0% in 2016 to 1.5% in 2017, the fastest pace in four years, and ahead of its potential growth of around 1%. Japan will continue to reap gains from supportive external conditions in 2018. Moreover, growth in capital investments points to greater business confidence that the external recovery is trickling down to domestic sectors. The step-up in activities leading up to the 2020 Tokyo Olympics is expected to catalyse construction and tourism growth.

China has been an anchor of stability in the region, with annual GDP growth tracking 6.8% in 2017, ahead of the official target of 6.5%. High-level policy directives from the 19th National Congress suggest a balance of policy priorities between pursuing growth and arresting risks from rising debt levels. An emphasis on sustaining growth at about 6.5% p.a. and the rebalancing of the economy towards consumption from investment bode well for Asian exporters. The deleveraging process is expected to remain gradual, with a focus on untangling and mitigating systemic risks in the formal financial sector and the shadow banking system.

Growth in India wobbled in 2017 in the aftermath of the demonetisation exercise in late-2016 and the introduction of the Goods and Services Tax (GST) in Jul 2017 but the country is expected to recover in 2018 on the back of robust domestic demand.

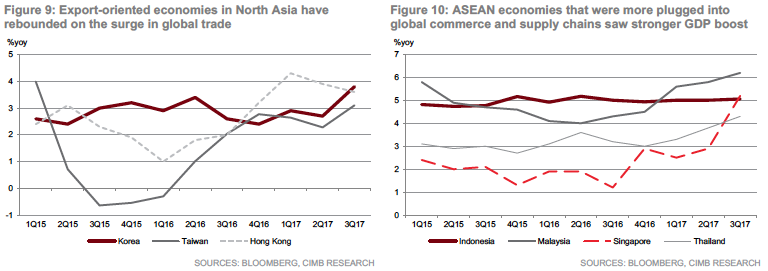

Growth in export-oriented economies in Asia generally fared better than their domestically-driven counterparts. The North Asian economies of Hong Kong and South Korea have ridden a strong wave of demand, especially for electronics-related exports. Likewise, in ASEAN, economies, like Singapore and Malaysia, that were more plugged into global commerce as well as the electronics and machinery equipment supply chain saw stronger boosts to GDP growth.

Geopolitical and event risks abated in 2017 following a spate of surprises in 2016, including Brexit, the unanticipated election of Donald Trump to the US presidency and populist anti-globalisation threats. The relatively benign outcomes to these events have encouraged markets to adopt a more even-handed reaction to event risks this year, including concerns of a Eurosceptic outcome in the French elections, the independence movement in Spain’s Catalan region, the weakened political position of Merkel’s coalition government, escalation of the nuclear threat in the Korean Peninsula and conflicts in the Middle East. Nonetheless, we believe investors should not ignore the possibility that these risks could rear their heads again in 2018.

Dialing back the monetary medicine

Base case: Goldilocks conditions of improving growth and muted inflation have allowed policymakers to engineer an orderly exit from unconventional monetary policy. As central banks close in on inflation targets and interest rates rise, global financial conditions are set to tighten but remain supportive of global growth in 2018. Of the G3 economies, the US appears the most assured that the economic recovery is strong enough to withstand the removal of monetary policy accommodation.

The Federal Reserve (Fed) delivered the last of its three guided policy rate hikes on 13 Dec, which lifted the upper end of the Fed Funds rate (FFR) target range to 1.50%. Forward guidance was unchanged, implying that the Fed expects to deliver a hat-trick of rate hikes next year, with the FFR ending 2018 at 2.25% and subsequently at 2.7% by end-2019 and 3.1% by end-2020. The passage of US tax reforms has only reinforced expectations of further US monetary policy tightening next year. The Fed has factored in the impact of the fiscal stimulus, estimated at 0.8% of GDP, revising its GDP growth forecasts for the US economy to 2.5% in 2018 from a Sep estimate of 2.1% and tweaked the outlook higher to 2.1% in 2019 (from 2.0%) and to 2.0% in 2020 (from 1.8%).

Janet Yellen presided over her last press conference in Dec and will chair one last FOMC meeting on 30-31 Jan before handing over the reins to incoming Fed chairman Jerome Powell. Expect policy continuity despite the leadership change, which will bolster confidence that the tightening cycle will progress in an orderly manner.

A re-energised Eurozone economy has compelled the European Central Bank (ECB) to initiate a slow and gradual reversal from its bond purchase programme by halving its monthly purchases from €60bn to €30bn between Jan and Sep 2018. It has kept the asset purchases open-ended as inflation has persistently undershot the policy target of 2% (ECB forecast: 1.4% in 2018 and 1.5% in 2019). This means its balance sheet will continue to grow through 2018 and put the ECB several paces behind the Fed in the monetary policy normalisation process. Likewise, the ECB is unlikely to increase interest rates in 2018 and until more progress is made on lifting inflation.

