Published on 10 January 2020.

As a region of more than 650 million people but with only 27% of its population banked, reaching out to the unbanked and achieving financial inclusion remains one of ASEAN’s goals. Digital technology, Fintech in particular, has been viewed as an enabler of financial inclusion. This was reflected in the ASEAN Chair Thailand’s 2019 theme of “Advancing Digital ASEAN” under the umbrella theme of “Advancing Partnership for Sustainability,” along with the ASEAN Business Advisory Council’s 2019 theme, “Empowering ASEAN 4.0”.

As ASEAN Chair, Thailand led efforts towards the issuance of the “ASEAN Declaration on Industry Transformation to Industry 4.0” which reaffirms the regional bloc’s commitment to advance Industry 4.0 (4IR) through the development of an ASEAN-consolidated strategy.1 In addition, several guidelines and framework related to 4IR were adopted including the ASEAN Digital Integration Framework Action Plan (DIFAP) 2019-2025; the Guidelines on Skilled Labour/Professional Services Development in Response to 4IR; and the Policy Guideline on Digitalisation of ASEAN Micro Enterprises.2

In 2019, the CIMB ASEAN Research Institute (CARI), in partnership with the ASEAN Business Advisory Council, launched the inaugural Smart Showcase Series on Fintech, with the theme “The Future of Fintech in ASEAN.”

Throughout the one-day event, around 30 speakers from Malaysia, Singapore, Thailand, and Japan showcased the latest developments in Fintech technologies in various areas including Bank-tech, Insurtech, RegTech, Lending Tech, Wealthtech, equity crowdfunding, and blockchain.

We look back at the key takeaways from the discussions and showcases held during the Smart Showcase Series on Fintech.

The key takeaways of the conference are presented in the following five parts:

(Click any topic to read the related section)

- Five Key Observations in Fintech in ASEAN

- Fintech Fast Facts

- Fintech Regional Initiatives

- Spotlight on RegTech

- Fintech Key Takeaways

1. Five Key Observations in Fintech in ASEAN

a. Rapid growth in Fintech in ASEAN

Fintech firms in selected ASEAN countries saw a higher growth rate of venture capitalist (VC) investment compared to globally.

- VC investment in Fintech firms in Singapore, Indonesia, the Philippines, Malaysia, Thailand, Vietnam and Myanmar grew 16 times between 2014 and 2018

- VC investment in global Fintech firms grew 4 times during the same period.

