LIFTING-THE-BARRIERS REPORT 2015 | AIR TRANSPORTATION

Published date: August 2015

TABLE OF CONTENT

(Click any topic to read the related section)

- 1. Overview – The ASEAN Single Aviation Market (ASAM) as ‘Work in Progress’

- 2. The Big Picture: The Changing Face of ASEAN Aviation

- 3. Technical Integration: Toward an ASEAN Regulator?

- 4. Economic Integration: Settling Unfinished Business

- 5 Conclusion

OVERVIEW – THE ASEAN SINGLE AVIATION MARKET (ASAM) AS ‘WORK IN PROGRESS’

The Association of Southeast Asian Nations (ASEAN) has laid down an ambitious 2015 deadline by which to establish an ASEAN Single Aviation Market (ASAM) among its 10 member states. ASAM’s goal is to liberalise air transport services in the region and to create a single integrated market for the airline industry. This is in line with the broader aim to create the ASEAN Economic Community (AEC) by the same 2015 deadline.

With the end of 2015 fast approaching, the reality is that ASAM is unlikely to be fully achieved in time (nor will the AEC, for that matter). For ASAM, much remains to be done for the economic/market integration of the aviation sector, while the work on technical/regulatory integration is still at its early stages. It is thus likely that ASAM will have to be extended, or to have a second stage declared for the post-2015 period to tackle both unfinished and new matters. In other words, ASAM remains very much a work in progress . This Report highlights the critical items that government and industry players must address as ASAM is further developed beyond 2015. In particular, the focus here is on the nascent state of technical/regulatory integration and the need to accelerate its development.

THE BIG PICTURE: THE CHANGING FACE OF ASEAN AVIATION

Infrastructure and Human Capital Constraints

- The dynamics of ASEAN aviation has changed significantly in the last decade and continues to evolve rapidly. According to calculations by the Centre for Aviation (CAPA), low-cost carrier (LCC) operations now account for more than half of all airline seat capacity (international plus domestic) in Indonesia (55%), the Philippines (51%) and Malaysia (51%). The next highest LCC penetrations rates are 38% in Thailand, 34% in Vietnam, 30% in Singapore and 20% in Myanmar.

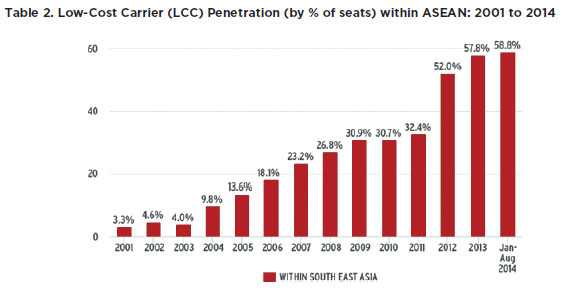

- Region-wide, the market share of LCCs on intra-ASEAN routes alone rose to 58.8% of all seats offered in 2014, up significantly from 3.3% in 2001 and 30.7% in 2010. The LCC share of capacity is expected to increase even more dramatically in the next decade, particularly for the short-haul intra-ASEAN routes. As at early 2015, six of the world’s ten busiest international LCC routes are already found within ASEAN, with Singapore-Kuala Lumpur and Singapore-Jakarta being the top two routes.

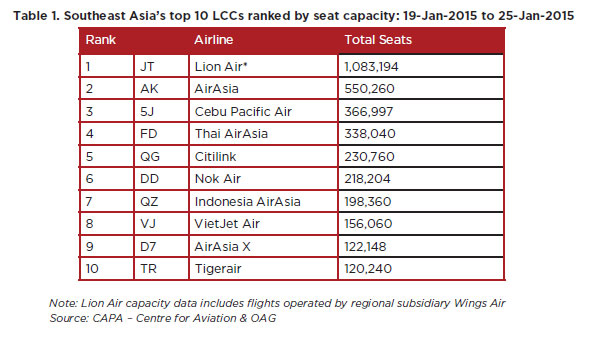

- In terms of actual seats offered, LCC capacity in ASEAN (for both intra- and extra-ASEAN flights) has increased eight-fold (800%) over the last 10 years, from about 25 million seats in 2004 to nearly 200 million in 2014. Over the same period, the full service carriers’ capacity grew by only 45%, or less than 5% per annum, from about 180 million seats in 2004 to 260 million seats in 2014. Tables 1 and 2 below show the top LCCs in ASEAN and their market penetration.

