LIFTING-THE-BARRIERS REPORT 2015 | INFRASTRUCTURE

Published date: August 2015

TABLE OF CONTENT

(Click any topic to read the related section)

- 1. Landscape Of Infrastructure and Financing Sources In ASEAN

- 2. Financing

- 3. Barriers

- 4. Recommendations

1. LANDSCAPE OF INFRASTRUCTURE AND FINANCING SOURCES IN ASEAN

1. A. Infrastructure and Connectivity in ASEAN

There is common understanding that infrastructure is important in economic development and to improve welfare. Infrastructure is at the least needed to: (i) provide basic needs (electricity, clean water, transportation, etc.), (ii) facilitate the access, network, and mobility for people and products, and (iii) support and improve productivity. Infrastructure is the key for connectivity, where it connects people, goods, and services through various means.

This implies that connectivity is vital to support productivity and trade. One important example is logistics cost that determines the cost of production and thus influences the competitiveness level of location or country. The World Bank released the score card on Logistic Performance Index (LPI) that demonstrate comparative performance—the dimensions show on a scale (lowest score to highest score) from 1 to 5 relevant to the possible comparison groups—of all countries (world), region and income groups1. Out of the 2014 top 20 LPI rank, only Singapore (rank 5), Japan (rank 10), Hong Kong (rank 15), and Taiwan (rank 19) represented Asia.

Further, according to estimations by Armstrong & Associates, in 2013, the logistics cost contributed to GDPs of Indonesia, Malaysia, Philippines, Thailand, and Vietnam as much as 10.7%, while in Singapore is 8.5% of GDP2. The numbers show the significance of logistics sector to the economy and imply that infrastructure is equally important.

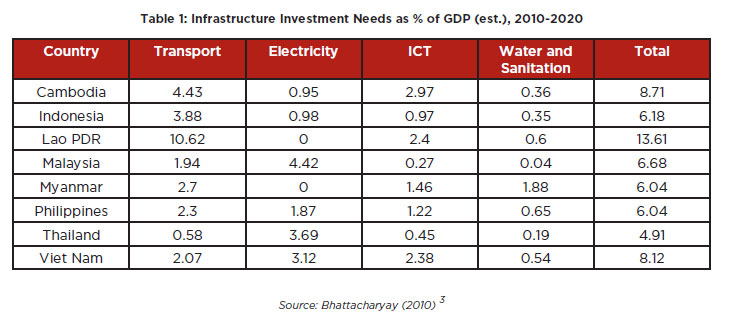

With expanding population and economy, the demand for quality infrastructure also increases. However, infrastructure is typically expensive and the general public usually view it as government’s responsibility, leading to the demand for free access. While it is not always wrong, it is also the fact that public funds are limited and public programs are competing for these funds. In developing economies it is usual that public spending for infrastructure is lower than the actual need. Bhattacharyay (2010) estimated the demand for infrastructure in majority of ASEAN state members (AMS) as shown in Table 1.

Current level of ASEAN infrastructure spending is at 3%-4% of GDP. However, World Economic Forum reported that in terms of overall quality of infrastructure, ASEAN faces high diversity (see Figure 1). For example, Singapore score is higher than those in Japan, US, South Korea, or Australia; while Myanmar is among the lowest scores in the world.

Thus, the main issues of regional infrastructure development can be categorised into two groups. The first one is dealing with domestic connectivity and sufficiency of infrastructure in each country4. This is no longer the homework for countries with the level of development of Singapore, Malaysia and Brunei; but it is a serious matter for the rest of AMSs. The second issue is the connectivity and sufficiency of infrastructure at the level of the region—where as a resilient region, ASEAN should be well integrated, including its physical terms. This report will deal with the first issues, namely infrastructure development to fulfil domestic demand.

1. B. Existing and future demand for infra projects in ASEAN countries

Indonesia estimates that during the period of the current administration (2015-2019) it needs approximately US$500 billion to build the necessary infrastructure in the country. Some estimates and compilation made by KPMG (2014) indicate that Myanmar needs US$320 billion by 2030, Thailand needs US$105 billion between 2013-2020, Malaysia needs US$100 billion between 2013-2020, Vietnam needs US$170 billion between 2013-2020, Cambodia needs US$12-16 billion between 2013-2022, and the Philippines need US$110 billion5.

The project list is not exhaustive, due to dynamism of human behaviour. Migration – especially urbanization-, changes in socio-economic status, natural challenges, technology changes, etc. will influence the quantity, types, and quality of infrastructure in demand. Infrastructure will be increasingly demanded in the future.