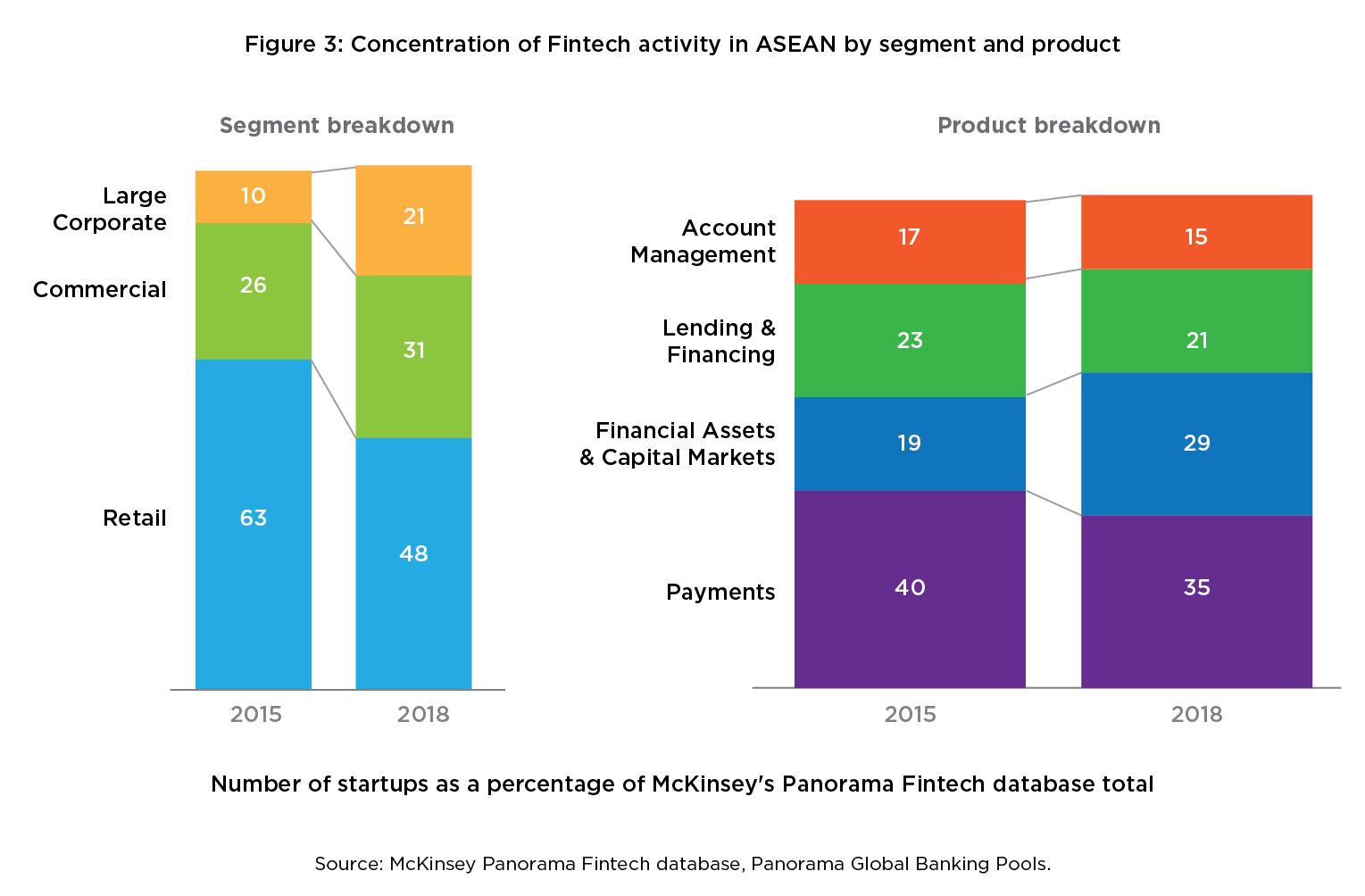

b. Shift to new areas

In terms of segment breakdown, the number of Fintech firms in ASEAN shifted from retail in 2015 towards large corporate and commercial in 2018. There was a noticeable shift in product focus from payments in 2015 towards financial assets & capital markets in 2018.

c. Equal involvement by innovators, incumbents and institutions

The ASEAN Fintech landscape was driven by the involvement of innovators (Fintech startups), incumbents (large banks) and institutions:

- During the period 2014-2018, the number of Fintech firms rose rapidly.

- Incumbents such as commercial banks spearheaded digitalisation through partnerships with innovators.

- Regulators in ASEAN have been active in creating new frameworks, with Singapore being the leader. This is notable considering the different leaders in Fintech in other regions. In the US, Fintech is driven by innovators while in Europe, the regulatory institutions have taken a proactive role in the development of Fintech.

d. Unique opportunities brought upon by Fintech’s market disruption

- Around three quarters of major Asian banks (76%) have partnered with Fintechs.

- Banks have started to build their digital banking propositions incubators

- Several digital banks have been launched including CIMB which launched the first all-digital bank in the Philippines in early 2019.

- DBS Bank launched DBS Asia X, a fintech and startup innovation hub.

- Banks are leveraging on Fintech’s advantages to reinvent themselves and target the entire digital ecosystem.

- Big platform players such as Google, Facebook, Alibaba and Tencent have started to introduce innovative fintech solutions in several areas including e-payment, P2P and consumer financing.

e. Regulatory support

- Regulatory institutes in Asia are promoting innovation in Fintech through various initiatives:

- China granted banking licences for internet platforms, e.g., WeBank.

- India has an open API that is mandated for e-KYC

- Singapore launched a US$19.8 million grant for the integration of AI by financial institutions

Source: McKinsey & Co during the presentation titled “Fintech Trends in ASEAN” at the Smart Showcase Series on Fintech on August 15, 2019.

2. Fintech Fast Facts

3. Fintech Regional Initiatives

4. Spotlight on RegTech

Money-laundering is a major concern for financial institutions. According to Sagar Sinha, VP – Head of APAC & ME Sales & Channels of RegTech firm Tookitaki, a total of US$1.8 trillion of money is being laundered globally on an annual basis. This amount, he said, is equivalent to the 9th largest economy by GDP. Money laundering has a 10% growth rate, and in 5 to 10 years’ time could surpass the GDP of the US, China or Japan.

Financial institutions need a strong anti-money laundering (AML) model that changes the way the processes of problem-solving and scoring are done. Regulatory technology, or Regtech, is a classification of technology that specifically addresses regulation and compliance issues in the financial industry.35

“Coming into the AML industry landscape, the key problems that the banks are facing is the rules-based system, reduced efficiencies from handling of the problem point of view and ever-changing regulations,” explained Sagar during his showcase on RegTech. “Banks need a strong AML based model which changes the way we solve problems with proper scoring, profiling and triage mechanism so that we can focus on real problems; effectively moving from a black box scenario to a glass box scenario where there is full explainability in the process.”

According to Sagar, an AI-powered AML model can help financial institutions reduce the number of fake alerts received and preempt financial institutions on unknown patterns which had previously not been identified. With this, a bank’s compliance team can focus on real alerts and not waste time and resources looking into hundreds of fake alerts. He added that a shared typology approach could even notify a bank of a previously unknown issue that had been detected by another bank and thus alert and prepare banks of a potential issue.

Citing Tookitaki as an example, the RegTech firm is currently utilising AI in its regulatory compliance technology and has succeeded in reducing the number of false positives by 60% and reducing transaction monitoring by 40%, making the transaction monitoring process more efficient.

RegTech is poised to increase the efficiency of current regulatory compliance programmes and reduce the risk and cost to financial institutions. Seeing itself as a sustainable compliance programme for anti-money laundering, Tookitaki aims to eliminate money laundering from the financial services industry together with the cooperation from regulators and financial institutions.

5. Fintech Key Takeaways

During the Smart Showcase Series on Fintech themed “The Future of Fintech in ASEAN”, speakers shared their thoughts and ideas through 10 showcases while panellists discussed current issues in Fintech during two separate roundtable sessions and one Ambassadorial Insights session. The outcome that emerged are as follows:

a. Fintech’s role in achieving financial inclusion in ASEAN

With less than 27% of its population banked36, ASEAN is still far from achieving financial inclusion. Innovative technology related to the Fourth Industrial Revolution (4IR) includes Fintech which has the potential to provide mobile payment solutions that cut across various income segments of society. Apart from this, Fintech can provide solutions to improve access to financing for MSMEs and promote intra-regional trade through applications.