- With such huge growth rates, ASEAN aviation now faces real concerns over congestion. These concerns affect facilities ranging from terminal and runway capacity to airspace management. From the human capital angle, the challenge relates specifically to the supply of pilots, maintenance crew, air traffic controllers and other technical experts. The aircraft manufacturer, Boeing, projected in 2014 that the Asia- Pacific region alone will require 216,000 new pilots and 224,000 new maintenance personnel for the next 20 years. In ASEAN, such pressures on infrastructure and human capital have largely been caused by the huge spike in new flights made possible by the increasing economic liberalisation of the region’s skies.

- Recent huge aircraft orders by LCCs illustrate the problem. The ASEAN LCCs alone have more than 1,000 aircraft on order between them. New joint venture airlines like Malindo, Thai Lion Air, Thai VietJet Air and NokScoot have also ordered aircraft and started operations. As ASEAN airlines order more planes, the infrastructure and human capital constraints can only get more acute.

- At the same time, the regulatory landscape remains highly fragmented. ASEAN member states continue to apply their own national rules over airlines and flights in their airspace. These rules and the way they are enforced typically differ from state to state, resulting in airlines having to adhere to multiple technical standards, certifications and inspections. Regional co-operation in customs, immigration and quarantine (CIQ) procedures is also lacking, resulting in uneven rules and enforcement. For the airlines, such fragmentation increases the costs of complying with the relevant rules.

- In sum, investments in infrastructure and human capital have not kept up with the economic liberalisation that has fuelled the aviation boom in ASEAN. Neither has there been convergence in national laws and standards to create a more integrated and cost-efficient regulatory regime. There must thus be greater investments in infrastructure and human capital to keep up with the additional planes entering the ASEAN market in the coming years. At the same time, technical/regulatory integration must take place in the subsequent phase of ASAM to complement economic liberalisation. Only then can there be true regional integration for the airline industry.to have a meaningful sector integration.

TECHNICAL INTEGRATION: TOWARD AN ASEAN REGULATOR?

- Harmonised technical standards and a single regulator have the advantages of increasing the reliability of regional monitoring and compliance, reducing duplication and costs, and enhancing the overall effectiveness of aviation regulation. In this regard, the ASAM project should eventually steer the region toward creating a common ASEAN regulator to oversee technical matters. Obviously, the challenges are significant given the ASEAN member states’ concerns over loss of sovereignty as well as the disparity in economic and technical capacities among them. However, progress can be achieved in a phased, gradual manner if there is political will among governments and strong industry-government co-operation. This Report highlights the important issues that need to be addressed at the regional level in order to achieve greater technical integration.

- The initial step could be to form a body or committee comprising the civil aviation authorities of the member states (with the Directors-General of Civil Aviation presiding over several sub-committees). This would be similar to the Joint Aviation Authorities (JAA) arrangement adopted in the European Union (E.U.) in the early stages of E.U. air transport integration before the JAA evolved to become today’s European Aviation Safety Agency (EASA). A responsive JAA-type arrangement that directly involves the civil aviation authorities can complement and improve upon the current ASEAN institutional procedure that negotiates through numerous bodies, including the ASEAN Transport Working Group (ATWG), the Senior Transport Officers’ Meetings (STOM) and the ASEAN Transport Ministers’ Meeting (ATM).

- In this early stage, the guiding philosophy would be that of “mutual recognition of equivalent standards”. This means that the member states would continue to enact and apply their own national standards, but the JAA body would start working to harmonise these standards and to reduce their differences or variances so that they can be broadly equivalent (though not yet similar) across member states. The assumption here is that the member states would begin to align their standards accordingly. There could then be progressive mutual recognition of these standards across the region. This does not mean that the JAA would begin enacting common standards for all states to follow. Indeed, not being a regulator, the JAA would not have such a mandate (at least not in the initial stages). The standards would still be national standards, but they would be broadly equivalent and aligned so as to allow for mutual recognition.

- The above approach raises several critical questions as to how the effort could best be structured and pursued. These questions are fundamental and will form the basis of discussion on how the approach can be started, and more importantly, how the system will eventually end up looking like. These questions are:

- Should ASEAN aim for a unified U.S. Federal Aviation Administration (FAA)-style of regulation or a model that is more flexible akin to the E.U.’s European Aviation Safety Agency (EASA)? The fact that ASEAN comprises several countries with different regulatory systems suggests that the E.U. model might be more relevant.

