Economic Snapshot: ASEAN Focus May 2017 | Economic Outlook

Published on 24 May 2017

by Dr. Arup Raha, Chief Economist, CIMB ASEAN Research Institute

Accidental bears

I was tempted to start this piece with a Dickensian “best of times, worst of times” quote but suspect it has been greatly overused. I will simply note that after nine long years it appears that the global economy is recovering from the GFC (Global Financial Crisis) but I will also note that rarely has there been such policy uncertainty, particularly on some issues that the global economy has long taken for granted. Also, geo-political risks, particularly in Asia, are escalating in a manner I haven’t seen for some time.

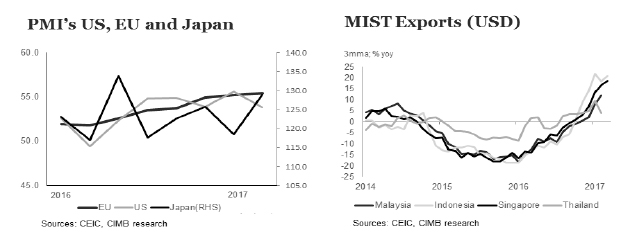

The good economic news has mainly been in global manufacturing and trade and has been backed up by improving consumer and business confidence. Moreover, starting in 2H16, growth has been geographically broadening. ASEAN’s exports have benefited.

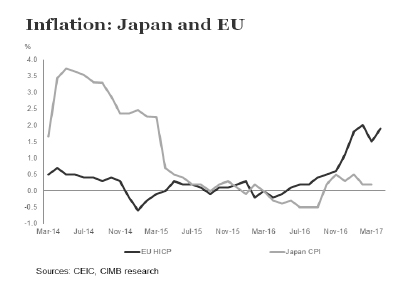

Both Japan and the EU have done better than expected. Japan has seen a boost in its net trade while countries in the EU such as Germany and Spain have seen a firming up of demand. The IMF expects Japan to grow at 1.2% and the EU at 1.7% in 2017. Moreover, the UK is showing little signs of being weighed down by an impending Brexit.

There has been an improvement in a vast array of indicators in Japan and the EU. Perhaps, most importantly, employment growth has improved and deflationary pressures have abated. A good growth outcome is expected this year with both economies matching, if not exceeding, their 2016 growth rates.

However, structural issues, namely demographics and productivity, are likely to constrain how fast Japan and the EU can grow. So, while ASEAN can look forward to slightly higher growth rates for the EU and Japan it will not be a game changer. For Europe, the average growth rate has been declining every decade for the last 50 odd years and it has been a somewhat similar trajectory in Japan. It is quite unlikely that either economy will provide significant upside on growth on their 2016 growth performance in 2017. The optimistic end of forecasts have the EU growing at 2% and Japan at 1.2% in 2017.

The onus of providing the “delta” on external demand then falls on China and the US. For ASEAN, if all goes well, the optimistic economic story then unfolds is as follows: As trade recovers and manufacturing grows there is a need to add capacity and so investment grows which, in turn, leads to more trade, rising incomes and hence consumption growth. That then entails a need for more investment and so on and so forth. Is it likely?

The reflation trade: A pause or is it over?

Before I get to the medium-term picture, let’s address a shorter-term issue on the so-called reflation trade. The expectation of global reflation started in earnest in July last year as it became obvious that China was going to exceed growth expectations. A further boost came in November when Donald Trump won the US presidential elections, stoking expectations of considerable fiscal stimulus and deregulation. These expectations manifested themselves in higher US bond yields, a stronger dollar, and firmer commodity and equity prices, leading perhaps to higher inflation.

For ASEAN’s emerging markets, these developments meant the pressure of outflows and hence weaker currencies. It also raised the specter of higher inflation – via both higher commodity prices and weaker currencies, effectively ending expectations of any further rate cuts in countries such as Indonesia and Malaysia.

Since January though, a large part of these expectations have started getting rolled back, with various prices starting to head to where they were before the US elections. The question is whether this retracement is merely a pause in the market’s belief about reflation or whether it is permanent.

