LIFTING-THE-BARRIERS REPORT 2013 | INFRASTRUCTURE, POWER & UTILITIES

Published date: November 2013

TABLE OF CONTENT

(Click any topic to read the related section)

- Part 1. The Infrastructure Imperative for ASEAN

- Part 2. Barriers to Achieving the Goals of greater connectivity in ASEAN

- Part 3. Recommendations to catalyse infrastructure development

- Part 4. Rethinking how ASEAN can meet its infrastructure imperative

Part 1. The Infrastructure Imperative for ASEAN

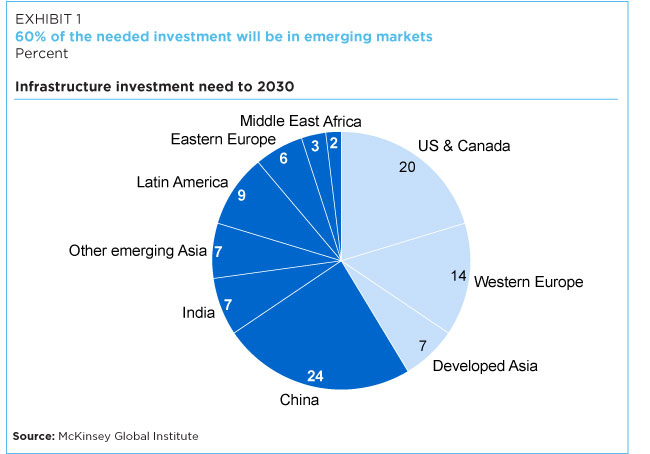

Historically infrastructure investment in ASEAN countries accounted for an average of 3 per cent of GDP each year, slightly below the global average of 3.8 per cent. Majority of global spending on infrastructure has now shifted to developing economies, with China and India being some of the largest investors. Over half of the required investments till 2030 will in fact be in emerging markets (Exhibit 1).

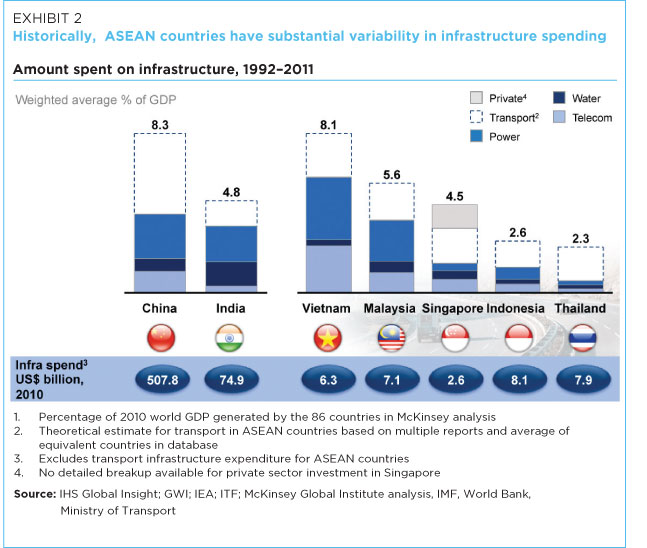

There has been substantial variability in the infrastructure spend on power, water and telecom between the different ASEAN countries (Exhibit 2). Beyond the utilities, there have also been large investments in real estate as well as transport infrastructure over the last decade. For example, Malaysia’s economic transformation programme included investment in an MRT system in Kuala Lumpur and the Greater Klang Valley. Vietnam is considering upgrading its rail transport system, including a high speed rail connecting North and South Vietnam.

SUBSTANTIAL ADDITIONAL INVESTMENTS REQUIRED FOR ASEAN COUNTRIES TO MEET THEIR INFRASTRUCTURE NEEDS

McKinsey Global Institutes’ research1 on infrastructure productivity shows that, with a few exceptions such as Japan, the value of infrastructure stock in most economies averages around 70 per cent of GDP independent of income (Exhibit 3). Infrastructure stock refers to the financial value of physical infrastructure assets (for example, kilometres of road, number of airport runways).

The ASEAN countries will need to spend more than their historical investments in infrastructure in order to accommodate expected GDP growth while maintaining this benchmark of infrastructure stock to GDP (Exhibit 4); we estimate that at least US$ 2.4 trillion is required in investment from 2013 – 2030 for ASEAN countries. To put this number in perspective, the GDP of the whole of Africa is expected to be US$ 2.6 trillion in 20202. Further, if less-developed economies are to meet their human development needs such as making safe drinking water, basic sanitation, and power widely accessible, they will need to invest substantially more than this baseline estimate. These estimates also do not account fully for maintenance and repairs that have been postponed or are part of upgrade programs.

