LIFTING-THE-BARRIERS REPORT 2014 | MINERALS, OIL & GAS

Published date: December 2014

TABLE OF CONTENT

(Click any topic to read the related section)

- 1. Foreword

- 2. Introduction

- 3. State of play: Oil and Gas

- 4. State of play: Minerals

- 5. Enablers

- 6. Meeting the challenge: Recommendations

- 6.1 Recommendation 1: Elevate awareness of the industry’s changing dynamics

- 6.2 Recommendation 2: Develop human capital for future needs

- 6.3 Recommendation 3: Promote free movement of human capital

- 6.4 Recommendation 4: Share technical knowledge

- 6.5 Recommendation 5: Collaborate on next-generation assets

- 6.6 Recommendation 6: Enhance service-sector effectiveness

- 6.7 Recommendation 7: Build nongovernmental local champions

- 7. Conclusions and next steps

1. FOREWORD

ASEAN countries rely heavily on the mineral, oil and gas industry to deliver GDP growth and regional energy security. But resource-producing nations throughout ASEAN face multiple issues in all three sectors.

One challenge, for example, is that the resource base in many ASEAN countries is maturing. That affects the number of operators in the industry as well as operators’ ability to reinvest in their businesses. New investment and innovation are necessary to sustain competitiveness, as more mature energy-producing regions such as the North Sea have demonstrated. But where can ASEAN nations find such investment, and how can they best stimulate innovation? From one perspective, ASEAN’s need to attract foreign investment and expertise has never been greater. From another perspective, ASEAN should promote local content and build or favor local champions.

This dilemma of whether to seek foreign investment or push local development raises a key challenge for all stakeholders: How can ASEAN strike the right balance in attracting investment, securing the best global capabilities, promoting local champions and building capability for the future? What can ASEAN do to break down cross-border barriers so that it can pursue these goals collectively, to every country’s benefit? Ultimately, how can ASEAN create a stable ecosystem to support the sustainable extraction of resources—an ecosystem that includes local entities and support systems?

A roundtable discussion held on September 8, 2014, with key industry leaders at the ABC Forum in Singapore addressed the challenges of the extractive industry. The discussion considered the following questions:

- Meeting Future Investment Needs

a. How competitive is ASEAN for resource-related investment relative to other regions around the world?

b. To what extent are its challenges a function of perception versus reality?

c. What steps can ASEAN and its governments take to improve its position? - Maximising the next-generation resource base

a. What are the common challenges in mature resource basins across ASEAN?

b. How can we address the emerging unconventionals and complex resources successfully?

c. To what extent can operators and service companies meet those challenges? In particular, how can national oil companies (NOCs) continue to extract resources at low total costs, safely, and without damaging the environment?

d. What special skills or expertise will ASEAN countries need to successfully transition to the next stage of the resource base’s development?

e. How should ASEAN think about building a thriving industry ecosystem through various forms of partnerships among governments, NOCs, and local entities? - Promoting Local Content

a. What role should governments and NOCs play in supporting local companies so that the value they create stays local?

b. What have we learned from other geographic regions about local content?

c. What is the right balance between promoting existing local champions and creating an open investment climate for new operators?

d. How can barriers and incentives designed to promote local content also achieve social-responsibility targets related to income distribution and local development?The roundtable provided a platform for leaders to voice their views and propose potential actions to address the challenges collectively. This paper offers context from that discussion and a selection of recommendations that ASEAN may wish to consider moving forward. While the roundtable members noted that ASEAN’s oil and gas and mining industries often face many distinct challenges given their different stages of maturity, many of the enablers required for success in all three sectors are similar and will be addressed jointly.

2. Introduction

ASEAN countries today are actively pursuing the dual objectives of energy security and economic growth, and the extractive industries have been a significant contributor to both. As geopolitical events and natural disasters increasingly roil global energy and resource markets, ASEAN countries are looking to domestic supplies to help ensure uninterrupted, affordable energy. They formalised this intent most recently with the March 2013 ratification of ASEAN Petroleum Security Agreement (APSA), a petroleum-sharing scheme for times of supply shortages. In addition to contributing to energy and resource security, the extractive industry plays a big role in the ASEAN economy. It accounted for approximately 11% of the region’s combined GDP in 2013 (see Exhibit 1).