- Should the initial JAA-style effort begin with a small core group of more advanced countries (e.g. Brunei, Malaysia, Singapore) seeking equivalence before extending it to the other member states? If yes, this pre-supposes a broad E.U.-style approach of harmonising standards first among a core group of countries, and then allowing and expecting the other states to come on board later (with sufficient technical assistance provided to the less developed states). The alternative is for the JAA body to develop equivalent standards at the outset for all member states to adhere to. This would be more complex and there would have to be “lowest common denominator” base levels to accommodate the differing capacities across the region.

- Beyond the structural question above, what “base” or “comparator” levels are we expecting the member states to peg their national standards to? Put another way, if we expect the certificates, licenses, permits and procedures of one member state to be recognised by the other member states, these would all have to comply with minimum “base” standards developed by the JAA. Otherwise, we cannot ensure “mutual recognition”, which can work only when there is “mutual confidence” in each other’s standards. Here, we would expect the JAA body to develop procedures for the following related areas:

- Setting out the “base” standards or harmonised regulations against which the national standards would be compared for equivalence; (again, these “base” standards could either be developed for a core group of member states first or for simultaneous application region-wide);

- The implementation of the national standards by individual member states in a manner that is consistent with the “base”

standards or harmonised regulations; - The constant monitoring of this implementation to ensure consistency with the “base” standards or harmonised regulations; and

- The provision for the JAA to recommend corrective measures and for the member states to adopt these measures

- The next issue is to identify the specific areas or disciplines of technical regulation that the mutual recognition process can cover. Here, the issues would range from relatively straightforward matters like air crew licensing to complex ones like air traffic control and airspace management. In the initial stages, the JAA body could target the following areas:

- Crew/personnel licensing and training organisations. For instance, if member states are in compliance with “base” standards on pilot training schools and certification, a pilot’s licence issued by one member state can be recognised as valid for the relevant duration by authorities in other member states. This would greatly facilitate the training and hiring of pilots across the region as well as elevate training quality. Practically, it would avoid the need for pilots to be certified by multiple states. It would also greatly facilitate hiring mobility across the region. The same approach could apply to cabin crew as well as aircraft engineers and maintenance crew.Overall, the demand for aviation professionals could then be managed and met on a regional, rather than national basis. This way, manpower can be positioned anywhere in the region as market demand dictates, with commonly-agreed certification standards recognised by all ASEAN member states. This reduces costs for airlines, governments and the individuals concerned (e.g. trainee pilots) and increases efficiencies all around.

- Safety and maintenance programmes. Similarly, if member states can enact and implement “base” standards on aircraft safety and maintenance, an inspection conducted by one member state authority would be accepted by the other member states’ authorities to be adequate and valid. To begin with, a harmonised checklist of “ramp inspection” items and procedures could be developed for all state authorities when inspecting aircraft from fellow member states arriving at their respective airports. A centralised information system could be set up to record and disseminate the results of such inspections. This information should be made accessible to all member states’ authorities so that there is immediacy and transparency in the system. Confidence in the process would then avert the need for subsequent multiple inspections on the same aircraft by other member states.

- Flight operations. “Base standards” on operations could also be developed. These would include standards on the rules of the air (e.g. general rules, visual flight rules, instrument flight rules, flight plans, right-of-way rules and communications with air traffic control), procedures on pilots receiving meteorological information, flight crew duty times, communications and navigation equipment, maintenance programmes, flight documents, responsibilities of flight personnel and the security of the aircraft against unlawful acts.

- Air Traffic Management. This is a more complex issue that even the E.U. states have not yet managed to integrate fully into a single sky with a common regulator. However, initial steps can be taken to harmonise protocols relating to flight information regions (FIRs), better coordination in “handing over” control from one FIR to another, and emergency back-up air traffic control by neighbouring states when a member state’s system fails.

- The above areas are not exhaustive and have only been set out in broad terms. Obviously, the specific procedures for each regulatory category or sub-category have to be set out and agreed upon by the member states in great detail. The next question is the precise mode for agreement. Whether the JAA approach is adopted among a core group of states first or region-wide at the outset, a formalised legal agreement would be needed to set out the mutual recognition procedure. This agreement can contain technical annexes that lay out the specific “base”-level standards for each category of regulation. It is thus recommended that ASEAN member states discuss and adopt an agreement for the mutual recognition procedure in relation to certifications, licenses, permits, approvals and other forms of documentations.

