LIFTING-THE-BARRIERS REPORT 2014 | TAX

Published date: December 2014

TABLE OF CONTENT

(Click any topic to read the related section)

- 1. Introduction

- 2. The tax impact on business

- 3. Global tax landscape

- 4. Current ASEAN tax landscape

- 5. Opportunities and risks for ASEAN

- 6. Demonstrating the potential of reducing tax complexity

- 7. Conclusion – the potential for an AEC tax agenda

- 8. Annex 1

- 9. Annex 2

IS TAX AN IMPORTANT MATTER FOR THE AEC?

1. INTRODUCTION

The Association of South East Asian Nations (ASEAN) 2007 Blueprint for the ASEAN Economic Community (AEC) envisaged an “integrated economic region by 2015” which will transform ASEAN into a single market with a free flow of goods, services , investment and skilled labour across the borders of its member countries.

The AEC Blueprint is due by 2015 and many of the targeted milestones will be achieved. The road to an integrated economic region is clearly a long one of which 2015 will be an important checkpoint. As new milestones are considered for the ongoing journey, should taxation be viewed as an important matter for the AEC, as the region continues to work towards regional integration?

The Blueprint currently recognises taxation as something to be addressed under the AEC, but there were only two specifically identified initiatives:

– Enhance the withholding tax structure, where possible, to promote the broadening of investor base in ASEAN debt issuance (item 31)

– ASEAN member countries should complete the network of bilateral agreements on avoidance among all member countries by 2010 (item 58)

There are other initiatives that have knock-on impacts to tax policies such as the reduction in tariffs on goods to achieve a single market and production base, the measures to enhance ASEAN investment climate etc.

In view of the current stages of development for ASEAN, and the new global tax landscape which is going through an unprecedented amount of change, it could be timely that tax policy plays a more central role within the broader framework of the AEC. This paper will look at the current global and ASEAN tax landscapes, as well as the opportunities that addressing tax matters can bring to ASEAN in the long-term.

2. THE TAX IMPACT ON BUSINESS

While it has been clear for many years that nations compete for foreign direct investment (FDI) through lower corporate income tax rates and other tax incentives, what is less well known is the impact of tax complexity and uncertainty on FDI and domestic business growth. It is useful to first define complexity and uncertainty in taxation.

Complexity of a tax regime may be measured in terms of the number of taxes, tax rates and tax bases, as well as the cost of complying with tax law. If a tax regime has many types of taxes requiring different information and numerous schedules to complete, complexity is increased. Increased complexity increases the cost of compliance in terms of the personnel, controls and information systems required to process and analyse the necessary data.

Uncertainty in taxation arises from complexity itself. In addition, tax legislation that is imprecise, impenetrable, or vague in language adds to uncertainty, including “grey areas” that are all too common in tax administration. But perhaps the greatest contributor to uncertainty in taxation is frequent changes in tax law or practice.

Tax compliance typically has a significant fixed cost component, thus you would expect that small and mediumsized enterprises (SMEs) face a higher burden of tax compliance relative to income. Various studies have found that total business tax compliance costs as a percentage of sales are significantly higher for SMEs. SMEs are often the driver for domestic business growth in national economies, thus it is argued that tax complexity and uncertainty should be pro-actively reduced for SMEs to unleash their potential to drive growth.

Beyond the costs associated with tax compliance, it is necessary for companies to allocate significant resources in order to navigate the tax challenges a business can face. Typically only the largest of companies are able to invest in the necessary resources to manage tax matters. Increased tax complexity is, therefore, something which is particularly challenging to SMEs.

When it comes to business investment decisions in overseas economies, there are many factors to consider.

Taxation is certainly one of these factors. The question is, how important is taxation to such decisions? Studies have shown a decline in corporate tax rates as global trade and capital flows have become more open, and this is attributed to competition for FDI. It is believed that tax complexity and uncertainty, not only tax rates, are also an important factor in investment decisions.

3. GLOBAL TAX LANDSCAPE

Government deficits are now driving a far greater focus on raising revenue. At the same time, in many countries, tax activism and media coverage is sparking broad public discussion and political focus on business taxation.