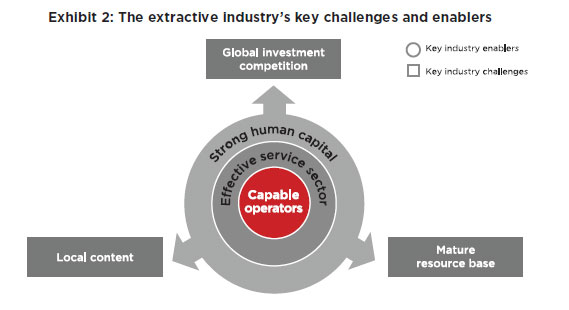

Given the need for energy and the economic importance of the extractive industry, ASEAN countries must maximise the industry’s value and capabilities by creating a strong, sustainable industrial ecosystem. The ecosystem includes operators (NOCs, internationals, and independents), a network of service providers, and the specialised talent that each of these companies needs. Creating such an ecosystem means managing three external challenges: global competition for investment, the maturing resource bases in many ASEAN countries, and governments’ desire to promote local content and build local champions. It also means strengthening the ecosystem’s three central elements. A thriving ecosystem requires a large number of capable operators, an effective and profitable energy service sector, and a deep, strong pool of human capital.

This is a critical time in the life of the ASEAN extractive industry. How leaders handle the interplay of these elements and challenges now will chart the industry’s course for many years to come (see Exhibit 2).

3. State of play

Oil and Gas

3.1 Challenge 1: Global competition for capital investment

We estimate that ASEAN will continue to attract upstream oil and gas capital investment, amounting to a total of US$250 billion between 2015 and 2020. However, the region’s share of global upstream investment is expected to flatline over the next five years as capital moves to more promising zones, such as Latin America and Africa. North America is also likely to continue attracting greater upstream investment as the shale gas revolution plays out in that region (see Exhibit 3).

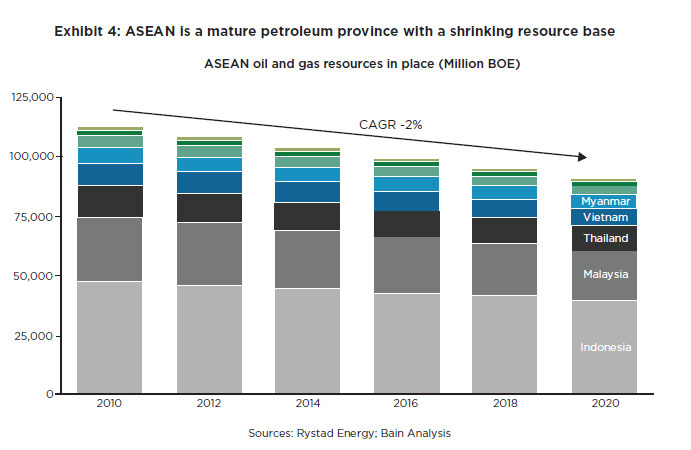

3.2 Challenge 2: Maturing resource base in ASEAN

The dwindling resource base in many ASEAN countries further exacerbates the worsening oil and gas investment climate (see Exhibit 4). In mature petroleum regions, such as Malaysia, more than 30 years of extensive exploration and production have left fewer and fewer opportunities for large discoveries with easy access.

Mining will experience similar competition for capital and resources, as less mature countries offer more promising returns for the limited investment capital of international miners.

3.3 Challenge 3: Desire to promote local content

Local-content policies designed to support broad-based economic growth are hardly a new phenomenon in the extractive industry. In ASEAN countries, typically, these policies aim to gradually reduce dependence on external involvement by creating opportunities for regional integration and international trade. However, a new strain of nationalism has emerged, and ASEAN governments increasingly want to promote local content and develop local champions. In Indonesia, for example, recent mineral policy rollbacks, such as stricter in-country mineral processing requirements, have deterred new mining investments. Foreign operators or investors interested in entering a market must understand the trade-offs that local-content enforcement may entail.

4. State of play

4.1 Challenge 1: Operating environment

Mine operators across ASEAN are collectively challenged by a range of factors that limit the ease of doing business and often their relative attractiveness to other choices. Many countries are promoting policies to increase the government’s take on mining revenues while limiting foreign ownership in the sector. While such moves enhance budgets in the short term, they undermine levels of absolute investment, in turn inhibiting the multiplier effect of investment for domestic economies. This is considerable in an industry where US$2.50 to US$3 of benefit is derived for every direct dollar of investment.

