LIFTING-THE-BARRIERS REPORT 2015 | RETAIL

Published date: August 2015

TABLE OF CONTENT

(Click any topic to read the related section)

- Executive Summary

- 1. Retail Innovation Landscape

- 3. Lifting-The-Barriers

- 4. A Great Opportunity for ASEAN

- 5. Table of Figures

- 6. Authors

EXECUTIVE SUMMARY

Innovation in retail has been accelerating for the past couple of decades across the globe and can be grouped into 3 buckets:

Offering – includes all the new products and services which are launched by retailers.

Shopping experience – captures innovation in the consumer interaction space such as e-commerce and emerging technologies like “virtual reality” or ‘beacon technology’.

Enablers – regroups innovation occurring on the back-end and more operational side of the value chain, enabling retailers to improve services, optimise processes and be more cost efficient.

Although most ASEAN countries have engaged in the path towards “retail modernity” over the last years, retail innovation in ASEAN is today still in the early stages of development. The penetration of new products, services and platforms such as private labels and e-commerce are indeed still low compared to more developed markets.

Driving innovation in ASEAN represents a unique opportunity to take the retail industry to the next level, improving the retail experience for consumers, facilitating the emergence of regional players, homogenising the retail space across countries and helping drive ASEAN markets integration.

However, there are barriers to the development of retail innovation in ASEAN, including market readiness, cumbersome regulations, integration of talent, insufficient infrastructure capabilities and lack of access to financing for innovators. The Lifting-The-Barriers Roundtable at the ASEAN Business Club forum, recently held in Singapore, highlighted four specific actions that ASEAN countries should consider to overcome those barriers and fully unleash the potential of retail innovation.

Reduce non-tariff barriers for new products – harmonising labelling & testing requirements and increasing the capacity and influence of the ASEAN secretariat.

Improve access to talent able to drive innovation – encouraging the inclusion of the retail sector into the design and delivery of vocational training and harmonising the recognition of certificates across ASEAN.

Improve trade efficiency to ease the flow of new products and services across countries – further driving the implementation of the ASEAN Single Window and harmonising the payment eco-system.

Drive integration of ‘Retail Innovators’ – establishing a regional network of government agencies promoting innovation and fostering collaboration between innovation incubators and retailers.

This paper provides an understanding of the landscape of retail innovation opportunities and assesses the current status of retail innovation in the region. It specifically highlights potential barriers and the role of key stakeholders in overcoming those, leveraging inputs from the Lifting-The-Barriers Roundtable recently held in Singapore during the last ABC forum.

1. RETAIL INNOVATION LANDSCAPE

ASEAN is lagging behind on innovation

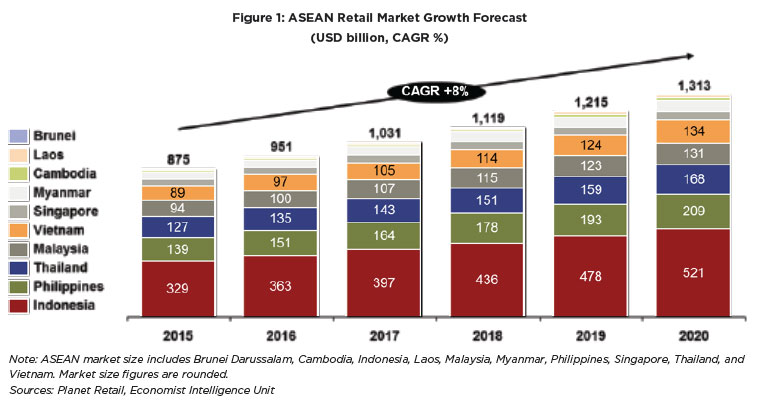

With over 600 million consumers in 10 countries whose collective GDP amounts to about US$2.4 trillion, ASEAN is today the seventh largest market in the world and is expected to be the fifth largest by 2020. The ASEAN retail market is currently worth an estimated US$875 billion driven by Indonesia (38%), the Philippines (16%) and Thailand (15%).

However, the level of retail development significantly varies from one country / region to another, often driven by the ability of key players to innovate. But what does innovation mean for the retail sector?

The different types of innovation in the retail space can be grouped into 3 buckets: Offering, Shopping Experience and Enablers.

Offering

Some of the most visible innovations in the retail space are down to the new products and services which have been progressively launched over the years by retailers across the globe.

Product Innovation. Retailers have first looked at creating their own store-label brands, directly competing with the branded products that they were distributing. Those own-store-branded goods also known as private label goods really started taking off in the 1990s. In what started as a retailer’s low-cost & low-quality substitute for known brands, private labels now have significantly increased in quality, delivering against consumer needs across wider price points. They have even become a key differentiator for some retailers in terms of a good quality offering with lower prices, positively affecting the retailer’s image.

Service Innovation. Retailers have also looked at expanding their offering to become more competitive and drive consumer loyalty, getting into new product categories and expanding into new services. For example, major retailers such as Tesco have expanded their businesses into financial services (Tesco Bank) and telecommunications (Tesco Mobile).

Shopping Experience

E-commerce growth. One of the key innovations in the consumer interaction space has certainly been the growth of e-commerce, which has been revolutionising not only the retail business but also how FMCG companies develop, market and distribute their products. E-commerce gained scale in the 1990s as an alternative way of engaging customers from the traditional brick-and-mortar store format and to provide more convenience. Over the past two decades, it has grown steadily, making up 6% of the global retail industry in 2014, or around US$ 1.3 trillion.1 The global e-commerce market is expected to grow between 13 and 20% per year to reach US$ 2.2 trillion by 2017 and more than US$ 7 trillion by 2025. Growth in the developed markets will be driven by the increase in share of wallet and basket size while growth in the developing regions is expected to be fueled by digital adoption and the increased penetration of shoppers.