“The AEC Blueprint 2025 puts a strong emphasis on innovation and technology is a core for ASEAN with e-commerce being one of the sectors that are likeliest to experience growth among member countries. The synergy within the Fintech industry can help to achieve the action plan of financial integration by 2025,” said Dr. Mohamed Zulkhibri Abdul Majid, Assistant Director/Head of Analysis on Finance and Socio-economic Division of ASEAN Secretariat during his speech at the Smart Showcase Series on Fintech.

In the ASEAN Economic Community Blueprint 2025, financial inclusion is one of the three strategic objectives of the financial sector integration vision for 2025 (the other two being financial integration and financial stability).

At the 35th ASEAN Summit held in Bangkok in November 2019, the ASEAN Digital Integration Framework Action Plan (DIFAP) 2019 – 2025 was adopted. The DIFAP translates the six priority areas (seamless trade; data protection; seamless digital payment; digital talent base; entrepreneurship; and coordination) of the ASEAN Digital Integration Framework into an action plan to be implemented from 2019 to 2025.

According to Dr. Zulkhibri, the financial services industry in the region is ripe for growth based on the growing usage of smartphones, rising middle class and relatively young population. Commendable work has been done by ASEAN member countries towards achieving financial integration but the gap remains. In order to bridge the gap, ASEAN member countries need to accelerate the harmonisation of regulations and standards in the areas of financial inclusion and digital financial services, he concluded.

b. Interoperability the way forward for Fintech in ASEAN

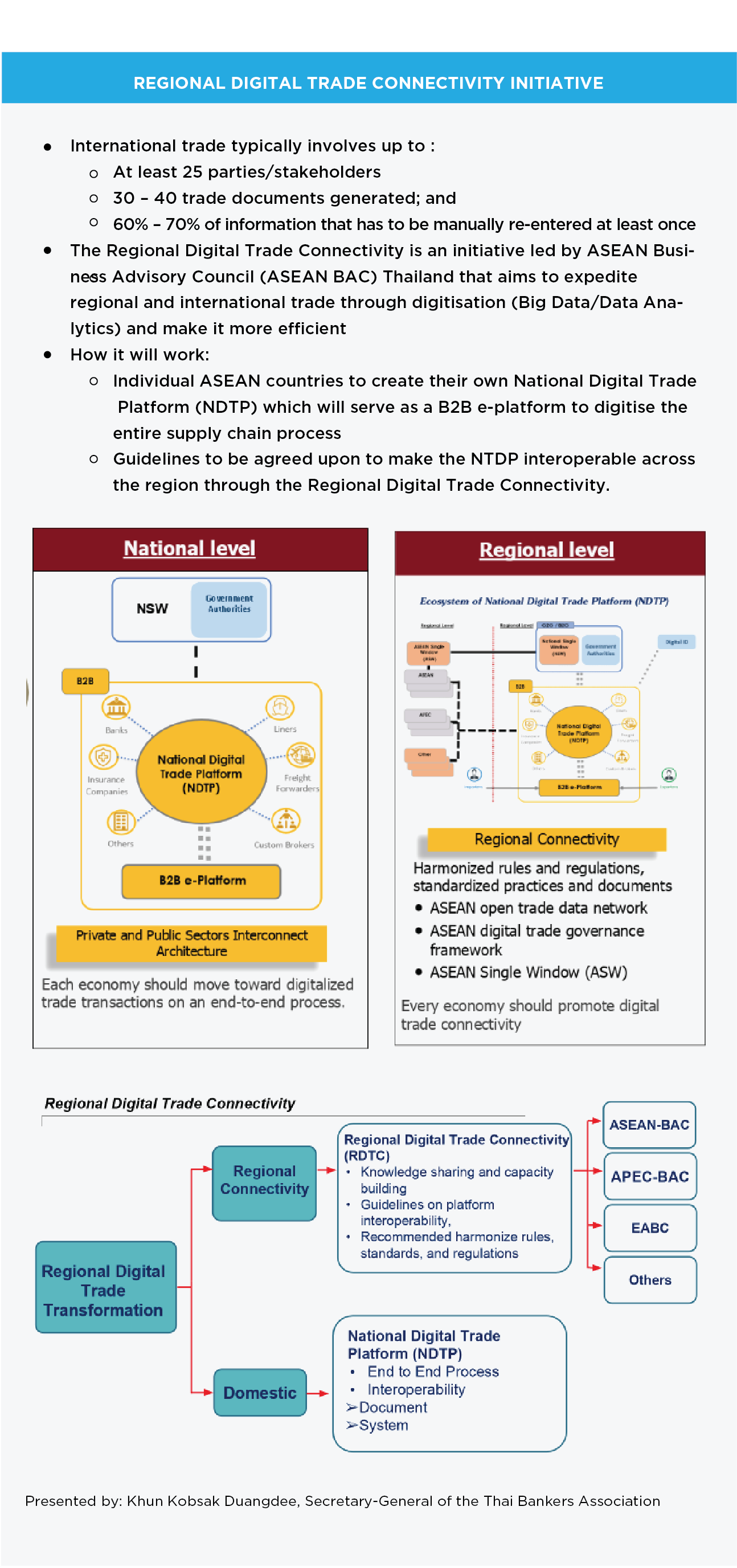

A regional cross-border payment system would bring ASEAN closer to financial integration. Recent collaborations between Thailand, Cambodia, Laos and Singapore explored the interoperability of QR codes to promote the utilisation of cashless payment schemes across the region. In the first half of 2020, the Thailand-Singapore payment system linkage is expected to go live.37

“If we want to do cross-border [payment], we need interoperability. In terms of collaboration, in Thailand and in Singapore, we have used the ISO 20022 to connect between PromptPay and PayNow,” said Paul Gwee Choon Guan, Secretary-General of ASEAN Bankers Association during the second ASEAN Roundtable Series titled “Migrating to a cashless and borderless e-Payment ASEAN ecosystem.”