The two most common explanations for the pullback are: (1) markets have become increasingly skeptical of just how much of Mr Trump’s economic agenda will actually come to pass; and (2) the familiar “risk-on, risk-off” phenomena moved to a risk-on phase as French election results got discounted and money sought riskier assets.

The lack of belief in the passage of Mr Trump’s legislative agenda seems to have been crucial in this regard. It reduced concerns about future deficits and also inflation. Not only did bond yields come off but so did inflation expectations, resulting in more dovish expectations about the Fed’s actions. The “risk-on” bit caused money to return to emerging markets.

How either of these will progress is difficult to predict but it looks likely that Mr Trump, fiscally speaking, is unlikely to be able to fully deliver on his election promises. Or, at least, he is unlikely to deliver them in the near future. At the time of writing, the “repeal and replace” of the Affordable Care Act (ACA) has narrowly cleared the house and now goes before the senate. If the pundits are to be believed, there is still a long road ahead.

While the ACA has little direct economic impact on ASEAN, it does affect the likelihood of other bills, such as tax reform, passing and that affects ASEAN. As “repeal and replace” works its way through both houses of Congress, markets are assigning a lower probability to a passage of the rest of the legislative agenda.

The markets appear to be signaling that tax reforms are unlikely in the near term as is any kind of infrastructure bill. In short, not much stimulus is expected. In the event it does happen, the markets will be surprised.

If the markets are now discounting that a Trump stimulus is unlikely, or at least uncertain, in the near term, then the next appropriate question is whether they are also signaling a more cautious growth outlook than what was originally believed. Are markets losing faith in the likely performance of the economy? The answer to that question will tell us whether the retracement is a pause or if the reflation trade is indeed over.

No ordinary recession and the divergence in data

At the initial stages of the recovery, the news was all good with manufacturing and retail sales rising, wage and inflationary pressures coming back, and external trade doing better. More recently there has been a divergence in hard and soft data; soft data being surveys and hard data being actual prints. PMIs and measures of consumer and business confidence have been rising but, as 1Q GDP numbers from the US indicated, these increases have not manifested themselves in actual expenditure.

US 1QGDP grew at 0.7%. While this number has issues with measurement, in particular with seasonal adjustment, and inventories played a larger-than-expected role, it is worth noting that the growth rate was the worst in 3 years when similar measurement problems were present in 1Q data. Moreover, it came in below the expectations of those who were very familiar with the measurement issues. So, while the number was perhaps not as poor as it appears on the surface, it was still a low number.

Of course, the 1Q clip is expected to be transitory as duly noted by the Federal Reserve in their May meeting. True, nobody expects another recession and there is consensus that the US economy should do better in 2017 than 2016. The debate is about the robustness of the recovery. Does one believe the soft or the hard data? I lean toward the latter; in my belief, any recovery should be mild.

The last few years have been unusual for forecasters. They have regularly downgraded expectations and yet, each year, actual growth rates have fallen short of even these diminished expectations. Things were indeed unusual. For example, despite interest rates going to 0%, we never saw inflation. Or higher fiscal deficits never resulted in higher bond yields.

This was more of a “balance sheet recession” or “secular stagnation” where nominal interest rates, while zero, were still too high to revive growth. A balance sheet recession meant that as asset prices collapsed during the GFC, economic agents – mainly consumers – took a hit on their net worth. So, even as interest rates went low (an occurrence that would normally reduce savings and revive consumption), people actually saved more as they felt the need to rebuild their net worth. Given a zero lower bound, nominal interest rates could not go low enough to actually revive consumption growth.

For companies, in the early days after the crisis, this meant more retained profits as they feared a liquidity crunch. Later, investment remained curtailed as there was a lack of demand. As utilisation levels remained low, there was little need to add capacity. Further, the rise in digitization may have may have permanently reduced the need for traditional investments.

A modest recovery

This change in savings behaviour may, in part, explain why soft and hard data are diverging. Consumers being confident now does not elicit the same response as it did a decade ago; behaviourally people are spending less. To get the old consumer behaviour back, we need even greater confidence than we did before and that means greater increases in real wages and productivity. I will get to that later. For now, if my thesis is correct, it means somewhat more sluggish consumer behaviour despite increases in confidence.