Emergence of virtual reality. More recently, the retail space has also seen the emergence of “Virtual Reality” (VR) innovations providing consumers with an augmented in-store experience. VR could be the next frontier for retail, most of the VR applications currently still being under development. Different retailers ranging from fashion apparel companies or furniture providers to automotive and grocery retailers have launched several initiatives into the virtual reality space, in an effort to merge the physical and digital world. These initiatives also serve as a differentiating factor for the retailers, helping create a buzz that further showcases their brand image. Several applications implemented by retailers include VR stores recreating the in-store experience; VR fitting rooms used by apparel retailers allowing quick and hassle-free fittings; VR mirrors enabling shoppers to e.g. try the look of different eyeshadows and lipsticks without applying them to the skin.

Beacon technology. Some retailers are also increasingly using the ‘beacon technology’ which enables them to directly interact with the mobile phones of consumers in store. Beacons are short-range (Bluetoothbased) communication devices that interact with smartphone apps and enable retailers to offer consumers live offers (incl. real-time, situational, dynamic pricing), live couponing, loyalty programs, mobile payment, and data collection (which in turn again can be used for e.g. live offers and coupons) as consumers visit the store.

Revolutionary payment / check-out process. The payment process is a critical element in the sales chain as a bad experience can erode any relationship built with the consumer while in-store. Speed is one of the most important performance criteria and retailers have spent much effort on reducing queuing & check-out times. In that context, self-scanning stations are being increasingly deployed by food retailers and drugstores. Other innovative applications that speed up the check-out process, increase consumer interaction, and collect sales intelligence for the retailer during the check-out process are e.g. facial recognition / digital signage or “Pay-by-Selfie” (Alibaba).

Other shopping experience innovations. Finally, other innovations include i.) storefront extensions / infinity aisles that display related products, which are not available in-store but can be ordered online and delivered home (portfolio / reach extension) or ii.) the embedment of social media into a physical store environment such as the display of the number of Facebook likes on clothes hangers in real time.

Enablers

Significant innovation has also occurred over the past years on the back-end and more operational side of the value chain. Innovations have specifically enabled retailers to optimise processes and be more cost efficient whilst improving service levels.

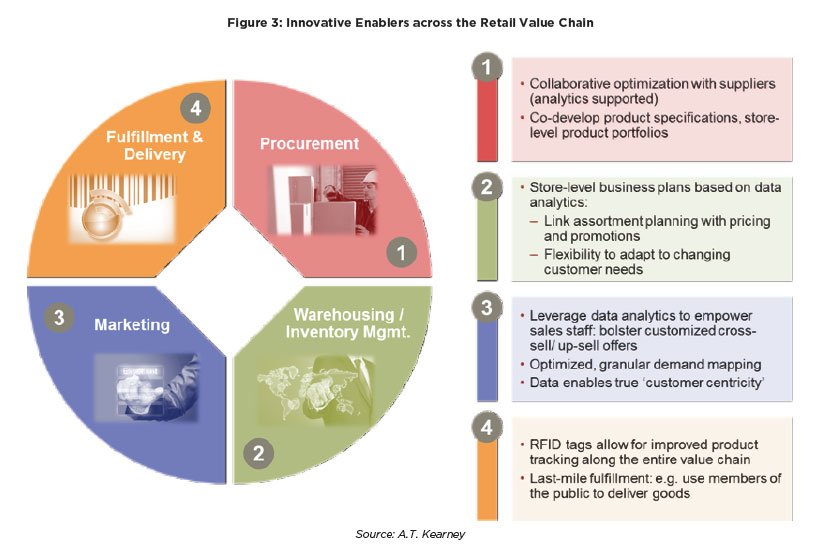

Optimised, collaborative procurement. Retailers increasingly co-create value with their suppliers. This starts right at the beginning of the value chain and leverages capabilities which are unique and inherent to the supplier as well as to the retailer. As an example, retailers use during the sourcing process, an RFP structure that enables ‘collaborative’ or ’expressive’ proposals. This encourages supplier innovation and creativity and enables suppliers to align capabilities and interests with requirements. Combinatorial optimisation (‘analytics engines’) accelerates analysis and evaluates complex, interdependent proposals based on specified business constraints. This approach allows retailers to develop targeted, store-level product portfolios, alternate specifications, and targeted incentive / discount / rebate structures.

Customer-driven inventory / warehouse management and assortment planning. To maximise sales, inventory and assortment planning must be integrated into a store-level business plan that is based on customer data analytics. Leading retailers link the planning process with pricing and promotions, such as increased promotion activity in select categories; they incorporate assortment and placement decisions, such as assortment extensions into their planning and reflect on competitive actions. They further model economic and demographic conditions, also weather conditions, such as low temperatures which would increase sales of winter clothes. This together with shorter planning cycles builds an agile organization that knows its customer needs and can flexibly cater to them.

Analytics-enabled marketing & offering customisation. The rise of the internet and concurrent investment in IT infrastructure has made data available like never before. Data analytics drives relevant insights out of the data and applies the insights to strategies that help organizations create and extract value. Analytics provides detailed information on customer needs to salespeople, for example, bolstering customised cross-sell and upsell offers and scripts. Analytics can also optimise supply levels, distribution and logistics with granular demand mapping and forecasting. It can also help optimise production processes with more sophisticated assessments of bottlenecks and waste, or product design, leading to smarter investment in product elements that are most valued by customers while reducing cost and delivery for those elements that customers do not value much.

Improved product tracking. With the rise of “The Internet of Things”, radio-frequency identification (RFID) technology is gaining increasing importance: the next frontier is end-to-end RFID tagging along the entire value chain from the manufacturer to the consumer. Integrating RFID technology with the above described collaborative procurement strategy and advanced data analytics provides a powerful end-to-end solution. Other applications include mobile RFID readers that constantly and automatically maintain inventory counts and monitor asset location.

