CARI Captures Issue 728: Total IPO proceeds in Southeast Asia in 2025 reach USD 5.6 billion

Captures has widened its scope to include news related to all the members of the Regional Comprehensive Economic Partnership (RCEP) agreement which was signed towards the end of 2020. Besides the ASEAN Member States, this includes Australia, New Zealand, China, Japan, and South Korea. The other weekly newsletters under CARI, China-ASEAN Monitor and Mekong Monitor will also be consolidated into the Captures newsletter. We hope this new version of Captures will serve you better and look forward to providing a curation of stories relevant to ASEAN and its trading partners.

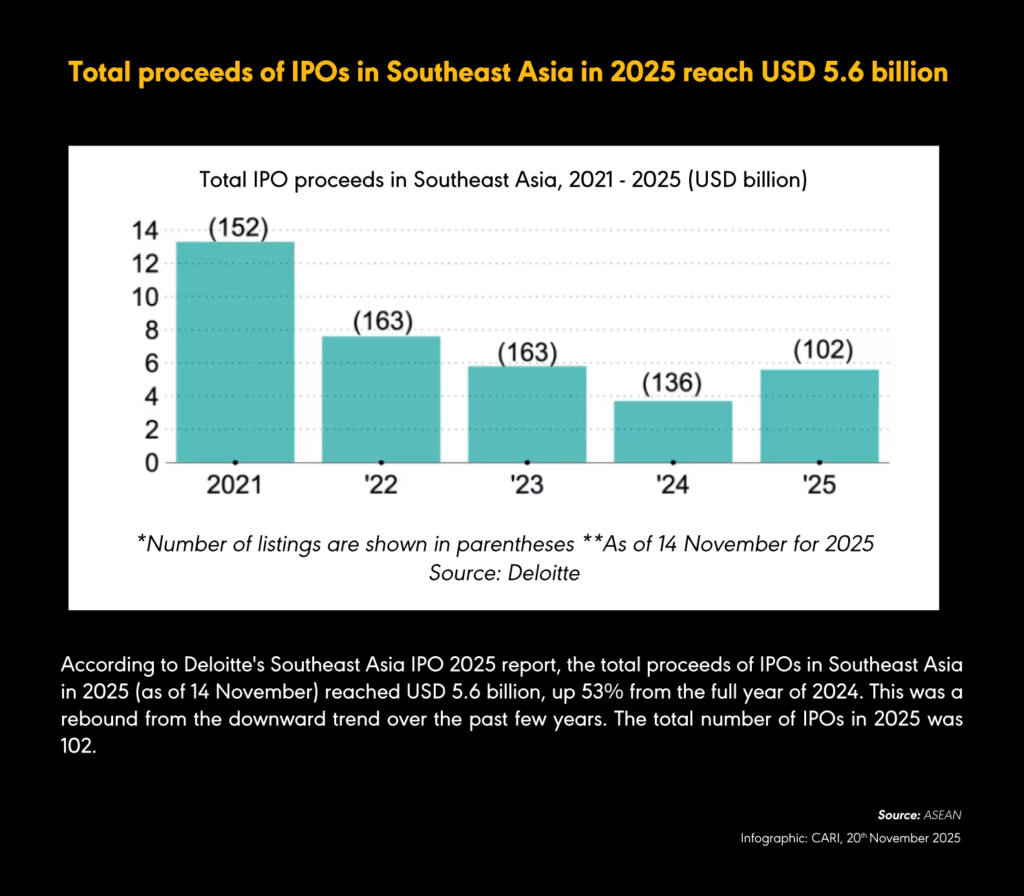

ASEAN

Total IPO proceeds in Southeast Asia in 2025 reach USD 5.6 billion

(19 November 2025) Southeast Asian IPO proceeds reached USD 5.6 billion as of 14 November, up 53% from full-year 2024 despite the number of deals falling to 102 from last year’s 136, according to Deloitte’s Southeast Asia IPO 2025 report. Deloitte attributed the rebound to larger issuers and an average deal size rising to USD 65 million from USD 27 million. Singapore led by total proceeds of USD 1.6 billion from nine listings, including NTT DC REIT (USD 824 million) and Centurion Accommodation REIT (USD 597 million), while Viet Nam raised a combined USD 1 billion from Techcom Securities (USD 525 million) and VPBank Securities (USD 484 million). Malaysia recorded 48 IPOs raising USD 1.1 billion; Indonesia saw 24 deals totalling USD 921 million, led by Merdeka Gold Resources (USD 279 million) and Chandra Daya Investasi (USD 144 million); major regional listings also included Thailand’s Mr. D.I.Y. unit (USD 174 million) and the Philippines’ Maynilad Water Services (USD 583 million). The report noted that 27 Southeast Asian companies listed in the U.S. raised USD 329 million, and three listed in Hong Kong raising USD 588 million. Deloitte expects sustained momentum into 2026, supported by regulatory reforms, improved sentiment and cross-border pipelines, though tariff policies, trade tensions and issuer caution may influence timing and offer sizes.

MALAYSIA, UNITED STATES

Malaysia-United States Reciprocal Trade Agreement to expand US market access for Penang

(18 November 2025) Penang’s Chief Minister told the state assembly that the Malaysia–United States Reciprocal Trade Agreement (ART) is expected to expand market access for the state’s electrical and electronics sector in the US, attract new foreign direct investment and generate additional high-skilled employment, while also strengthening workforce training to meet high-technology industry requirements. He said ART is projected to support agricultural commodities, including natural rubber, palm oil and food products by enabling value-added activities and access to premium markets, despite Penang not being a major producer. For the halal sector, he stated that ART would provide tariff-free access for local halal SMEs to the US, facilitating their integration into high-value global supply chains and reinforcing growth in ready-to-eat and processing segments. The Chief Minister added that the state is reviewing measures to enhance the halal ecosystem, including strengthening Jakim halal branding, expanding automation and exploring new export markets, and noted that the government will continue broader resilience and competitiveness initiatives through InvestPenang.