The next few years will be a critical time for business taxation; the effort to reshape the international tax architecture is a chance to avert “global tax chaos”, according to the Organisation for Economic Co-operation and Development (OECD), which has said a failure to act could result in governments taking unilateral action.

The global tax environment is therefore currently characterised by the following:

a) Tax fairness – whether companies are paying their “fair share” of taxes.

b) The growing number of countries that turn to policies that mix austerity and stimulus together.

c) A growing role for indirect taxes (E.g. GST/VAT) as governments seek sustainable ways to rebalance their budgets and stimulate growth. d) Tax transparency – the debate on taxation of multinational companies has led to a growing call for increased levels of transparency by business taxpayers; while some have called for data to be made public, others have focused on increased transparency between taxpayer and revenue body.

e) Cooperative compliance (enhanced relationships) – a framework for an “enhanced” relationship between taxpayer and tax authority. Such a relationship would be based on a working environment, processes and protocols which are based upon mutual trust, transparency and cooperation between large corporate taxpayers and tax authorities.

f) Transfer pricing continues to be a leading area of dispute for businesses. Documentation requirements are also being strengthened.

g) More aggressive tax audits with businesses experiencing a significant increase in the volume of tax audits, coupled with more aggressive behaviour adopted by tax authorities throughout the course of an audit.

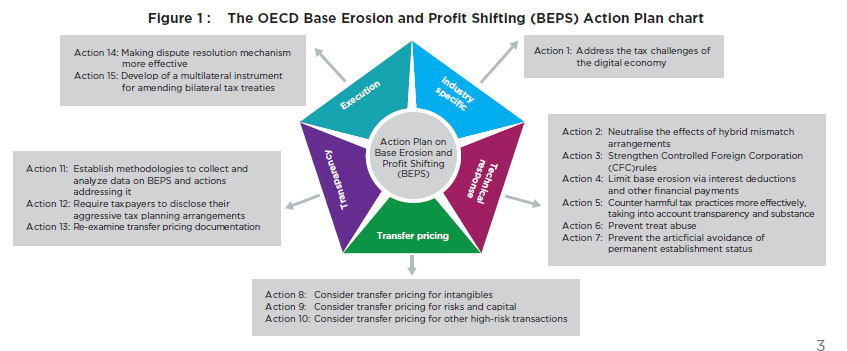

The OECD Base Erosion and Profit Shifting (BEPS) project

The OECD BEPS project, with the support of both the G8 and G20, is one of the key mechanisms being used to develop recommendations on possible coordinated action to address concerns of base erosion and profit shifting. The OECD in July 2013 released the 15 point BEPS Action Plan. The Action Plan sets out the OECD’s view that gaps in the interaction of domestic tax rules of various countries, the application of bilateral tax treaties to multijurisdictional arrangements, and the rise of the digital economy with the resulting relocation of core business functions have led to weaknesses in the international tax system (see Figure 1 for summary of the Action Plan).

The Action Plan is an ambitious document that reflects the high-level political concern about BEPS issues in many OECD member countries and proposes an extraordinary amount of work to be undertaken over 2.5 years. With the current environment being a patchwork of disparate but aggressive enforcement activities by tax authorities – now increasingly encouraged by the media and some political figures – this puts businesses at risk for both the cost of increasingly visible and expensive tax disputes and the less visible burden of unrelieved double taxation.

The changes being considered and debated by the OECD working teams will have important implications for businesses and for the global economy, and hence it is critical that businesses and governments consider how they should “get involved”.

