Economic Snapshot: ASEAN Focus December 2017 | Malaysia

Published on 20 December 2017

by Michelle Chia & Lim Yee Ping, Economists, CIMB Equities & Economic Research

MALAYSIA: Shifting gears in 2018

After a dip in form in 2016, Malaysia’s economy rebounded strongly in 2017, driven by stabilisation in the commodities sector, a strong turnaround in external demand for manufactured goods, a rebound in spending by consumers and tourists, and brighter prospects in the services sector. With the low-hanging fruits harvested this year, 2018 will be time to apply the elbow grease, with renewed focus on improving domestic growth drivers and external macro buffers. Nonetheless, there is no need to fret about the moderation as it takes Malaysia’s GDP growth back to trend, to 5.2% in 2018 from 5.9% in 2017. Against this backdrop, expect the Overnight Policy Rate (OPR) to rise by 25bp in 1Q18.

Riding a crest of domestic and external tailwinds

A number of complementary tailwinds have propelled the economy to 5.9% yoy expansion in 9M17, on track to meet forecast of 5.9% for 2017 (+4.2% in 2016). The transitory drag from El-Nino-impacted agriculture output in 2016, especially that of palm oil and rubber, was supplanted by normalising production this year. Following a 5.1% contraction in 2016, output in the agriculture sector is poised to grow 5.4% in 2017, accounting for 0.8% pt or half the increase in headline GDP growth in 2017, before moderating to 2.2% in 2018, as the one-off rebound from adverse weather fades.

As a relatively open economy with total trade accounting for 138.6% of GDP, Malaysia has participated in the stronger-than-expected global trade recovery this year, with exports expanding 10.4% yoy and imports rising 12.3% yoy in 9M17. Producers of export-oriented goods, such as electrical and electronics (E&E), processed vegetable oil, rubber products, and machinery and equipment, were beneficiaries of increased external demand, lifting the manufacturing sector by 6.2% yoy in 9M17 (+4.4% in 2016). The broad trade upturn is likely to moderate in 2018 due to a more demanding base in 2017, and export growth is forecast to slow to 4.2% (+9.9% in 2017); likewise for imports (+4.9% vs. +11.5% in 2017).

While the strong rebound this year sets a tall order to beat, expect domestic demand to sustain a healthy pace in 2018, underpinned by private consumption (+6.3% in 2018 vs. +7.0% in 2017) and private investments (+8.4% in 2018 vs. +9.1% in 2017). Expect private consumption to remain supported by quickening wage growth, stable labour market conditions, easing inflationary pressure, a personal income tax cut for the middle class, maintenance of the 1Malaysia People’s Aid (BR1M) handout and higher current transfers to civil servants, pensioners and other social groups. However, household incomes will face some downward pressure when they lose access to the temporary voluntary reduction in employee contribution to the Employee Provident Fund (EPF) from 11% of gross salary to 8%, as it expires on 31 Dec 2017.