While in absolute terms, Indonesia leads ASEAN countries in infrastructure spend at US$ 8 billion per year, excluding the investments in transportation; this represents a mere 1.1 per cent of GDP, well below the required amount. On the other hand, the level of infrastructure spending by Malaysia and Vietnam takes them close to the global bench mark of 70 per cent infrastructure stock to GDP.

COUNTRIES WILL NEED TO ADDRESS THEIR OWN INDIVIDUAL INFRASTRUCTURE DEMANDS FIRST

The ASEAN Connectivity Master Plan envisages major cross-border infrastructure linkages in roads, rail, power and gas valued at almost US$ 600 billion during 2006-2015, according to indicative estimates by the Asian Development Bank (ADB) in 2008. The underlying intent and objective of the master plan is to position a more “connected” ASEAN that can leverage lower transport and transaction costs as well as consolidate into a commerce hub. The physical connectivity part of the plan encompasses the hard infrastructure in transport, communications and energy as well as the associated regulatory frameworks required. Example projects that have been launched under the master plan include the ASEAN Highway Network, Singapore Kunming Rail Link, Trans-ASEAN Gas Pipeline, ASEAN Power Grid memorandum, and other initiatives for greater energy security and sustainability in the region. However, before these cross-border linkages are implemented, it is important to note that individually, many of the ASEAN countries lag significantly behind developed economies in developing basic infrastructure, such as airports, roads and rail (Exhibit 5) which will allow them to contribute effectively to the regional initiatives.

The World Economic Forum’s (WEF) annual survey on business across countries highlights well-developed infrastructure as a key pillar for country competitiveness. The WEF survey indicates significant variability in the quality of existing infrastructure across ASEAN countries – while Singapore ranks 3rd globally for its world-class infrastructure, other countries, such as the Philippines, Vietnam, Myanmar3 and Indonesia have a much farther way to go.

Most estimates of global infrastructure spend do not account for either the additional cost of making infrastructure more resilient to the effects of climate change or of lessening the impact of infrastructure on the environment. A significant proportion of infrastructure around the globe has not been hardened against rising sea levels and more frequent extreme weather events. The tsunami that hit parts of Asia in December 2004 damaged or destroyed houses, buildings, roads, bridges, and other physical infrastructure. In Aceh, Indonesia alone, the estimated costs of infrastructure damage was US$ 1.4 billion. Additional infrastructure to address growing demand can often threaten fragile ecosystems and pose new design and engineering challenges that will add further cost to ensuring they pass the tough environmental scrutiny. The environmental costs of infrastructure development in some developing countries have already reached an estimated 4 to 8 per cent of their GDP, with the effects falling disproportionately on the poor.

ECONOMIC DEVELOPMENT AND CONNECTIVITY HINGE ON GETTING THE INFRASTRUCTURE INVESTMENTS RIGHT

Infrastructure investment can have a sizeable impact on economic potential when delivered well (Exhibit 6). Large investments can also spur demand in the non-farming sector in emerging economies with significant multiplier effects.

However, making uninformed or no investment can be extremely costly from a socio-economic perspective. The quality and extensiveness of infrastructure significantly impacts economic growth and reduces income inequalities. For example, transport and telecom infrastructure enables connectivity with less developed and rural communities, thereby increasing access to economic activities. ASEAN countries need to individually and collectively review their infrastructure portfolio to appropriately plan for the required infrastructure that can catalyse economic development, and subsequently raise the productivity of the entire region.

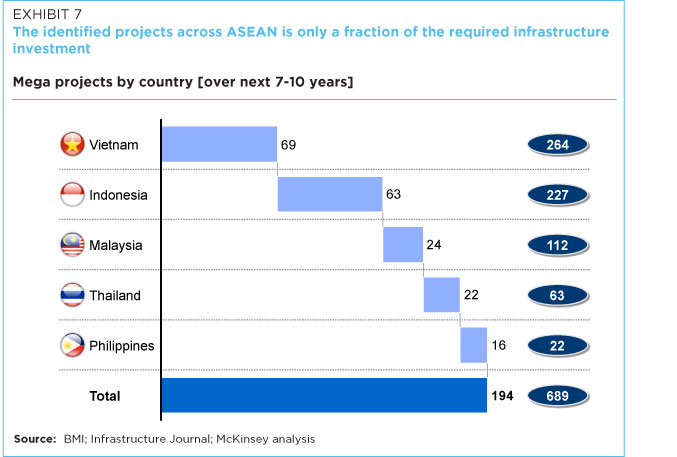

A review of the planned megaprojects across ASEAN countries for the next decade paints an encouraging picture; however, the estimated US$ 690 billion is far short of what is required to catalyse economic connectivity across these countries (Exhibit 7). It is absolutely imperative that the government and private sector in these countries come together to overcome the barriers and build the required infrastructure. Sustaining even the current levels of investment in infrastructure will be a challenge due to four main challenges that we outline in the next chapter.