4. CURRENT ASEAN TAX LANDSCAPE

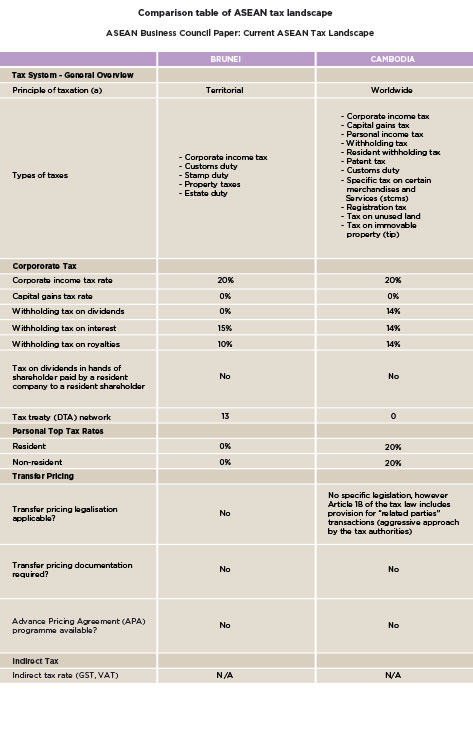

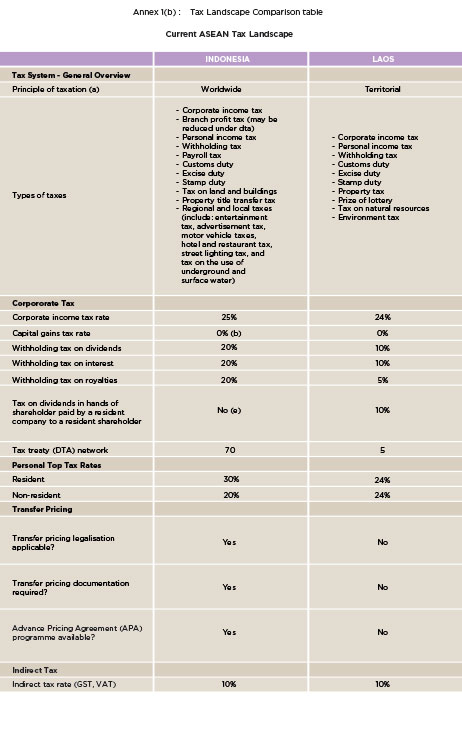

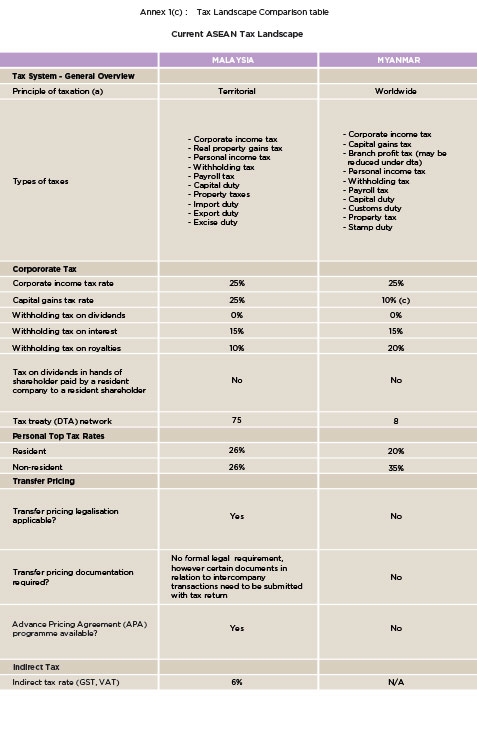

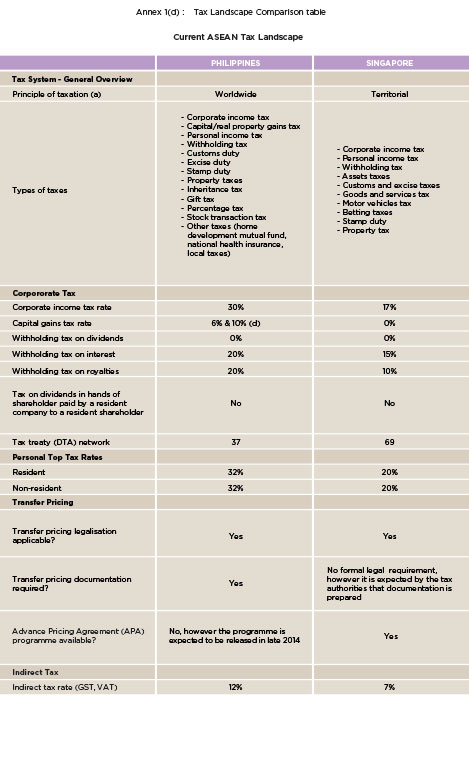

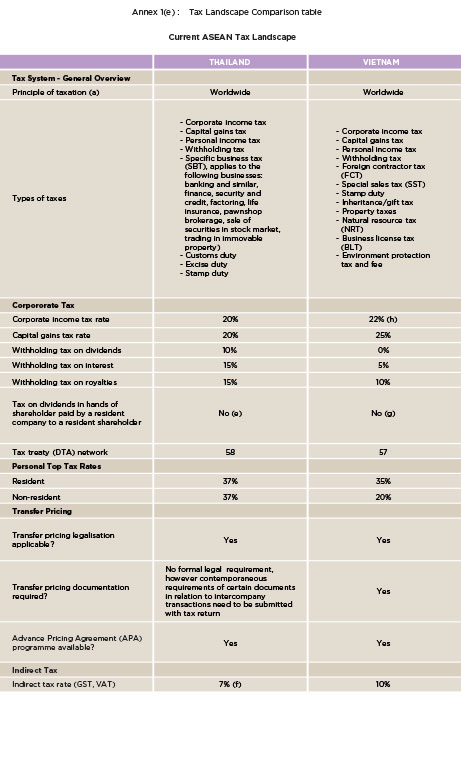

ASEAN is currently a diverse region in varying stages of economic development and growth, with 10 different tax systems in place. As can be seen from the comparison table in Annex 1, six out of the ten ASEAN countries use worldwide systems while the remaining four use territorial tax systems.

As discussed earlier in this paper, complexity of a tax regime may be measured in terms of the number of taxes, tax rates and tax bases, as well as the cost of complying with tax law. Uncertainty in taxation arises from complexity itself, in addition to legislation that is imprecise, vague or frequently changing.

Tax Systems and Types of Taxes

Within ASEAN there is currently a complex web of differing tax systems and tax types. The number of different taxes that are applicable within each of the ASEAN countries varies significantly, with Brunei having the lowest number of five tax types and Vietnam having the highest of 12 different tax types. The variance can also be seen in terms of the headline corporate tax rates of the various ASEAN countries, which range from 17% to 30%, with Singapore being the lowest and Philippines the highest.

According to data published by the World Bank Group, complexity as measured by total tax compliance hours ranges from 82 in Singapore to 872 in Vietnam. Tax systems vary across ASEAN and, particularly when taken as a whole, ASEAN’s tax regimes are clearly both incredibly complex and uncertain.

Tax Administration

Other than differences in key features in the tax system, there are also significant variances in tax administration resulting in a myriad of rules and regulations that can be challenging for investors. One example would be transfer pricing, which businesses consistently view as their most important tax concern. Rules and documentation requirements, and most importantly how these are implemented in practice, vary widely across ASEAN. Later in this paper we will use a case study example to cover Transfer Pricing in more detail.

