LIFTING-THE-BARRIERS REPORT 2013 | AVIATION

Published date: November 2013

TABLE OF CONTENT

(Click any topic to read the related section)

- EXECUTIVE SUMMARY

- FULL REPORT

- The ten member states of the Association of Southeast Asian Nations (ASEAN) have identified a 2015 deadline to establish an ASEAN Single Aviation Market (ASAM) for the liberalisation of air transport services in the region. Also referred to as the “ASEAN Open Skies” policy, the aim is to have the ASAM in place by the time the proposed ASEAN Economic Community (AEC) takes effect in 2015.

- This Report analyses the barriers confronting the aviation sector in ASEAN, including but not limited to those raised by the ASAM. It identifies the strategies required to overcome or lift the relevant barriers, including the policy decisions that governments should make in the light of rapid changes to the aviation industry.The Big Picture and Changing Aviation Dynamics

- The profile of the aviation industry in ASEAN is changing rapidly. Low-cost carrier (LCC) operations now account for more than half of all airline capacity (international plus domestic) in Indonesia, the Philippines and Malaysia. The next highest LCC penetrations rates are in Singapore, Thailand and Vietnam, with emerging economies like Myanmar, Cambodia and Lao PDR growing strongly from relatively low bases. The vibrant economies in ASEAN and greater Asia mean that more passengers and cargo are being transported by air, and increasingly by LCCs. The tremendous growth in LCC capacity is expected to continue well into the next decade even as the relative market shares of full-service carriers (FSCs) decline.

- Infrastructure. Yet, governments in ASEAN have not made adequate policy changes to accommodate the LCC phenomenon. In particular, infrastructure needs are not being met quickly enough. Airports or terminals dedicated to LCC operations remain the exception in ASEAN. Policies intended to spur LCC travel by making it more cost-efficient and accessible are also lacking, e.g. by reducing airport and user charges and passenger taxes. Existing airport terminals and runways are growing near or beyond capacity, leading to increasing congestion and longer delays.

- Several intra-ASEAN international routes are now the busiest LCC sectors in the world. This reflects the specific problem that there are few viable alternative airports in the region from which LCCs can operate. Diverting LCC traffic to smaller airports will significantly relieve the infrastructure and slot congestion issues at the ASEAN primary airports.

- Recent huge aircraft orders by LCCs are compounding the problem, as are the rapid establishments of new LCCs in the region. The LCCs’ standard operating model – using smaller planes that make more trips in a day – has the effect of increasing terminal and runway usage rates. With market access liberalisation being pursued within ASEAN, most of the new planes on order will end up being deployed in the region. This may have the effect of further compounding the congestion and infrastructural problems.

- Governments must thus pay more attention to airport capacity investments. A significant policy re-think is required on issues like secondary airports and budget terminals to relieve congestion at primary airports. Securing private sector financing for such secondary facilities should be a priority. At the same time, governments should look into lowering airport charges to incentivise airlines to relocate to these facilities.

- Slots. One infrastructure-related problem relates to slot constraints: the shortage of suitable and convenient landing and take-off slots throughout the day. The issue could be a function of a lack of terminal space, runway congestion or air traffic restrictions. Slot problems require a whole array of solutions, ranging from employing technology to facilitating more landings and take-offs to using market-based slot allocation mechanisms. Within ASEAN, member states should begin discussions on whether and how a more coordinated response to the slot problem can be forged.

- Human Capital. The projected growth in aviation will also impose tremendous pressure on the provision of human capital, particularly pilots and maintenance personnel. The provision of training facilities will thus have to be accelerated to meet this demand. The region will benefit from harmonised programmes for pilot training and licensing. Training centres should receive common accreditation to ensure harmonised standards and quality. Overall, the demand for aviation professionals should ideally be managed and met on a regional, rather than national basis. This way, manpower can be positioned anywhere in the region as market demand dictates. Commonly-agreed certification standards should be recognised by all ASEAN member states so that enforcement efforts need not be duplicated and costs can be reduced.

- ASEAN Regulator. There is a need for ASEAN member states to consider establishing a common regional regulator. The ASAM project should thus take on the issue of creating an ASEAN regulator to oversee technical matters. Such a body could take the form of a Joint Aviation Committee comprising the respective member states’ civil aviation authorities. Eventually, it could become an independent administration altogether. The regulator could legislate harmonised technical standards relating to air traffic management (ATM), safety, security, as well as customs, immigration and quarantine (CIQ) matters. Cross-border enforcement should be facilitated, so that an inspection conducted by one authority can be recognised as valid by the other authorities.

- The Environment and Future Sustainability. The region could also benefit by moving toward harmonised requirements on aircraft carbon emissions. Issues relating to sustainable growth and the use of biofuels and environmentally-friendly construction materials also require a concerted regional stand.

- A United Stand for External Relations. There is a critical need for an increasingly integrated ASEAN to craft a common external policy for aviation matters. This involves coordinating the individual member states’ positions to reach a united negotiating stand on issues ranging from climate change to traffic rights. This will strengthen the member states’ collective bargaining position when negotiating with bigger trading partners.The ASEAN Single Aviation Market (ASAM)

- The liberalisation of the ASEAN air transport sector is directed at both the provision of air passenger and air freight (cargo) services. Multilateral agreements have been adopted to replace the traditional bilateral air services agreements between states that often contain market restrictions. The multilateral agreements tackle the two key areas for liberalising the sector: (i) market access for carriers from other member states and (ii) ownership and control of carriers by nationals of other member states.

- Market Access. For market access liberalisation, the ASEAN multilateral agreements do away with the so-called third, fourth and fifth freedom restrictions. Hence, Member State A’s carriers can conduct unlimited operations between A and Member State B (third freedom), between B and A (fourth freedom), and between A and Member State C through B (fifth freedom). These relaxations are fairly modest in that they do not involve the seventh freedom operations or domestic services within member states. Hence, A’s carriers cannot conduct stand-alone international operations between B and C (seventh freedom), or domestically within B or C (domestic carriage).

- Even so, the relatively modest third, fourth and fifth freedom relaxations have not been accepted by a number of ASEAN member states, particularly the biggest economy in the region, Indonesia. To protect their carriers’ market share, governments have traditionally restricted the capacity of foreign carriers operating into and out of their territories. Such protection takes place despite compelling economics-based evidence that liberalisation brings significant benefits to the overall economy. Such benefits include more competition among providers and greater choice for users, and with that, lower fares and freight rates for the travelling public and exporters. In addition, there are significant indirect benefits for tourism, travel-related businesses and inward foreign investment. While the local airlines are likely to lose some market share as a result of increased access for foreign carriers, they will also benefit on the whole from a significant increase in volumes carried and revenues generated.

- That said, there have been recent positive signs in Indonesia that the government is prepared to liberalise further. In particular, significant capacity relaxations have been offered in bilateral agreements with some states. In addition, Indonesia’s own carriers are expanding their operations rapidly, leading to their own need for more liberal market access into other ASEAN states. At the same time, Indonesian carriers have begun to establish joint venture subsidiaries in other ASEAN states. Such expansion is only possible with greater reciprocal liberalisation among all ASEAN member states.

- The ASEAN Secretariat, the other member states and their respective carriers should continue to engage the Indonesian government and its carriers to encourage them to accept the ASEAN agreements fully. Co-operative ventures with Indonesian carriers (e.g. in the form of joint ventures and code-sharing) should be encouraged to provide incentives for these carriers to support ASEAN’s liberalisation efforts. In time, as Indonesian carriers become more competitive and grow their own overseas operations, they will require greater reciprocal access into other ASEAN states as well. This will boost the ASAM project significantly, with benefits for all players.

- The ASAM project currently stops with the third, fourth and fifth freedom relaxations. This is detrimental as it renders the Single Aviation Market incomplete and “single” only in name. The result is that airline operations remain restricted by artificial barriers erected by governments, despite the economic justifications for lifting such barriers. The true potential of airlines and the economic growth they can stimulate by carrying more passengers and cargo at more efficient cost remain unrealised. The ASEAN member states must thus go beyond the current liberalisation agenda to give each other’s airlines the seventh freedom and domestic operation rights. This way, they will have the full benefit of a common market to operate freely between any two points in the region. Hence, carriers from Member State A should eventually be allowed to mount flights between Member States B and C, or even within B or C, without the flight having to originate and terminate in A.