In many countries, miners are also challenged by regulatory complexity in permitting and other approvals, by a changing regulatory landscape around export requirements, and by the degree of “upgrading” completed in some locales like Indonesia.

4.2 Challenge 2: Infrastructure

The remote location of mining sites in many countries adds considerable cost, which challenges economics for many players. In a world where, all countries compete with one another for the incremental mining dollar and capital expenditure for new mines is rising, ASEAN countries’ cost competiveness is challenged in many locations by the high cost to gain access to new mining sites, to secure the needed route, and to develop and market the supply.

Challenge 3: Talent pipeline

Acquiring and developing local talent represent an additional test for mining operators in need of engineers, operations staff, and other technical support to deliver and operate new projects. In many locales, operators are tested by restrictions in their use of expatriate staff, as well as in the free movement of ASEAN talent across projects within the region. At the same time, the local supply of experienced talent is challenged in the domestic market, where the balance between the requirement and the available pool is off.

5. Enablers

While ASEAN countries need to address these external challenges, maximising the industry ecosystem’s value also requires investment in its three main enablers: capable operators, an effective energy service sector, and strong human capital.

5.1 Enabler 1: Capable operators

As the ASEAN resource base matures, easy-to-find resources are scarcer and smaller. Large operators, which focus on big fields or assets and are often short of skilled labor, typically do not find these marginal opportunities appealing. Smaller companies, however, are likely to be well positioned to capitalise on such opportunities, thanks to their nimble capital structures and use of innovative technical solutions. The changing composition of industry players has been a key factor in the revitalisation of the North Sea oil and gas landscape as it matures (see Box 1). Similar trends manifest themselves in the minerals industry.

Such shifts generally require encouraging more foreign operators and investors. In light of this challenge, governments will need to balance the benefits of policy changes, incentives and other accommodations for foreigner operators against domestic pressures in favor of local operating companies.

5.2 Enabler 2: An effective energy service sector

A strong extractive industry requires a vast network of service providers. To develop homegrown global champions, host governments need to support local service providers and ensure they are capable of delivering the same level and quality of services as those offered by their international competitors. A combination of barriers and incentives, hopefully only temporary, can be used. The goal of these measures must be to ensure long-term optimisation of resources while at the same time achieving social-responsibility objectives. They should enable safe, effective extraction resulting in lower costs and higher national income over the lifecycle of the industry.

Global best practices suggest that local service providers must develop three key capabilities:

- Strong core suites of product and service offerings geared toward specific local challenges. In ASEAN nations, these challenges include marginal, deepwater, and enhanced oil recovery (EOR). Within these domains, providers should strive to build distinctive capabilities that deliver more than agency services. Host governments can structure local-content policies to encourage service companies to develop real expertise in partnership with international players, as opposed to just acting as agents.

- Strong project management and cross-business-unit integration capabilities to handle both external stakeholders, such as operators and contractors, and internal stakeholders. Service providers can accelerate the development of these capabilities by partnering with global engineering, procurement, and construction (EPC) firms that have distinctive technological know-how and strong project execution capabilities. ASEAN governments can play a crucial role in influencing the nation’s investment climate and facilitating access to these world-class EPC firms.

- Flexible business models that allow for a range of offerings, from providing discrete services to fully designing and managing complex projects. On the execution front, service companies need to build the necessary track records to meet operators’ requirements. They will also need sufficient financial backing to overcome project delays and losses.