Above all, business is encouraged and efficiency is gained when tax policy, law and administration is transparent and certain. This allows businesses to focus on business, and not find themselves trying to survive and compete on the basis of tax strategy. In ASEAN’s 10 markets the diversity of the tax systems, especially the diversity in tax administration, has the potential to detract from the transparency and certainty which business requires.

Complete tax harmonisation may be neither achievable nor desired. However ASEAN should recognise the current state of diversity as an impediment to business. Clarity in policy and law may be achieved, while leaving individual nations free to determine taxation according to the needs and customs of their jurisdiction. Standards of administration may be achieved without detracting from national sovereignty. Interpretation of cross border matters, such as tax treaty interpretation and customs valuation of imported goods, may also be agreed upon at an ASEAN level to promote fairness and transparency for all. This level of standardisation, while not being full harmonisation, may be sufficient and could be a step to increasing business investment and activity for all of ASEAN. The rapidly changing global environment and the current ASEAN tax landscape will increasingly add pressure and urgency for ASEAN tax authorities to adapt.

5. OPPORTUNITIES AND RISKS FOR ASEAN

As can be seen from the global and ASEAN tax landscape, the impending tax environment will be increasingly challenging and uncertain for companies and investors. In the context of such a landscape, what does this mean to ASEAN governments in terms of tax policies, and their ambitions towards the AEC?