Part 2. Barriers to Achieving the Goals of greater connectivity in ASEAN

Failure to meet the infrastructure needs of ASEAN could stifle growth in GDP and employment and compromise a range of human development efforts in less-developed ASEAN partners. Infrastructure is a rare “win-win” that generally boosts overall economic productivity in the long run and creates jobs in the short term, the latter being of significant importance given the current employment challenges and excess construction capacity in many countries.

The McKinsey Global Institute report on Infrastructure Productivity1 suggests that an increase of infrastructure investment equivalent to 1 percent of GDP could translate into an additional 3.4 million direct and indirect jobs in India, 1.5 million in the United States and 700,000 in Indonesia. In addition to supporting growth and job creation, infrastructure investments lead to improved health, education and social outcomes. For example, in the Indian state of Assam, a 1 percentage point increase in the electrification rate, resulted in a 0.17 percentage improvement in the literacy rate, suggesting that complete rural electrification of the region could contribute to raising the literacy rate to 74 per cent from 63 per cent.

However, simply sustaining the level of infrastructure investment required within the ASEAN countries will be challenging, much less delivering on the large-scale cross-border projects envisioned in the ASEAN Connectivity Master Plan. There are four significant barriers to delivery – fiscal pressures that limits direct public investment, the lack of a robust pipeline of projects that can be financed by the private sector, uncertain local regulatory and permitting processes which cause delays, and the lack of a strong institutional framework to enable effective coordination.

CHALLENGE 1. FISCAL CONSTRAINTS

Many governments face years of fiscal consolidation and “deleveraging” to bring public debt down to more manageable levels. In ASEAN today, the debt to GDP ratio is on average 50 per cent; for example, Malaysia (53 per cent), Philippines (51 per cent) and Vietnam (45 per cent) are under some fiscal pressure. In addition many countries face the challenge of gradually removing huge subsidies from the government budget such as in the case of Indonesia where petrol and electricity subsidies take up around 20 per cent of the government budget.

In this environment, there are difficult choices that need to be made between longer term infrastructure investment and other immediate priorities including education, health care, social services, and other welfare support, which are a priority concern in economies where rising cost of living is a major issue, particularly for the lower income groups. Academic research has observed a link between rising deficits and falling public investment (Exhibit 8). Between 1980 and 2003, annual public investment in infrastructure fell by 0.2 per cent of GDP across EU nations, and by 0.8 percent of GDP in Latin America, in line with increasing fiscal deficits.

Part of the challenge is that most governments apply cash-accounting standards that do not sufficiently differentiate between long-term investment that adds to a country’s balance sheet or generates growth over the long term, and near-term consumption. This cash-flow-oriented accounting overlooks the value of public assets, future income, and the inter-temporal dimension of solvency. It often forces countries to finance the build-up of infrastructure through tax increases and leads to under-investment in times of fiscal constraints. Very few governments subscribe to the notion of a national balance sheet.

Some policy makers, commentators, and infrastructure experts have held out the hope that increased private financing, particularly from institutional investors such as pension funds, insurance companies, and sovereign wealth funds, will help address the growing need for infrastructure finance. Indeed, these funds are attracted by the fact that life cycles of infrastructure assets often match the long-term nature of their liabilities and the growing investor confidence in ASEAN countries such as the Philippines which was recently granted its first investment grade rating. In addition, public-private partnerships (PPPs) and privatisation of state-owned assets are often viewed as an important part (and in many cases, the majority) of the solution to address infrastructure financing challenges. However, governments are often poorly prepared to tap into private financing due to unclear allocation of risk and returns between the public and private sector, and often lack the legal, regulatory and institutional frameworks that are a critical pre-requisite for successful PPPs, as discussed in the following section.

There is also significant debate around the value for money of PPP financing. In many cases, private finance is significantly more expensive than public debt, typically justified on the grounds of higher private sector efficiency as well as risk transfer. But private sector efficiency can also be achieved via design-build-operate contracts and similar structures, and particularly in transport projects. It is also questionable whether the risk transfer happens in practice.5

CHALLENGE 2: LACK OF INVESTOR-READY PPP PROJECT PIPELINE

There is limited understanding across several ASEAN countries on the prioritisation of infrastructure projects and the most optimal financing structures to launch these projects. For example, only 40 per cent of the required US$ 450+ billion investment in Indonesia over the next 10 years can be tied to specific infrastructure projects; others are yet to be conceived or identified.

Further, some ASEAN countries have launched portfolios of Public-Private Partnership (PPP) projects to tap into private financing, including Thailand, Indonesia and Philippines. As an example, Indonesia estimates that only 15 per cent of their required investment can be financed by the public sector; the remaining will need to rely on PPPs. To encourage investor participation in a range of water, ports and airport projects, Jakarta is embarking on a European road show to market these projects to potential investors. In another example, the Philippines has prepared over 16 PPP projects worth more than US$ 4 billion, but has only successfully bid out two.