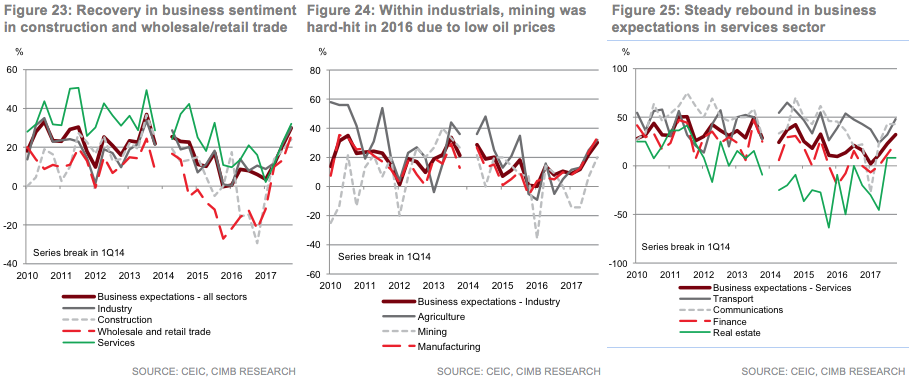

A consumption conundrum

While headline GDP and private consumption growth rates have recovered to pre- goods and services tax (GST) levels, consumer sentiment has been distinctly more muted. Data on retail sales from the industry such as the Malaysia Retail Association (+2.2% yoy in 9M17) and Retail Group Malaysia (+1.9% yoy in 9M17) appear to contradict much stronger takeaways from the official GDP numbers for retail trade (+9.8% yoy in real terms and +13.1% yoy in nominal terms in 9M17). The dissonance between survey-based data and industry estimates relative to the official national accounts may be due to to several factors: 1) a tougher competitive environment due to changing consumer preferences and disruptions to traditional retail channels by new technology like e-commerce and the sharing economy, 2) thin buffers as household savings have fallen to 1.5% of disposable income, 3) the rise in property prices, which has a redistributive effect between homeowners and potential homebuyers, 4) redistribution of incomes as a result of reforms such as the introduction of GST, subsidy rationalisation, current transfers to lower income groups, 5) other factors apart from actual consumer purchasing power and spending patterns that may affect consumer sentiment such as politics or policy changes.

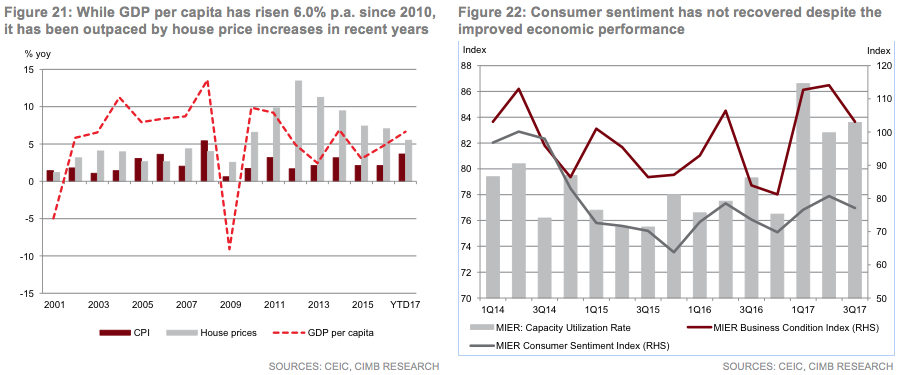

Housing burdens may have induced belt-tightening

The consumer price index (CPI) reflects housing inflation through rentals rather than residential property prices. Housing rental, according to the CPI, has grown 2.4% p.a. since 2009, trailing the 8.8% p.a. increase national house prices. However, rentals account for just a fifth (19.6%) of occupied dwellings in Malaysia while the homeownership rate stood at 76.3% as at end-2016. Real GDP per capita recorded a growth rate of 3.5% p.a. in 2001 to 2017 but would fall to 2.6% p.a. if housing rental were to be replaced by house prices in the CPI. While it is recognised that this representation likely overstates the erosion in household incomes, since it includes the capitalised value of future housing consumption, and not all consumers were homebuyers during a housing upcycle, it offers a possible explanation as to why ‘house-poor’ consumers are feeling sidelined from the stronger headline GDP growth 4.9% over the corresponding period in 2001 to 2007.