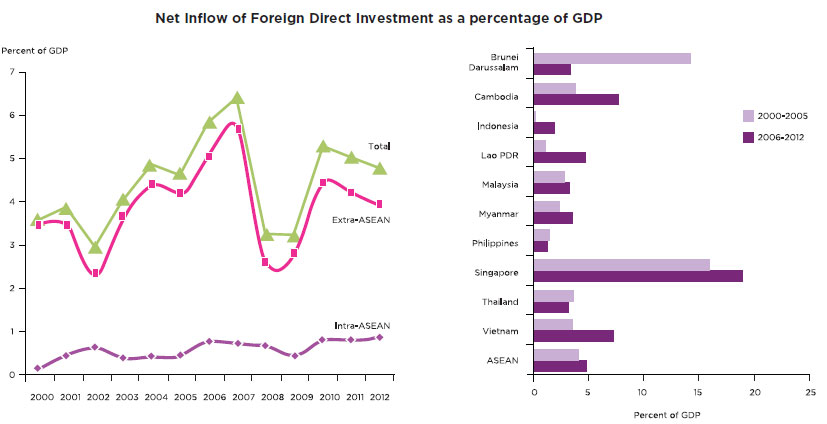

Economically, whilst ASEAN has come a long way in terms of its economic growth, with growth of 5.6% in 2012 and a 4.7% growth in 2011, the engine of this economic growth remains somewhat reliant on inbound FDI. In terms of net inflow of FDI, as can be seen from Annex 2, FDI as a percentage of GDP hovered around 5% in 2012. The highest recorded was in 2007, with FDI as a percentage of GDP reaching 6.5%.

It is important to note that while many of the global tax initiatives currently being debated are targeted at the MNCs, these tax measures, when implemented globally, could have a significant impact on MNCs’ overseas investments. For example, incentives can come under “attack” with the BEPS developments, and rules that could nullify the effectiveness of certain incentives will erode ASEAN’s competitiveness in terms of attracting inbound FDI.

ASEAN is one of the few “bright spots” of growth globally. The ASEAN Business Outlook Survey 2014 highlighted the growing importance of ASEAN, in particular for business growth potential. For example, 73% of the respondents indicated that ASEAN will become more important to their companies’ worldwide revenues over the next two years. Tax complexity and uncertainty is likely to have a significant negative impact on FDI and we should not forget the impact to SMEs that are the engine of Intra-ASEAN growth.

Any improvements to the tax environment in ASEAN will enhance ASEAN’s operating environment, streamline and reduce the cost of doing business for companies, will further increase its attractiveness to MNCs and also support domestic business growth. The AEC supports ASEAN to “promote and market” itself as a collective region to MNCs in this fierce global competition for FDI.

6. DEMONSTRATING THE POTENTIAL OF REDUCING TAX COMPLEXITY

There are many actions that could be taken collectively on taxation that would not impact a nation’s sovereign right to taxation, yet would reduce complexity and uncertainty of taxation within ASEAN. This paper does not seek to provide a definitive list of the areas where improvements to the tax systems and tax administration in ASEAN could enhance the business and investment environment. Instead we highlight two example case studies where improvements would assist business and facilitate AEC’s broader objectives:-

Case Study: Example 1 – Taxation of Business Travellers

Intra ASEAN mobility of business travellers

With increased cross border investment between ASEAN member states, mobility of people is exponentially on the rise. Such movement can take numerous forms, including permanent relocation, either prompted by the individuals or their employer, long term work assignments, short term work assignments and frequent or infrequent business trips.

It is clear that people who relocate permanently or for a formal work assignment would typically require a working permit and incur personal income taxes in the host location. With increased globalisation and the economic development of many ASEAN member states, a larger pool of frequent business travellers and ‘commuters’ has developed for whom such issues are not as clear.

As businesses expand across the ASEAN countries and cross borders more seamlessly, executives, business developers, technicians and other employees are required to travel regularly across markets, either to establish new operations, develop market opportunities, or service clients in those markets. They may travel to many countries for limited periods, or to one or two countries on a regular basis. An executive with regional responsibilities might visit a key location for a week each month as part of his or her regional role, which may trigger personal tax and immigration obligations for the employer and employee.