2. FINANCING

2. A. Sources of Financing

The demand for quality infrastructure is huge in the ASEAN region where economic growth has been robust. It is projected that ASEAN economies need to invest over US$60 billion a year in infrastructure until 2020 to support and maintain the region’s high economic growth10. However, infrastructure supply in ASEAN economies remains low relative to the needs. Except Singapore that ranks in the third position in the world, the majority of states in the region are struggling with low quality infrastructure. Infrastructure investment has mainly been funded by sovereign resources with some variations of mix financing such as subsidised semi private facilities, backed up by user fees, or supplemented by foreign aid. These traditional sources still cannot fulfil the whole demand for infrastructure investment.

Particularly after the severe Asian crisis in 1998 and later in times of global crisis in 2008, many governments’ fiscal space has narrowed due to expansionary stimulus packages to offset the impact of the crisis. With current development of strong US economy, appreciation of US Dollar against all other currencies, and anticipated higher interest rates in the US, many emerging countries including those in Asia are struggling to cope with capital flight and maintain monetary stabilization. This condition puts pressure on public fiscal space.

In addition, Official Development Assistance (ODA) will likely decline for many countries that have achieved medium income status. Infrastructure projects are also competing for donor’s funds with social sectors and projects with direct poverty alleviation impact. Therefore, with the rapidly rising demand the infrastructure deficit is expected to widen in most of the member countries. The majority of ASEAN member states, except Singapore and Malaysia, could only feed less than half of estimated demand.

With inadequate financial sources from government and ODA, the governments try to find new financing ways by inviting the private sector to participate. Private financing participation is expected to increase through Public Private Partnership (PPP) scheme, equity participation, and privatisation.

The terms of privatisation, private participation, and Public-Private Partnership (PPP) become hot issues despite the complexities to implement the programs. However, there are also success stories in improving the economy through these schemes. PPP and privatisation essentially do not only deal with lack of financial sources but enhances efficiency and improves the quality of infrastructure.

One of the market instruments to channel funds into the business is through utilisation of capital markets. ASEAN’s bond markets vary in size and have developed at different rates but are mostly dominated by government bonds. There is no specific information on the size of the portion of this fund that goes into infrastructure.

Private financing participation is also expected to increase through Public Private Partnership (PPP) schemes, equity participation, and privatisation. However, since the majority of infrastructure projects falls into the category of noncommercial business, they attract limited private financing.

The rate of PPP implementation remains slow in Asia and, in particular, in ASEAN countries. The dollar amount of PPP infrastructure projects that came to financial close, in fact, declined significantly after the Asian crisis and has not recovered. In 1997, private participation in infrastructure in the East Asia and Pacific Region amounted to US$36 billion11. After the crisis, the amount fell to a little over US$10 billion in 1998. Although it recovered to US$20 billion by 2000, the amount has since been fluctuating between US$10-20 billion. A large part of this are investments in China and Thailand.

2. B. Regional Sources of Financing

In light of enhancing regional cooperation and regional resilience, several initiatives have been developed in the region including those related to financial supply and channelling. Among those are Asia Bond Fund (ABF), Asian Bond Market Initiative (ABMI), ASEAN Infrastructure Fund (AIF, subsidiary of ADB), and the latest one: China-led Asia Infrastructure Investment Bank (AIIB).

The ABF was created in 2003 as an initiative of the Bank for International Settlements (BIS) to foster regional cooperation, promote intra-regional investment and capital market development. The ABF has achieved its early objectives including withholding tax reforms, the liberalisation of foreign exchange rules and reduction in cross-border settlement risk. Nevertheless, challenges remain including improvement in both debt and liquidity with the development of repo markets, the adoption of derivatives trading and opening the market to non-resident investors (Bank for International Settlements, 2011).

The ABMI was established to prevent resurgence of financial crisis and to promote growth. It would reduce the risks of dual mismatch in the term structure and currency in financing activities through harmonisation and integration in Asia Bond Market, aiming at strengthening regional capital market and channelling savings into the East Asia region. The ABMI was introduced in 2005 by ASEAN+3 with the support of the Asian Development Bank.

The ABMI in its early years adopted a supply side perspective with the objective of improving depth and diversification of offers. The market doubled in size between 2007 and 2013. The future development of the ABMI market includes a strategy to increase the volume of infrastructure which will offer several advantages unavailable with foreign-sourced project finance, including better diversification of project risk and investor liquidity.