Especially in e-commerce, real-time end-to-end tracking is becoming ever more critical as innovations to fulfil ‘the last mile’ are deployed: crowd sourcing, i.e. paying members of the public to deliver items on their way home has been explored as one option. Deutsche Post DHL has e.g. started the “MyWay” program in Sweden: the company pays members of the public to deliver online goods. Also Walmart in the US has expressed interest in using shoppers to deliver products on their way home from its stores in return for a discount.

All of the above new technologies / enablers are reshaping the retail environment at an unprecedented pace. Retailers must therefore stay at the forefront of technological innovations, not only to be competitive in terms of store profitability, but also to deliver a state-of-the-art customer experience.

2. WHERE IS ASEAN TODAY?

2.1 ASEAN is lagging behind on Innovation

According to the latest Global Innovation Index (GII), ASEAN (except Singapore) appears to overall lag behind when it comes to innovation in general. The GII measures 81 innovation drivers across a nation’s institutional quality (political / regulatory / business environment), human capital and research (education / R&D), infrastructure quality (including digital infrastructure), market sophistication (access to capital / investment), business sophistication (innovation linkages and absorption). On the output side, the GII measures knowledge creation, knowledge linkages / diffusion as well as creative outputs (intangible assets, creative goods and services, online creativity).

As we zoom into innovation in the retail space, the overall picture is no different. Although most ASEAN countries have engaged in the path towards “retail modernity” over the last years, retail innovation in most of ASEAN today is indeed still in the early stages of development. The penetration of new products, services, supply chain enablers, and analytics applications described in chapter 1 are indeed not at the level observed in more developed markets.

2.2 ASEAN’s modern retail is underdeveloped

A key indicator of Innovation in the retail space is the penetration level of modern trade. Across ASEAN, that indicator remains largely underdeveloped, with modern trade representing 50% or less of total retail in all countries but Singapore (currently at ~60%) vs. 70-80% in developed markets.

Modern retail naturally congregates in the more developed parts of ASEAN and is a direct reflection of the heterogeneity of the region. Markets in Singapore as well as the city centers of the major metropolitan areas (e.g. Bangkok, Jakarta, and Kuala Lumpur) are mature and saturated and the retail environment is highly competitive. The outskirts of the major metropolitan areas can be defined as ‘semi-mature’ with still many white spots remaining, retailers having over the past years first and foremost focused on site acquisition rather than driving innovation. Finally, rural areas as well as emerging nations such as Cambodia and Laos constitute a low margin, low cost environment and pose significant logistics challenges to retail operations.

2.3 ASEAN retailer driven product innovation is low

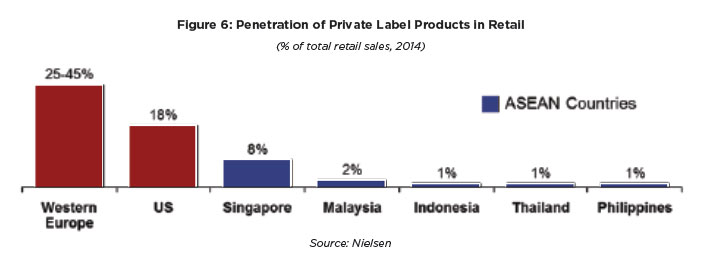

Retailer driven product innovation remains relatively low in the region, with private label penetration in ASEAN accounting for 2% or less (except Singapore) vs. 20% to 45% in more developed countries.

As modern retail markets in the region mature, private label penetration has not accelerated at the same pace as expected by retailers. A recent study from Nielsen confirmed the strong brand loyalty of South- East Asian shoppers: especially the lower income segments believe that it is worth to pay a premium for brand names as they fear losing money if they try a new brand (6 out of 10 respondents in Indonesia, the Philippines and Thailand see this risk of losing money associated with private labels). Moving forward it will be up to the retailers to build trust in their own brands to stimulate private label sales in the region.

2.4 ASEAN’s E- /M-Commerce is growing fast but is still underdeveloped

As highlighted in last year’s report “Lifting the Barriers to E-Commerce in ASEAN”, e-commerce remains underdeveloped in the region, representing 2% or less of total retail sales in 2014 (excluding Singapore at 5.6%).

However, the recent growth over the past year confirms that ASEAN will be one of the world’s fastest growing markets for e-commerce in the next few years – we estimated an annual growth of ~25 percent across the region in last year’s report. Developments since have allowed for an even more optimistic outlook driven by favorable demographics, improved digital infrastructure, increased adoption of social media, and improving offerings.

Importantly, cross-channel integration has started to develop, with ASEAN e-commerce players entering the offline world: Zalora for example has been opening pop-up stores next to established offline retailers (e.g. Zara) in Singapore, as well as in Malaysia and Vietnam to give customers the opportunity to ‘touch and feel’ the actual products. This model is currently being further rolled out in the Philippines and Thailand. Zalora also partners with 7-Eleven in a unique way, 7-Eleven stores serving as pick-up points for Zalora. Bricks-and-mortar stores are likewise investing in multi-channel offering in order to stay competitive – this trend is relatively developed in Indonesia, Thailand and the Philippines, where the growing number of online shoppers have prompted retail brands to offer innovative services such as online gift registries or in-store pickup or delivery services. Net, ASEAN is overall lagging behind in terms of retail innovation but the potential is there, should some key barriers be lifted.