With this risk in mind, some companies seek to proactively monitor and manage frequent business travellers, often looking to avoid the imposition of tax by limiting the number of days the traveller spends in each location. This process is often labour intensive and can also have the effect of artificially reducing the business flows for that country. Thus there is a business cost in managing and controlling such travel, as well as an indirect cost of restricting cross-border business initiatives.

Tax treaties

A number of ASEAN member states have an extensive tax treaty network with each other, as well as with other major economic partners. Cambodia, Laos, Brunei and Myanmar however do not have such an extensive network of treaties in place (see Table 1).

The OECD model tax treaty generally allows for a resident of one member state to exercise employment within another member state for up to 183 days without incurring a host country income tax liability, provided the resident meets certain conditions. These conditions generally require the remuneration to be paid by, or on behalf of, an employer who is not a resident of the host state, and that the remuneration is not borne by a permanent establishment (PE) or fixed base that the employer has in the host location. The precise details of such protection differ per treaty. For example, the number of days, the relevant time period for consideration and other conditions can differ. To understand the precise position, each country combination must be reviewed.

Where a tax treaty is in place, prima facie protection exists if an employee of one ASEAN country works in another ASEAN location for less than the stated number of days. However, for businesses the position is more complicated than understanding the tax treatment of an individual employee. For example, in the case of a revolving group of employees working for short terms over an extended period at a site overseas, a PE may be established. In such case, the company may become liable to income taxes on its profits, and the treaty protection for employees might not apply.

Again, while the concept of PE is embodied in the OECD model treaty, the details will differ slightly per treaty as agreed.

Domestic tax exemptions

Both Singapore and Malaysia provide for de-minimis periods of physical presence in their domestic tax law. These provisions allow for physical presence of up to 60 days in that country, without incurring a personal income tax liability, regardless of the existence of any tax treaty with the person’s country of residence. Such domestic law provides a greater degree of certainty that, even though the employee may otherwise be taxable due to the provision of personal services in that jurisdiction, such income will be exempted from tax in that host country. These exemptions help to remove any doubt that a person who exercises employment for a brief time in a country might be subject to taxes on their income pertaining to that period, even where no treaty exists.

The link to immigration

Immigration and personal tax are clearly separate issues, but inextricably linked. Business visas generally allow for the holder to participate in ‘business meetings’ in the overseas location, but this broad term is not clearly defined to provide certainty of its application.

Sponsorship for a work visa will typically involve a host country employer, which in turn adds to a presumption of an employer/employee relationship in the host country.

AEC – the tax opportunity

With regard to movement of people doing business, the rules are not simple or consistent. With bilateral tax treaties (or absence thereof) across 10 countries, there are 90 different scenarios for consideration. If consistent pan-ASEAN rules were created, there is the possibility to reduce 90 scenarios to one scenario.

For example, ASEAN might provide a domestic tax exemption for business travellers between member states for a de-minimis period of 60 days per calendar year. Such exemption should apply to residents of member states or employees of businesses that are resident of member states, as many such travellers will be foreign nationals working in that state. Such a simple, consistent and transparent rule would considerably reduce complexity and uncertainty in taxation.

Similarly ASEAN member states might clarify visa requirements for business travellers between member states. For example travellers may be exempted from any work visa requirements if they exercise employment on behalf of an employer who is resident in another member state, for less than the de-minimis period in a calendar year. This would not apply to employees of a company that is resident in the host country.

A further suggestion would be that the definition of PE be refined to exclude business travellers who meet the requirements mentioned above.

Case Study: Example 2 – Transfer Pricing

Harmonisation of transfer pricing rules

Transfer pricing concerns the price at which entities transact within a group. Transfer pricing can apply to all types of transactions including goods, services, loans and payments relating to intangibles.

Every cross-border dealing has a transfer pricing impact that will be felt in countries at both ends of the transaction. Common concerns include:

- Transfer pricing compliance requirements across countries are becoming more cumbersome as tax administrations seek additional information and the information differs from that being requested by other tax administrations. This creates a resource need to meet the requirements just to demonstrate appropriate pricing.