The lower than expected success rate for PPPs across ASEAN can be attributed to a wide variety of factors including poor project selection, lack of sufficient preparation for the private sector to adequately assess the viability of the project and disagreement over the allocation of risk and returns between the public and private sectors.

Globally, many poorly conceived projects have been approved “because benefit-cost ratios presented to investors and legislators were hugely inflated, deliberately or not,” according to Bent Flyvbjerg, professor and chair of major programme management at Oxford University. “Competition between projects and authorities creates … an incentive structure that makes it rational for project promoters to emphasize benefits and de-emphasise costs and risks,” Flyvbjerg notes. McKinsey’s experience in helping governments rationalise infrastructure project portfolios confirms the need for projects to be more clearly linked to national priorities and more accurately evaluated in terms of their system-wide costs and benefits. Some of the root causes of poor planning and decision making include the failure to link infrastructure planning to broader social and economic goals, routine under-estimation of costs and over-statement of benefits, the pressure to allocate resources to cater to narrow political interests, and, in the most extreme cases, the damaging impact of corruption on the selection of projects.

Often PPP projects which are offered to private sector investors do not come with the necessary level of information that is required for the investors to make a fair and accurate assessment of the project’s viability. For example, Independent Power Products (IPPs) in Indonesia are often required to identify the land upon which the plant will be built and conduct extensive due diligence such as site surveys, soil investigation and environmental impact assessments in order to arrive at a cost estimate. This often results in investors pricing in high risk premiums due to the lack of information, a duplication of efforts across bidders or a long drawn out tender and negotiation process. Best practice PPPs typically have clearly defined scope and boundaries (such as the site identified and ideally already purchased) and provide the private sector with sufficient level of information in a comprehensive information memorandum to allow them to competitively price their offers – ultimately reducing the price tag to the public sector and consumers.

Another cause of PPP failure is the inability of the public and private sector to agree on the allocation of roles and responsibilities (and hence risk and returns). Lack of clarity on policies around market structure, pricing and subsidies and ownership and finance can lead to delays in implementation as the private sector are unable to accept the initial terms laid out for PPP projects. For example, the Indonesian government, under pressure from investors, ultimately introduced a series of implicit and explicit financial guarantee packages for IPP projects in order to ensure that the projects can successfully achieve financial closure. In another example, Malaysian toll road PPPs evolved over time transitioning from explicit revenue guarantees (on traffic volume and price) to price guarantees for later concessions, making the terms less attractive for investors. This negotiation of assigning risk and returns across the public and private sectors is critical because the terms that are agreed on upfront need to be upheld over the life of the PPP concession which can last decades.

Finally, the capability to design, structure, and deliver PPP projects in the government entities is not sufficient to meet the growing demand in many ASEAN countries. Government officials are not given the appropriate tools and training to ensure that the projects are being scoped appropriately or to comprehensively prepare the business case analyses. These factors have contributed to the limited pipeline of PPP projects in the region and must be systematically addressed to fundamentally transform and catalyse future infrastructure development.

CHALLENGE 3: COMPLEX EXECUTION DUE TO REGULATORY AND INSTITUTIONAL INEFFICIENCIES

Securing regulatory approvals usually consumes a significant portion of a project timeline—often many years and, not infrequently, longer than the time it takes to actually construct a piece of infrastructure. The necessary involvement of various stakeholders such as environmental interest groups, local administrative authorities, communities, and businesses and property owners can further slowdown already complex and bureaucratic government procedures. Such regulatory and institutional inefficiencies, coupled with judicial systems which do not always offer efficient recourse for the private sector, are a major hindrance to both public and private sector investment in infrastructure.

One of the most often cited examples of such regulatory hurdles is that of land acquisition. In India, about 80 per cent of road projects are delayed due to land acquisition issues. In Indonesia, minority land owners can hold up the land acquisition process and land speculation on the news of a new infrastructure development often drives up land prices – this has been identified as one of the major barriers to infrastructure development. To resolve this, Indonesia introduced a new law which provides for a process of land acquisition that will take less than two years from planning to acquisition. This new law is yet to be implemented, so the operational details will be critical in setting the ground rules for many years to come. In Malaysia and Singapore, similar laws allow the government to acquire land for projects that are deemed to be in the public interest and the government assumes the responsibility for acquiring the land.

Nevertheless, these processes can and should be shortened significantly. Best practice in issuing permits involves the rigorous prioritisation of projects, clear roles and responsibilities, transparency on performance, and time-bound process steps (including time limits on public review). Even in cases where accelerating approvals is not a critical priority from a pure impact perspective, the improved process and timeline predictability is often greatly valued by the stakeholders involved, and may therefore be justified on these grounds alone.