- While such operations are controversial, they are needed in the long run to forge a truly liberalised common market in ASEAN. This Report recommends a phased timetable to allow the commencement of seventh freedom and domestic services by ASEAN carriers, beginning with points that are hitherto not connected by direct flights, points that are not capital cities, and eventually the capital cities. However, these are likely to attract some political opposition. As such, where domestic carriage is contentious and threatens to derail liberalisation of seventh freedom operations, the latter should take priority. In other words, domestic carriage relaxations can be left for a later period while seventh freedom should be freed up more urgently.

- Ownership and Control. Apart from market access barriers, there are significant ownership and control restrictions in existence. In ASEAN member states, airlines must typically subscribe to the traditional “substantial ownership and effective control” rule. This means that all carriers must be majority-owned (i.e. beyond 50%) by the nationals of their own designating or home state. To liberalise this rule, the ASEAN member states should accelerate efforts to recognise “community carriers” that can be majority-owned by ASEAN nationals taken cumulatively. Hence, a Cambodian-registered carrier need not necessarily be majority-owned by Cambodian nationals; instead, it can be majority-owned by a mixture of ASEAN nationals. This will be a departure from the traditional concept of an airline having to be majority-owned by nationals of its home state.

- The “community carrier” concept will enable airlines to raise capital from across the region rather than from their home states alone. This will especially help airlines in the less developed member states that need more foreign investments in their aviation sector. In addition, it will facilitate mergers among ASEAN airlines so that they can compete more effectively against airlines from outside the region. Presently, the “community carrier” concept exists only in theory under the ASEAN multilateral agreements, and no such carrier has actually been established to date. This is largely because the member states retain the discretion to deny such community carriers the rights to operate to their points. This creates uncertainty for any investor wishing to establish such a carrier.

- One way to lift this barrier is for member states to retain the traditional ownership rule for their own carriers only, if they so wish. For other ASEAN carriers, the “community carrier” model should be allowed and welcomed, with no threat of market access being denied. Eventually, all restrictions on ownership and control by ASEAN nationals, even for member states’ own airlines, should be phased out. This can only be logical for a true “single” aviation market to appear. In sum, liberalisation of market access and of ownership/control rules must naturally be pursued as a package. It would be meaningless for ASEAN to recognise a community carrier (that is owned by a multitude of ASEAN interests) if this carrier’s market access to other member states can be constricted by these states at their discretion.

- External Relations. Seventh freedom rights are also crucial for ASEAN carriers to operate from anywhere in the region to external points, e.g. in a third state like China. Without such rights, the ASEAN carriers could end up being disadvantaged as against carriers from third states with a unified home market. Hence, without seventh freedom liberalisation, a Philippine carrier can have unlimited operations to China but only from its own home points. In comparison, a Chinese airline can connect any point in China with any point in ASEAN. This creates a network imbalance that can only be rectified if the ASEAN member states start to treat their own backyard as a true common market. Hence, the Philippine carrier must be allowed seventh freedom rights to connect Vietnam, Thailand, Indonesia and indeed, all of ASEAN with China.

- Such concerns highlight ASEAN’s lack of a united negotiating stand when it engages with third countries. The problem is complicated because ASEAN lacks a mechanism like that which exists in the European Union (E.U.) to compel member states to prioritise the regional interest over individual national interests. ASEAN needs its biggest economies (the natural leaders for negotiations with external trading partners), to embrace intra-ASEAN liberalisation and to lead the region. At its core, the problem has to do with the uneven level of development and competitiveness among member states’ airlines. Deeper intra-ASEAN liberalisation must thus be forged so that the region’s airlines do not end up becoming disadvantaged against airlines from outside the region. This is a risk that ASEAN member states and their airlines cannot continue to ignore.

- Committing to overcome infrastructural, slot and human capital constraints

- Continuing to liberalise market access and ownership/control rules for a true ASAM

- Establishing an ASEAN regulator to oversee and enforce harmonised standards

- Fostering a united ASEAN negotiating stand as against other countries and regions

- Singapore carriers from Phuket to Shanghai

- Malaysian carriers from Cebu to Guangzhou

- Vietnamese carriers from Siem Reap to Kunming

- Chinese carriers from Ho Chi Minh City to Manila

- AN ANALYSIS OF THE ASEAN COOPERATION IN TRANSPORT

- ASEAN NEEDS TO ADOPT BASE STANDARDS ACROSS THE REGION AS FIRST STEP TOWARDS HARMONISATION

- LIFTING-THE-BARRIERS REPORT FOR ASEAN AVIATION

- LIFTING-THE-BARRIERS REPORT 2015: AIR TRANSPORTATION

EXECUTIVE SUMMARY

Conclusion

25. Policy-makers in the region must seize the opportunity to re-think their strategies for ASEAN aviation. In the face of the rapidly- changing dynamics of the airline industry, the following priorities should guide policy-making in the future:

Facilitating cost reduction and efficiencies for all airline operations, FSC and LCC

FULL REPORT

Introduction

The ten member states of the Association of Southeast Asian Nations (ASEAN) have identified a 2015 deadline to establish an ASEAN Single Aviation Market (ASAM) to liberalise the provision of air transport services in the region. Also referred to as the ASEAN “Open Skies” policy, the aim is to have the ASAM arrangement in place by the time the proposed ASEAN Economic Community (AEC) takes effect in 2015.

This Report analyses the barriers facing the aviation sector in ASEAN, including but not limited to those raised by the ASAM. It identifies the strategies required to overcome or lift the relevant barriers, particularly the policy changes that governments should undertake in response to the rapidly evolving aviation industry.

I. The Big Picture: Changing Aviation Dynamics in ASEAN

A. Infrastructure Constraints

The face of ASEAN aviation is changing rapidly and significantly. Low-cost carrier (LCC) operations now account for more than half of all airline capacity (international plus domestic) in Indonesia (56%), the Philippines (51%) and Malaysia (50%). The next highest LCC penetrations rates are 31% in Singapore, 30% in Thailand and 24% in Vietnam (see Table 1).

The LCCs’ share of capacity is expected to increase even more dramatically in the next decade. For sure, there is still ample room for growth in populous markets like Indonesia, Vietnam and Thailand. On their part, the emerging economies of Myanmar, Cambodia and Lao PDR can be expected to grow strongly, albeit from relatively low bases. Compared to the lacklustre situation in the developed economies, the vibrant economic growth in ASEAN and greater Asia has also meant increasing travel and exports within the region. A large proportion of such growth is being captured by the LCCs, and increasingly on long-haul sectors too.

In fact, LCC operations have proven to be consistent, all-weather growth generators for airports in ASEAN. In 2009, recognised as a tough year for aviation worldwide, growing LCC traffic was a resilient feature at all leading ASEAN airports. For instance, Singapore Changi Airport saw passenger traffic and aircraft movements grow robustly in that year on the back of LCC operations, even as the shares contributed by long-haul flights and full-service carriers (FSCs) slipped. In 2009 alone, LCC passenger traffic and aircraft movements at Changi increased a dramatic 50% over the previous year. Across ASEAN, such momentum has continued well into the present and is expected to hold steady for the future.

Yet, ASEAN governments on the whole do not appear to have made adequate policy changes to accommodate the LCC phenomenon. In particular, the LCCs’ infrastructure needs are not being addressed quickly enough. Airports or terminals dedicated to LCC operations remain the exception in ASEAN. Only Bangkok Don Mueang counts as a dedicated LCC airport, while the soon-to-be-opened Kuala Lumpur International Airport 2 (KLIA2) fashions itself as a “hybrid” terminal for both LCCs and FSCs. Some governments are spending large amounts of money to build new airports or terminals mainly for traditional FSCs. This is often borne out of their belief that the “hub” status of major airports must be protected by reinforcing the operations of FSCs, particularly the national carriers. Policies intended to encourage or spur LCC travel by making it more cost-efficient and accessible are also lacking, e.g. by reducing airport and user charges and passenger taxes.

Other governments are not investing adequately in general airport infrastructure, be this for FSCs or LCCs. Major airports like Jakarta Soekarno-Hatta, Manila Ninoy Aquino and Bangkok Suvarnabhumi have reached saturation point and even exceeded their intended capacity. This has naturally resulted in increasing congestion and ever longer delays. The re-opening of Bangkok Don Mueang to cater to LCC operations is a reminder of the infrastructural constraints posed by the LCCs’ spectacular continuing growth. Such constraints will become even more of a challenge in the near future as the LCC “boom” continues. This is made more acute by the fact that LCCs typically use smaller planes that make more take-off and landing frequencies in a day.