5.3 Enabler 3: Strong human capital

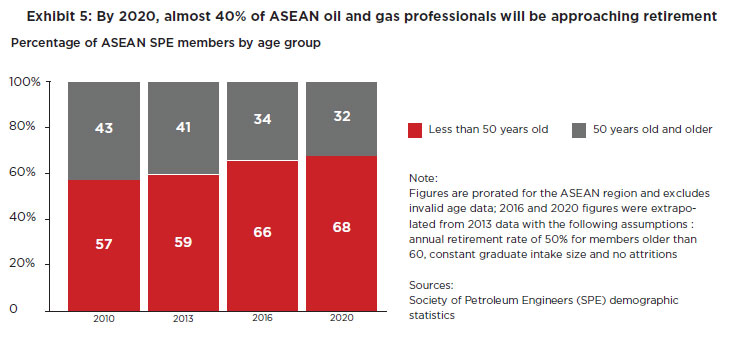

The need to attract, develop, and retain talent is a persistent issue for many industries in the world, but it is particularly acute for the extractive industry in ASEAN countries. Despite its mature state, the ASEAN extractive industry is likely to face challenges in replenishing its workforce. Approximately 40% of oil and gas professionals will approach retirement in the next decade, eliminating a major pool of expertise (see Exhibit 5).

In the past, some companies have managed to avoid a talent crisis by poaching employees from rival firms. But this is at best a stopgap solution. Instead, companies and governments need to forge stronger public-private partnerships to create programs that can train the next generation of the extractive workforce. And they need to do this before a crisis occurs, not after.

One strategic task in developing strong human capital is to proactively identify the skill sets needed to tackle emerging industry challenges. For example, as mining companies in Indonesia aim to improve operational safety and reduce operating costs in the nation’s many remote areas, they are placing greater emphasis on training miners to operate autonomous equipment.

6. Meeting the challenge: Recommendations

ASEAN’s extractive industry faces considerable challenges as it moves into the next decade. What can be done to enhance ASEAN’s competitiveness in the international arena and to attract the investment required to support the industry? Also, what can ASEAN do to help the industry meet the challenge of a maturing resource base through its operators, service companies, and human capital?

The roundtable discussions brought forward several recommendations and action items for ASEAN countries to consider. These actions encompass the critical areas ASEAN nations need to address collectively and individually to overcome the challenges of today’s industry landscape.

6.1 Recommendation 1: Elevate awareness of the industry’s changing dynamics

Given the importance of extractive industries, leaders need to be aware of the ongoing pace of change and the corresponding implications for ASEAN countries jointly and individually.

The relative attractiveness of Southeast Asia is declining in oil and gas, and it will be increasingly challenging to attract investments into the region. Awareness of this situation is the first step in helping policymakers respond with measures that can counter the emerging dynamic.

Roundtable discussions led to the following proposals to elevate awareness of the issue among key decision makers:

- Engage with energy/minerals ministers on issue

– ABC leaders to meet with energy ministers to highlight emerging change

– Make ministers aware of critical changes and potential impacts on industry and country - Publish position paper to increase profile of issue

– Develop position paper on issue with industry leaders

– Publish and distribute to leaders and policy makers to heighten awareness and provoke more discussion - Hold forums with industry leaders to draft action plan

– Conduct discussion forums with ASEAN leaders to encourage a more collaborative approach to problems

– Develop concrete plans for each country and for ASEAN collectively to address the changing dynamics

6.2 Recommendation 2: Develop human capital for future needs

Competition for skilled manpower across the globe is intensifying, and ASEAN must prepare itself now to ensure a sufficient supply in the next three to five years. Moreover, the portfolio of the extractive industry is shifting, and the skills required will be different in the future from what they were in the past. For example, mature fields management, innovative low-cost developments, and EOR capabilities are key skills required for the next generation of oil and gas assets in ASEAN. Certain types of craft labour will also be vital.

Governments must put policies in place today to build the capabilities required in the future. If they delay, ASEAN will be unable to capitalise on the next phase of growth.

The roundtables proposed the following actions in this context:

- Establish alliances between industry and local universities

– Build alliances with local universities and institutes to enhance interest and visibility of topic among students

– Prioritise critical skillsets and careers that face shortages—e.g., reservoir/drilling - Offer scholarships and training on critical technical skills

– Provide scholarships for students from both local and international universities to ensure a robust pipeline of talent

– Prioritise key technical and craft skills required in the next three to five years - Promote “work in ASEAN” policy to attract key talents

– Introduce a plan to encourage foreign and local talents to work in the ASEAN region

– Conduct information sessions in leading universities to highlight potential opportunities and benefits of working in ASEAN

6.3 Recommendation 3: Promote free movement of human capital

Despite their proximity, ASEAN nations do not always facilitate the movement of skilled individuals from one country to another. Expatriates in general are able to move from country to country relatively easily, sometimes within or outside the same company. Local talent typically finds such moves much more difficult.