3. LIFTING THE BARRIERS

The Lifting-The-Barriers Retail Roundtable at the recent 2015 ASEAN Business Club Forum highlighted four specific barriers to innovation in retail in the region: (1) Significant non-tariff barriers persist that impede trade flows and dampen innovation – divergent national labeling and food safety regulations are most critical. (2) Increasing talent shortage stifles innovation and drives up labor cost. (3) As highlighted in last year’s report on e-commerce in ASEAN, trade efficiency remains low with an underdeveloped transport infrastructure. (4) Finally an immature networking culture and a focus on the short-term has hampered the development of an innovation-based ecosystem.

The following sections examine each barrier in detail, elaborate on how current local or regional initiatives help address these barriers, and offer pragmatic recommendations for future action to be considered by the ASEAN community.

3.1 Reduce non-tariff barriers for new products

Understanding the Barrier

Current picture

In 1992 ASEAN member countries committed to reduce tariffs under the CEPT2 scheme. Most tariff barriers have since been successfully reduced, but tariffs are only ‘the tip of the iceberg’ – attention has now shifted to non-tariff barriers (NTBs). Reducing NTBs could really help step-up product innovation and can be considered as the next frontier in ASEAN integration. The task is not easy as NTBs originate from local legislation and touch the very core of a country’s sovereignty. Non-tariff measures (NTMs) are therefore unlikely to disappear completely in the near-term, but the ASEAN business club retail roundtable argues that minimising and harmonising NTMs across the region is the key to unlock innovation and growth in the retail sector and beyond. Domestic regulations governing e.g. testing and food safety are key barriers to innovation in retail in ASEAN. Other NTBs that affect the retail sector include inconsistent labelling requirements across member states (e.g. language / nutritional information for food products), or inconsistent regulations on obtaining a license to operate. These NTBs significantly increase product development cost and create an environment of elevated risk that deters both manufacturers and retailers from launching new products across ASEAN or from investing in technology / new business models as scale economies are likely not to materialise (numerous national plays instead of a concerted, integrated, regional ASEAN play). This regulatory complexity as well as issues of transparency, predictability and consistency in interpretation of these regulations impede growth across the region.

ASEAN leaders are certainly cognizant of the importance of addressing NTBs in the process of driving the AEC, and many programs are well underway. Below we take stock of what is being done today, how the actions have impacted the retail sector and what should be done additionally or differently moving forward.

Root causes

Domestic regulations. Complex regulations lead to inefficiencies and issues of transparency, predictability as well as consistency in interpretation of rules and regulations remain. There are many manifestations of these issues – one is acceptance of certificates of origin: with testing requirements not harmonised across ASEAN, certificates of origin are often not accepted by the importing country and further inspection is triggered. This causes a delay in goods forwarding as cargo is being held in customs. Another example is the varying labelling requirements across the region – some countries will only accept labels in local language which makes SKU portfolio management very complex for both manufacturers and retailers. Even within a country, legislation often varies state by state. Licenses to operate a business must be obtained in every member state, business registration times varying significantly across the region.

Limited public-private cooperation. Legislation can have a direct and positive impact on the business environment. However, there are hardly any regional private sector feedback loops institutionalised that would feed into the legislative process. Most policies are conceived by civil servants without inclusion of private sector know-how and are therefore not always optimum.

Lifting the Barrier

What is being done today?

Prioritised measures for AEC implementation. 505 high-impact measures from the AEC blueprint have been prioritised for fast-tracking and in March 2015 about 90% (457) had been implemented. These measures address matters related to tariffs, investments, services, air transport, financial services, customs procedures and standards. Measures not yet implemented are more complex in nature and include the 10th services package, single self-certification scheme, as well as the ASEAN Single Window3. End-of-year target is to complete 95% of integration measures in the run up of the AEC launch.

These measures have significantly improved the ASEAN business environment by substantially removing tariffs for intra-ASEAN trade. Barriers to trade in services and investment have been further reduced and the trade facilitation environment improved. However, a significant layer of barriers, especially non-tariff, remains.

Focus of post-2015 agenda on non-tariff barriers.

A key focus of the post-2015 agenda therefore will be on addressing non-tariff barriers. The ASEAN Secretariat has for example launched a program for direct filing of non-tariff barrier cases. By May 2015, however, only 69 cases had been reported and 45 were subsequently resolved. This shows both a lack of trust in the authority and capacity of the Secretariat in the region and limited visibility the business community has in the work of the Secretariat.

To operationalise the reduction of NTBs and track progress, the ASEAN Trade Facilitation Joint Consultative Committee that started work in 2008 has been re-instated after a period of inactivity. National Trade Repositories (NTRs) have been put in place to strengthen the institutional arrangements and management of the regional economic integration process. Further, the “NTM Work Program” has been launched – the program collects data on non-tariff measures and links with the WTO4. As part of this program, ASEAN member countries have agreed to eliminate some NTBs, but a majority of measures that have been identified as potential trade barriers, are defended by individual members as legitimate and not as a barrier. To eliminate NTBs, concerted regional decision making is required, reliance on self-notification and voluntary removal by member countries having proven to be ineffective.

Malaysia is currently leading the way and has institutionalised private sector feedback loops with industry representatives participating in joint legislative workshops. On the ASEAN-level, ‘Project Pathfinder’ has been launched to roll out this model across the region.

Key recommendations for tomorrow

Harmonise labelling and testing requirements. For the further development of the retail sector in ASEAN, two priority NTBs stand out: complex and nontransparent labelling requirements as well as repetitive testing of products in each member state impact speed to market and increase cost for manufacturers and retailers. This cost is eventually passed on to the consumer. Harmonising testing requirements would certainly be most welcome, driving efficiency and accelerating new product development and launch. With regards to language requirements, specifying which components need to be in local language (e.g. nutritional facts) and harmonising requirements across ASEAN would greatly reduce SKU complexity and cost, speed and cost at the manufacturer and retailer level.