CHALLENGE 4: INEFFECTIVE GOVERNANCE SYSTEMS

The effective delivery of services in many areas of economic and public life must happen within a framework of well-defined systems. When health care, national security, or finance systems function well, they boast effective coordination between the critical actors such as health-care providers and insurance companies (“payors”); a clear division of labour between policy and execution, as in civilian oversight of the military; and clarity on the roles of the public and private sectors—in financial services, between central banks and private financial institutions, for instance. When such systems lack these characteristics, they become dysfunctional and unproductive.

In the case of infrastructure, the system often functions poorly. Indeed, too few people in the public and private sectors regard infrastructure as a system at all but rather think in terms of single projects. For example, often over 15 distinct decision-making entities are involved in an average urban transit project, with limited accountability and mechanisms to attain consensus.

Until sound infrastructure ecosystems are in place, countries will continue to fund the wrong projects, place the wrong priorities in the wrong areas, and fail to meet the needs of their people. Today, there are typically multiple authorities, agencies and ministries involved covering different sectors of infrastructure such as roads, rail, ports and water and different functions such as financing or contracting. The governance of these systems has not advanced in many places. Among the few exceptions are Singapore’s Urban Redevelopment Authority, Land Transport Authority and Development Planning Committee that work together seamlessly to translate national priorities into plans, goals and individual projects that are entirely consistent with one another.

In addition, there is typically not a clear separation of technical and political responsibilities – the balance between politicians and technocrats involved in an infrastructure project needs to be right. A long-term view for infrastructure investments is required, which is in contrast to the typically short political horizons. Ideally, policy makers should set overall aspirations and the strategic direction – making the call between investment in roads rather than hospitals, or vice versa. Experts need to determine how best to meet those overarching goals and evaluate, as well as execute, the projects. Leaving delivery to independent institutions tends to be much more successful.

Finally, the effective planning, delivery and operations of infrastructure requires people with the right skills and capabilities at each step of the value chain: urban planners to conduct feasibility assessments and manage stakeholder involvement, financial and technical analysts to create cost-benefit analyses; engineers to scope and design projects; project managers to oversee EPC or EPCM firms; lawyers to manage contracting and bankers to advise on financing. The lack of capability and capacity in these areas is commonly cited as one of the major barriers to delivery – particularly for the private sector. As long as governments under-invest in these capabilities, the outcome in a competitive market for talent is predictable – poor oversight of projects, delayed assets that commonly cost billions of dollars and long term contracts that will be deemed unfavourable on hindsight.

Part 3. Recommendations to catalyse infrastructure development

There are three major near-term recommendations that could potentially catalyse infrastructure development in the region as discussed during the round table.

A COHERENT TRANSPARENT REGULATORY FRAMEWORK

There are few consistently implemented regulations around infrastructure projects in the region (e.g., water project that was withheld approval and handed over to a state-owned enterprise), resulting in reduced confidence to invest in large-scale infrastructure projects. The relatively faster pace and longer term view of the private sector is in sharp contrast to the changing political landscape that tends to be focused on short-term gains.

One recommendation that was unanimously supported during the roundtable discussion was to set up an Institute for Regulators, along the lines of the Asian Corporate Governance Association, which would train high calibre and credible regulators for the ASEAN countries. This institute would be mandated to develop leaders that understand the benefits of coherent transparent regulations, willing to engage in productive dialogues with the private sector on the key issues, and are focused on effective implementation. Ensuring stable regulations that invite private sector participation, especially in large-scale infrastructure projects, will be critical to achieving the AEC objectives and the long-term economic development of the ASEAN markets.

Further, a common regulatory framework at an ASEAN level, instead of individual countries, could be helpful to encourage faster adoption of changes for infrastructure projects.

There is also a need to create forums for exchanging knowledge and best-practice solutions across borders within ASEAN. These learnings should be focused on success stories and inspiring change in the region. Forums could be in the form of annual conferences where there is an emphasis on sharing successful interventions or integrated into the curriculum and learning program in the above-mentioned institute.

SUFFICIENT UPFRONT INVESTMENT IN AND REVIEW OF PROJECT PREPARATION

A lack of viable projects that could attract investors in the ASEAN countries was nominated by participants in the roundtable as a concern. Transparency on the project pipeline as well as the number of local and foreign investors in a country often influences the willingness to invest in long-term large-scale projects. There is also an increasing need for governments to show their commitment by enabling the right environment to accelerate infrastructure projects.

Poor strategy and planning results in significant cost and time overruns during construction as well as wasteful investment, i.e., under-utilised or redundant infrastructure. Sufficient investment in the early stages of project selection and project preparation is critical to ensuring that the right infrastructure is built at the most optimal cost.