Christopher Davison, Chief Executive Officer of BigPay pointed out that the current digital infrastructure is still lagging and therefore, interoperability is the key towards a digital regional e-payment system. “I think it’s beyond inevitable that people would go cashless. Interoperability would level the playing field for everyone. This is particularly important since ASEAN is diverse in absolutely everything,” he said.

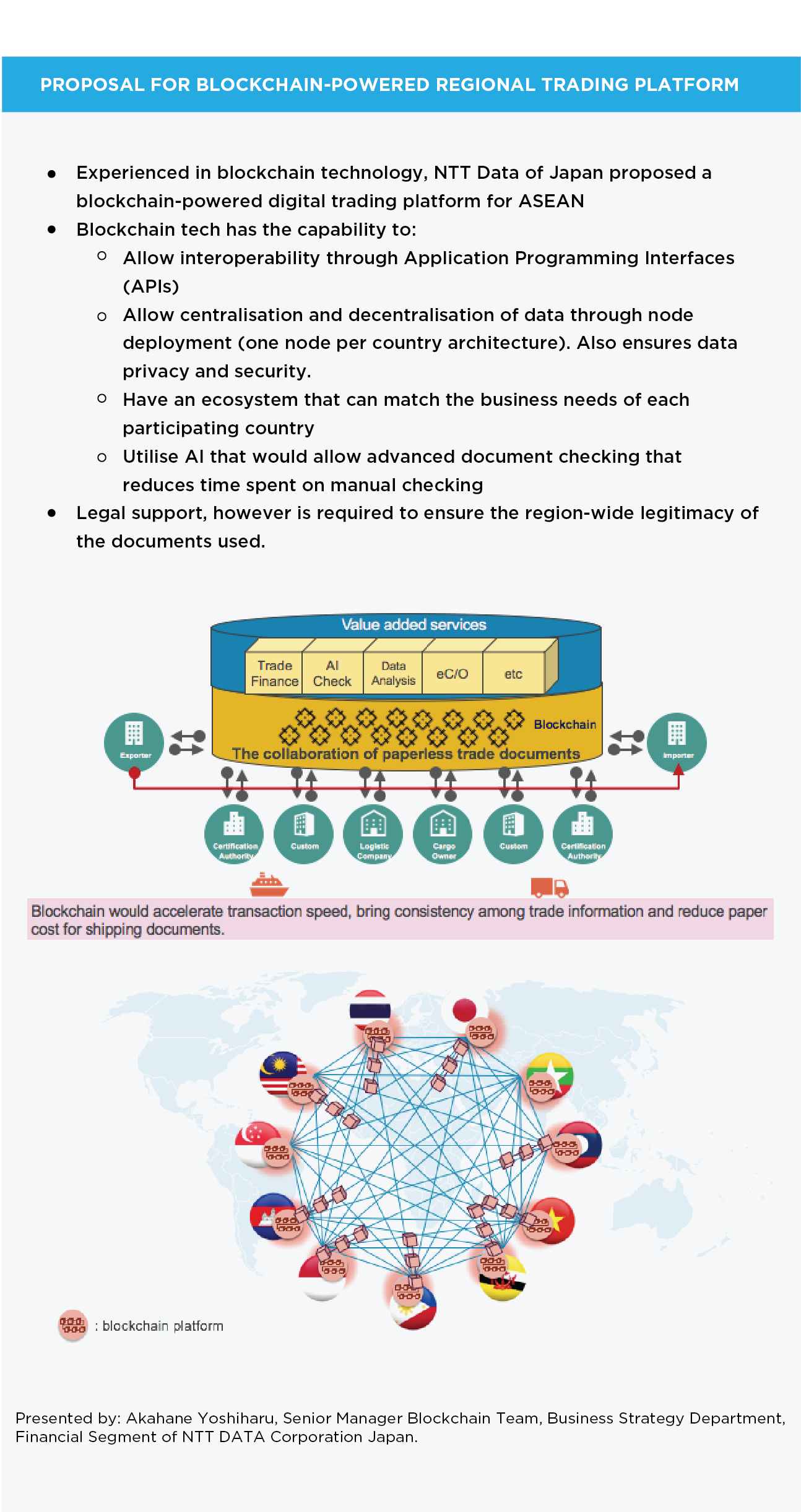

ASEAN’s diversity, however, may prove to be a challenge towards achieving interoperability, cautioned H.E. Narong Sasitorn, Ambassador of Thailand in Malaysia during the Ambassadorial Insights of the Smart Showcase Series on Fintech. Interoperability is needed not just between the countries’ systems but also between the many platforms used in Fintech, i.e., QR code, blockchain, credit card and Application Programming Interface (API).