Recent huge aircraft orders by LCCs compound the problem. The Lion Air and AirAsia groups alone have more than 1,000 aircraft on order between them. Other LCCs like Cebu Pacific, Tigerair, Nok Air and Jetstar are expanding as well. Newer LCCs like Malindo, Philippines AirAsia, Tiger Mandala and VietJet Air have also started operations. With increasing market access liberalisation within ASEAN, most of the new planes on order will end up servicing ASEAN skies. Quite apart from whether the skies are truly open, there is now a significant gap between aircraft orders and infrastructure expansion efforts.

Governments must thus pay more attention to airport capacity investments, particularly those relevant to LCC operations. Airport competition and connectivity issues require forward planning, and not just with FSC considerations in mind. A significant re-think is required on issues like secondary airports (e.g. Bangkok Don Mueang, Manila Clark, Jakarta Halim Perdanakusuma) and hybrid terminals (e.g. KLIA2) to relieve the congestion at primary airports. Securing private sector financing for such facilities should be a priority. At the same time, governments should provide for lowered airport charges to incentivise airlines to relocate to these facilities.

B. Slot Constraints

A particularly acute infrastructure-related problem relates to the availability of suitable landing and take-off slots. “Slots” refer to the facility for an aircraft to land and take off within a desired time period, and to have access to the usual services such as aerobridges, ramps and ground-handling. In this regard, busy airports like Jakarta Soekarno-Hatta and Manila Ninoy Aquino are already stretched near or beyond capacity. Airlines already face difficulties mounting new flights to and from these airports because of congestion and the unavailability of convenient landing and take-off slots.

At some airports, the problem is a function of lack of terminal space (e.g. aerobridges for aircraft to park and handle passengers). Elsewhere, the problem could be due to runway congestion and the need for additional runways, such as at Singapore Changi. Airspace restrictions that affect the efficiency of aircraft landings and take-offs can also contribute to slot problems. The situation is particularly serious during the desired peak periods in the day, and some airlines have been forced to arrive and take off at unfavourable hours such as after midnight. This raises new problems such as the unavailability of customs, immigration and quarantine (CIQ) personnel and land transport options to and from the city centre during non-peak hours.

Slot issues are complicated and require holistic policies that balance user (i.e. airline) and provider (i.e. airport) needs. In the short term, employing more sophisticated air traffic and runway control technology could provide for more landing and take-off slots per hour without compromising safety. At the same time, market-based slot allocation mechanisms such as exchanges and auctions have been used in congested airports such as London Heathrow, often with some controversy. At some airports, airlines with unused slots have been forced to return them to the common pool, while antitrust/competition law authorities have been known to force co-operating airlines to surrender slots to prevent them from becoming too dominant at particular airports.

The LCC “boom” has naturally contributed to these slots problem and associated congestion at major airports in ASEAN. The fact is that six intra-ASEAN routes are now among the ten busiest international LCC sectors in the world. This is testimony to the LCCs’ spectacular growth in ASEAN (see Table 2). At the same time, it reflects the specific problem in ASEAN of there being few viable alternative airports from which LCCs can operate. In other words, a high level of LCC traffic in ASEAN still operates from the primary airports. Diverting LCC traffic to smaller airports (as has been done with Bangkok Don Mueang) will significantly relieve the infrastructure and slot congestion issues at the ASEAN primary airports.

Within ASEAN, member states should begin discussions on how a more coordinated response to the slot problem can be forged. The ASEAN Single Aviation Market (ASAM) project has thus far focused on liberalising air traffic rights, with little discussion on slots. Yet, with rights being progressively freed up, the extra flights mounted by airlines capitalising on “open skies” liberalisation could end up causing even more congestion and imposing more stress on slots.

C. Human Capital Constraints

The projected growth in aviation will also impose tremendous pressure on the provision of human capital, particularly pilots and maintenance personnel. The airline industry projects that the Asia-Pacific region alone will require 185,000 more pilots and 243,500 maintenance personnel for the next 20 years. The provision of training facilities will thus have to be accelerated in the coming years to meet this demand.

The region will thus benefit tremendously from a harmonised programme for pilot training and licensing. Training centres should receive common accreditation to ensure harmonised standards and quality. The ASAM project should look into such issues in a manner similar to, though not necessarily identical with how the European Union (E.U.) has addressed them. Overall, the demand for aviation professionals should be managed and met on a regional, rather than national basis. This way, manpower can be positioned anywhere in the region as market demand dictates, with commonly-agreed certification standards recognised by all ASEAN member states. This reduces costs for airlines, governments and the individuals concerned (e.g. trainee pilots) and increases efficiencies all around.

D. An ASEAN Regulator?

Some of the above issues raise the need for a common regional regulator. Moving forward, the ASAM project should steer the region toward creating an ASEAN regulator to oversee technical matters. Initially, such a body might take the form of a Joint Aviation Committee comprising the member states’ respective civil aviation authorities. Eventually, it could mature into an independent administration with a regional mandate.

The regulator would be in charge of legislating and enforcing harmonised standards relating to air traffic management (ATM), safety, security, and other technical matters in line with the requirements of the International Civil Aviation Organisation (ICAO). As a first step, the standards need not be uniform, but harmonised to a sufficient degree so as to afford co-operation in cross-border enforcement. For example, a harmonised set of safety rules for aircraft inspections can be applied to airlines by all member states’ national authorities, and an inspection conducted by one authority should be accepted by the others as adequate or valid for a period of time. This will save resources and avoid duplication in enforcement. At the same time, regional co-operation in customs, immigration and quarantine (CIQ) procedures can be enhanced to combat problems like human trafficking.

Harmonised standards, particularly if overseen by a common regulator, have the advantages of increasing the reliability of monitoring and compliance, reducing duplication and costs, and enhancing the overall effectiveness of the system. Of course, such harmonisation requires the necessary “levelling-up” of resources and capabilities across all ASEAN member states. This is a significant challenge, given the varying levels of development across member states. Technical training would have to be provided by the more advanced member states, as well as by states and aid agencies from outside the region.

E. The Environment and Future Sustainability

The region could also benefit by forging harmonised requirements on contemporary issues such as aircraft carbon emissions. The linkage between aviation and climate change has already emerged as a controversial issue with the E.U. unilaterally subjecting aviation to its Emission Trading Scheme (ETS). Issues relating to the sustainable growth of the industry also require a concerted regional stand or strategy. Moving forward, such issues include the use of biofuels and alternative construction material for aircraft and aircraft parts.

F. A United Stand for External Relations

The above issues highlight a critical need for an increasingly integrated ASEAN to craft a common external policy for aviation matters. This involves coordinating the individual member states’ positions to reach a united negotiating stand. Such a move will strengthen the member states’ collective bargaining position when negotiating with bigger trading partners such as China, India, the E.U. and the U.S. As noted above, one issue requiring a common stand is aircraft carbon emissions. Another critical area is negotiating market access rights with other countries (see below).

II. Overview of the ASEAN Single Aviation Market (ASAM)

The liberalisation of the air transport sector in ASEAN is directed at both the provision of air passenger and air freight (cargo) services. In this regard, the concept of progressive liberalisation of air transport services had been laid out by an Action Plan for ASEAN Air Transport Integration and Liberalisation 2005-2015. This Action Plan, together with an accompanying document known as the Roadmap for Integration of Air Travel Sector (RIATS), had identified the target date of 2015 for achieving an effective “open skies” regime for the region.

To this end, three multilateral agreements have been adopted to formalise the intra-ASEAN liberalisation of aviation in the following key areas:

i. market access by foreign carriers (i.e. carriers from other ASEAN member states); and

ii. ownership and control of local carriers by foreign nationals (i.e. from other ASEAN member states)

A. Market Access

Pursuant to the ASAM objective, the ASEAN member states have adopted several multilateral agreements designed to provide unlimited third, fourth and fifth freedom operations within the region. Hence, member states that are contracting parties to these agreements agree to liberalise the following operations such that they become unlimited in terms of frequency and capacity of operations and aircraft type used:

i. “Third freedom” – this refers to the right of a carrier designated by Member State A to carry passengers, cargo and baggage for profit from a point in Member State A to a point in Member State B.

Example: Thai Airways’ (TG) operation from Bangkok to Singapore, or Phuket to Bali, or Chiang Mai to Hanoi.

ii. “Fourth freedom” – this is the same airline’s corresponding right in the reverse direction.

Example: The same TG flight returning from Singapore to Bangkok, or Bali to Phuket, or Hanoi to Chiang Mai.

iii. “Fifth freedom” – the same right but with an additional right in both directions to make a stopover in Member State C to discharge and take on traffic for profit.

Example: TG operation between Bangkok and Singapore, but with a stopover in Kuala Lumpur in both directions to discharge and take on traffic.