- Where transfer pricing rules or approaches from governments are not aligned, double taxation can quickly become a concern. This is a cost to business.

- In such cases there are some avenues to resolve double taxation through double taxation agreements. In some cases these are effective, but they could be improved with more harmonisation. Alternative dispute resolution mechanisms such as arbitration may also be considered.

Even where rules and approaches are broadly consistent between the countries, the subjective nature of transfer pricing means that price setting, compliance, documentation and dispute resolution can put a strain on resources of companies.

Existing reference points

The OECD transfer pricing guidelines are the most widely-adopted reference point for transfer pricing globally. Most countries in the world consider the “arm’s length principle”, as set out in the OECD transfer pricing guidelines, to be the basis for their transfer pricing rules.

The United Nations (UN) also has a transfer pricing manual. This also advocates the arm’s length principle but seeks to provide a voice from more developing countries.

Whilst the OECD and UN can provide a framework and reference point for transfer pricing principles, these do not automatically become law; indeed the implementation of the arm’s length principle and requirements to demonstrate compliance differ considerably country-to-country.

The European Union (EU) has set up the European Union Joint Transfer Pricing Forum (EUJTPF) in an attempt to harmonise transfer pricing approaches towards methods, compliance, documentation and dispute resolution (including arbitration). This has had some success but does not yet represent harmonised implementation of transfer pricing within the EU.

AEC – the opportunity

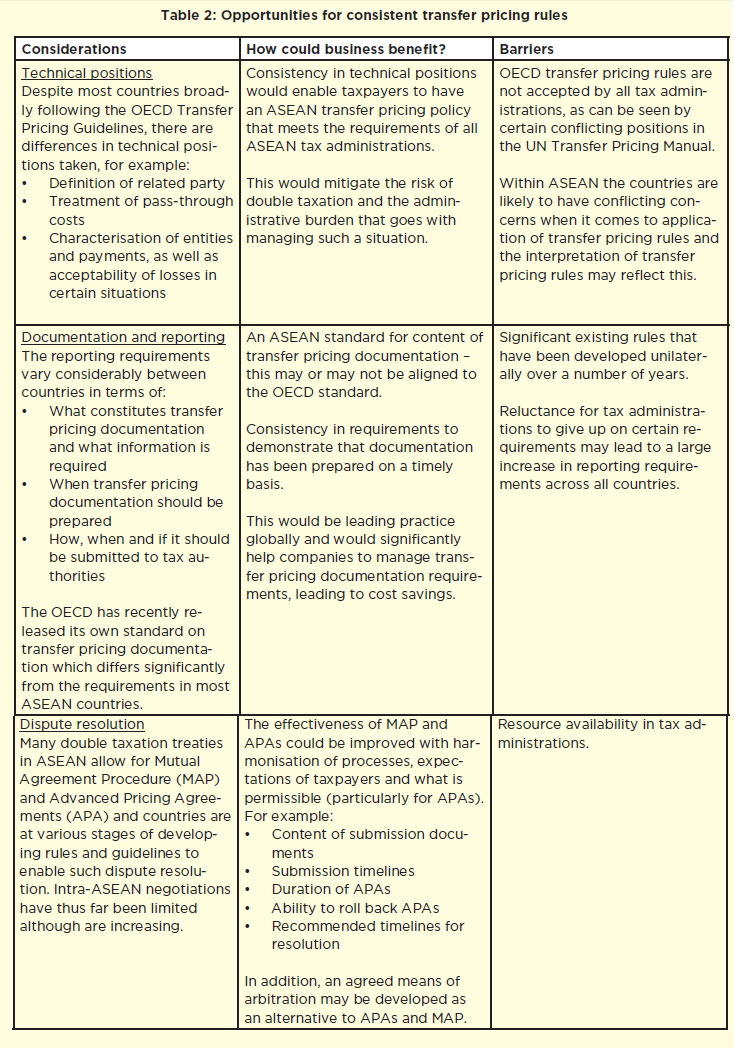

Transfer pricing has an array of aspects that could be harmonised, as described in Table 2 below. If tax administrations were able to agree on some or all of these aspects it would lead to a reduction in cost for companies with intra-ASEAN cross-border transactions within their group.