c. Collaboration between various stakeholders

i. Fintechs and banks

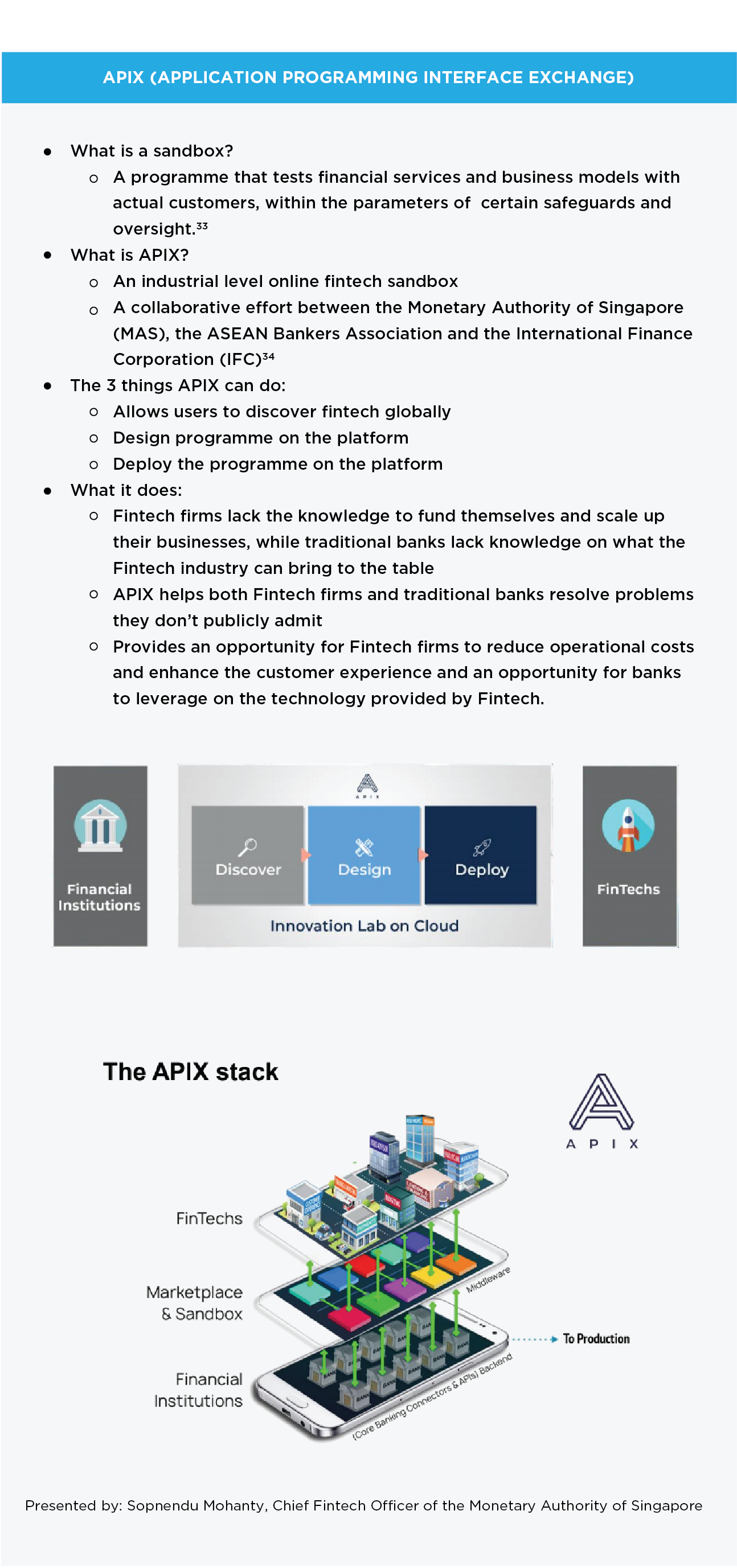

With regulatory support gaining traction in the region, collaboration between Fintechs and banks are easier to arrange/realise. “The way forward for banks is to leverage upon the technology provided by Fintechs, which can reduce the banks’ operational costs and improve customer experience,” said Sopnendu Mohanty, Chief Fintech Officer, Monetary Authority of Singapore (MAS) during his showcase on MAS’s Application Programming Interface Exchange platform.

Effendy Shahul Hamid, CEO, Group Ventures and Partnerships (GVP) of CIMB Group concurred that banks need to collaborate in order to stay relevant. “Partnering with platforms mean co-creating a product at scale and not partnering just to sell their product. The ability to co-create products with customers becomes very important because then we can scale,” he said during his showcase on Bank-tech.

“Today, banking economics in terms of its book value is not as attractive anymore. Today, those platform companies are being traded at a higher value than banking economics and if platform economics have gotten better than banking economics, then surely we have to own the economics of the banks. This is why partnerships like with Alipay and our joint-venture with Touch n Go are going to become important,” he added.

ii. Between Fintechs

For Fintechs, working with each other is vital to the development of the industry. “The key success of the Thai Fintech Association is not being disruptive but networking collaboratively so that stakeholders are not left behind. The Thai Fintech Association is more collaborative than disruptive,” explained Olarn Weranond, President of the Thai Fintech Association during the ASEAN Roundtable Series titled “Opportunities for Fintech in ASEAN – Perspectives from the ground in ASEAN”.

iii. Between regulators

Apart from collaboration between banks and Fintechs, and among Fintech firms, cooperation between regulators can strengthen the regulatory framework of the involved parties’’ Fintech ecosystem. “For example, France has signed an agreement for cooperation with Singapore between regulators and I think this is a useful agreement. We need more dialogue between regulators, ” said H.E. Frederic Laplanche, Ambassador of France in Malaysia during the Ambassadorial Insights.