- It should be noted that many of the relevant standards have already been laid out by the International Civil Aviation Organization (ICAO) in the form of Standards and Recommended Practices (SARPs) contained in the Annexes to the Chicago Convention on International Civil Aviation (to which all ASEAN member states are party). It is the implementation of these standards that typically vary across states. Of course, ICAO also allows states to deviate from the SARPs as long as these are notified to ICAO. The reality is that some states do not notify ICAO of their deviations, and disparities become common and entrenched. A regional effort such as that described above would be useful in ensuring consistent implementation across member states.

- The role of industry is critical to such discussions. To begin with, the body that represents most major airlines, the International Air Transport Association (IATA), already possesses expertise on technical and regulatory issues. In fact, IATA recently established a voluntary safety audit programme – the IATA Standard Safety Assessment (ISSA) – for carriers such as LCCs which are typically not IATA members. While the ASEAN LCCs are not yet members of IATA, there are prospects for both sides to work together and with governments on relevant technical issues.

- This Report recommends convening an initial high-level industry meeting to bring together all ASEAN airline CEOs and IATA to discuss concrete steps for advancing the region’s technical integration agenda. If the various ASEAN airlines lead the way and find consensus on what is meaningful and practicable for their own regulation, they can then convince their respective governments to give priority to the issue. After all, technical integration benefits all airlines, be they full-service or low-cost carriers. Such agreement among the industry players can provide huge momentum for the governments to act. In other words, if the airlines can agree that they all desire technical integration, their governments will have to help them achieve this at the ASEAN level.

- In sum, for technical integration to be realised in the ASAM, it is recommended that:

- A high-level industry players’ meeting be convened to bring together all ASEAN airline CEOs and IATA to discuss advancing the region’s technical integration agenda in the manner described above. If the airlines can agree on what is beneficial for all of them, they should then convince their respective governments to help them secure this at the regional level.

- A wide-ranging “scoping” study should then be conducted to compile the various national standards that exist, to determine which are currently implemented in the member states, and to identify the material disparities.

- A Joint Aviation Authorities (JAA)-type body be established to begin the process of establishing “base” standards against which the national standards can be compared and re-enacted for equivalence.

- A legal agreement be adopted to lay out the formal procedures for mutual recognition of certifications, licences, permits, approvals and other documentations that are aligned with the relevant “base” standards. Annexes to the agreement can lay out the specific categories of regulation such as crew/personnel licensing and training organizations, safety checks, maintenance programmes, flight operations and air traffic management.

- Procedures be established to ensure consistent implementation, monitoring of such implementation and the taking of corrective measures by member states in the event of non-compliance.

ECONOMIC INTEGRATION: SETTLING UNFINISHED BUSINESS

Market Access

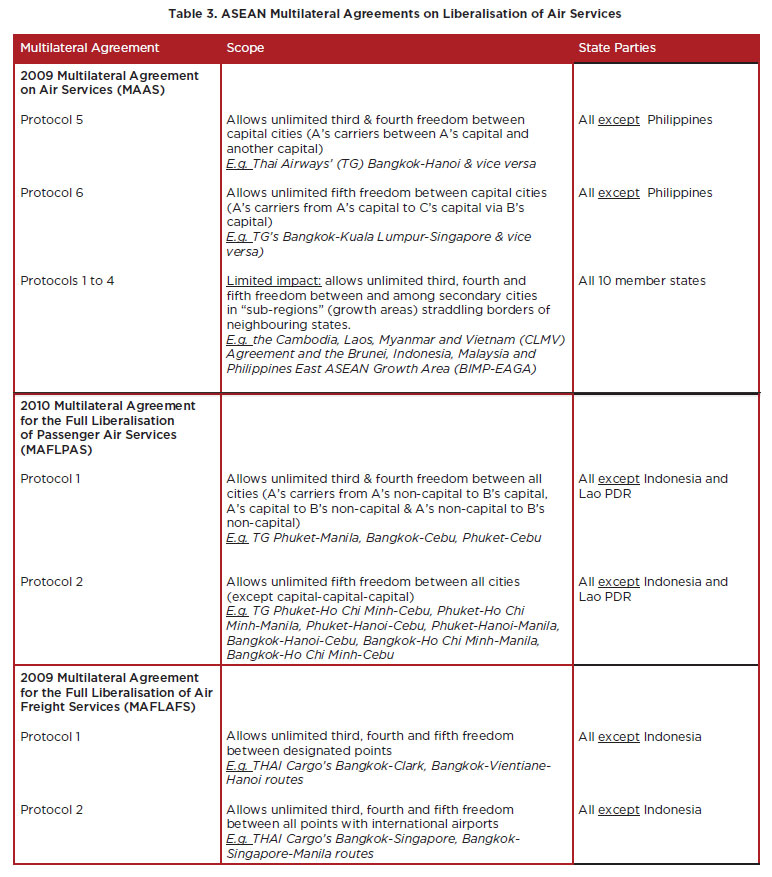

- The ASAM process of liberalising market access for ASEAN member states’ carriers into each other’s market is currently limited to the so-called third, fourth and fifth freedom rights. The table below explains the relevant existing agreements that set out these rights and the member states that have and have not

accepted them.