Pent-up demand and infrastructure to spur investments

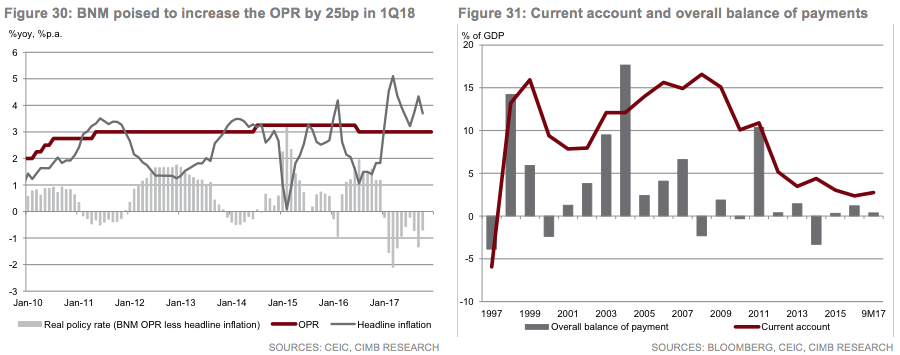

Robust external demand in 2017, will create positive spillovers to domestic investments next year. Expect the rebound in business climate and sentiment, especially in the manufacturing and services sectors, to buoy increased capital expenditure in 2018 as capacity utilisation rates climb. Renewed momentum in infrastructure investments has camouflaged the slower growth in other areas of construction, namely residential and non-residential properties. A steady pipeline of infrastructure projects tallied at RM210bn, including the MRT2, LRT3, East Coast Rail Link (ECRL), the Gemas-Johor Bahru rail line, will reinforce investment growth in 2018.

Building buffers against external risks

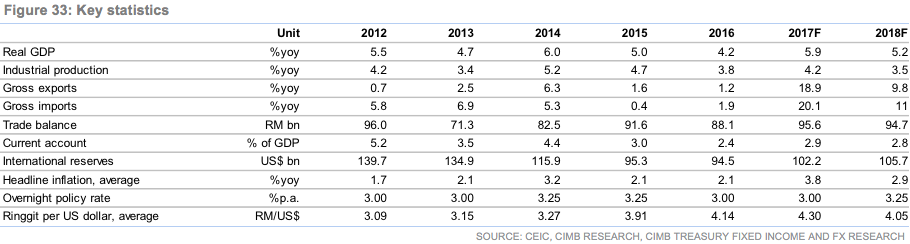

While understanding on the potential external risks posed by the monetary policy normalisation process in advanced economies, Malaysia has taken steps to reinforce its position against external risks. Despite the impending general elections in 2018, the government stayed on course for fiscal consolidation, with Budget 2018 targeting a budget deficit of 2.8% of GDP, narrowing from 3.0% of GDP in 2017. Robust trade led to an expansion in the goods surplus, expect this to lift the current account surplus from 2.4% of GDP in 2016 to 2.9% of GDP in 2017 and 2.8% of GDP in 2018. On the back of the expansion in the current account surplus and recovery in portfolio flows, international reserves have recovered to US$101.9bn in Nov from the trough of US$94.5bn during the Trump tantrum in Dec 2016, equivalent to 7.5 months of retained imports and 1.1 times short-term external debt. In addition, the exposure to foreign holders of government bonds receded to RM180.7bn or 28.8% from a peak of RM214.8bn or 36.0% in Oct 2016.

Prepped for interest rate hike

The rise in fuel prices from a low base in 2016 were a prime contributor to the elevated average inflation rate of 3.8% in 2017. As the base effects ease, expect headline inflation to moderate next year but headline inflation forecast will be raised for 2018 to 2.9% from 2.5% to factor in higher food prices, the impact of recent gas tariff hikes and uptick in demand-driven core inflation. Potential risks to forecast include electricity tariff hikes, a review of the minimum wage, additional foreign worker levies and higher oil prices.

The Nov Monetary Policy Committee (MPC) statement hinted strongly that Bank Negara Malaysia (BNM) is close to increasing its Overnight Policy Rate (OPR) from 3.00% currently for the first time since Jul 2014 as stellar economic growth this year pushes back the need for the pre-emptive cut made in Jul 2016. The base case assumes BNM will raise the OPR in 1Q18, followed by an extended pause before hiking it again in 2019F. BNM may consider a second OPR hike in 2H18 if upside inflation risks surface meaningfully beyond the forecast.

Appendix: Malaysia

Disclaimer: All rights reserved. No part of this report may be reprinted or reproduced or utilised in any form or by any electronic, mechanical or other means, now known or hereafter invented, including photocopying or recording, or in any information storage or retrieval system without proper acknowledgement of CIMB ASEAN Research Institute. The views, responsibility for facts and opinions in this publication rests exclusively with the authors and their interpretations do not necessarily reflect the views of CIMB ASEAN Research Institute.

![]()