There are at least a couple of other reasons why the recovery may be mild. First, there is the presence of debt in the system. After the initial increase after the crisis, household debt to GDP has been coming off but to a large extent it has been replaced by government debt. While government debt does not carry the same headwind as private debt, it can, nonetheless, inhibit a policy response. Mr Trump’s tax reform/cutting agenda may run into trouble with the deficit hawks within his own party.

The story does not end there. Rising public debt is essentially a trade-off between short-term stimulus and medium to long term debt servicing and its possible effects on growth. A paper from the IMF shows that while the focus is often on debt levels, it is not as important as the direction in which debt is headed. Rising public debt levels have a negative relationship with long term growth1. As such, while a stimulus may be fine in the short term, it needs to accompanied by a fiscal stability plan. Moreover, the deficit spending should preferably be directed toward increasing productivity.

There is also risk from corporate debt. While debt-to-equity ratios have been falling, largely due to rising equity values, corporate debt has been rising. The IMF points out that $7.8 trillion of corporate debt has been added since 2010 and about 10% of it is vulnerable to rising rates2. In short, stimulus has to be applied very carefully so as not to spook the bond markets.

Besides debt, there is a supply side constraint on how fast the economy can grow. Productivity growth has been languishing, indeed declining; firmly stuck below a growth rate of 1% since 2011. Some of this poor productivity growth could have compensated for if there were significant unutilized resources in the economy that could be pulled into the production process. But with the unemployment rate at 4.4%, there is little slack in the labour market. In short, with the economy near full employment and with productivity growth being poor, that effectively means there is a supply side imposed ceiling to the economy’s growth rate.

This growth ceiling, under the Congressional Budget Office’s (CBO) base case assumptions, is at 1.8%. It also fits in well with the FOMC’s (Federal Open Market Committee) long term growth projections of between 1.6%-2.2%. Of course, the economy can grow faster than that in the short-term but it will likely be inflationary, which means the Fed will come into the picture with more a accelerated glide path on interest rate increases.

The nature of policy measures will be crucial. Even if there is stimulus, it should be directed toward productivity-enhancing measures, such as deregulation or investing in infrastructure to ease the supply-side constraint on growth. For now though, a growth rate of around 2% is the most likely scenario.

Fleeting Issues

The positive case of ASEAN usually starts with a belief that external demand is likely to get a boost this year. Sure, export growth is unlikely to be as poor as it was in 2016 but expecting a robust rebound may actually be an accidental bear case.

I have argued above that the “delta’ on growth in advanced economies is likely to come from the US. Moreover, this improvement is likely to be modest. If fiscal measures try for a short-term boost above the potential growth rate of around 1.5%-1.8%, then given the current state of the economy, inflationary pressures are likely to build up and make the Fed more active than currently assumed. That would lead to higher policy rates as well as firmer long term bond yields. There would also be further pressure on longer-term bond yields from rising deficits.

None of this would bode well for ASEAN as currencies would weaken, rates would be under pressure to rise and domestic demand would come under pressure. Currently, the region is benefitting from capital inflows but if US rates rise aggressively it is possible that could reverse causing stress in financial markets.

