Economic Snapshot: ASEAN Focus May 2017 | Cambodia

Published on 23 May 2017

by Krzysztof Halladin, Research Fellow, CIMB ASEAN Research Institute

With gross domestic product (GDP) growth of 7 % year over year (yoy) in 2016 Cambodia is continuing its fast pace of growth, aided by the export of garments, strong construction activity and government spending. The tourism sector slowed down but the agriculture sector rebounded a bit compared to sluggish performance in last couple of years caused by low commodities’ prices and adverse weather conditions. The current account has narrowed last year thanks mainly to a steady increase in foreign direct investment (FDI) and low oil prices on the import side. Although revenue collection improved, the increase in public wages led to the higher fiscal deficit. Rising consumption spending and wages accelerated inflation. The risks to an overall positive outlook involve the possible slowdown in China and in the European Union (EU); the potential elections in 2018; the fallout from further US rate hike (as the economy is highly dollarized); and rapid credit growth highly concentrated in real estate and construction sectors.

Moderation in garment export and construction activity

- GDP growth reached 7% in 2016 and I expect the economy to sustain this robust trajectory with forecasted growth rates of 7% in 2017 and 2018. The main drivers of growth remain garment and footwear exports; expansion in construction activity; and increase in government spending. There are however some signs of moderation in the first two areas mentioned above.

- The garment and footwear sector constitutes around 70% of Cambodia’s exports and, in USD terms, it grew by 8.4% in 2016 compared to 12.3% growth in 2015. Despite introducing higher value additions like embroiler or printing and more stable industrial relations, export growth decreased, most likely because of competition from producers in Vietnam and Myanmar.

- The tourism sector increased only 5% in 2016, compared to 6.1% in 2015.I believe that this year there is a likelihood rebound driven by new direct flights from Asian countries. The agriculture sector, lethargic due to low commodity prices, benefited from good weather in 2016, leading to growth of 1.8 % which is much improvement since in 2014 and 2015 the growth amounted only to 0.2 and 0.3 % respectively.

- Government expenditure is estimated to reach 21.4% of GDP, compared with 20.5% in 2015. A fair amount was allocated to a rising wage bill — up from 6.5% of GDP in 2105 to 7.4% of GDP in 2106 — which should provide support to income growth and consumption demand. Expenditure also targeted at urban and rural infrastructure shortcomings.

- Credit growth moderated last year increasing 25.8 % yoy in comparison to 28.6% in 2015.However, credit to construction, real estate, and mortgages increased slightly. I expect moderation in credit as new banking regulation on liquidity and capital requirements will be introduced.

- The private investors deposits expanded 19.3% yoy, compared to 16.6% yoy in 2015. This provide some comfort for those who feared that credit bubble which is mainly concentrated in contraction sector might burst.

Improved external position from FDI and export performance

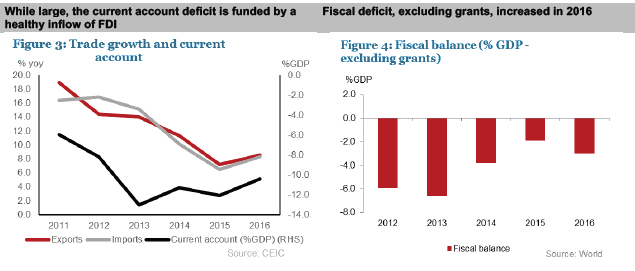

- The Current account deficit (excluding official transfers) has narrowed to 9.5 % of GDP in 2016, in comparison with 10.6% the previous year. The main reason for this decline was a moderation in import growth due to low commodity prices for the majority of 2106, plus growing remittances and strong FDI mainly from Asian countries (about 40% from China). Gross foreign reserves rose to US$6.4 billion (or 5.4 months of imports) compared with US$5.6 billion in 2015.

- After 2 years of decline, Net FDI grew 30.5 % yoy. The inflows where mainly to telecommunication and construction sector, and the FDI to manufacturing sector drop, which might be assign to increased competition in the region.

Inflation edging upwards

- Inflation accelerated at the end of year to 3.9 % pushed by strong consumption. I expect a further increase this year as last year inflationary pressures had been dampened by low oil prices.

More fiscal expansion than improvement in revenue collections

- Fiscal policy is the main demand side policy tool in Cambodia given the limited scope of monetary policy in a highly dollarized and cash-based economy.

- Revenue mobilisation improved to 17.6%% of GDP compared to 16.8% the year before, though because of government spending is increasing at a faster rate. The reason for that are higher public wages. The fiscal deficit widened last year to 3 % of GDP compared to 1.9 % in 2015, yet it was still far lower than 4.2% that was planned under 2016 Budget Law.

Risks and Other Issues

- Cambodia’s highly concentrated export market (70% of all exports are garments) makes it highly vulnerable to regional competition. The risk is increased when one considers that the materials for production are largely imported from China. Lower growth in China would spill over to Cambodia through channels of tourism, banking and FDI.

- Some policies were introduced to promote the use of local currency, yet the economy is still highly dollarized; 95% of all bank deposits are in USD. An appreciation of the dollar will affect the economy not only, through higher prices for tourists, but also reducing the competitiveness of Cambodia exports.

- The amount of Chinese aid inflows is increasing while the amount of military and humanitarian assistance from US and EU is decreasing. The reason for that is lack of fulfilment of US aid conditions regarding human rights and technical specifications. This make Cambodia more depended on China and vulnerable to possible slowdown in Chinese economy.

- Some upside is expected from structural reforms pertaining to human development and infrastructure, although historically, reforms infamously stop at the regulatory stage. Consistent enforcement will be needed to put plans into practice.

Disclaimer: All rights reserved. No part of this report may be reprinted or reproduced or utilised in any form or by any electronic, mechanical or other means, now known or hereafter invented, including photocopying or recording, or in any information storage or retrieval system without proper acknowledgement of CIMB ASEAN Research Institute. The views, responsibility for facts and opinions in this publication rests exclusively with the authors and their interpretations do not necessarily reflect the views of CIMB ASEAN Research Institute.

![]()