- As highlighted in the previous Lifting-the-Barriers Report for Aviation in 2013, it is absolutely critical that all ASEAN member states accept all the above agreements in full. At present, ASEAN airlines face capacity limits when operating passenger flights to the Philippine capital, Manila, from their own respective capitals. Similarly, flights to non-capital cities in Indonesia and Lao PDR also face capacity constraints. As for allcargo operations, flights into Indonesian points remain restricted.

- Even if all ASEAN member states were to accept all the above agreements to accord each other’s airlines fully unlimited third, fourth and fifth freedom rights, slot constraints at congested airports (principally Jakarta Soekarno-Hatta Airport and Manila Ninoy Aquino Airport) remain a huge problem. In other words, the above ASEAN agreements do not cure the slot problem. This is an infrastructural constraint that member states must resolve separately.

- In addition, even if all ASEAN member states were to accept all the above agreements, their airlines will still have to begin and end their flights in the home state’s points. For instance, a Thai carrier will not be able to station planes in Indonesia to connect Jakarta and Manila (i.e. the “seventh freedom”). At best, it can only connect Jakarta and Manila with operations beginning and ending in Bangkok, its home point. As such, it can operate a Bangkok – Jakarta – Manila – Jakarta – Bangkok route, which is a fifth freedom operation that starts and ends in Bangkok, but that enjoys traffic pick-up rights in Jakarta in both directions.

- Even then, such fifth freedom operations are controversial in ASEAN because the Thai carrier in this example would be servicing a “V”-shaped geographical route, as opposed to a linear or straight line route. The practical effect of a V-shaped route is that most or all the passengers getting on board in Bangkok will likely be bound for Jakarta (and will disembark there). In Jakarta, a full new load of passengers will be taken on for Manila. This effectively turns the operation into a seventh freedom operation, i.e. a carrier carrying traffic between two international points outside its home base. Yet, such operations are permitted by the ASEAN agreements which explicitly state that there are no directionality or capacity conditions on fifth freedom flights. Since they are wholly consistent with ASAM’s liberalising spirit, all member states should give approval when any ASEAN airline requests authorization for such fifth freedom operations.

- The seventh freedom must thus be addressed explicitly in the post-2015 period and allowed to flourish. To begin with, all fifth freedom routes, as illustrated above, must be permitted without restriction and regardless of their route “shape”. In time, pure seventh freedom routes should also be allowed – this would allow the Thai carrier to station planes in Jakarta to operate stand-alone flights between Jakarta and Manila. Just as in the E.U. common market, it is essential for a single aviation market project like ASAM to include the seventh freedom (although for now, domestic “cabotage” flights for foreign airlines remain controversial in ASEAN and should best be left for future discussion). In other words, the ASAM cannot stop at third, fourth and fifth freedom rights only. If it does, the ASAM will remain restricted and become “single” only in name.

- There are still significant barriers to ownership and control of airlines in ASEAN. Typically, all ASEAN carriers must be “substantially owned and effectively controlled” by their own nationals. This means that stakes owned by foreigners must remain in the minority (i.e. less than 50%). To address this, the ASEAN agreements have introduced the “community carrier” concept, which allows any member state to designate an airline as long as it is substantially owned and effectively controlled by one or more ASEAN member state. For instance, this means that Cambodia can designate an airline that is 40% owned by Thai interests, 40% by Vietnamese interests and only 20% by Cambodian interests. Since substantial ownership and effective control lie within the family of ASEAN interests, it would not matter that there is minority (or even zero) Cambodian interests. Of course, Cambodia, as the designating state, will still have to exercise effective regulatory control over that airline (e.g. safety and security oversight).

- The above community carrier concept currently exists only on paper. New joint venture airlines in ASEAN like Thai Lion Air, Thai Vietjet Air, Malindo and NokScoot have all employed the traditional 51:49 ownership rule, following the model of the more established AirAsia and Jetstar joint ventures. This is because the ASEAN agreements provide that the community carrier, once designated, must still obtain the consent of each member state to which it wishes to fly. In the post-2015 period, this protectionist barrier must be removed so that community carriers can be freely established to exercise all rights available to them within ASEAN.