Scale up leadership capacity of the ASEAN Secretariat. Strong regional leadership is required to drive integration. Hence the ASEAN Business Club Retail Roundtable argued that the leadership capacity of the ASEAN Secretariat had to be further scaled up. To strengthen the institutional capacity of the Secretariat, we would recommend to set up special divisions that deal with sector specific issues such as retail or financial services or transportation. These sector-specific sub-divisions will not only contribute to policy making but more importantly enforce implementation by regularly reviewing and tracking sector commitments ASEANwide. These groups will also complement, upgrade and centralise the current dispute settlement process to drive resolution speed and if necessary make recommendations for policy amendments. The sector-specific special divisions must consist of both civil servants as well as private sector representatives. This set-up will allow for the most pressing issues a sector is facing as well as possible solutions to be brought to attention to policy makers in a timely manner.

Step up marketing of the ASEAN idea to the wider public. For the ASEAN community to move forward, the people of the region need to feel a sense of common ASEAN citizenship and be more connected to one another. Only this type of mindset will drive more people (other than the political and business elites) to engage in shaping ASEAN and thereby highlighting to a greater degree the issues and pain points. Nontariff barriers would then become more visible more quickly and public pressure to address these issues will increase. Ultimately this “public push” will lead to faster reduction of NTBs and harmonisation of regulations across the region. Today’s ASEAN, however, is still to some extent a concept that only the elite is familiar with – in a move toward truly realising the ASEAN Economic Community by 2015, campaigns for ASEAN awareness must be stepped up. We also suggest engaging the private sector to a greater degree to bring to life the ASEAN idea. The retail sector is uniquely positioned as retail reaches literally every person in ASEAN.

Understanding the Barrier

Current picture

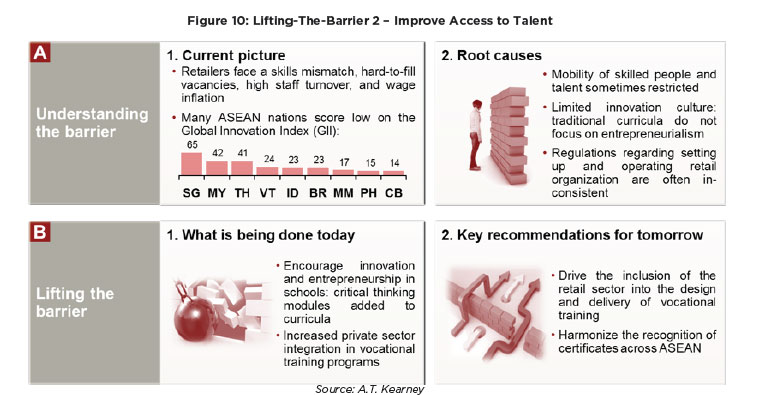

One of the key drivers of innovation is the quality of a nation’s human capital – creative and critical thinking, appetite for risk taking and thinking entrepreneurially are the constituting parameters. While we recognise that there is no short-term program that will elevate an entire nation’s human capital, we specifically argue for closer cooperation on vocational training between retailers and the public sector. More broadly, we argue for policies to be implemented that foster an innovation ecosystem.

The Global Innovation Index (GII) that we referenced earlier has made the ‘Human Factor in Innovation’ the guiding theme of its latest 2014 report. Also economic literature demonstrates that human capital formation is a central element of technical and innovative progress and therefore of economic growth – as the Oslo Manual puts it: “Innovation capabilities, as well as technological capabilities, are the result of learning processes, which are conscious and purposeful, costly and time-consuming, non-linear and path-dependent, and cumulative”. Zooming into human capital parameters measured by the GII (cf. figure 10), many ASEAN nations score low on education and R&D.

One of the key drivers of innovation is the quality of a nation’s human capital – creative and critical thinking, appetite for risk taking and thinking entrepreneurially are the constituting parameters. While we recognise that there is no short-term program that will elevate an entire nation’s human capital, we specifically argue for closer cooperation on vocational training between retailers and the public sector. More broadly, we argue for policies to be implemented that foster an innovation ecosystem. The Global Innovation Index (GII) that we referenced earlier has made the ‘Human Factor in Innovation’ the guiding theme of its latest 2014 report. Also economic literature demonstrates that human capital formation is a central element of technical and innovative progress and therefore of economic growth – as the Oslo Manual puts it: “Innovation capabilities, as well as technological capabilities, are the result of learning processes, which are conscious and purposeful, costly and time-consuming, non-linear and path-dependent, and cumulative”. Zooming into human capital parameters measured by the GII (cf. figure 10), many ASEAN nations score low on education and R&D.

Root causes

Restrictions on mobility of skilled people and talent. Availability of talent in ASEAN is a topic across sectors and retail is no exception. Part of the low availability is attributable to limited flexibility in labor markets in the region. The free movement of skilled professionals under the AEC is partly driven by the requirements of the 1995 ASEAN Framework Agreement on Services, which includes provisions for the movement of natural persons. Progress on labor mobility through the ASEAN Framework Agreement on Services has, however, been fairly slow. One example of limited flexibility is the “full time employment “ rule in the retail space in select countries; opening up the possibility of part-time employment would allow the sector to more flexibly cater to consumer needs and thereby create more value.

Limited innovation culture (education system). Most ASEAN economies are merit-based societies, where creative thinking based classes have traditionally not been part of school curricula. Education systems across the region mostly focus on test-based academic performance and favor science and technology subjects. In particular an environment that focuses on the acquisition of academic knowledge often dampens creativity and entrepreneurialism. Academic excellence is important but is no longer a guarantee for success in today’s interconnected business environment. Students must indeed be readily able to apply their knowledge in a variety of (changing) contexts.