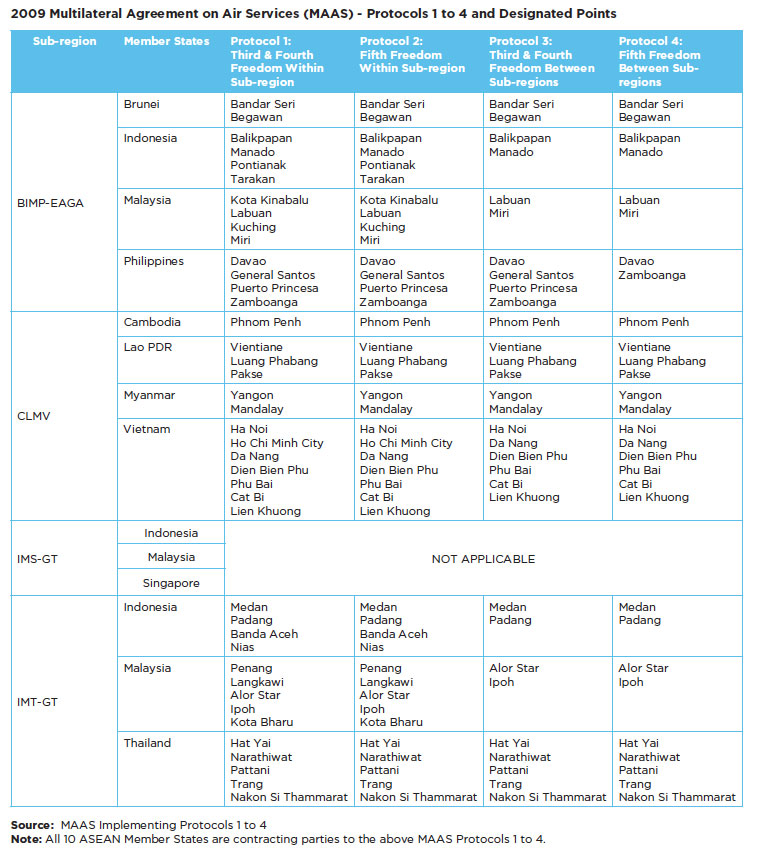

The specific multilateral agreements, their scope and the current member state parties are detailed in the following table:

B. Ownership and Control

The traditional bilateral air services agreements between states typically require airlines designated by either state to be “substantially owned and effectively controlled” by that state and/or its nationals. The effect of such a requirement is to prevent foreign majority shareholding and control of an airline, as well as to prohibit the cross-border merger of airlines (see discussion below on Barriers). The ASEAN multilateral agreements described above attempt to relax this requirement by providing member states with the following three options on ownership and control (these are listed from least to most liberal):

III. Benefits of Liberalisation

Before analysing the specific barriers that confront the liberalisation of the airline industry in ASEAN, it is important to highlight the numerous comprehensive studies that have detailed the benefits of air services liberalisation for ASEAN economies. In general, most studies are in unanimous agreement as to the overall benefits, including increased choice, more competition, lower fares and lower freight rates for passengers and exporters; increased tourism and foreign investment revenue; increased employment in airline-related jobs, and positive growth for all kinds of related ancillary services. At the same time, the studies acknowledge that incumbent local carriers are generally expected to lose market share to foreign competitors, although this is made up for by increased volumes and revenue as liberalisation stimulates overall traffic growth for all sides.

A. Malaysia and Thailand

An Intervistas Consulting report1 released in 2006 concluded that the liberalisation of air services between Thailand and Malaysia brought substantial benefits to both countries in 2005. The liberalisation covered unlimited third and fourth freedom rights, entailing no restrictions on points served in either country, multiple designation of airlines and open code-sharing rights. The following benefits were estimated to accrue to each country:

An Intervistas Consulting report released in 20092 concluded the following benefits for Singapore arising from liberalised air services agreements:

The most recent comprehensive study for Indonesia was released in June 2011 by the Indonesia Infrastructure Initiative (IndII), an Australian-funded aid programme.3 The study sought to quantify the benefits for Indonesia in the year 2025 of implementing an “Open Skies” policy. “Open Skies” was understood as the liberalisation of air services between the ten ASEAN member states in the following areas: relaxation of existing bilateral agreements between member states, existing restrictions on airline designation, market entry/access, frequency, capacity, schedules, products, code-sharing, tariffs and ownership and control . The study quantifies the following substantial benefits of an “open skies” policy for Indonesia by 2025:

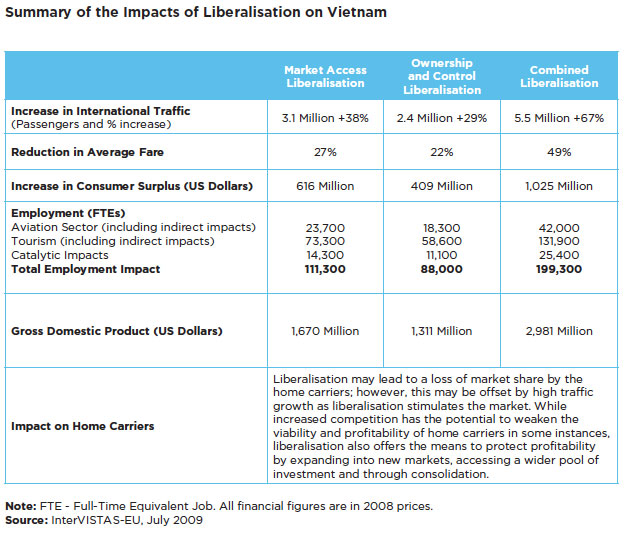

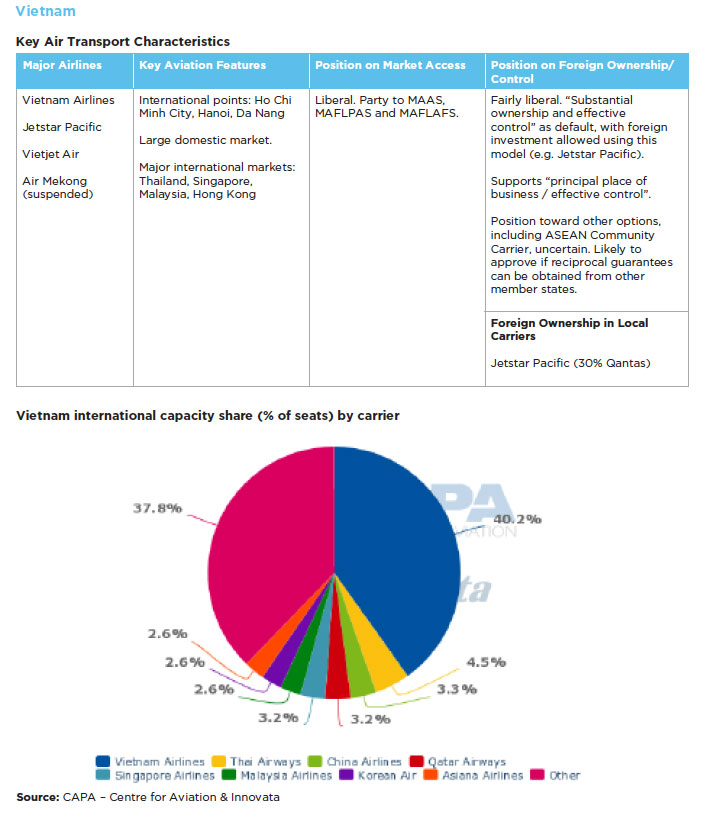

D. Vietnam

An Intervistas Consulting report released in 20094 concluded the following benefits for air services liberalisation for Vietnam:

E. Malaysia, Thailand, Singapore and the Philippines

The following summary provides information on the contribution of aviation to the economies of four ASEAN member states. The figures reflect absolute contributions, as opposed to incremental benefits arising from liberalisation.

IV. Lifting the Barriers to Liberalisation

A. Barrier #1. Several Member States Have Not Yet Accepted the ASEAN Agreements and Protocols

From Table 3 above, it can be seen that several ASEAN member states have yet to accept (or in legal language, to “ratify” or to become “contracting parties” to) the relevant Protocols of the ASEAN multilateral agreements. The Protocols contain the actual substantive commitments for market access and ownership and control relaxations. All the Protocols have now entered into force and are binding, though only for those member states which have ratified them. Hence, if all ten ASEAN member states were to ratify all the Protocols, an unlimited third, fourth and fifth freedom regime between and among all international points in ASEAN will come into full effect.