- One way to lift this barrier is for member states to apply the traditional “substantial ownership and effective control” rule to their own carriers only, if they so wish to retain this rule. For carriers from fellow ASEAN states, the community model should be fully allowed with no risk of any member state denying operating consent. This will reassure airline investors of the community carrier’s long-term sustainability. In sum, community carriers must enjoy the confidence that they can freely and fully exercise the relevant third, fourth and fifth freedom rights within ASEAN. At the same time, the member states must ensure that their domestic laws are aligned so as to allow the establishment and designation of community carriers in which ASEAN nationals hold a majority share. Eventually, all restrictions on ownership and control by ASEAN nationals, even for member states’ own airlines, should be phased out. This is only logical if a true “single” aviation market is to emerge.

- Even if this matter is resolved, an ASEAN community carrier will only be able to fly within ASEAN. The moment it wishes to fly to another country outside ASEAN, e.g. Australia, India and Japan, it would have to satisfy the substantial ownership and effective control requirements contained in its designating state’s bilateral air services agreements with those countries. As such, another post-2015 priority is to get ASEAN member states to come together and adopt new air services agreements with third countries that recognise the designation of ASEAN community carriers. The ASEAN-China agreement already does this, and further expected agreements with other countries should contain the same feature.

- It also bears re-stating that in ASEAN’s negotiations with third countries, a limited third, fourth and fifth freedom exchange will have long-term disadvantages for ASEAN carriers. As shown by the ASEAN-China agreement, Chinese carriers can now operate from any point in China (it being one market) to any point in ASEAN. In contrast, ASEAN carriers can only operate from their own national home points (and not the whole of ASEAN) to any point in China. This is simply because ASEAN is not a true single market yet, and ASEAN member states still do not allow each other’s carriers seventh freedom rights to China (e.g. a Thai carrier being permitted to operate between Singapore and Beijing). This is another item to be tackled post- 2015 in tandem with intra-ASEAN seventh freedom rights.

CONCLUSION

- The post-2015 ASAM agenda must pursue the following items to ensure the creation of a truly single aviation market in ASEAN:

On infrastructural and human capacity

• Facilitating cost reduction and efficiencies for all airline operations, be these full-service or low-cost;

• Committing to overcome infrastructural (airport terminal, runway and slots) constraints as well as the shortage in skilled human capacity.

On technical integration

• Establishing a Joint Aviation Authorities (JAA)-type body to drive the adoption of “base” standards against which national standards can be compared for equivalence;

• Adopting a formal legal agreement on mutual recognition for certifications, licenses, permits, approvals and other forms of documentations that are aligned with the relevant “base” standards. The specific categories of regulation will include crew/personnel licensing and training organizations, safety and maintenance programmes, flight operations and air traffic management;

• Establishing procedures to ensure consistent implementation, monitoring of such implementation and the taking of corrective measures in the event of non-compliance;

• To kick-start discussions on the above items, a high-level industry meeting among ASEAN airline CEOs and IATA should be convened to identify what the airlines need by way of technical integration that would benefit all of them. These needs can then be formally communicated to their own member states and the ASEAN Secretariat so that rapid action can be taken at the ASEAN level to achieve them.

On economic integration

• Pursuing market access liberalisation beyond third, fourth and fifth freedom operations to include seventh freedom rights that take in both: (i) “V”-shaped fifth freedom operations; and (ii) stand-alone or pure seventh freedom operations;

• Lifting restrictions on “community carriers” so that these can operate unimpeded without having to secure the consent of each destination state; at the same time, the member states must align their domestic laws to allow the establishment and designation of such airlines in which ASEAN nationals hold a majority share;

• ASEAN member states need to negotiate with third countries as a unified bloc and to ensure that ASEAN community carriers are recognised for operations to those countries;

• ASEAN member states need to begin recognising seventh freedom rights for fellow member states’ carriers to operate externally (i.e. extra-ASEAN) to third countries.

Ownership and Control

![]()

RELATED REPORTS

- AN ANALYSIS OF THE ASEAN COOPERATION IN TRANSPORT

- ASEAN NEEDS TO ADOPT BASE STANDARDS ACROSS THE REGION AS FIRST STEP TOWARDS HARMONISATION

- LIFTING-THE-BARRIERS REPORT FOR ASEAN AVIATION

- LIFTING-THE-BARRIERS REPORT 2013: AVIATION