A business case analysis is important prior to deciding how to finance the project (e.g., PPP, purely public sector support). Every project should go through a detailed cost-benefit or feasibility analysis as well as financing/ business case development to be defined as “bankable”, i.e., attractive to credible financiers. Project preparation is more complicated and more expensive than most governments initially anticipate. Many priority projects also involve multiple ministries and jurisdictions requiring substantial stakeholder management to ensure sufficient ownership and decision-making to move the project forward. There is typically inadequate financing set aside for robust project preparation, largely because the work is done much before the actual transaction, which may or may not result in a closed deal. Private investors as well as development banks find this unattractive given the long time lines and high risk. Some entities, such as the Asian Development Bank and the African Development Bank, have initiated efforts to develop a project pipeline and preparation tool that can offer transparency.

Further, the feasibility studies must be credible. Insufficient data and lack of rigorous analyses result in misinformation on costs and inaccurate demand projections for the project. When the project preparation is done accurately and transparently, it also speeds up the downstream procurement process. South Korea established an independent central government agency (PIMAC) to review projects for cost underestimation, benefits overestimation, and fraud, by forming a multi-disciplinary feasibility team. This team rejected 46 per cent of projects (up from 3 per cent), reducing cost overruns from 122 per cent to 41 per cent. The UK’s Cost Review program, published by Infrastructure UK, identified 40 major projects for prioritization. The review resulted in a reformed planning process and then created a cabinet sub-committee to oversee and ensure quicker delivery of projects through reduced spending from GBP 18-20 billion to GBP 12-18 billion reflecting 10-15 per cent in savings.

Governments across the ASEAN countries would benefit from the establishment of mechanisms that encourage upfront investment in rigorous and high-quality project preparation. For example, the Ministry of Finance could set up a national revolving fund that is dedicated to reimbursing the project preparation costs; the tender winners from projects that go to financial close will then pay the equivalent project preparation expenses into the fund. They could also draw on best practices from the private sector capital projects (e.g., oil and gas megaprojects) that have clearly outlined stage-gated processes. The stage gates serve as important check points and have clear deliverables that the project must meet in order to get clearance to move forward. Example performance indicators could include cost-benefit analysis, including a value at risk that is revised at each project stage.

Further encouraging the private sector to bring their expertise in economic business case analysis and project preparation early in the project life cycle can be helpful. For example, the government can introduce “Swiss auction rules” for PPP projects. This means that when the private sector brings a prepared project, and the PPP unit tenders it, the private sector entity essentially gets the right of first refusal to match the final bid price.

For unsolicited projects, i.e., those initiated by the private sector, the government could enable a mechanism to fund or reimburse the project preparation costs, with appropriate controls. The tender preparation is still undertaken by an appropriate government entity (e.g., PPP unit) to ensure it is a fair process. The private sector entity could still bid competitively for the project in the open tender. Chile, Brazil and South Africa have introduced frameworks for private sector project initiation.

CREATING MECHANISMS FOR LONG-TERM FINANCING

Solutions to incentivise the private sector for investing long-term in the ASEAN countries will be important. This includes mechanisms such as infrastructure guarantee funds (similar to that which Indonesia has established), transparency on foreign investors operating in a country, and domestic bond market development (e.g., Malaysia has enabled project companies to raise bonds for their infrastructure projects). For example, the European Commission and the European Investment Bank (EIB) have initiated the Europe 2020 Project Bond initiative to attract additional capital through long-term debt instruments. The Brazilian Agency for Funds and Guarantee Management has been set up to provide more competitive insurance policies for infrastructure projects.

While several developing countries have set up infrastructure guarantee funds to attract investors, the utilisation of the national funds has traditionally been low, especially relative to those set up by multi-lateral organisations (e.g., World Bank’s Multi-lateral Investment Guarantee Agency). International investors must be typically convinced that the national guarantee funds do not have the same sovereign risks as the infrastructure projects themselves; partnerships between the national guarantee funds and multi-lateral organisations may help attract international investors.

Further, improving the funds flow between ASEAN countries, including pooling investments from multiple ASEAN countries for infrastructure projects could open up the market to long-term foreign investments as well. The Japanese government was cited as a best practice example for investing in international markets by working closely with local regulators and companies as well as taking a long-term view on their investments.

Infrastructure funding and finance is likely to become more challenging, especially if the regulatory environment continues to be unpredictable in these countries. Tapping new revenue streams and innovating with sources and structures for finance will become even more critical.

While addressing these immediate challenges will begin to create the right environment for long-term infrastructure planning and investments across the ASEAN region, they will be insufficient to meet the large and growing demand in the developing countries. Governments and the private sector need to re-think how they can build better-quality infrastructure for less, i.e., make the sector more productive across the region in order to realise the ASEAN connectivity goals. In the next chapter, we elaborate on potential approaches to selecting, designing, delivering and managing infrastructure projects to raise the productivity of the infrastructure investment substantially.