Inconsistent regulations regarding set-up and operations of retail organisations. Another barrier is around the inconsistency of requirements with regards to setting up retail organisations across ASEAN. According to the World Bank Services Trade Restrictions Database, Malaysia e.g. limits foreign ownership to 70 percent. In Thailand on the other hand there is no restriction on foreign ownership – however, the applicant must have a total capital over THB100 million (USD $3 million) and total capital per store over THB20 million. A license is required for commercial presence while a retail specific license is not required, and if the minimum capital requirement is not met, a special license is necessary. A coherent approach to eliminate these non-tariff barriers would be beneficial to the AEC.

Lifting the Barrier

What is being done today?

Encourage innovation and entrepreneurship in schools. Many programs have already been put in place to encourage innovation at schools. As part of the country’s 10-year infocomm master plan, Singapore has for example launched the FutureSchools@Singapore program which strives to develop schools into peaks of excellence following an ability-driven education paradigm and encourages innovation and enterprise at school. It is jointly run by the Ministry of Education and iDA5. Industry partners also use FutureSchools to experiment and commercialize the most promising new ideas.

Public-private sector cooperation on vocational training6. ASEAN recognises the need of vocational training and has together with the Regional Cooperation Platform (RCP) launched programs to address vocational education reform. The group appreciates the disconnect between what traditional public education institutions offer and what today’s increasingly knowledge-based and interconnected job market requires. As an example, Singapore has set up the “Singapore Institute of Retail Studies” (SIRS), which is a Continuing Education & Training (CET) institute of Nanyang Polytechnic. The primary mission of SIRS is to provide market driven holistic training solutions through the national Workforce Skills Qualifications programs in Retail, Service Excellence, Productivity and Business Management to enhance the skills and employability of the Retail and Service workforce in Singapore. The SIRS example serves as a best-in-class case, but further collaboration between public education institutions and the private sector is still required to bridge the skills gap across ASEAN.

Key recommendations for tomorrow

Drive integrated approach to vocational training6. The levels of development and education systems in each ASEAN member state are very different – however, vocational training is a common theme across the region. It would be therefore wise that workforce development (or human capital development) is pursued using a holistic approach that encompasses education systems, economic development policies & programs, and the private sector to drive effective outcomes. Best practice demonstrates indeed that skill sets required in today’s work environment can be achieved if employers are actively involved in a dialogue with educators. Trainings, however, that are delivered stand-alone by companies in isolation of a country’s education system are not as effective as their reach is limited.

We would therefore recommend to further foster collaboration between the retail sector and educators through a structured framework that supervises curriculum development as well as training delivery. We have highlighted the importance of curricula to incorporate employability skills including entrepreneurship and high order thinking skills for innovation. One lever – as discussed – is to scale up vocational training. Other levers are to institutionalise critical thinking elements early on in school curricula by placing greater emphasis on creativity, innovation and the role of R&D throughout the education and training system.

Improve recognition of professional qualifications across ASEAN. There have been several attempts by various organizations to develop an ASEAN Regional Qualification Framework. However, until today, national qualification frameworks mostly prevail. To move forward, there is a need to identify major obstacles including reaching a mutual understanding between the “sending” and the “receiving” countries and identifying key players for setting up a taskforce. Also here, we recommend strong integration of the private sector and collaboration within and across ministries, and educators.

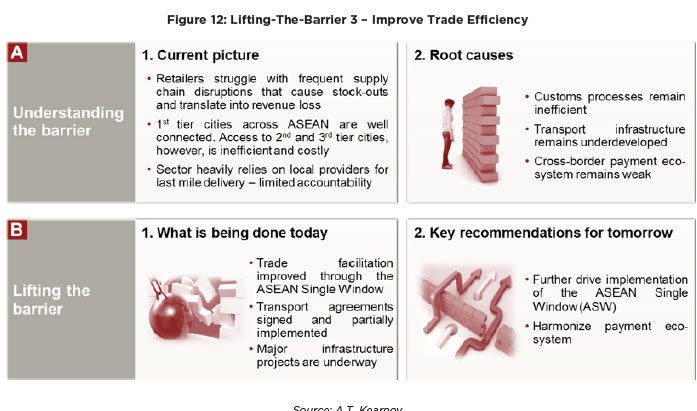

3.3 Improve trade efficiency

Understanding the Barrier

Current picture

The retail sector today faces significant trade efficiency challenges: a key area of concern is down to the burdensome and slow intra-ASEAN customs procedures. Cross-border trade flows are often slowed down due to goods being held long time in queue for inspection. Weak land transportation infrastructure is the second most important issue impacting trade efficiency, especially outside the main urban areas.

This not only drives up delivery costs and cycle times, but often leads to supply chain disruptions, which in turn directly translate into revenue loss for retailers. Minimising stock-outs has therefore become a key focus area for retailers in ASEAN – having to deal with these issues means that less resources (management time / capital) are available to drive an innovation agenda.

Root causes

Inefficient customs. One reason for stock-outs / supply chain disruptions is goods being held in customs for a much longer time than budgeted by the trade partners. Time consuming documentation and inspection requirements and different classifications of goods in different countries lead to inefficient inbound clearance processes. Multiple uncoordinated customs offices and sometimes arbitrary independent rulings by local customs offices leads to low confidence and dampens the efficient exchange of goods and services across the region and therefore significantly reduces the ability to innovate across the region.

Underdeveloped transport infrastructure. Transport infrastructure still remains underdeveloped in the region, but several projects are well underway to enhance the network. Upgrading the roads network and reducing bottlenecks in the region are the highest priorities to improve logistics in ASEAN. The lack of efficient and cost effective transportation links and associated infrastructure means it is only profitable for retailers to invest in first or second tier cities – significantly reducing market reach and dampening economic growth.