The AIF is a part of the ADB that focus on financing infrastructure projects. The fund was established by contribution from ASEAN member countries and the Asian Development Bank (ADB) in 2011 agreement and became fully operational in 2013. The AIF is administered by the ADB. The initial fund size is about US$500 million (with ADB contributing US$150 million), and it is expected that the total lending from the Fund will amount to US$4 billion by 2020. Coupled with ADB cofinancing, the scheme could generate funding of up to US$13 billion.

Asian Infrastructure Investment Bank (AIIB) is a soon to be established financial institution that will focus on financing infrastructure in Asia. It was led by China’s initiative in 2013, and till the date, almost 60 countries are committed to be founder of the bank. The AIIB is expected to operate by the end of 2015 with estimated capital of US$100 billion. It is expected to significantly increase the financial supply for infrastructure investment in the region.

3. BARRIERS

The gap between infrastructure demand and supply is usually attributed to the lack of financing. It is indeed true, but the problems lie beyond the adequate financial supply. The data of global savings show there is larger potential supply than the estimated demand for infrastructure investment. The question of what is going wrong has led to the identification of critical points of the bottleneck. Of course the first thing to match is the need for long-term investment portfolio vis-à-vis the attractive projects offered. There are problems of finding good projects in the pipeline, the channelling barriers, as well as refinancing the project’s subsequent terms or expansion.

Infrastructure Financing Paradox12

- The World Bank estimates that approximately US$800 billion is being invested annually in infrastructure in developing countries (of which 40 percent goes to East Asia and Pacific), with about US $600 billion financed from government budgets; the remainder comes from the multilateral development banks (MDBs) (about US$40 billion/year) and from private sector investments (about US $160 billion/year).

- To maintain annual economic growth at 5 percent, the current annual infrastructure investment will need to double over the next 10 years.

- The Bank estimates a ‘gap’ of roughly US$1 trillion/year by year until 2020. This is the gap that cannot be met by government budgets or by the MDBs.

- At the same time, there are massive supplies of surplus capital — global savings currently amount to US$17 trillion — with investors looking for long-term stable returns. This is the ‘infrastructure paradox’. A similar paradox exists in ASEAN countries, too, where both savings rates and foreign reserves are high.

Thus the main question should not only be directed to where the money is to fund the projects, but also how can we channel the idle money to investments in real projects. Channelling is another issue that has its own complexities. Another important thing is the way to realise the investment in developing economies.

Channelling

Channelling potential financial supply is determined by hard and soft infrastructure, namely: the market and regulation. Markets work as an intermediary between lenders and borrowers. A well-functioning market exists only if it is based on good regulatory framework and run by credible regulators. Complexities in capital markets pose high risks that are typically avoided by bureaucrats; thus operating a capital market requires both knowledge and wisdom in markets and regulations. A responsive regulator is important to fix the problems and bring the policy development to the next level of maturity.

Attracting Investment

The report focuses on PPP schemes to attract investment, but goes beyond the technical issues on implementation. The potential key of success and failure of a PPP project is determined at the very beginning of the process, namely: investment planning. Before the government decides that a project would be offered as PPP project, the objectives and expectation of the project should be very clear. Thus, the first question should be: “Why do we want to buy this project?” to provide the rationale of the project.

What is the impact on the economy if we build this project? The answer from governments will provide the analysis of current situation and future forecast of relevant socio economic indicators. It also provides the expectation and targets, as well as the contradictive scenario, i.e. what if the project is not developed. This rationale will lead to the level of project’s significance. It also help the governments to have the list of projects’ priority.

The next step in investment planning is doing some exercises on different project schemes; they could be financed by public funds, fully private resources, private sector participation, or PPP scheme. All of these scenarios will provide the policy makers with the economic cost and benefit analyses to see how different schemes will have different impact. The decision to choose PPP –if PPP is the best scheme– after going through this step will enhance the project’s attractiveness and eliminate unnecessary criticisms from public. The solid arguments of the project’s scheme will also increase credibility of the government, which is very important because in PPP the government should take the leading role. Among the identified barriers, the following three issues (regulatory, market, and operational) are typically found in emerging economies:

- Poor regulatory system causes lack of private confidence, inefficiencies, delayed project implementation, weak government support, and public challenges. Common problems in regulatory issues are: conflicting regulations, poor investment planning, unclear investment procedures, changing tax regime, barriers for foreign investors, repatriation issues, barriers for foreign workers, irrelevant objectives in investment regulation, and expensive dispute settlement.

- The following issues are related with the market for PPP: underdeveloped capital market, lack of viable attractive projects, costly transaction, lack of market instruments to manage portfolio risk, and barriers for entry and exit of funding flows. Some of these issues are shaped by regulation; however, having good regulation is necessary but not sufficient. Implementing good regulation by credible and capable regulators is much more important.