Part 4. Rethinking how ASEAN can meet its infrastructure imperative

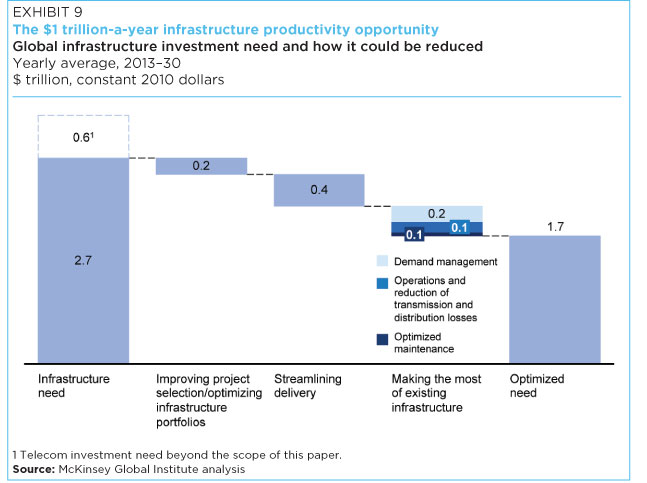

A recent McKinsey Global Institute Report1 has found that by scaling up best practice in selecting and delivering new infrastructure projects, and getting more use out of existing infrastructure, nations could obtain the same amount of infrastructure for 40 per cent less — or, put another way, deliver a 60 per cent improvement in infrastructure productivity. Over 18 years, this would be the equivalent of providing US$ 48 trillion (excluding telecoms) of infrastructure for US$ 30 trillion globally, a savings of US$1 trillion a year (Exhibit 9). This estimate is based on a review of more than 400 case studies of best practices—over 100 of which have quantified the savings they have achieved—and a subsequent global extrapolation of their impact.

Achieving these productivity gains will not require ground breaking innovation, but merely the application of established and proven practices from across the globe. The potential to boost productivity is so large because of failings in addressing inefficiencies and stagnant productivity in a systematic way. On the whole, countries continue to invest in poorly conceived projects, take a long time to approve them, miss opportunities to innovate in how to deliver them, and then don’t make the most of existing assets before opting to build expensive new capacity.

In many countries, the process of selecting, building, and operating infrastructure—and the governance systems that could force improvements—has not changed for the better in decades. In the construction sector, for instance, labor productivity has barely moved for 20 years in many developed countries despite steady and significant gains in the productivity of other sectors.

All too often, a surprisingly stable status quo persists in which inaccurate planning and forecasting lead to poor project selection. A bias among public officials to build new capacity, rather than make the most of existing infrastructure, is common, leading to more expensive and less sustainable infrastructure solutions. A lack of incentives, accountability, and capabilities as well as risk aversion has prevented infrastructure owners from taking advantage of improvements in construction methods such as the use of design-to-cost and design-to-value principles, advanced construction techniques, and lean processes. Infrastructure authorities frequently lack the capabilities necessary to negotiate on equal terms with infrastructure contractors, rendering them unable to provide effective oversight and thereby drive performance.

McKinsey’s research finds that pulling three main levers can deliver the potential savings.

LEVER 1. IMPROVING PROJECT SELECTION AND OPTIMISING INFRASTRUCTURE PORTFOLIOS

A review of global best practices indicate that one of the most powerful ways to reduce the overall cost of infrastructure is to optimise infrastructure portfolios—that is, simply to select the right combination of projects. All too often, decision makers invest in projects that do not address clearly defined needs or cannot deliver desired benefits. Equally often, they default to investments in additional physical capacity (for example, widening an arterial road into a city) without considering the alternatives of resolving bottlenecks and addressing demand through, for instance, better planning of land use, the enhancement of public transit, and managing demand. Improving project selection and optimising infrastructure portfolios could save 20 per cent of the total productivity opportunity. To achieve these savings, owners must use precise selection criteria that ensure proposed projects meet specific goals; develop sophisticated evaluation methods to determine costs and benefits; and prioritise projects at a system level, using transparent, fact-based decision making.

For example, to guide its selection of transit projects, the Government of Singapore has a clear metric: to support its broad socioeconomic goal of building a densely populated urban state, any project must contribute to the specific objective of achieving 70 per cent use of public transit. In Chile, the National Public Investment System evaluates all proposed projects using standard forms, procedures, and metrics, and rejects as many as 35 per cent of all projects. The organisation’s cost-benefit analyses consider, for instance, non-financial costs such as the cost of travel time, and a social discount rate that represents the opportunity cost for the country when its resources finance any given infrastructure project. Final approval rests with Chile’s finance ministry, which allocates funding based on a combination of these cost-benefit analyses and national goals.