As growth gains traction and inflation picks up as the output gap narrows, the Bank of Japan (BOJ) may begin to communicate the process of stepping away from its current monetary policy stance of 1) keeping the key policy rate at -0.1%, 2) yield curve control with a cap on the 10-year bond yield at “around 0%”, and 3) asset purchases of ¥80tr a year. BOJ Governor Haruhiko Kuroda’s term ends in Apr but he is expected to be re-appointed, which provides some visibility in policy continuity.

As monetary policy reverts to more normalised settings in the advanced economies, several central banks in the emerging markets may follow suit to counter inflation and financial stability risks. The recovery in global commodity prices has raised producer prices, which, combined with robust demand and a narrowing output gap, could translate into higher consumer price inflation.

The Bank of Korea was one of the first movers, raising its benchmark 7-day repurchase rate by 25bp to 1.5% in Nov. On 14 Dec, the People’s Bank of China raised money market rates by 5bp, including for the seven-day reverse repo rate to 2.5% and for the 28-day reverse repo rate to 2.8%. At the same time, it raised rates for one-year medium-term lending facilities by 5bp to 3.25% but benchmark policy rates were left unchanged. Further hikes could come in 2018 to counter rising inflation and in line with the policy focus on domestic financial deleveraging.

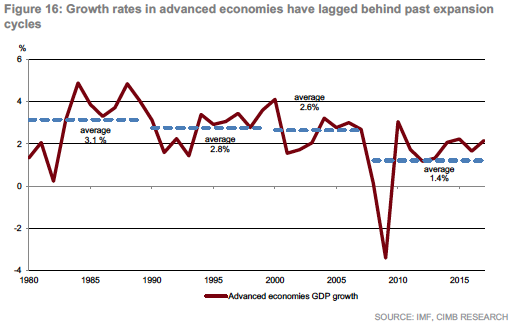

While the rise in global interest rates could result in a tightening of financial conditions from very accommodative levels, expect the current monetary tightening cycle to be more gradual than in the past as growth rates and inflation have lagged behind past expansion cycles. The key risk here is if monetary policymakers misjudge the strength of the economy and over-tighten as a result or inflationary pressures and financial imbalances emerge more intensely than expected. An unexpected tightening of financial conditions in Asia, through higher bond yields, wider credit spreads, a correction in asset prices and currency weakness, could dampen growth and undermine business and consumer sentiment. Disorderly dislocation of capital as a result of risk aversion or portfolio re-balancing in the financial markets could create negative spillovers to the real economy. Since the global financial crisis, about US$2.2tr has flowed into emerging market (EM) debt and equity, including US$1.0tr into EM Asia. The good news is that Asian economies have improved buffers against sharp capital reversals through the accumulation of foreign exchange reserves, well-capitalised banking systems, macro prudential curbs to contain the build-up of financial imbalances as well as fiscal and structural reforms.

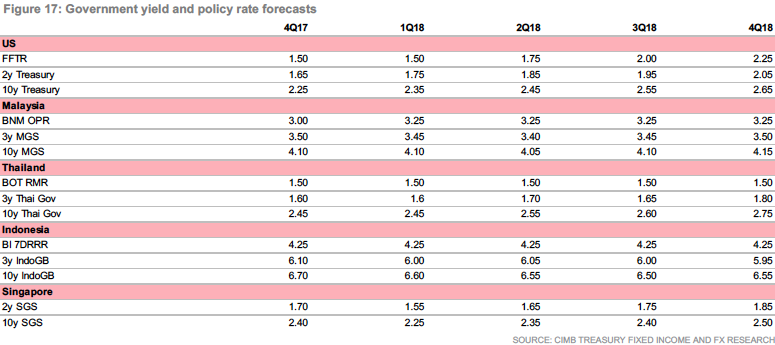

ASEAN: Interest rate and currency forecasts

In ASEAN, expect Bank Negara Malaysia (BNM) and the Monetary Authority of Singapore (MAS) to be the first movers in a tightening monetary policy. Expect a pencilled in a 25bp hike in the Overnight Policy Rate (OPR) in 1Q18 and expect MAS to allow appreciation of the S$NEER at the Apr 2018 review. The cyclical upturn has been more muted in Indonesia and Thailand. Therefore, the interest rate normalisation cycles by Bank Indonesia and the Bank of Thailand is projected to only commence after 2018. Against this backdrop, CIMB Treasury FX Research is expecting the ASEAN currencies to appreciate against the US$ in 2018, with the Malaysian ringgit forecast to see the largest gains, having been the biggest laggard this year.

Disclaimer: All rights reserved. No part of this report may be reprinted or reproduced or utilised in any form or by any electronic, mechanical or other means, now known or hereafter invented, including photocopying or recording, or in any information storage or retrieval system without proper acknowledgement of CIMB ASEAN Research Institute. The views, responsibility for facts and opinions in this publication rests exclusively with the authors and their interpretations do not necessarily reflect the views of CIMB ASEAN Research Institute.

![]()