Economic Snapshot: ASEAN Focus Jan 2017 | Cambodia

Published on 23 January 2017

by Dr. Arup Raha and Krzysztof Halladin

With the expected real GDP growth of 7% this year and forecasted 6.9% for both 2017 and 2018, Cambodia continues on a fast pace led by the export of garments, strong construction activity and government spending. The tourism sector was slowing down but it seems to have benefitted in Q3 from new direct flight routes into Cambodia. Good weather conditions this year have somewhat supported the agriculture sector, which had been troubled by low commodities’ prices. The current account has continued to narrow this year thanks to a steady increase in FDI, strong exports of footwear and textiles, and low oil prices on the import side. Although revenue collection is steadily increasing, the government spending is rising at a faster rate, resulting in a higher fiscal deficit. Consumption spending is edging up as is inflation through the surge in food prices. The risks to an overall positive outlook involve the possible slowdown in China and in the EU; the forthcoming elections in 2017 and 2018; the fallout from US rate hike (as the economy is highly dollarized); and rapid credit growth highly concentrated in real estate and construction sectors.

Garment sector, government consumption and construction activity to lead growth

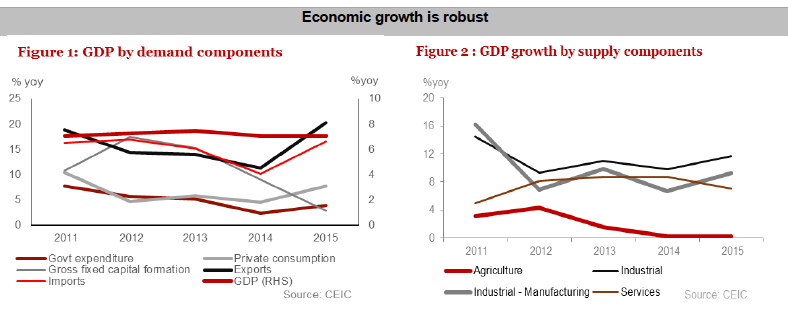

- GDP growth is expected to reach 7% in 2016 and to sustain its trajectory with forecasted rates of 6.9% in 2017 and 2018. The main drivers of growth are garment and footwear exports; continuing expansion in construction activity; and increase in government spending.

- The garment and footwear sector constitutes around 80% of all of Cambodia’s exports and it grew 10.5% to mid-2016 yoy (7.8% for the same period in 2015). The growth is underpinned by the introduction of higher value additions like embroiler or printing, more stable industrial relations and, to the largest extent, by a moderate recovery in the EU (about 40% of all garments exports are to the EU). We expect the garment exports to continue to grow rapidly in coming years, benefiting from China’s move up the value chain. The competition is now from producers in Vietnam or Myanmar.

- The tourism sector was sluggish for the first half of the year, with the growth rate of international tourist arrivals at 2.4 % yoy. There was a big bounce in 3Q16 to 9.2% yoy, most likely driven by new direct flights from Asian countries. The agriculture sector, lethargic due to low commodity prices, will benefit from good weather In the medium term, it might also receive a boost from Chinese investors attracted by Cambodia’s fertile and inexpensive land1.

- Government expenditure is expected to reach 21.7% of GDP, compared with 20.5% in 2015. Most of the spending will be allocated to the wage bill which should provide support to income growth and consumption demand but some are also targeted at urban and rural infrastructure deficits. The increase of government outlay is expected to continue because of upcoming elections.

- The construction sector will continue to grow rapidly with the value of approved projects amounting to US$ 6.8 billion only in the first half of 2016 compared to US$ 3.3 billion for entire 2015. The import of building materials is also on the rise with

that of steel (by volume) increasing by 44.2 % yoy in the first half of the year. The growth rate of construction should moderate gradually in coming years.

Improved external position from FDI and export performance

- The Current account deficit is expected to narrow to 10.2% in 2016, in comparison with 10.6% the previous year, mainly driven by low oil prices, completion of major hydro project, growing remittances and strong FDI mainly from Asian countries (about 40% from China). Gross foreign reserves rose to US$6.4 billion (or 5.4

months of imports) by mid-2016, compared with US$5.6 billion in 2015. - FDI as % of GDP are expected to decrease to 8.5% in 2016 while in 2015 the number was 9.1%. This slight decrease might be contributed to increased regional

competition and uncertainty associated with upcoming elections.

Inflation edging upwards

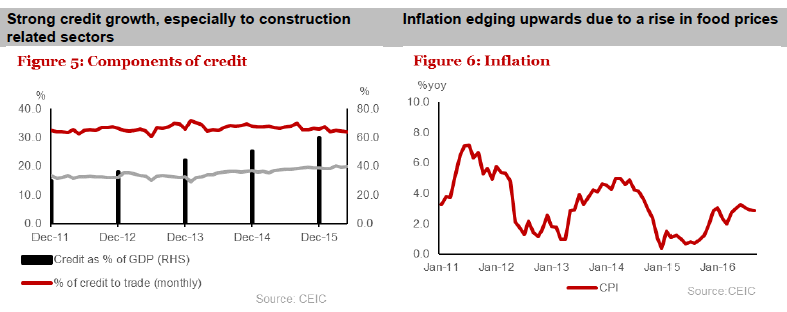

- Although low oil prices kept some components of CPI at bay, higher food prices edged up the inflation rate to 3.06% yoy in July. We expect the inflation at the end of 2016 to reach 3.3%.

Expansionary fiscal budget planned amid improvement in revenue collections

- Fiscal policy is the main demand side policy tool in Cambodia given the limited scope of monetary policy in a highly dollarized and cash-based economy

- Revenue mobilisation is improving and is expected to reach 18.8% of GDP compared to 18.5% the year before, though government spending is increasing at a

faster rate. The fiscal deficit is expected to stretch this year to 2.6% of GDP compared to 1.6% last year; we expect further widening in coming years.

Risks and Other Issues

- Cambodia’s highly concentrated export market (80% of all exports are garments) makes it highly vulnerable to regional competition. The risk is increased when one considers that the materials for production are largely imported from China. Lower growth in China would spill over to Cambodia through channels of tourism, banking and FDI.

- Although there are signs of moderation, credit growth is still very high (26.9% – mid 2016) and has a high concentration in real estate and construction sector. However, the recent introduction of liquidity and minimum capital requirements for financial institutions should provide some comfort.

- Some policies were introduced to promote the use of local currency, yet the economy is still highly dollarized; 95% of all bank deposits are in USD. An appreciation of the dollar will affect the economy in many ways, though mainly through higher prices for tourists.

![]()