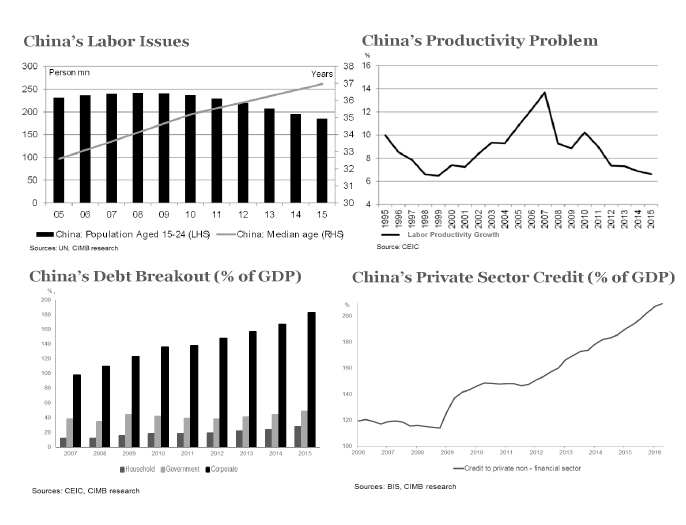

Another way in which ASEAN’s export growth could benefit is if China maintains its recent growth uptick. However, if we look one step beyond the obvious, this too is an accidental bear story. China is in a structural slowdown. Besides issues of a debt and capacity overhang, productivity growth is slowing, the demographics are worsening and the return on assets is falling. The recent growth uptick has been credit- fuelled and is unlikely to sustain itself. The “bullish” story implicitly assumes that it is sustainable, thereby inadvertently calling for a greater credit bubble and perhaps a quicker, and harsher, day of reckoning.

China’s debt level has always received a fair amount of attention, from commentators, analysts, newspapers, think tanks, multilateral institutions, pretty much everyone. The problem is largely with corporate debt and there is clearly an issue. While estimates differ on the magnitude of debt (by some estimates total debt to GDP being close to 280% of GDP and corporate debt being more than half of that) there is near unanimity that it is high.

Work done by the IMF, based on BIS data, looking at credit gaps is perhaps even more revealing. Between 2009 to 2015, the nonfinancial private credit-to-GDP ratio (including credit to local government financing vehicles rose from around 150% to 200%. This is 20-25% percentage points higher than what would have been under a normal trend. A look at other countries, where similar credit gaps showed up, implies a painful adjustment lies ahead.

The chart below comes from the IMF5.

The debt issue is well known. But from a markets perspective it only becomes problematic if an unruly adjustment is imminent. To some extent, markets may have started signalling that they would like to see an “orderly” adjustment. According to IIF data, China faced outflows of $725 billion in 2016 despite exceeding growth expectations, thereby meaning that the markets were more concerned with stability than growth6. This was also the message that came out of the CEWC (Central Economic Work Conference) in December 20167. Moreover, credit conditions are now tightening; the SHIBOR (Shanghai interbank overnight rate) is currently hovering over 2.80%, a level not seen since April 2015.

In any case, indications are that growth is moderating with the both the manufacturing and services PMI slowing in April. I expect the softening of China’s GDP growth in the second half of the year and it’s consequent damping effect on ASEAN trade.

The bullish case on ASEAN trade implicitly assumes the opposite, that Chinese growth will sustain. That implies that credit growth will also continue unabated, which in turn implies the worsening of what is near-unanimously acknowledged as a bubble. Thus the bullish case is, in reality, an accidental bear case.

There is one huge positive in China’s growth story that is often missed out and that is political stability and hence consistency of economic policies. While there may be an occasional deviation from the script as we have seen with the boost in credit or with capital controls, these are largely short term measures to cushion the impact of medium to long term policies. The commitment to economic rebalancing, greater internationalization and a greater reliance on the market in domestic matters is likely to remain intact.

The reason for this stability is actually economic. The rise of populism in Europe and US, with profound consequences, has its roots in rising inequality. In China, income distribution have gone the other way. While inequality rose in the early days of the reform process, which started in 1979, the last decade has seen a turnaround and inequality has declined as urbanization has grown and rural labour markets have tightened. Regulations on minimum wages and improvements in social programs, such as rural medical insurance and social security, have helped8. In short, this is a slowing, but stable, China.

Risks – uncertain policies; unknown players

Besides all this, the reader may have noticed that in my entire argument, I have yet to mention risks. In short, the case for caution goes through without appealing to uncertainty. But, of course, there are risks.

Start with the two obvious ones: macro-policy especially toward international trade; and geo-politics. These have been much discussed in the past and I will leave it there for now. My scenario recognizes the risk but does not explicitly include a possible trade war or a serious incident on the Korean peninsula or in the Middle East.

There is also the risk of a financial problem in China. As argued above, while I recognize the excess in credit, I don’t think a problem is imminent. In any case, if there was a problem, I hardly think that the authorities would stand back and let it happen. They would use all their financial resources and policy tools to fight back and, need I add, the resources are substantial. A serious financial incident in China is unlikely in the near term.