In March 2017, France’s Autorité de Contrôle Prudentiel et de Résolution (ACPR), the authority monitoring banks & insurance companies and the Autorité des Marchés Financiers (AMF), France’s stock market regulator signed an agreement with the Monetary Authority of Singapore that would adhere to a framework that fosters the sharing of information relating to FinTech trends and services. Malaysia’s own Securities Commission signed a series of innovation agreements with the Australian Securities and Investments Commission (ASIC), Hong Kong Securities and Futures Commission (SFC), the Dubai Financial Services Authority (DFSA) and the Monetary Authority of Singapore (MAS) in the same year.39

d. Funding for SMEs and Fintechs

One of the areas of Fintech is LendingTech which provides alternative financing in the form of P2P lending. This area has the potential to fill the SME financing gap in ASEAN. The SME loan-to-GDP ratio of the five countries vary between 3% and 34%. In 2015, less than 60% of SMEs in ASEAN-5 countries (Indonesia, Malaysia, the Philippines, Singapore and Thailand) obtained financing from banks. Globally, the SME financing gap is estimated at US$320 billion.

“Banks have been good at serving two ends of the spectrum: one end is retail and the other end is corporate customers. Where there is a gap is the middle (the missing middle), which is where the SMEs are and the reason is that they are not as homogenous as the retail customers and they are not big enough,” explained Wong Kah Meng, co-founder and chief executive officer of Funding Societies Malaysia during his showcase session on LendingTech.

Fintech firms that provide P2P lending serve as an intermediary between SMEs and online investors. They can serve everyone from a sole proprietorship to a small listed company. The needs between SMEs and MSMEs are different as well, for example MSME require basic funding but an SME may require customised funding and accompanying ancillary services, he added. As of August 2019, Funding Societies have disbursed a total of US$551 million in loans, which is equivalent to 825,000 in the number of loans disbursed.

In the alternative lending space, peer-to-peer crowdfunding also provides funding outside of the conventional banking system. A few years ago crowdfunding used to be an initiative within a community, whereby if people liked your idea, they would lend you the money. But with the advent of the internet and social media, those who seek funding can obtain it from people they don’t even know but resonate with their idea and this has contributed to the propagation of crowdfunding in Asia, explained Elain Lockman, Co-Founder & Director of Ata Plus who spoke during the showcase on Crowdfunding.

Beyond P2P crowdfunding, equity crowdfunding (ECF) offers financial assistance to businesses that are expanding. “The beauty of these two funding is that they offer financial inclusion to these companies but also offer a potential higher return along with higher risk to investors,” she added. As of August 2019, Ata Plus has raised US$90 million for P2P Crowdfunding and US$13 million for ECF.

Among the SMEs there are many Fintech firms as well that have difficulty obtaining funding. Mohammad Ridzuan Abdul Aziz, President of Fintech Association of Malaysia (FAOM) divulged how the precursor to Grab had trouble obtaining funding. “Funding is a problem [for Fintechs], in Malaysia as well. A lot of companies run away to another country. The most classic example is Grab which started here as MyTeksi but became Grab and is now a US$14 billion in valuation company residing in another country. This is why I am promoting the use of Labuan for funding purposes in terms of matching foreign VCs and startups in Malaysia that require the funding.”

Bringing Fintechs together with VCs provides startups with an opportunity to obtain capital that would then allow them to scale up, and regulators in Singapore has gone a step further to facilitate this process.

“Two years ago, Singapore streamlined its venture capital regulatory regime to make it easier and more cost effective to set up a VC in Singapore,” said Chia Hock Lai, President of Singapore Fintech Association during the ASEAN Roundtable Series titled “Opportunities for Fintech in ASEAN – Perspectives from the ground in ASEAN”. He added, “To date, in Singapore, we have more than 300 VCs and close to 100 accelerators and incubators. So these are different avenues for Fintech firms to gain access to capital.”

e. Policy Recommendations

i. Convergence between RegTech and SupTech

With the risks faced by Fintechs ranging from money-laundering to cyberattacks, there needs to be a convergence between regulatory technology (RegTech) and supervisory technology (SupTech), said Mohammad Ridzuan.

According to him, it is not just regulators that should focus on this but also everyone in the financial industry. Many Fintech firms do not understand anti-money-laundering (AML) and know-your-customer (KYC) and Fintechs are prone to DoS (Denial of Service) and DDoS (Distributed Denial of Service) attacks.