MALAYSIA

October trade data shows 15.7% year-on-year rise in exports

(19 November 2025) Malaysia’s October trade data showed a 15.7% year-on-year rise in exports, exceeding Bloomberg’s forecast of under 8%, supported by higher shipments to Singapore (+MYR 5.1 billion), Hong Kong (+MYR 2.7 billion), the European Union (+MYR 2.5 billion) and Taiwan (+MYR 2.3 billion), alongside a MYR 14 billion increase in electrical and electronics (E&E) exports; additional gains were recorded in palm oil and palm-based agriculture, optical and scientific equipment and metal manufacturing. Re-exports grew 36.4% to MYR 39.1 billion, accounting for 26.4% of total exports, while domestic exports rose to MYR 109.2 billion (73.6%). Imports increased 11.2% to MYR 129.3 billion, driven by higher inflows from China (+MYR 8.7 billion), Taiwan (+MYR 3.2 billion), Costa Rica (+MYR 2.8 billion) and Viet Nam (+MYR 2.2 billion), with E&E imports up MYR 12.6 billion and metalliferous ores and metal scrap up MYR 1.4 billion. Capital goods imports rose 51.9% to MYR 18.7 billion and consumption goods increased 3.6% to MYR 10.0 billion, while intermediate goods declined 5.7% to MYR 59.2 billion. Month-on-month, exports increased 6.7% and imports 8.9%, narrowing the trade surplus by 6.1% from MYR 20.0 billion to MYR 19.0 billion, though the surplus was 58.9% higher year-on-year. Total trade reached a record MYR 277.6 billion in October, bringing cumulative trade for the first 10 months to MYR 2.5 trillion.

INDONESIA

Indonesia records first trade surplus in 10 quarters and largest relative to GDP since Q4 2022

(20 November 2025) Indonesia recorded a current account surplus of USD 4 billion, equivalent to 1.1% of GDP, in the July–September quarter, marking its first surplus in 10 quarters and the largest relative to GDP since Q4 2022, driven by a larger goods trade surplus and higher oil and gas export values supported by rising crude prices; this follows a 0.8% of GDP deficit in Q2 2025. Despite the improvement in the current account, the balance of payments posted a USD 6.4 billion deficit, slightly narrower than the USD 6.7 billion deficit in the prior quarter. Bank Indonesia reported a surplus in direct investment, indicating positive investor sentiment towards economic prospects and the investment climate, while portfolio investment registered a deficit due to foreign capital outflows from the bond market and higher private-sector foreign debt repayments. The central bank revised its full-year current account forecast to a range between a 0.1% surplus and a 0.7% deficit of GDP, compared with its earlier projection of a 0.5% to 1.3% deficit.