Weak cross-border payment ecosystem. As highlighted in last year’s report, a major barrier to e-commerce in ASEAN is the underdeveloped payment eco-system, especially when it comes to cross-border transactions. With many innovations linked to the concept of omni-channel retailing, an inefficient payment system precludes retailers from implementing some innovative solutions. Harmonizing existing legislative frameworks is a first step, the creation of a regional online dispute resolution facility another. These areas, however, remain work-in-progress and continue to impact retail development and innovation (especially e-commerce).

Lifting the Barrier

What is being done today?

Trade facilitation: the ASEAN Single Window. The AEC aims to create “simple, harmonised and standardised trade and customs, processes, procedures and related information flows […] to reduce transaction costs in ASEAN” (AEC Blueprint 2008). Against this backdrop, the ASEAN Single Window (ASW) has been created to address customs and administrative procedures that act as obstacles to the free flow of goods across borders.

Transport agreements signed. Intra-ASEAN connectivity has been enhanced through the implementation of transport-related agreements. Goals of the Brunei Action Plan (ASEAN Strategic Transport Plan) 2011 – 2015 include the completion of the ASEAN highway network, establishment of efficient and integrated inland waterways, implementation of the Singapore-Kunming (SKRL) rail-link. The final objective is to establish a sustainable, energy efficient, and environmentally friendly intelligent transport system.

Infrastructure upgrading projects. Many projects are underway that address the logistics bottlenecks across the region. Indonesia has e.g. increased its spend on infrastructure investments by 63% and launched several initiatives aimed at reducing overall logistics cost as a percentage of GDP from 23% to 18% by 2020. 60 new airports are for example planned across Indonesia by 2030, a move that is expected to significantly reduce delivery times to Tier 2 and 3 cities.

Key recommendations for tomorrow

Prioritise implementation of ASEAN Single Window. The ASEAN Single Window is expected to solve logistics challenges, especially difficulties with customs clearances. The ASW is a network of “National Single Windows” (NSW) – the level of readiness of the individual NSWs is therefore crucial for the full implementation of the ASEAN Single Window. The ASW as of today (2015) is still work in progress: ASEAN member countries are for example still experimenting with self-certification schemes – a legal framework agreement is being drafted. The ASW implementation has been slowed down by different priorities of each member state and the progress made on developing the NSWs. We should therefore contemplate the idea of complementing the current structure of NSWs with a strong supra-national supervisory body that tracks implementation and can overrule domestic protectionist agendas.

Harmonise payment eco-system. Developing common financial instruments, standards, procedures, and payment infrastructure enables economies of scale and would reduce the overall cost to the ASEAN economy of moving capital around the region. Improved cross-border payments will support trade flows and dissemination of innovative solutions and directly contribute to supply chains becoming more efficient. Complementary institutions / policy measures can dock to this frame like the creation of a regional cyber security or dispute resolution facility. The latter will directly contribute to the development of the e-commerce sector in ASEAN.

3.4 Promote integration of ‘Retailer Innovators’

Understanding the Barrier

Current picture

Innovation is only starting to represent a focus area for retailers in the region as the sector matures. The traditional owner-driven culture, coupled with a focus on short-term gains in a low margin environment, has indeed led to low technology adoption so far. This manifests itself e.g. in the low exploitation of data analytics and deployment of sophisticated targeted marketing.

As the Omni-channel concept is becoming more prominent, it is now critical for retailers in ASEAN to design and implement a comprehensive Omni-channel strategy of which technology and innovation are crucial components. However, exposure of ASEAN retailers to retail innovators is relatively low due to a combination of lack of support and resources and avenues to interact with “innovators”. To accelerate the development of the sector, developing incubators for retail innovation and stepping up efforts to create networking platforms is instrumental. At the same time, more can be done to further drive retailers’ appetite for innovation through coordinating innovation development efforts amongst smaller retailers, and building partnerships with international retailers that can bring retail innovations into the region. To illustrate, Singapore has developed the Retail Innovation Centre for Enterprises (RICE) in 2014. The institution aims to educate retailers by providing information as “one-stop service” on the latest technological solutions (mobile apps, management software, payment solutions, etc.). This initiative is the first of its kind in ASEAN and paves the way for further promising retail innovation developments in the region (more details below).

Root causes

Retail culture in ASEAN / short-term mindset. Retailers’ organizational structures in ASEAN tend to be rather hierarchical and often dampen bottom-up idea generation. Also, margin pressure has largely been addressed by focusing on short-term promotions at the expense of building long-term and innovation-based plans. Furthermore, retailers have often prioritised the expansion into new sites and countries to deliver against growth targets. The trend is still ongoing with retailers increasingly setting up shops in Vietnam and now also Myanmar. However, such a short term approach is not sustainable in the long-run and a shift in mind-set towards a long-term, knowledge and innovation-based model is required.

Immature networking culture. Many retail associations and networking platforms exist at the national level and increasingly at the ASEAN level, but we observe low participation from the sector. A key reason lies into the immature networking culture. The competitive environment has been characterised by taking and gaining market share (short-term top-line growth) rather than differentiation and development of unique selling positions. With the market moving Omni-channel, supply and distribution chain partnerships are expected to become the new norm and government institutions can act as trade-facilitators in this regard.

Lifting the Barrier

What is being done today?

Government agency support. As highlighted above, the Singapore Institute of Retail Studies (SIRS) has established the “Retail Innovation Centre for Enterprise” (RICE). It was set up to seed innovation and technology adoption to help retailers increase their productivity through automation and technology and overcome the manpower crunch. RICE is not an academic research institute but an innovation centre focused on showcasing the latest innovation to the retail sector and on helping the sector with applying technology to increase productivity. The centre’s main objectives are to showcase technology solutions through a one-stop approach to create greater awareness and educate retailers on the various technologies that can enhance their business productivity. It further aims to facilitate the adoption of technology through its partnership with the Singapore Productivity Centre that provides consultancy services and promotes technology adoption. Lastly, RICE offers training programs and workshops on technology through SIRS to assist retailers in the implementation of the solutions. The programs vary in level and depth depending on the sector’s requirements and are geared towards both frontline as well as management staff.