As noted in Table 3, the member states’ ratification status is as follows:

2009 Multilateral Agreement on Air Services (MAAS)

Protocols 1 to 4 for the liberalisation of flights between and among sub-regions

Ratified by all 10 member states

Protocol 5 for the liberalisation of third and fourth freedom flights between the capital cities

Ratified by all member states except for Indonesia and the Philippines

Protocol 6 for the liberalisation of fifth freedom flights among the capital cities

Ratified by all member states except for Indonesia and the Philippines

2010 Multilateral Agreement for the Full Liberalisation of Air Passenger Services (MAFLPAS)

Protocol 1 for the liberalisation of third and fourth freedom flights among all cities

Ratified by all member states except for Indonesia and Lao PDR

Protocol 2 for the liberalisation of fifth freedom flights among all cities

Ratified by all member states except for Indonesia and Lao PDR

2009 Multilateral Agreement for the Full Liberalisation of Air Freight Services (MAFLAFS)

Protocol 1 for the liberalisation of flights among designated points

Ratified by all member states except for Indonesia

Protocol 2 for the liberalisation of flights among all points with international airports

Ratified by all member states except for Indonesia

The individual states’ motivations require elaboration. The main non-contracting party is Indonesia. Spanning 17,000 islands and home to nearly half the entire ASEAN population, Indonesia has the region’s largest land area, population, economy and air travel market. Its capital, Jakarta, is ASEAN’s biggest city by population and also the headquarters of the ASEAN Secretariat. Given its size and influence, Indonesia’s non-acceptance of the ASEAN agreements substantially affects the entire ASAM project.

One explanation for Indonesia’s position is its carriers’ lobbying of their government to continue protecting their international operations against those of competitor airlines from neighbouring ASEAN states. Through the Indonesian National Air Carriers Association (INACA), the local carriers have (particularly in the recent past) opposed efforts to open up the ASEAN air travel market entirely. As explained below, the situation could be different today.

INACA’s traditional concern lies with the stronger airline competitors from the other ASEAN member states, principally Singapore and Malaysia, whom they fear will dominate the international market between Indonesia and these countries. The Indonesian position is that as a huge archipelago, it has hundreds of points to offer international aviation, whereas the other states have relatively fewer to offer (indeed, Singapore has all of one!). In INACA’s view, this represents a systemic imbalance for exchanging traffic rights.

In recent years, such dynamics have led the Indonesian government to propose only five points for an “open skies” policy with its neighbours – the major cities of Jakarta, Surabaya, Medan, Makassar and Bali. At the same time, there have been calls by INACA to implement a selective or “partial” open skies policy with some ASEAN neighbours, even if full “open skies” can be accepted and implemented with others. This suggests that access into the five cities can be fully or partially open, depending on where the foreign carrier is from. Naturally, such a “pick and choose” policy is inconsistent with the ASEAN multilateral agreements and the overall integration aims of ASAM and the ASEAN Economic Community (AEC).

In itself, the offer of the five major cities is to be welcomed, as long as it applies equally to all ASEAN member states and their airlines. Even if falling short of full relaxations, it will effectively open up a sizeable amount of the international market into and out of Indonesia. This is because the five cities (particularly the capital, Jakarta) account for the bulk of international traffic into and out of the country.

However, the reality is that some interests in Indonesia remain opposed to full and unlimited access into Indonesia for foreign carriers, especially those from Singapore and Malaysia. This is consistent with the “partial” or selective open skies policy advocated by INACA. In large part, the concern revolves around the sixth freedom operations of certain foreign airlines. The “sixth freedom” is actually a simple combination of a “fourth freedom” (e.g. a Singapore carrier’s Jakarta-Singapore operation) with a connecting “third freedom” operation (from Singapore to anywhere else). This is the familiar operating model of major “sixth freedom” carriers worldwide such as Singapore Airlines, Emirates, Etihad, KLM, Korean Air, Turkish Airlines and Qatar Airways.

In essence, “sixth freedom” hub operations depend simply on two factors – a geographically strategic “hub” airport in the centre of airline routes to serve as a transit stop, and unlimited third and fourth freedom rights to operate to numerous “spoke” points. Due to the Indonesian carriers’ relatively limited international operations, most travellers from Europe, North America and Northeast Asia travel into and out of Indonesia on foreign carriers’ sixth freedom operations. The major operator in this regard is Singapore Airlines, which channels these travellers through its hub at Singapore Changi Airport. In recent years, the highly successful Malaysian LCC, AirAsia, has also begun to transport the budget-minded segment of travellers in this same manner through its hub at Kuala Lumpur International Airport.

The discomfort with such sixth freedom operations accounts in part for Indonesia’s cool reception toward the ASEAN multilateral agreements. This extends to MAAS Protocol 5 that opens up unlimited third and fourth freedom access into and out of Jakarta (although, as flagged below, such reluctance may be dissipating as Indonesian carriers themselves expand their operations across the region). Since third and fourth freedom flights form the backbone of sixth freedom operations, staying out of MAAS Protocol 5 could be seen as a strategy to restrict rival carriers’ sixth freedom operations into and out of Jakarta, and with that, the rest of the country.

For the Indonesian carriers, Jakarta itself may be too big a prize to give up even if it constitutes only one point in the sprawling archipelago. Indeed, Jakarta accounts for the bulk of the Indonesian economy and is the principal gateway into the country. At the same time, opening up the other points will allow foreign carriers to bypass the main hub at Jakarta and to carry unlimited traffic directly into secondary points such as Bali, Surabaya, Medan and Lombok. This will affect the business of local airlines that thrive on domestic connecting traffic. This has long been a concern of Indonesian carriers, and it explains their resistance to MAFLPAS, the agreement that opens up the non-capital cities.

Such considerations shape the Indonesian government’s traditional preference for bilateral, instead of multilateral agreements. In turn, this has had the effect of restricting the other ASEAN carriers’ operations into Indonesia, subjecting them to finite capacity that has to be negotiated bilaterally. At the same time, the Indonesian position affects the ASAM liberalisation project significantly. In the process, the travelling public misses out on concrete benefits such as increased competition and lower fares. In addition, Indonesia’s connectivity to the region and the outside world remains relatively low.

The airlines’ lobbying influence has to be contrasted with the position of other stakeholders in the Indonesian economy. As might be expected, sectors such as the tourism industry greatly welcome the economic advantages that air services liberalisation might bring. Indeed, the benefits of such liberalisation for the overall Indonesian economy are obvious – greater choice and lower fares for the travelling public and cargo exporters, increased business and tourist arrivals, and positive overall effects for export-oriented businesses, inward foreign investment, airport and ancillary services and indeed, the entire economy (see Part III above on Benefits of Liberalisation).

In recent years, several provincial governments in Indonesia have also emerged as keen lobbyists to champion direct flights by foreign airlines into their cities. These provincial authorities recognise that tourism and foreign investment could grow faster if there were greater direct connectivity to key regional cities such as Singapore, Bangkok and Kuala Lumpur. Indeed, a recent economic study commissioned by the Indonesian central government and published by the Indonesia Infrastructure Initiative (IndII) (see Part III above) had identified benefits of around 6 trillion Rupiah (US$650 million) in additional GDP that could potentially accrue to the overall economy if an “open skies” policy were adopted by 2025.

As indicated above, the neighbouring states’ efforts to relax market access into Indonesia have had to be pursued bilaterally. For instance, up till early 2013, the Singapore carriers’ passenger capacity entitlement between Singapore and Indonesia (especially Jakarta) was close to being exhausted. However, in January 2013, both sides came to an agreement to increase capacity substantially on the routes between Singapore and Jakarta as well as other points such as Surabaya, Bali and Medan.

The Indonesian government had agreed to such reciprocal but incremental additions only after capacity on the Indonesian side had itself come close to being reached. This followed the requests by several Indonesian carriers, particularly LCCs such as Lion Air and Indonesia AirAsia, to expand their operations into Singapore from various Indonesian points. In turn, the reciprocal adjustments allowed Singapore Airlines and Singapore-based LCCs such as Tigerair and Jetstar Asia to increase their own operations into Indonesia, including Jakarta. While capacity has now been significantly increased between Indonesia and Singapore, there are still overall limits that remain controlled by the bilateral agreement between both sides.