Improving the movement and allocation of human resources within ASEAN is thus a major opportunity. Policies that encourage and enable easy movement of resources, as and when required, would be highly valuable: A country or region with a surplus of engineers or skilled oilfield labor could reallocate its resources to countries or regions with shortages. Enabling this process would benefit ASEAN as a whole, especially as the pace of activity changes in the next few years.

The roundtables proposed the following actions related to the movement of human capital:

- Allow movements of certain technical professionals and craft labour within ASEAN (surplus vs deficit)

– Establish which professions and trades are most critical for ASEAN extractive industry

– Formalise a process to enable ease of movement within ASEAN for skilled people within these professions and trades - Develop specific regulations to establish common standards

– Select which professions or skillsets require a common accreditation scheme

– Assess ease of implementation and implications

– Establish a common accreditation scheme that is recognised and standardised across ASEAN

– Introduce policies to enable ease of movement of accredited personnel throughout ASEAN - Create flexible policies to allow companies to meet employment commitments across multiple countries

– Assess feasibility of policies enabling companies to meet local content rules while still allowing them to optimise resources across ASEAN depending on need

– Conduct pilots in two or three companies with operations across ASEAN

– Implement policy across all companies

6.4 Recommendation 4: Share technical knowledge

ASEAN countries share many similar challenges and are often at similar stages of development and maturity. However, knowledge developed in facing these challenges is often not widely shared among countries and technical professionals. Forums to share technical knowledge among ASEAN countries are scarce, and sharing often takes place on an informal and ad hoc basis.

ASEAN nations would benefit from formalising and further encouraging such knowledge sharing. Each country can gain from the lessons learned by others, reducing the number of trials and mistakes required to achieve success. Sharing of data among countries can also be immensely valuable, reducing the costs of data acquisition and improving the accuracy of decision making.

The roundtables proposed the following actions in connection with knowledge sharing:

- Promote joint studies on specific topics (e.g., geosciences, drilling optimisation, mine management, technical training)

– Provide funding for research institutes and university research centers to perform directed research for national oil companies

– Identify key topics and projects for joint studies, particularly topics that are applicable to several ASEAN countries and with several studies in pipeline

– Formalise joint study partnerships and parties involved

– Conduct study and publish results of collaboration - Implement policies to enable more open sharing of selected technical data

– Assess what data should be shared among ASEAN nations; identify data sets that will jointly benefit both countries and improve efficiency

– Gain agreement from ASEAN countries and formalise the process - Knowledge-sharing forums among leading professionals

– Select several leading topics for discussion in ASEAN

– Schedule periodic forums and document outcomes

6.5 Recommendation 5: Collaborate on next-generation assets

The portfolio of assets in the ASEAN context is evolving. Existing conventional assets are maturing, and the importance of complex and unconventional assets is increasing. Majors and larger oil and gas independents are starting to move out of the region as the size and scope of Southeast Asia’s conventional assets declines. The challenges each country faces are similar, and there are potential synergies that could benefit all parties.

ASEAN thus needs to approach this wave of change collectively, understanding what can and should be done together to address the emerging challenge. Currently, studies and pilots on these emerging themes are done individually, with no joint effort to undertake and share the results among ASEAN countries. The synergies of a joint effort are lost; neither costs nor lessons learned are shared.