But I do see another kind of financial risk. There are likely to be some discontinuous changes in monetary policy with the ECB perhaps accelerating the rate on tapering and the Fed starting to shrink its balance sheet. Both are possible by the end of the year and the outcome of these measures in uncertain. Add to that the run up we have seen in US equity prices9 and there is clearly a risk of a correction if monetary policy gets it wrong. Actually, there is a risk of a correction even if monetary policy gets it right. In the event, to state the obvious, the effects will be worldwide. I will leave it at that.

ASEAN Trade – how much can the cycle do?

As argued above, any recovery in the global economy is likely to be modest and that essentially means that ASEAN trade is likely to settle down soon with the growth rates of the past few months unlikely to be repeated in the second half of the year.

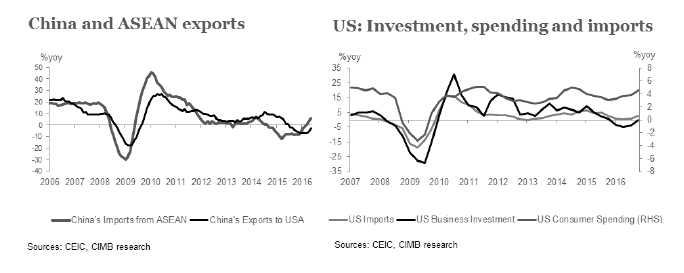

On cyclical grounds trade isn’t even really about global growth per se but more about business investment, which tends to be much more import intensive. While there is a bounce in investment in the US in 1Q, this variable tends to be volatile and there have been increases before that were not sustained. In my view, we are going to need the recovery to gather more steam before capital commitments are made. So, while business investment will ultimately recover, it may take some time. Public investment, or infrastructure spending is, at best, a 2018 story.

Investment demand in China poses an even greater hurdle. Besides being targeted as part of a policy-induced slowdown, it is also becoming less import intensive. Work done by the WTO (World Trade Organization), looks at the import intensity of growth and finds that the import content of Chinese investment spending fell from around 30% in 2004 to 18% in 2014 as China sourced intermediate goods domestically. That implies weaker ASEAN trade on structural grounds.

Compared with the boom days of the past, China is likely to provide headwinds to ASEAN trade in a variety of ways: it is slowing; it is rebalancing away from the more import intensive activity – investment – to a less import intensive activity – consumption; and even its more import intensive activity is getting less import intensive as the onshoring of intermediate inputs is picking up. Add to that, the lethargy of investment demand and the maturation of supply chains, this reduction in trade flows is a worldwide phenomenon as the ratio of world trade to GDP had declined meaningfully. In 2016, it stood at 0.6 and has been less than 1 since 2011.

Even under a relatively robust global growth scenario, trade is unlikely to be the driver of growth that it once was for ASEAN. There are too many structural headwinds. That said, we have come off about 18 months of negative export growth before the recent pick up. While commodity prices are softening, they are higher in year-on-year terms adding to growth in value terms. As such, the moderation in trade may take a few months to show up in the numbers.

ASEAN: If not trade, then domestic demand?

The other common belief is that domestic demand, in particular consumption, will drive growth in particular countries, not only domestically but will provide an additional boost via intra-ASEAN trade. I have addressed this in detail before and in my view the reliance on the consumer is misplaced10.

First, I note that domestic consumption is largely not driving growth in ASEAN. While consumption is strong in the Philippines and Vietnam, that has more to do with overall GDP and income growth than a rising share of consumption to GDP. And consumption is strong because of income being generated from other sources.

Second, where consumption to GDP is rising, say Malaysia, it has more to do with trade’s share declining than robust consumption growth. Here too consumption demand is steady but it is not driving growth.