Overall, despite Indonesia’s traditional stance toward liberalisation, the recent capacity revision with Singapore indicates some positive signs. It shows that the Indonesian carriers are likely to support (or not object to) capacity increases for foreign carriers when they themselves come close to exhausting their own capacity limits to fly to other states. Indeed, the Indonesian carriers are expanding their services rapidly across the region, showing a capability and willingness to compete with their regional rivals. Lion Air has even established a subsidiary, Malindo, in Malaysia, taking the challenge to the doorstep of its rival, AirAsia. In essence, Lion Air is seeking to penetrate AirAsia’s home market the same way the latter has entered Indonesia. Another subsidiary, Thai Lion Air, is scheduled to commence operations in Thailand in late 2013. Lion Air is thus seeking to replicate AirAsia’s success with Indonesia AirAsia and its other joint venture subsidiaries in the region.

Such expansions – particularly in light of the huge aircraft orders that airlines like Lion have made – can only be made possible through greater reciprocal liberalisation of market access rights among ASEAN member states. In other words, the Indonesian carriers will themselves need and benefit from greater ASEAN liberalisation. In the light of such developments, there are encouraging signals that Indonesia’s policy on the ASEAN agreements could be evolving. Indeed, the Indonesian government is reportedly considering the ratification of MAAS Protocols 5 and 6. When this happens, it will be a huge boost for the ASAM project and the entire region.

Meanwhile, the Philippine government has embraced MAFLPAS Protocols 1 and 2 to open up access to its secondary cities. At the same time, it has kept its capital Manila restricted and has not accepted MAAS Protocols 5 and 6. The government justifies its decision by reference to the shortage of landing and take-off slots and overall runway congestion at central Manila’s Ninoy Aquino International Airport. In this regard, the government’s preference is to liberalise access into the alternative airport at Clark, the former U.S. airbase that is some 80 kilometres northwest of downtown Manila. Indeed, access into Clark has been fully open to carriers from other ASEAN states for some years now.

While the Philippine government’s concern over congestion at Ninoy Aquino International is understandable, its attempt to link traffic rights and airport slots is problematic. Indeed, these are separate matters that should be kept distinct. In particular, the lack of slots at an airport should not prevent member states from ratifying the ASEAN agreements to liberalise market access rights and to signal support for ASEAN’s market integration commitments. Linking slots to access rights is also a negative precedent in that it encourages air rights negotiators to use congestion and lack of airport slots (which may be within the competence of other government agencies) as reasons to delay their commitment to regional agreements.

The individual states’ motivations require elaboration. The main non-contracting party is Indonesia. Spanning 17,000 islands and home to nearly half the entire ASEAN population, Indonesia has the region’s largest land area, population, economy and air travel market. Its capital, Jakarta, is ASEAN’s biggest city by population and also the headquarters of the ASEAN Secretariat. Given its size and influence, Indonesia’s non-acceptance of the ASEAN agreements substantially affects the entire ASAM project.

One explanation for Indonesia’s position is its carriers’ lobbying of their government to continue protecting their international operations against those of competitor airlines from neighbouring ASEAN states. Through the Indonesian National Air Carriers Association (INACA), the local carriers have (particularly in the recent past) opposed efforts to open up the ASEAN air travel market entirely. As explained below, the situation could be different today.

INACA’s traditional concern lies with the stronger airline competitors from the other ASEAN member states, principally Singapore and Malaysia, whom they fear will dominate the international market between Indonesia and these countries. The Indonesian position is that as a huge archipelago, it has hundreds of points to offer international aviation, whereas the other states have relatively fewer to offer (indeed, Singapore has all of one!). In INACA’s view, this represents a systemic imbalance for exchanging traffic rights.

In recent years, such dynamics have led the Indonesian government to propose only five points for an “open skies” policy with its neighbours – the major cities of Jakarta, Surabaya, Medan, Makassar and Bali. At the same time, there have been calls by INACA to implement a selective or “partial” open skies policy with some ASEAN neighbours, even if full “open skies” can be accepted and implemented with others. This suggests that access into the five cities can be fully or partially open, depending on where the foreign carrier is from. Naturally, such a “pick and choose” policy is inconsistent with the ASEAN multilateral agreements and the overall integration aims of ASAM and the ASEAN Economic Community (AEC).

In itself, the offer of the five major cities is to be welcomed, as long as it applies equally to all ASEAN member states and their airlines. Even if falling short of full relaxations, it will effectively open up a sizeable amount of the international market into and out of Indonesia. This is because the five cities (particularly the capital, Jakarta) account for the bulk of international traffic into and out of the country.

However, the reality is that some interests in Indonesia remain opposed to full and unlimited access into Indonesia for foreign carriers, especially those from Singapore and Malaysia. This is consistent with the “partial” or selective open skies policy advocated by INACA. In large part, the concern revolves around the sixth freedom operations of certain foreign airlines. The “sixth freedom” is actually a simple combination of a “fourth freedom” (e.g. a Singapore carrier’s Jakarta-Singapore operation) with a connecting “third freedom” operation (from Singapore to anywhere else). This is the familiar operating model of major “sixth freedom” carriers worldwide such as Singapore Airlines, Emirates, Etihad, KLM, Korean Air, Turkish Airlines and Qatar Airways.

In essence, “sixth freedom” hub operations depend simply on two factors – a geographically strategic “hub” airport in the centre of airline routes to serve as a transit stop, and unlimited third and fourth freedom rights to operate to numerous “spoke” points. Due to the Indonesian carriers’ relatively limited international operations, most travellers from Europe, North America and Northeast Asia travel into and out of Indonesia on foreign carriers’ sixth freedom operations. The major operator in this regard is Singapore Airlines, which channels these travellers through its hub at Singapore Changi Airport. In recent years, the highly successful Malaysian LCC, AirAsia, has also begun to transport the budget-minded segment of travellers in this same manner through its hub at Kuala Lumpur International Airport.

The discomfort with such sixth freedom operations accounts in part for Indonesia’s cool reception toward the ASEAN multilateral agreements. This extends to MAAS Protocol 5 that opens up unlimited third and fourth freedom access into and out of Jakarta (although, as flagged below, such reluctance may be dissipating as Indonesian carriers themselves expand their operations across the region). Since third and fourth freedom flights form the backbone of sixth freedom operations, staying out of MAAS Protocol 5 could be seen as a strategy to restrict rival carriers’ sixth freedom operations into and out of Jakarta, and with that, the rest of the country.

For the Indonesian carriers, Jakarta itself may be too big a prize to give up even if it constitutes only one point in the sprawling archipelago. Indeed, Jakarta accounts for the bulk of the Indonesian economy and is the principal gateway into the country. At the same time, opening up the other points will allow foreign carriers to bypass the main hub at Jakarta and to carry unlimited traffic directly into secondary points such as Bali, Surabaya, Medan and Lombok. This will affect the business of local airlines that thrive on domestic connecting traffic. This has long been a concern of Indonesian carriers, and it explains their resistance to MAFLPAS, the agreement that opens up the non-capital cities.

Such considerations shape the Indonesian government’s traditional preference for bilateral, instead of multilateral agreements. In turn, this has had the effect of restricting the other ASEAN carriers’ operations into Indonesia, subjecting them to finite capacity that has to be negotiated bilaterally. At the same time, the Indonesian position affects the ASAM liberalisation project significantly. In the process, the travelling public misses out on concrete benefits such as increased competition and lower fares. In addition, Indonesia’s connectivity to the region and the outside world remains relatively low.

The airlines’ lobbying influence has to be contrasted with the position of other stakeholders in the Indonesian economy. As might be expected, sectors such as the tourism industry greatly welcome the economic advantages that air services liberalisation might bring. Indeed, the benefits of such liberalisation for the overall Indonesian economy are obvious – greater choice and lower fares for the travelling public and cargo exporters, increased business and tourist arrivals, and positive overall effects for export-oriented businesses, inward foreign investment, airport and ancillary services and indeed, the entire economy (see Part III above on Benefits of Liberalisation).

In recent years, several provincial governments in Indonesia have also emerged as keen lobbyists to champion direct flights by foreign airlines into their cities. These provincial authorities recognise that tourism and foreign investment could grow faster if there were greater direct connectivity to key regional cities such as Singapore, Bangkok and Kuala Lumpur. Indeed, a recent economic study commissioned by the Indonesian central government and published by the Indonesia Infrastructure Initiative (IndII) (see Part III above) had identified benefits of around 6 trillion Rupiah (US$650 million) in additional GDP that could potentially accrue to the overall economy if an “open skies” policy were adopted by 2025.

As indicated above, the neighbouring states’ efforts to relax market access into Indonesia have had to be pursued bilaterally. For instance, up till early 2013, the Singapore carriers’ passenger capacity entitlement between Singapore and Indonesia (especially Jakarta) was close to being exhausted. However, in January 2013, both sides came to an agreement to increase capacity substantially on the routes between Singapore and Jakarta as well as other points such as Surabaya, Bali and Medan.