VIET NAM

Heavy rainfall in Dak Lak province delays harvesting of robusta coffee

(20 November 2025) Heavy rainfall in Viet Nam’s main coffee-producing province of Dak Lak has delayed harvesting and increased risks to the 2025–26 robusta crop, with small plantations in Krong Bong already flooded and some trees toppled; farmers report threats of root rot and damage to near-harvest cherries if downpours continue, and the regional hydro-meteorology department expects worsening conditions through at least Sunday. Severe flooding has submerged 70% of a 300-hectare farm managed by the Thang Binh cooperative, with damage still being assessed. Industry representatives noted that only about 15% of the crop has been harvested, with rain slowing both collection and ripening. The Vietnam Coffee and Cocoa Association had previously projected a 10% year-on-year production increase for 2025–26, potentially the largest crop in four years, contingent on favourable weather. Robustas have risen in London since late July on expectations of strong demand for Vietnamese supply, and indications of crop damage could add further upward pressure.

THE PHILIPPINES

Philippine bonds draw increased interest as investors price in more rate cuts

(20 November 2025) Philippine bonds are drawing increased interest as investors price in about 22 basis points of Bangko Sentral ng Pilipinas rate cuts over the next three months, following a surprise reduction that lowered the policy rate to its weakest level since 2022 amid political uncertainty triggered by a corruption scandal that led to the removal of two cabinet ministers and the appointment of Frederick Go as finance secretary; Western Asset Management is evaluating whether his appointment signals fiscal shifts but still anticipates declining yields. Philippine 10-year yields stand near 5.9%, and Western Asset Management projects a fall to around 5.75% by end-2025 and 5.5% by end-Q1 2026. The scandal has prompted a shift to safer assets, with local equities down over 2% this quarter, the worst in Southeast Asia, while Q3 GDP growth slowed to its weakest pace since 2021. Rate-cut expectations in the Philippines exceed those in Malaysia and South Korea, where swaps imply stable policy, and in India and Thailand, where only 10–20 basis point cuts are expected. Strong demand at auctions reflects this sentiment, with a 10-year Philippine bond drawing 4.43 times its issue size—the highest in more than a decade—compared with Malaysia’s 1.9 times and Thailand’s 2.83 times. Major investors, including Brandywine Global Investment Management, hold overweight positions in Philippine government bonds based on high real yields, easing growth, a widening output gap and expectations of further monetary easing.

MALAYSIA, SINGAPORE, BRUNEI DARUSSALAM

The Future of Investment and Trade (FIT) Partnership urges rules-based trading

(19 November 2025) The Future of Investment and Trade (FIT) Partnership, a new grouping of 16 small and medium-sized economies including Singapore, Malaysia, New Zealand, Brunei Darussalam, Chile, Costa Rica, Iceland, Liechtenstein, Morocco, Norway, Panama, Rwanda, Switzerland, the UAE and Uruguay, held its first in-person ministerial meeting and endorsed a joint declaration committing to “concrete actions” in areas such as supply chain resilience, investment facilitation and emerging trade issues; Malaysia and Paraguay formally joined at the meeting. The bloc represents 3.6% of global GDP, and Singapore’s Deputy Prime Minister and Trade Minister, who chaired the meeting, emphasised the aim of strengthening a predictable, open and rules-based order while clarifying that FIT is not a free trade agreement and carries no binding obligations. The minister said discussions began two years ago and that the partnership seeks to pilot practical trade and investment measures, with members now focused on developing and implementing initiatives that remain at a conceptual stage. Malaysia’s Deputy Minister underscored the need to address vulnerabilities and prepare for future crises through multilateral cooperation. Singapore currently serves as coordinating partner, with New Zealand set to take over in mid-2026, and the next ministerial meeting will be held in Auckland next year.