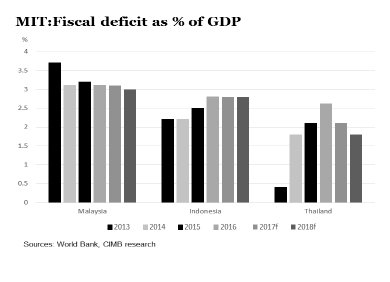

That then leaves investment and mainly public investment. In this regard, ASEAN is doing well and governments in Indonesia, Malaysia, Philippines and Thailand all have extensive plans to boost infrastructure, while still maintaining fiscal stability. Over the long term it should boost productivity and improve growth potential but in short-term it is unlikely to change the growth trajectory. The prime example is perhaps Indonesia whose fiscal management has been exemplary and infrastructure development has been seen as the next driver of growth. Yet, growth is stubbornly hovering around 5%. In short, the right policy moves are being made but the results may take time. That is likely to be in story in other ASEAN countries too.

Moreover, there is little fiscal space to provide a meaningful boost in other ways. Yes, Thailand has space and some of it is being used and Malaysia has increased transfers to the poor but they are more safety nets rather than drivers of growth.

Currencies and Rates:

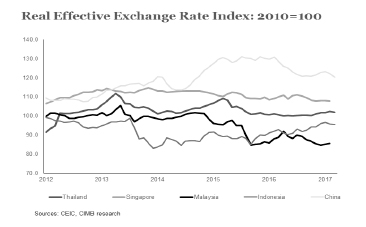

I’ve addressed the shorter-term currency outlook earlier in this piece, recognizing that emerging market currencies are being driven mainly by US dollar weakness. And barring any surprises, this trend should continue. There is a current re-evaluation going on about just how much of Mr. Trump’s campaign promises will actually come to pass. From a market perspective, that means the markets are starting to discount a lack of stimulus. It also means, from a pure currency perspective, that markets are looking at the lack of a border tax or other protectionist measures for those would appreciate the US dollar. Also, as I have argued earlier, the markets may be showing some concerns about the growth outlook.

Over the near term I expect the current trends to continue: US dollar weakness plus soft bond yields. That does two things. First, it provides some stability in the region as China’s reserves and hence the currency are under less pressure, in turn reducing the pressure on ASEAN currencies.

Second, as the markets stay in “risk-on” mode ASEAN benefits directly from capital inflows, providing not just stability but currency appreciation at a time when imported inflation is raising domestic prices. The current state of affairs gives more breathing room to regional central banks.

Over the medium term though things are likely to change. While the ECB may move to an accelerated tapering of its QE program, the Fed will still, by some distance, be conducting tighter monetary policy. By the scatter plot of forecasts it releases every quarter, the Fed is still on track to raise rates a couple of times this year and another 2 to 3 times next year. The BOJ is not expected to move.

Moreover, growth prospects in the US look better than in either Japan or the EU. Taken together, the US dollar should return to the stronger side. Dollar strength and the divergence in monetary policy will change a fair amount of the current dynamic for ASEAN and they are likely to face outflow pressure. For countries such as Malaysia and Indonesia, commodity prices will be crucial too.

How each country responds will depend on their policy space. To counter outflows, countries could raise policy rates, or allow bond yields to rise, or use reserves, or simply allow the currency to weaken. There is a further option of imposing capital controls but let’s leave that aside for now. I discuss these choices in more detail in the section on currencies, but suffice to say that raising policy rates is probably the last option and, in almost every country, the currency will bear at least some of the adjustment.

I think policy rates are likely to be stable largely because, as argued earlier in the report, I do not see great intrinsic strength in any of the domestic economies. The main driver of domestic incomes is trade and that is unlikely to have as good a year as the rear view mirror suggests. As such support really comes from fiscal measures and so, unless pushed to a wall (for example if they were facing a crashing currency or runaway inflation), it is unlikely that monetary policy will work at cross purposes with the fiscal side.

But could they be pushed to a wall? Barring some serious geopolitical or financial market event, it looks unlikely that currencies will crash. In any case, under such circumstances, most likely there will be some degree of capital controls. Then it comes down to inflation and whether the recently seen pressures could get central banks to act.