The Indonesian government had agreed to such reciprocal but incremental additions only after capacity on the Indonesian side had itself come close to being reached. This followed the requests by several Indonesian carriers, particularly LCCs such as Lion Air and Indonesia AirAsia, to expand their operations into Singapore from various Indonesian points. In turn, the reciprocal adjustments allowed Singapore Airlines and Singapore-based LCCs such as Tigerair and Jetstar Asia to increase their own operations into Indonesia, including Jakarta. While capacity has now been significantly increased between Indonesia and Singapore, there are still overall limits that remain controlled by the bilateral agreement between both sides.

Overall, despite Indonesia’s traditional stance toward liberalisation, the recent capacity revision with Singapore indicates some positive signs. It shows that the Indonesian carriers are likely to support (or not object to) capacity increases for foreign carriers when they themselves come close to exhausting their own capacity limits to fly to other states. Indeed, the Indonesian carriers are expanding their services rapidly across the region, showing a capability and willingness to compete with their regional rivals. Lion Air has even established a subsidiary, Malindo, in Malaysia, taking the challenge to the doorstep of its rival, AirAsia. In essence, Lion Air is seeking to penetrate AirAsia’s home market the same way the latter has entered Indonesia. Another subsidiary, Thai Lion Air, is scheduled to commence operations in Thailand in late 2013. Lion Air is thus seeking to replicate AirAsia’s success with Indonesia AirAsia and its other joint venture subsidiaries in the region.

Such expansions – particularly in light of the huge aircraft orders that airlines like Lion have made – can only be made possible through greater reciprocal liberalisation of market access rights among ASEAN member states. In other words, the Indonesian carriers will themselves need and benefit from greater ASEAN liberalisation. In the light of such developments, there are encouraging signals that Indonesia’s policy on the ASEAN agreements could be evolving. Indeed, the Indonesian government is reportedly considering the ratification of MAAS Protocols 5 and 6. When this happens, it will be a huge boost for the ASAM project and the entire region.

Meanwhile, the Philippine government has embraced MAFLPAS Protocols 1 and 2 to open up access to its secondary cities. At the same time, it has kept its capital Manila restricted and has not accepted MAAS Protocols 5 and 6. The government justifies its decision by reference to the shortage of landing and take-off slots and overall runway congestion at central Manila’s Ninoy Aquino International Airport. In this regard, the government’s preference is to liberalise access into the alternative airport at Clark, the former U.S. airbase that is some 80 kilometres northwest of downtown Manila. Indeed, access into Clark has been fully open to carriers from other ASEAN states for some years now.

While the Philippine government’s concern over congestion at Ninoy Aquino International is understandable, its attempt to link traffic rights and airport slots is problematic. Indeed, these are separate matters that should be kept distinct. In particular, the lack of slots at an airport should not prevent member states from ratifying the ASEAN agreements to liberalise market access rights and to signal support for ASEAN’s market integration commitments. Linking slots to access rights is also a negative precedent in that it encourages air rights negotiators to use congestion and lack of airport slots (which may be within the competence of other government agencies) as reasons to delay their commitment to regional agreements.

On its part, it is unclear why Lao PDR has not ratified MAFLPAS and its Protocols 1 and 2. It is likely that internal consultations are still ongoing within the Lao government and that ratification will happen soon. It should be noted that Cambodia has very recently in 2013 submitted instruments of ratification for MAFLPAS and Protocols 1 and 2, becoming the latest member state to accept these agreements.

As for the liberalisation of air freight (cargo) services, this is considered an equally critical component of the regional economic integration effort, given the export-oriented nature of ASEAN economies. It is generally the case that states are less sensitive to foreign carriers’ air freight operations compared to passenger services. For one thing, governments tend to care less about how their exports arrive at destinations, as long as the cargo is transported efficiently and at reasonable cost. At the same time, there is much less political or sentimental attachment associated with the transport of cargo. Typically, air freight services can also be conducted during off-peak hours (indeed, usually at night), thereby relieving airport and slot congestion problems.

Yet, this does not mean that all states readily grant unlimited market access for foreign cargo carriers. As with air passenger transport, the nature and dynamics of airline competition are hugely relevant. It must be noted that the relevant ASEAN multilateral agreements – the MAFLAFS and its Protocols – apply to all-cargo transportation only, i.e. carriage on dedicated cargo aircraft or freighters. Like with passenger services, the third, fourth and fifth freedom relaxations apply to carriage wholly within ASEAN only, and not to points outside the region or domestic carriage within a member state.

MAFLAFS Protocol 1 provides for unlimited third, fourth and fifth freedom all-cargo traffic rights between specific points designated by member states. Protocol 2 frees up similar rights for all points in ASEAN with international airports. Consistent with the less controversial nature of cargo transport, MAFLAFS grants unlimited fifth freedom rights along with third and fourth freedom rights. This contemplates the reality of air freight services – cargo flights typically operate from Points A to B, and onwards to C, D, E and so on, without strict requirements on returning to the carrier’s home states (unlike passenger operations). At each point along the route, there are typically minimal or no capacity restrictions on discharging and picking up cargo.

In ASEAN, there are only several all-cargo carriers that operate dedicated freighters. These include the cargo arms of Singapore Airlines, Malaysia Airlines and Thai Airways, as well as specialised cargo carriers that can be found in several member states. Both types of specialised all-cargo operators provide competition to the regular airlines that carry cargo in the holds of their passenger aircraft (the so-called “combination carriers”). The fact that Indonesia has not accepted the MAFLAFS Protocols reflects its carriers’ concerns that the extensive all-cargo operations of neighbouring countries’ carriers affect their own cargo business. These Indonesian carriers include regular airlines like Garuda (operating combination carriers) as well as specialised cargo airlines such as Cardigair, Tri MG and Republic Express.

Recommendations to Lifting-The-Barriers

Lifting the barriers here is relatively straightforward. The ASEAN Secretariat, the member states’ governments as well as the region’s airlines must continue to engage the Indonesian government and its carriers to encourage them to accept all the ASEAN agreements and the associated Protocols. The following steps can be taken:

i. ASEAN member states and their airlines should facilitate Indonesian carriers to grow operations into their points. As far as possible, member states’ carriers should assist Indonesian carriers in technical and other forms of assistance, and accede to reasonable requests for code-sharing, joint operations and any other form of co-operation. In particular, efforts by Indonesian carriers to establish joint venture subsidiaries in other ASEAN member states should be welcomed. Overall, it is only when Indonesian carriers come close to exhausting their own capacity limits to other states that they are likely to support foreign carriers’ capacity increases into Indonesia. In this regard, there are encouraging signs that Indonesia is considering whether to accept MAAS Protocols 5 and 6 that provide for unlimited third, fourth and fifth freedom capacity between the capital cities.

ii. The region’s airlines should also directly engage the provincial governments in Indonesia to convince them that their economies will benefit if they have greater direct connectivity to key regional cities. To this end, technical development studies funded by overseas aid agencies should emphasise local benefits more, instead of concentrating only on benefits for the entire national economy.

iii. ASEAN member states, their airlines and their business leaders should step up efforts to engage other sectors of the Indonesian economy (apart from airlines) such as the tourism, foreign investment and commodity export sectors. This is to impress on these stakeholders the benefits of a liberalised policy affording unlimited third, fourth and fifth freedom international access for foreign carriers.

iv. Steps should also be taken to engage the Philippine and Lao PDR governments to find out what obstacles they face in ratifying the relevant protocols to the multilateral agreements, and to extend assistance if required. In particular, the Philippine government and airline industry should be encouraged to drop any linkage between market access rights and airport slot capacity, as the two matters should be left distinct.

B. Barrier #2. Seventh Freedom and Domestic Operations Remain Prohibited

If the relatively modest third/fourth and fifth freedom relaxations analysed above do not even enjoy full acceptance from all ASEAN member states, prospects are even bleaker for any further relaxations to “seventh freedom” and cabotage restrictions. The seventh freedom refers to the right of a carrier to connect two international points outside of its home country (e.g. Thai Airways to connect Manila and Jakarta without the flight having to begin or end in Thailand).