“We should focus on RegTech, SupTech and Fintech using AI,” he said. “The most important thing is to have a collaborative mindset, not a competitive mindset. One of the things we have been proposing is a self-learning expert system using AI and we are working with some of the innovators in the market to look at how to converge [RegTech and SupTech].”

ii. TechnoEthics

The many benefits and advantages that Fintech provides also come with risks and vulnerabilities. Oversight by regulators and Fintechs themselves is one of the avenues to anticipate and prepare for potential issues. TechnoEthics has been described as a framework on the ethical use of emerging technologies, with the aim to protect the consumers against the misuse and abuse of innovations.43

In the Philippines, a code of ethics for online lenders have been created by the FinTechAlliance.ph, an organisation of fintech and digital firm, together with regulators and government agencies. The code of ethics was launched in September this year. The code of ethics aims to safeguard borrowers from abusive practices of Fintech firms such as shaming them in cases of default and late payments and to foster transparency for both creditors and borrowers.44

“Now we are engaging with the regulators to ensure the Fintech Alliance is going to become a SRO (Self Regulatory Organization) because even the SEC (Securities and Exchange Commission) has a limited view of the players in the industry,” explained Lito Villanueva, EVP and Chief Innovation & Inclusion Officer, RCBC, and Chairman, Fintech Alliance.Ph during the ASEAN Roundtable Series titled “Opportunities for Fintech in ASEAN – Perspectives from the ground in ASEAN”.

“We are also working on how to produce an e-KYC because now it is inefficient for a customer to key in their data with numerous financial players, and with the emergence of [EU’s] PSD2 (Payment Services Directive 2), which is something that will likely be embraced by Fintech stakeholders, taking these proactive measures will ensure that open banking API can be a reality. Initiatives like these will ensure more integration within ASEAN through the sharing of best practices within the region,” he added.

Similarly, the Indonesian Fintech Association (AFPI) requires its members that are P2P lenders to comply with the organisation’s code of ethics and related commitments.45

iii. Bridging the financial outreach gap

Financial inclusivity in ASEAN is an issue that most stakeholders are working towards addressing. However, financial outreach is equally important in meeting the needs of the underbanked and underserved.

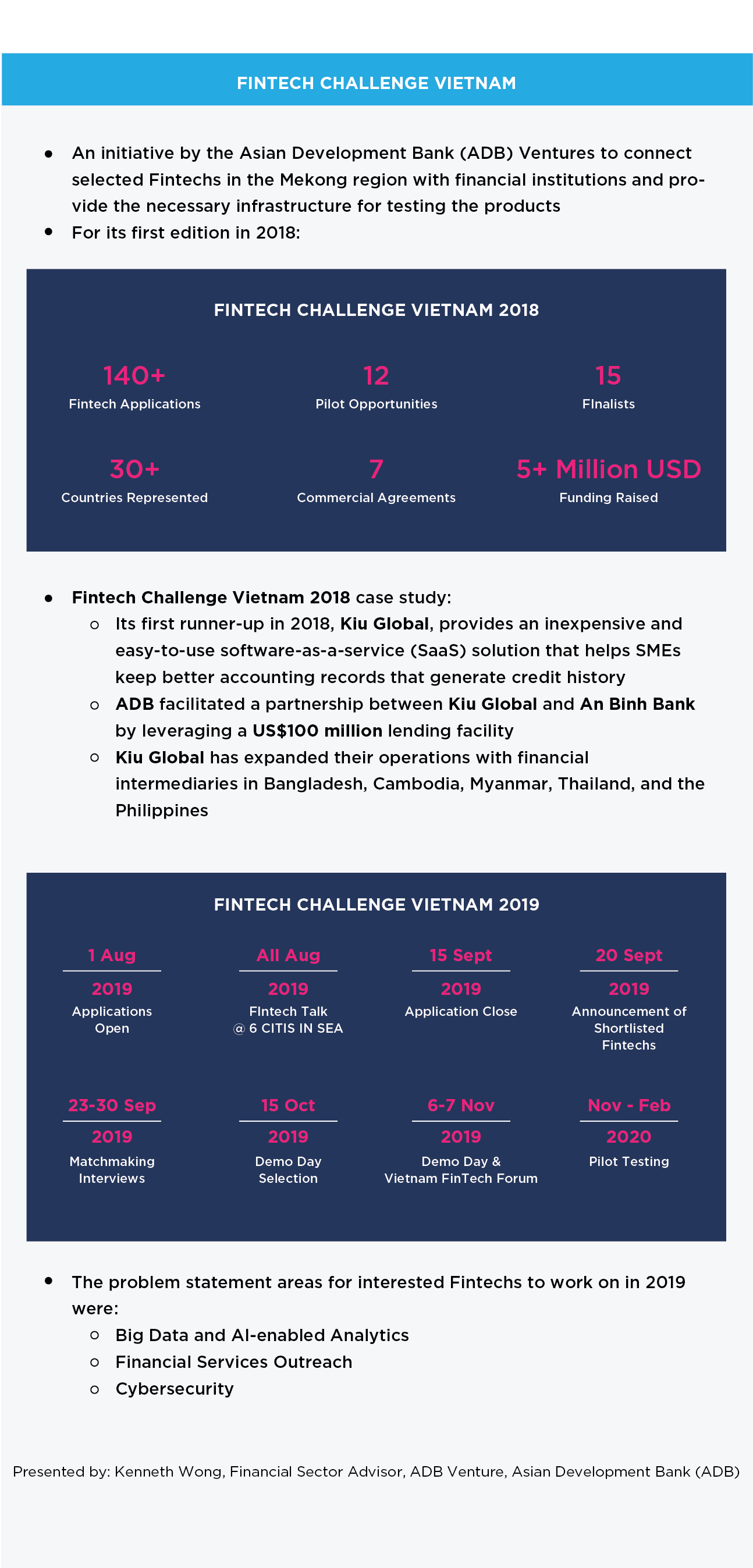

“As regulators, how do you bridge that gap in terms of educating, what I call the financial and technological literacy gap? How do we as planners manage this?” said Kenneth Wong, Financial Sector Advisor, ADB Venture, Asian Development Bank (ADB) during the Master Showcase Q&A session.