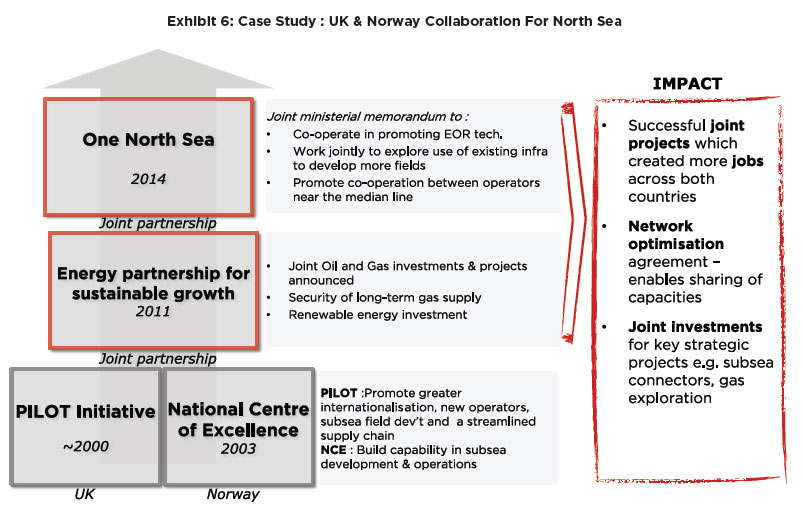

An example of a cross-country collaboration that has produced immense benefits is the North Sea energy industry. Norway and UK initially operated as separate entities with limited collaboration on both the technical and the commercial front. In the past five to ten years, however, the two countries have increased their joint efforts and have realized great benefits in terms of investment, job creation, and capacity building for both (see Exhibit 6).

The roundtables proposed the following actions related to next-generation collaboration:

- Optimise the service base across all ASEAN countries

– Encourage local and regional development of service assets, technology and personnel for EOR - Establish regional forums to discuss technical challenges (somewhat similar to technical knowledge sharing)

– Conduct forums on topics common to ASEAN countries

– Develop learnings and programs that can be shared among policymakers and technical professionals - Promote joint pilots to cost-share R&D in EOR for offshore

– Identify which projects and pilots can be done jointly given similarities

– Establish a partnership and conduct joint pilots

6.6 Recommendation 6: Enhance service-sector effectiveness

The emergence of a strong energy service sector within ASEAN is critical to move the extractive industry in Southeast Asia to the next level. Countries often overlook the importance of this sector, failing to create actions or policies that address its challenges and issues. Today, given the changing landscape within ASEAN, policies that further increase the efficiency of the sector’s operations and execution are vital.

What are some of the issues? Service companies often find it difficult to move equipment from one country to another, even within ASEAN. For example, rigs or barges that are underutilised in one country often have to undergo a lengthy process to be used in another country. This reduces the efficiency of equipment and increases the cost of operations.

In addition, service providers are often dominated by foreign or international companies, and they often focus on low-value services. Although a few local companies have emerged, governments have put too little emphasis on developing the sector and have created too few policies to build local service companies’ capabilities.

The roundtables proposed the following actions in connection with the service sector:

- Develop selective local content exemptions for critical technologies and capabilities

– Assess which fields, professions, and technologies should be exempted from local-content rules given their criticality and global shortage

– Formalise processes to allow exemption from local-content policies - Create a working group to evaluate the next generation of technologies

– Conduct working session to evaluate next-generation technology and applications

– Short-list a few technologies for evaluation and pilot

– Encourage development of high-value, strategic capabilities and specialised technical skills among service companies - Revisit duties and tariffs to allow for free movement of equipment

– Consider areas where significant cost advantages could be achieved

6.7 Recommendation 7: Build non-governmental local champions

ASEAN has strong local champions in its members’ national oil companies: PETRONAS, Pertamina, and PTTEP have developed from strength to strength and are a testament to local capability and growth. Similar strength is seen in many local monopoly producers.

Some local companies and service providers, such as Sapura Kencana in oil field services, have emerged as strong competitors. Despite local content and vendor development programs, however, governments have not always given sufficient emphasis or achieved much success in building nongovernmental local champions and companies.

Given this lack, ASEAN has an opportunity to increase support for the growth of such companies. Affirmative policies and programs could help develop these local champions and enable them to flourish across borders. This will create a more level playing field and will encourage the growth of international champions on a par with current multinational players.

Potential actions might include the following:

- Consider preferential treatment to develop more ASEAN providers and suppliers

– Identify a specific list of industry segments where ASEAN sees strategic value in stronger local service providers

– Formalise processes to implement preferential treatment on selected local providers (e.g., local content requirements, taxation, and investment limits)

7. Conclusions and next steps

Effective management of the extractive industries will be critical to ASEAN’s next phase of development. Of course, building an effective ecosystem that meets production and investment targets, offers a free and attractive market, and helps to build homegrown champions poses a major challenge. But the forthcoming arrival of the ASEAN Economic Community offers opportunities to break down barriers across the region and work together to address common challenges. While the resource sector will always by its nature be strategic and require single-country policies, the roundtable has identified a wide range of recommendations that can create the right balance in the pursuit of a healthy ecosystem.

![]()

RELATED REPORTS