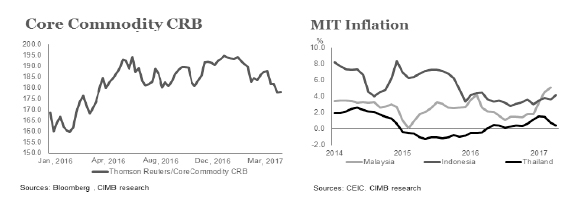

For that, consider the source of inflation. Most of it is cost push, as commodity prices are higher. For example, in year-on-year Ringgit terms, oil prices were about 60% higher in January than they were last year. If the rise in commodity prices was demand-led there were potentially some areas of concern. However, most of the rise is from supply issues. To the extent that there are demand pull pressures, they have been due to China’s credit fueled growth burst and that is unlikely to persist.

Second, are we seeing inflationary pressures from the labor market? The answer again is no and employment conditions still remain relatively slack. Third, is there demand pull inflation. The short answer is maybe. The reason I am vague about it is that it is difficult to estimate potential growth around the end points. Still, my research shows that if any demand pull pressures exist at all, they are mild.

In short, the inflation I see is largely cost push and that does not warrant a demand management response such as monetary tightening. In any case, some of the necessary tightening is being done via stronger currencies and I don’t expect any central banks to act as yet.

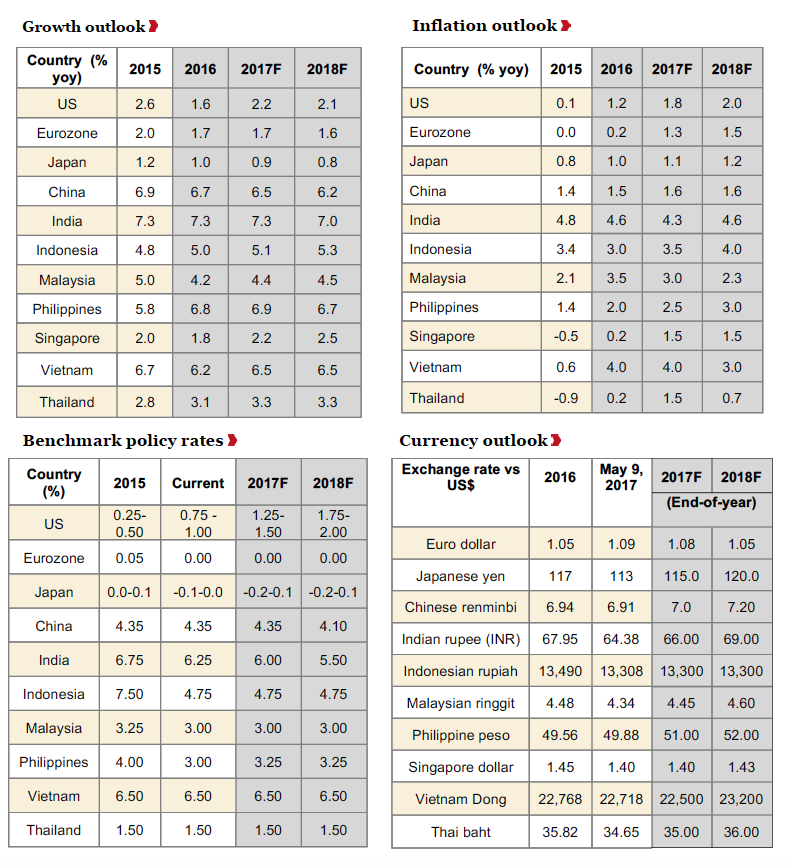

This Snapshot has a staggered release. 1Q17 GDP data from several countries are due out over the next couple of weeks and will publish the country pages after those prints. However, barring any big surprises in those numbers, my main forecasts are below.

Global & Regional Forecasts

Disclaimer: All rights reserved. No part of this report may be reprinted or reproduced or utilised in any form or by any electronic, mechanical or other means, now known or hereafter invented, including photocopying or recording, or in any information storage or retrieval system without proper acknowledgement of CIMB ASEAN Research Institute. The views, responsibility for facts and opinions in this publication rests exclusively with the authors and their interpretations do not necessarily reflect the views of CIMB ASEAN Research Institute.

![]()