ASEAN Retail Chains & Franchise Federation (ARFF). The ASEAN Retail Chains & Franchise Federation was established in 2008 to champion the promotion and development of trade particularly in the retail chains, franchise & tourism and shopping industries within the 10 ASEAN countries + 6 countries (China, Japan, Korea, India, Australia, New Zealand). The vision is to “make ASEAN the world class tourism & shopping paradise.” The federation specifically aims to make ASEAN a hotspot for business opportunities by harnessing the collective strength of all countries in ASEAN. It falls under the auspices of ASEAN Business Advisory Council which is mandated by the leaders in the region as the official ASEAN linkage. Its objectives are to provide private sector feedback and guidance to boost efforts towards economic integration, and to identify priority areas for consideration by the ASEAN leaders. As ARFF is designated under the tourism category, it has to submit its report card of activities to the 10 leaders of ASEAN countries at the yearly summit.

Key recommendations for tomorrow

Establish a regional network of government agencies promoting innovation. Following the RICE example, similar centres should be set up across the region to create greater awareness and educate retailers on the various technologies that can enhance their business productivity. Especially SMEs would benefit from this as they are most resource-constrained. This coupled with a grants scheme will allow retailers to access consultancy services and deploy innovative technology solutions more quickly. Singapore again stands out in this area: The Info-communications Development Authority (iDA) has set up the “iSPRINT” program that provides funding for a list of packaged ICT solutions and pay-per-use applications. Another government initiative is called “Spring – Enabling Enterprise”. The program issues “Innovation & Capability Vouchers” 66 LIFTING-THE-BARRIERS REPORT: RETAIL to encourage SMEs to take their first step towards capability development. SMEs can use the voucher to upgrade and strengthen their core business operations through consultancy in the areas of innovation, productivity, human resources and financial management. Apart from consultancy, ICV also supports SMEs in the adoption and implementation of simple solutions to improve business efficiency and productivity.

At the ASEAN level, we recommend a concerted effort to establish a network of incubators / trade facilitation agencies that increase awareness and ease access to technology. Further, grant schemes targeted particularly at SMEs will accelerate the diffusion of innovative technology and solutions across the region.

Foster collaboration between innovation incubators and innovators. Creative and extensive relationships are a cornerstone of business practice. Differences in culture, market dynamics, history and relationships can translate into massive variations in the way a company should market, distribute, price and, in general, function in different markets. Although the objective of ASEAN 2015 is to create an enhanced economic and trading region, ASEAN will remain a collection of vastly different cultures, histories, politics, markets, tastes, products and people. Developing new relationships or leveraging existing ones will be key to accessing local knowledge quickly in order to understand threats and opportunities. Promoting regional retail associations and facilitating networking will directly build capabilities and foster the diffusion of innovation in the sector.

4. A GREAT OPPORTUNITY FOR ASEAN

We have seen that retail is quickly moving towards an omni-channel structure and that sustainable growth for the sector in the region is dependent on strategies that market new products & services. Additionally, creating a seamless and unique shopping experience both offline & online whilst smartly leveraging innovative enablers across the value chain (cf. figure 14) will be critical moving forward. This requires innovative capabilities not only at the retailers’ top management level but across the organization, running a successful retail operation being all about people and their know-how. Deploying e.g. advanced IT applications to optimise assortments based on incremental demand or to optimise promotion activities based on scenario analysis requires sophisticated skill sets. Tracking products along the supply chain not only requires the implementation of RFID technology but a new collaborative way of working between suppliers and retailers.

This new wealth of technologies and the available amount of ‘big data’ is a great advantage, but it requires intelligent uses to address familiar challenges such as managing shrink and out-of-stocks. Innovation is not only important but has become an imperative for all the players in the sector who want to remain competitive.

Finally, lifting the barriers that we have identified constitutes a great opportunity not only for the retail sector but for ASEAN as a whole. It will indeed contribute to GDP growth, foster AEC integration beyond the pure economic aspect and boost employment of a large workforce.

Table of Figures

Figure 1: ASEAN Retail Market Growth Forecast

Figure 2: Retail Innovation Landscape

Figure 3: Innovative Enablers across the Retail Value Chain

Figure 4: Global Innovation Index Score Results – ASEAN vs. Regional / Global Competitors

Figure 5: Low Share of Modern Retail

Figure 6: Penetration of Private Label Products in Retail

Figure 7: E-Commerce Sales as % of Total Retail Sales

Figure 8: Key Barriers to Innovation in Retailer

Figure 9: Lifting-The-Barrier 1 – Reduce Non-Tariff Barriers

Figure 10: Lifting-The-Barrier 2 – Improve Access to Talent

Figure 11: Human Capital Performance by ASEAN Country – Global Innovation Index (GII)

Figure 12: Lifting-The-Barrier 3 – Improve Trade Efficiency

Figure 13: Lifting-The-Barrier 4 – Promote Integration of ‘Retail Innovators’

Figure 14: Summary – Top Innovations Transforming the Retail Sector

![]()

RELATED REPORTS

- LIFTING-THE-BARRIERS REPORT 2014 RETAIL

- AN ANALYSIS OF ASEAN CONSUMER PROTECTION POLICY

- ASEAN NEEDS TO CATCH UP ON RETAIL INNOVATION, REMOVE NTBS AND IMPROVE ACCESS TO TALENT

- BORDERLESS BY NATURE, E-COMMERCE SHOULD BE USED AS A VEHICLE TO DRIVE ASEAN RETAIL INTEGRATION