RCEP Monitor

CHINA

Urban youth unemployment rate declines to 17.3% in October

(18 November 2025) China’s urban youth unemployment rate for those aged 16–24 excluding students declined to 17.3% in October from 17.7% in September, according to the National Bureau of Statistics, though labour market pressures persist following the entry of 12.2 million graduates over the summer and the August spike to a post-2023-revision high. Graduates are increasingly pursuing alternatives to corporate employment, including further study and the national civil service exam, with 3.72 million applicants registered for the upcoming test compared with 38,100 available positions, creating a ratio of roughly one successful candidate for every 98 applicants; Beijing has also raised the exam’s age limit. Individual jobseekers report limited interview opportunities despite broad applications across sectors, citing economic unpredictability and a preference for stable civil service roles. The unemployment rate for those aged 25–29 excluding students remained at 7.2% in October, while China’s overall urban jobless rate declined to 5.1% from 5.2% in September.

CHINA

China accelerates consolidation of small and midsize financial institutions

(18 November 2025) China is accelerating consolidation of small and midsize financial institutions exposed to weak public-investment lending, with Inner Mongolia merging 120 lenders into Inner Mongolia Rural Commercial Bank in May and Henan combining 25 lenders into a new bank in February; the National Financial Regulatory Administration reported a net reduction of 225 institutions in the first half of 2025, exceeding the 195 decline recorded in all of 2024. Most closures involved rural institutions, which account for about 80% of China’s financial entities, and further mergers are under way, including 13 institutions in Jilin and planned consolidation in Xinjiang, driven by economic slowdown, population outflows and mounting local government financial stress. Local authorities face sharply reduced land-sale revenue, down around 60% from its 2021 peak, and rising off-budget debt linked to unprofitable local government financing vehicles, with IMF estimates placing outstanding LGFV debt at roughly CYN 60 trillion in 2023; Beijing has committed CYN 10 trillion over five years to contain hidden debt, though analysts argue the scale remains insufficient. The Central Committee’s recommendations for the 2026–2030 plan call for coordinated risk management across real estate, local government debt and small and medium financial institutions. Regional banks hold nearly CYN 1.4 trillion in nonperforming loans despite CYN 530 billion in public support over five years, raising concerns that bad-loan levels could increase without economic improvement. While mergers are expected to create economies of scale, analysts emphasise the need for stronger governance, noting past issues including misconduct, supervisory failures and the near-collapse of Baoshang Bank in 2019.

JAPAN

Economy contracts annualised 1.8% in July-September quarter, first decline in six quarters

(17 November 2025) Japan’s economy contracted an annualised 1.8% in the July–September quarter, or 0.4% quarter-on-quarter, marking the first decline in six quarters and narrower than the median market estimate of 2.5% annualised and 0.6% quarterly, with government data attributing the downturn mainly to weaker exports following the implementation of a baseline 15% US tariff on most Japanese imports. Net external demand subtracted 0.2 percentage points from growth after contributing 0.2 points in the previous quarter, as automaker shipment volumes fell sharply following earlier front-loading before tariff increases. Housing investment declined due to tighter energy-efficiency regulations introduced in April. Private consumption rose 0.1%, in line with expectations but slower than the 0.4% increase in the second quarter, while capital spending grew 1.0%, exceeding the 0.3% estimate. Economists characterised the contraction as driven by one-off factors such as housing investment and maintained a view of gradual recovery over the next one to two years. A Japan Centre for Economic Research poll of 37 economists forecasts a 0.6% expansion in the fourth quarter. The data coincides with Prime Minister Sanae Takaichi’s government preparing a stimulus package in response to high living costs, with advisers likely to cite weak GDP results in calling for caution in Bank of Japan rate-hike plans.

|

15 participating countries |

20 chapters |

2.2 billion |

US$26.2 trillion |

28% |

| ASEAN member states, Australia, China, Japan, South Korea, New Zealand | trade in goods and services, investment, intellectual property, e-commerce, competition, SMEs, economic and technical cooperation, and government procurement | combined population, 30% world’s population | combined GDP, 30% global GDP | global trade (based on 2019 figures) |