Agreement from all ASEAN countries could be sought to achieve a harmonised transfer pricing environment. Perhaps not all aspects of transfer pricing could be addressed initially, but each of them individually would improve the ability of companies to do business across ASEAN.

- The suggested first steps are: Confirmation of key areas in ASEAN where tax administrations differ in the application of

transfer pricing rules - Multilateral discussions to reach agreement on transfer pricing aspects

- Publication of a document that sets out clarification relating to these points

- Amendments to local law, regulations and guidance

7. CONCLUSION – THE POTENTIAL FOR AN AEC TAX AGENDA

For a region where FDI continues to be an important growth engine, global tax developments can have a major impact to the continued attractiveness of ASEAN. It is imperative that ASEAN’s ability to attract inbound FDI not be eroded. At the same time ASEAN needs to encourage intra-ASEAN business growth, not only for the development of the region, but to enhance its collective influence in global developments.

As mentioned earlier in this paper, increased complexity of tax systems and tax administration can place considerable resource demands upon companies. This puts SMEs at a disadvantage to large MNCs who more typically have such resources available to them. To reduce tax complexity is to support all businesses, but SMEs will be a leading beneficiary of any such reform. The case study examples quoted are only but two areas where benefits can be achieved.

A recognition from ASEAN, as part of the AEC, that tax is an important matter to business, will support the development of a framework where additional examples of tax reform can be identified and addressed.

Areas for consideration:

a) Enhancing transparency and certainty

Alignment of standards in:

- Clarity of tax policy and law

- Administration of tax, including assessment, dispute resolution, enforcement, advance rulings, APAs and overall transparency

- Interpretation of cross-border matters

Achieving alignment of standards in tax policy, law and administration across ASEAN countries would

upgrade tax transparency and certainty to encourage ASEAN business investment and activity.

b) Tax initiatives aimed at supporting intra-ASEAN business and community

For example, countries currently negotiate tax treaties bilaterally. As such, it is not uncommon to see instances whereby an ASEAN country has provided more attractive terms (e.g., lower withholding taxes) to a non-ASEAN country than an ASEAN country. Consideration could be given as to whether ASEAN countries should adopt the principle that countries outside of ASEAN will not have more advantageous tax treaty terms than those for ASEAN countries. This would help to ensure the attractiveness of intra-ASEAN investment and trade. While non-tax factors may play a more significant role in achieving this objective – such as relaxation of foreign ownership restrictions within ASEAN – tax policy should play its part.

c) Creating an AEC tax agenda

To create a specific tax agenda to be part of the AEC workstreams, this will entail a greater focus on the various tax policies each ASEAN country has in place, and will bring to light the issues that investors are currently facing. It will also allow the AEC to make a concerted effort to push for initiatives that would benefit ASEAN as a whole in terms of attracting inbound FDI. With an available tax platform under the AEC, this would provide an opportunity for ASEAN to have, where beneficial to do so, “one voice” from ASEAN in terms of inputs and contributions towards global discussions.

ANNEX 1

Annex 2

As a percentage of GDP, FDI inflows in the region was about 4.8% in 2012. The highest recorded was in 2007, reaching 6.5%. For periods 2006-2012, Singapore reaped the highest FDI inflows in percent of GDP at 19.2%, followed by Cambodia (at 7.8%), and Vietnam (at 7.3%). Meanwhile, the rest of the Member Stated posted below 5.0%.

Notes: Data for 2012 are preliminary figures; no data available for Brunei Darussalam. Lao PDR and Myanmar’s data on ‘by source

country’ are not yet available; intra-/extra-ASEAN breakdown for 2012 were estimated by the ASEAN Secretariat.

Source of data: ASEAN FDI Database

![]()

RELATED REPORTS

- AN ANALYSIS OF TAXATION COOPERATION

- REDUCING TAX COMPLEXITY IN ASEAN SUPPORTS ALL BUSINESSES, ESPECIALLY SMEs