- Operational issues: inadequate local partners, unarranged flows of deal, lack of capability, high cost economies (high cost of logistic, labour, and input), the absence of arbitration facility, and weak contract enforcement.

In short, the crucial issues in PPP implementation are very much related with the host country’s regulatory framework and the capacity of the government to manage and lead the project execution. ERIA’s studies in ASEAN implementation of PPP have confirmed the following key points:

a. Sufficient and coherent regulatory to provide investors with adequate confidence level and proper access to respond accordingly. Low risk perception will bring lower costs offered by private entities, thus will benefit the host country.

b. A strong and capable public sector, to lead the whole process and ensure fair risks sharing and competition.

c. A sufficient mechanism to provide inexpensive ways to channel the funds, access to financial sources, dispute settlements, and refinance the project. If the country’s capital market is not mature enough to provide the above financial functions, the access to regional/foreign capital markets and good mechanism to utilise relevant products will also work. An efficient and inexpensive dispute settlement is equally important.

Some countries may need to do reform and enforce a new way to provide conducive environment to implement PPP. It is important to note that regulatory reform does not mean to make additional regulations; in many cases, deregulation can be success key to rid the overburden caused by existing regulations. In short, the government should understand the nature of the private sector, i.e. profit-oriented institutions; and the government should be able to find the balance between public and private interests.

4. RECOMMENDATIONS

Further, some efforts could be devoted to address the following issues:

a. Provide or expand the market for long-term credit. Government should check the regulatory framework within which the capital market is regulated. Some regulations may need to be revised, adjusted, created, or eased/deregulated to facilitate funds channelling from the financial institutions into infrastructure projects. An example of typical barriers is regulations that treat insurance funds similar as bank savings, which in nature they are very different.

b. Widen the access for cross border financial flows especially for infrastructure financing. The infrastructure projects are safer in terms of vulnerability and uncertain capital mobility that many governments fear.

c. Establish a dedicated unit (especially for the case of PPP) that functions to speed up and streamline the process, communicate with potential investors professionally, and address the underlying problems such as how to offer good projects. To be well functioned, the unit should be equipped with competent experts and authorised officers, sufficient access and power to make appropriate decisions, and legal framework to secure and allow progressive movement.

In other words, the private sector has to actively participate in nurturing the market and supporting the public sector accordingly. Among crucial things are maintaining good communication with the host country’s government, willingness to involve local partners (even though there is no obligation), recruiting and transferring knowledge to local experts, and valuing the environment (with or without regulation). In the long run, if the local market is well developed, there will be higher opportunities and costs reduction to do the business in the host country.

Endnotes

1. The logistics performance (LPI) is the weighted average of the country scores on the six key dimensions:

1. Efficiency of the clearance process (i.e., speed, simplicity and predictability of formalities) by border control agencies, including customs;

2. Quality of trade and transport related infrastructure (e.g., ports, railroads, roads, information technology);

3. Ease of arranging competitively priced shipments;

4. Competence and quality of logistics services (e.g., transport operators, customs brokers);

5. Ability to track and trace consignments;

6. Timeliness of shipments in reaching destination within the scheduled or expected delivery time.

2. Amstrong & Associates (2015) (Accessed 17 July, 2015)

3. Bhattacharyay, Biswa N., 2010. “Estimating Demand for Infrastructure in Energy, Transport, Telecommunications, Water and Sanitation in Asia and the Pacific: 2010-2020,” ADBI Working Papers 248, Asian Development Bank Institute.

4. JICA-Bappenas (2013, unpublished)

5. An overview of infrastructure opportunities in ASEAN

6. Singapore Kunming Rail Link

7. ASEAN Power Grid

8. ASEAN Highway Network

9. Trans-ASEAN Gas Pipeline

10. In 2009 dollar. Asian Development Bank 2009.

11. Data are from the World Bank and PPIAF, and uses figures for East Asia and Pacific countries.

12. Moving MPAC Forward: Strengthening Public-Private Partnership, Improving Project Portfolio and in

Search of Practical Financing schemes (Shishido, Sugiyama & Zen, 2013)

RELATED REPORTS

- LIFTING-THE-BARRIERS REPORT 2013 INFRASTRUCTURE, POWER & UTILITIES

- ASEAN NEEDS TO PROVIDE THE RIGHT ENVIRONMENT TO MAKE PRIVATE INVESTMENTS IN INFRASTRUCTURE MORE FEASIBLE

- LIFTING-THE-BARRIERS REPORT FOR ASEAN INFRASTRUCTURE, POWER AND UTILITIES