A true single or common aviation market such as that which exists in Europe liberalises such seventh freedom operations fully and opens the door for greater market competition throughout the region. For instance, British Airways can now base a stand-alone plane or fleet to operate between Paris and Frankfurt if it wants to, without the flight having to begin or end in the U.K. (unlike fifth freedom flights which still have to). Of course, such operations will provide competition to the third and fourth freedom operations of the French and German airlines on that route, but it is the precise objective of a common market to allow such competition. The fact that British Airways has not chosen to mount such flights is because the Paris-Frankfurt market is too competitive, and not because governments prohibit that operation. Hence, the aim is to let the market, not governments, act as a control.

With ASEAN, however, the multilateral agreements do not even address such seventh freedom operations explicitly since the member states have not achieved consensus on the issue. Similarly, the ASEAN agreements do not tackle the domestic or “cabotage” operations. These are also known in the industry as the “eighth freedom” (if the flight originates in the carrier’s home country, e.g. a Singapore carrier operating Singapore-Jakarta-Bali as a continuing flight) and the “ninth freedom” (the Singapore carrier operating stand-alone flights between Jakarta and Bali without starting or ending in Singapore).

Cabotage remains highly sensitive for countries with large domestic populations. Typically, such operations are reserved exclusively for local airlines. Hence, in the ASEAN countries, no foreign airline – not even from friendly fellow ASEAN member states – can perform domestic flights, and most governments prefer to maintain that status quo. In contrast, the E.U. single or common market allows any E.U. carrier to operate what were previously considered cabotage flights. Hence, Air France can operate between Frankfurt and Berlin (both domestic points within Germany) if it wishes to.

As a result of the prevailing restrictions, the ASAM objectives are fairly modest: market access relaxations stop with the third, fourth and fifth freedoms, and do not extend to the seventh, eighth and ninth freedoms. Consequently, AirAsia (as a Malaysian carrier) cannot base a fleet in Singapore to ply routes between Singapore and third countries as these would be seventh freedom operations that compete head-on with the Singapore carriers. Neither can AirAsia operate between two domestic points in Indonesia. How does this explain AirAsia’s well-known operations in Thailand, Indonesia and the Philippines that allow it to operate from and even within these countries?

What happens in reality is that AirAsia has incorporated subsidiaries in those countries that are technically local airlines. Each subsidiary carries a different airline code and is majority-owned and effectively controlled by local interests (at least on paper). Thus, AirAsia owns only minority stakes – less than 50% – in each of these entities. The result is that Indonesia AirAsia flies as an Indonesian carrier between Jakarta and Singapore, exercising simple third and fourth freedom rights belonging to Indonesia, and not as a Malaysian carrier (if it were, it would be operating a seventh freedom flight).

This is one operating model that industry players have effectively used to get around the governmental prohibitions. In substance, the model allows the AirAsia group to circumvent the seventh freedom prohibition (such operations are not allowed under the bilateral or multilateral agreements) and to effectively operate such flights out of their Bangkok, Jakarta and Manila hubs under a well-known common brand. For the travelling public that does not appreciate legal distinctions, all the AirAsia subsidiaries’ flights are run by a single airline company, particularly since ticket sales are conducted through a common and integrated internet platform. In addition, this operating model allows circumvention of domestic cabotage prohibitions as well – Indonesia AirAsia would be entirely within its right to operate domestic flights between Jakarta and Bali simply because it is an Indonesian carrier.

Recommendations to Lift the Barriers

Seventh freedom and domestic operations are inherently controversial. Yet, the region’s liberalising momentum cannot stop with third, fourth and fifth freedom access alone as this will make the ASAM incomplete and ineffective (see Barrier #4 below for elaboration). Yet, securing agreement on seventh freedom and domestic carriage will be hugely difficult, given the member states’ instincts to protect their own carriers.

It must be remembered that ASEAN is unlike the European Union (E.U.), where there is an institutional mechanism for the European Commission to compel member states to adhere to Community law. There is no such mechanism in ASEAN, and it is probably unrealistic to conceive of one in the near future. Consequently, seventh freedom and domestic relaxations will have to be pursued in a gradual, phased manner using the traditional method of state agreements.

i. Adopting a liberalised attitude toward fifth freedom operations

Seventh freedom operations need not entail stationing an entire, free-standing fleet in another state’s airport (e.g. Singapore Airlines placing a fleet in Kuala Lumpur to operate between that city and points in Thailand). While that would be a “pure” seventh freedom right, it is presently unrealistic to expect ASEAN member states to allow each other’s carriers that right. Moreover, such rights are not presently permitted under the terms of the ASEAN multilateral agreements.

However, within the present wording of MAAS Protocol 6 is the right of carriers to conduct fifth freedom operations linking capital cities in the region (there is similar wording in MAFLPAS Protocol 2 for linking the other cities). Consider the following operation by AirAsia (Malaysia) from Kuala Lumpur, Malaysia to Yangon, Myanmar via Singapore:

Going by the terms of MAAS Protocol 6, the flight would be a legitimate capital-capital-capital fifth freedom operation among three contracting states, with discharge and pick-up rights in Singapore. Yet, because of the geography of the three cities involved, the aircraft would have to “backtrack” to Yangon after Singapore. The result is that it is highly unlikely for there to be many “through traffic” passengers who board in Kuala Lumpur, and who are actually bound for Yangon. The reality is that most, if not the entire planeload of passengers boarding in Kuala Lumpur, are bound for Singapore and will disembark there. A fresh planeload of passengers will thus get on board in Singapore, bound for Yangon.

The flight thus becomes an effective seventh freedom operation for AirAsia from Singapore to Yangon (and vice versa). Yet, nothing in MAAS and its Protocol 6 forbids this operation. In fact, there is even express language to the effect that designated airlines can fly between any of the permitted points (in this case, the three cities) in any combination or order, without directional or geographic limitation, provided the service serves a point in the territory of the Contracting Party designating the airline (in this case, that point is Kuala Lumpur as Malaysia is the designating state). Neither is there any language to curtail the number of passengers that can be disembarked or picked up at the mid-point fifth freedom stop (i.e. Singapore).

Hence, as long as the flight begins in Kuala Lumpur, the Singapore-Yangon sector can be characterised as a continuation of the service from Kuala Lumpur. There is even language in the MAAS Protocol 6 that allows for a “change-of-gauge” (i.e. change of aircraft type) in Singapore and Yangon, although the capacity of both aircraft must be the same and the flight on the new aircraft must be a continuing service from or to the carrier’s home state.

As things stand, AirAsia has reportedly sought the authorisation of the Myanmar and Singapore governments to conduct the above operation. The governments are still undecided on authorising it because there are misgivings about the seventh freedom nature of the operation (seventh freedom not being allowed in the ASEAN agreements). The matter is now scheduled for formal discussion at the inter-governmental ASEAN Transport Working Group (ATWG) and the ASEAN Air Transport Economic Cooperation Sub-Working Group (ATEC). There is a prospect that the member states will deliver an interpretation of the agreements that effectively deems such flights as legitimate. If this eventuates, it will be a significant liberalising move that will herald in more flexible operations region-wide that are unconstrained by capacity, aircraft type and geographic directionality.

However, there is some risk to securing such a liberal interpretation of fifth freedom flights. It could make states like Indonesia and the Philippines become even more wary of becoming party to the ASEAN agreements. This is particularly because these states are geographically located at the periphery of ASEAN. Their cities will thus become natural markets for “back-tracking” operations, e.g. Singapore-Jakarta-Hanoi, Kuala Lumpur-Manila-Phuket or Bangkok-Surabaya-Yangon. Of course, this could be off-set by the prospect of carriers like Garuda and Lion Air performing similar operations throughout the region, although their scale would be much less significant.

Yet another example of an imaginative interpretation of fifth freedom rights is the

following “triangular” operation that involves two aircraft:

Taking a Thai carrier’s operations as the example, the first aircraft (route in red) departs Bangkok for Hanoi and then proceeds to Singapore, with fifth freedom pick-up rights in Hanoi. The second aircraft (route in black) departs Bangkok for Singapore and then Hanoi, with fifth freedom pick-up rights in Singapore. In effect, the Bangkok-Hanoi-Singapore sector is carried out by the first aircraft (in red) while the return journey on this very sector, i.e. Singapore-Hanoi-Bangkok is performed by the other aircraft (in black). This is a simple example where the change-of-aircraft flexibility allows the carrier to have more efficient aircraft utilisation. Hence, instead of eight individual return sectors (A-B, B-C, C-B, B-A, A-C, C-B, B-C, C-A), there are only six (A-B, B-C, C-A, A-C, C-B, B-A). Again, effective seventh freedom flights would arguably have been performed between Hanoi and Singapore. There are numerous other examples of such flexible operations being possible.

ii. Gradual move toward allowing seventh freedom operations