According to him, communication policy remains as one of the biggest challenges in Malaysia and in Asia. Policy planners and regulators need to have a communication strategy on how you can align all the related matters so that they reach out to the millions of those who are unbanked.

To ensure wider coverage of the financial outreach, the relevant infrastructure has to be in place. “I have one small pitch: why don’t we promote cheap and reliable smartphones and cheap data plans as a start? This is so that everyone can be on board and the communication policy can finally reach them. This is something I would like to see policy planners start thinking about,” he said.

Conclusion

The Fintech landscape in ASEAN shows us that it is at different stages in different countries: some may be ahead in terms of legislation and framework while others are ahead of the curve in different sub-sectors of Fintech. However, all the Fintech firms in the region have the same desire to increase accessibility to financial services and in the process facilitate the region towards achieving financial integration and inclusion.

1 CARI, “Special Update on the 35th ASEAN Summit in Bangkok,” November 18, 2019.

2 Ibid.

3 The Star, “Please leave your wallets at home, July 12, 2019.

4 Tech in Asia, “China’s e-wallet success is an example for Southeast Asia players,” Jan 10, 2019.

5 Asian Banking & Finance, “Is cash still king in ASEAN?,” April 25, 2019.

6 Fintech Malaysia, Malaysia Fintech Report 2019, December 2019.

7 EY, “Thailand Fintech Landscape Report, 2019.

8 KPMG, “Fintech: Opening the door to the unbanked and underbanked in Southeast Asia,” April 5, 2016.

9 FintechnewsMalaysia, “How is Malaysia’s Equity Crowdfunding Scene Doing in 2019?,” March 15, 2019.

10 Securities Malaysia, “SC Releases New Guidelines to Facilitate Equity Crowdfunding,” February 10, 2015.

11 Securities Commission Malaysia, “SC Introduces Regulatory Framework to Facilitate Peer-to-peer Financing,” April 13, 2016.

12 Elaine Lockman, “Crowdfunding and Financial Inclusion: Alternative Financing – Equity and Peer-to-Peer (P2P) Crowdfunding” at the Smart Showcase Series on Fintech, August 15, 2019.

13 Ibid.

14 Fintechnews Singapore, “What Is Wealthtech? An Introduction,” May 18, 2018.

15 Ibid.

16 Statista.

17 Ibid.

18 Ibid.

19 McKinsey & Co., ”Digital Finance for All: Powering Inclusive Growth in Emerging Economies”, September, 2016.

20 OECD, ERIA, ”SME Policy Index: ASEAN 2018”. Based on the current GDP of US$2.9T.

21 Ibid.

22 Ibid.

23 World Bank IFC, “SME Finance Forum,” 2017.

24 The Balance – Small Business, “What Is Insurtech and How Are Insurers Using It?” August 7, 2019.

25 Tech Collective, “Top InsurTech startups in Southeast Asia,” January 9, 2019.

26 Ibid.

27 The Star Online, “PIAM targets 4% insurance penetration by 2020,” August 30, 2018.

28 Fintechnews Singapore, “Will Singapore Become a Regtech Leader? Regulatory Reporting 2.0.” July 10, 2017.

29 United Nations Office on Drugs and Crime (UNODC), “Money-Laundering and Globalization”.

30 Bloomberg, “Banks Trimming Compliance Staff as $321 Billion in Fines Abate,” March 23, 2017.

31 International Banker, “Spotlight on Compliance Costs as Banks Get Down to Business with AI,” July 4, 2017.

32 Bloomberg, “Anti-Money Laundering Solution Market Worth $3.6 Billion by 2024,” September 4, 2019.

33 Fintechnews Singapore, “What Have We Learned from Sandboxes and Innovation Offices?” March 1, 2019.

34 Fintechnews Singapore, “APIX, a Global Marketplace for Cross-Border Fintech Services Officially Hits The Market,” November 14, 2018.

35 Fintechnews Singapore, “Will Singapore Become a Regtech Leader? Regulatory Reporting 2.0.” July 10, 2017.

36 The Edge Markets, “Asia needs region-wide approach to harness fintech’s full potential, says ADB,” October 12, 2018.

37 CARI, “Special update on the 5th ASEAN Finance Ministers’ and Central Bank Governors’ Meeting (AFMGM),” April 18, 2019.

38 CCN, “Singapore Inks FinTech Cooperation Pact with France,” March 28, 2017.

39 Securities Commission, “SC Establishes Fintech Cooperation Agreements with Major Financial Centres,” September 14, 2017.

40 Deloitte, “ Digital banking for small and medium-sized enterprises – Improving access to finance for the underserved,” 2015.

41 Ibid.

42 World Bank IFC, 2017 “SME Finance Forum”, by benchmarking economies for potential demand and subtracting existing supply.

43 OpenGov, “Philippine Fintech alliance to adopt TechnoEthics,” September 24, 2019.

44 BusinessWorld, “Online lenders, fintechs to adopt code of ethics,” September 17, 2019.

45 Fintechnews Indonesia, “Indonesia’s P2P Lending Sector Sees 642% Growth in Disbursements,” October 25, 2019.

DOWNLOAD PRESENTATION SLIDES

READ PRESS RELEASE

Click here to read press release.