LEVER 2. STREAMLINING DELIVERY

Streamlining project delivery can save up to 15 per cent of total investment annually while accelerating timelines materially. Speeding up approval and land acquisition processes is vital given that one of the chief drivers of time (and time overruns) is the process of acquiring permits and land. In India, up to 90 per cent of road projects experience delays of 15 to 20 per cent of the planned project timeline because of difficulties in acquiring land. England and Wales in the United Kingdom have, for instance, implemented one-stop permitting processes. In Australia, the state of New South Wales cut approval times by 11 per cent in just one year by clarifying decision rights, harmonising processes across agencies, and measuring performance. Both the United Kingdom and Australia have implemented special courts to expedite disputes over land acquisition. A key source of savings in project delivery is investing heavily in early-stage project planning and design. This can reduce costs significantly by preventing changes and delays later on in the process when they become ever more expensive. Bringing together cross-functional teams from the government and contractor sides early in the design process can avoid the alterations that lead to 60 per cent of project delays.

Owners can structure contracts to encourage cost-saving approaches, including design-to-cost principles that ensure the development of “minimal technical solutions”—the lowest-cost means of achieving a prescribed performance specification, rather than mere risk avoidance. Contractors can also be encouraged to use advanced construction techniques including prefabrication and modularisation—facilitated by having the appropriate standards and specifications—as well as lean manufacturing methods adapted for construction. Strengthening the management of contractors, a weakness of many authorities, can also head off delays and cost over-runs.

Finally, nations should support efforts to upgrade their construction sectors, which often rely heavily on informal labour (a situation that often contributes to corruption), suffer from capability gaps and insufficient training as well as from ill-conceived regulations and standards, and under-invest in innovation. Enhancing construction industry practices is necessary to raise the productivity, quality, and timeliness of infrastructure projects.

LEVER 3. MAKING THE MOST OF EXISTING INFRASTRUCTURE ASSETS

Rather than investing in costly new projects, governments can address some infrastructure needs by getting more out of existing capacity. We estimate that boosting asset utilisation, optimising maintenance planning, and expanding the use of demand-management measures can generate savings of up to $400 billion a year. For example, intelligent transportation systems for roads, rail, airports, and ports can double or triple the use of an asset—typically at a fraction of the cost of adding the equivalent in physical capacity. Reducing transmission and distribution losses in water and power (which can be more than 50 per cent of supply in some developing countries) often costs less than 3 per cent of adding the equivalent in new production capacity and can be accomplished significantly faster.

Maintenance planning can be optimised by using a total cost of ownership (TCO) approach that considers costs over the complete life of an asset and finds the optimal balance between long-term renewal and short-term maintenance. By one estimate, if African nations had spent $12 billion more on road repair in the 1990s, they could have saved $45 billion in subsequent reconstruction costs. To optimise maintenance programs, nations should assess and catalogue needs. London, for instance, has a 20-year model for pavement deterioration. Denmark has reduced the expense of maintaining its roads by 10 to 20 per cent by adopting a total cost of ownership approach.

Finally, governments need to make more aggressive use of tools and charges that allow them to manage demand. Advances in technology are broadening the range and improving the effectiveness of such demand-management approaches. To fully capture the potential of demand management, governments need to take a comprehensive approach and use all available tools. The city of Seoul, for example, is dealing with congestion by combining improved bus operations, access restrictions, and electronic fare collection with an integrated traffic management system. Congestion pricing, widely regarded as the most effective measure to reduce congestion and reduce the need for capacity additions, especially in advanced economies, can be paired with intelligent traffic solutions to achieve even greater benefits.

What remains clear is that full integration within ASEAN is only achievable when each individual country attains a certain basic level of infrastructure. There are funds and investors eager to invest in ASEAN’s infrastructure projects, provided the right conditions for stable regulatory and policy environment are established. It is in the governments’ best interest to come together and create these conditions to catalyse the much-needed infrastructure development in these countries.

Endnotes

- McKinsey Global Institute, McKinsey Infrastructure Practice, Infrastructure productivity: How to save $1 trillion a year, January 2013

- McKinsey Global Institute, Lions on the move: The progress and potential of African economies, June 2010

- McKinsey Global Institute, Myanmar’s moment: Unique opportunities, major challenges, June 2013

- McKinsey Global Institute, The archipelago economy: Unleashing Indonesia’s potential, September 2012

- The Fantasy World of Private Finance via Public Partnerships” in “Better regulation of Public-Private Partnerships for Transport Infrastructure”, OECD/ITF 2013.

![]()

RELATED REPORTS

- LIFTING-THE-BARRIERS REPORT 2015 INFRASTRUCTURE

- ASEAN NEEDS TO PROVIDE THE RIGHT ENVIRONMENT TO MAKE PRIVATE INVESTMENTS IN INFRASTRUCTURE MORE FEASIBLE

- LIFTING-THE-BARRIERS REPORT FOR ASEAN INFRASTRUCTURE, POWER AND UTILITIES