Economic Snapshot: ASEAN Focus May 2017 | Currency Outlook

Published on 25 May 2017

by Dr. Arup Raha, Chief Economist, CIMB ASEAN Research Institute & Krzysztof Halladin, Research Fellow, CIMB ASEAN Research Institute

Currency Outlook

We still believe in US dollar strength over the longer term based on a divergence of monetary policy among the large central banks. However, we have revised our year-end forecasts for 2017 to reflect the uncertainties regarding US policy and our belief that the growth outlook is more modest than current consensus expectations.

We expect the current trends of a weaker dollar and soft bond yields to continue for the next few months, but should reverse later in the year as the Fed’s tightening cycle becomes more firmly entrenched. We expect a stronger US dollar next year.

As we had highlighted before1 we believe the key drivers of ASEAN currencies are likely to be the values of the US dollar and the Chinese renminbi. Further influences are likely to come from the direction of commodity prices, the vulnerability of each country to potential outflows, and the policy space available to deal with these outflows.

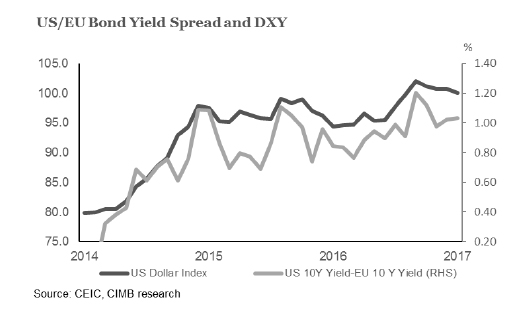

Since January the DXY has been on a downward trend as expectations of US policy have changed. On the fiscal side hopes of a stimulus have gradually faded, while on the monetary side there has been adjustment in projections of how fast and how firmly the Fed would move. The change in expectations was especially noticeable after a dovish statement by the Fed post the March FOMC meeting. Moreover, the difficulty in passing the “repeal and replace” of the Affordable Care Act, which cast a further doubt on the ability of the Trump administration to implement measures — tax cuts, infrastructure spending, and deregulation – promised by Mr. Trump during his campaign and expectation of which had led to a rally in the USD.

Although the Chinese currency was under stress in November of last year, it has been stable since January. This is largely due to a decrease in capital outflows from China, leading to a stable level of FX reserves since February. The curbing of capital outflows has been the result of capital controls and also a weaker US dollar.

Global central banks: Monetary policy divergence

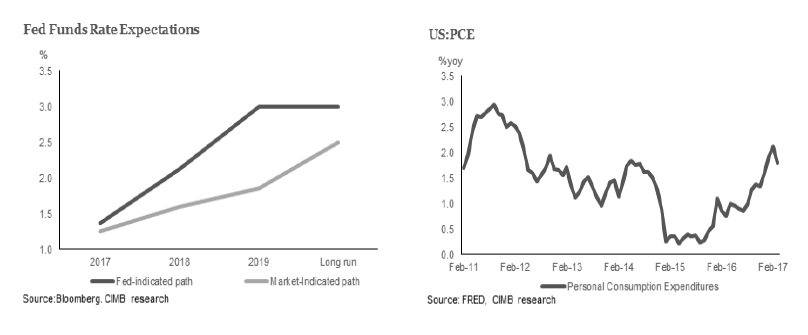

For the Fed, the risks to conducting policy have been asymmetric for some years. With low, indeed near-zero, rates the Fed has been much more equipped to fight inflationary pressures rather than a recession. As such it has been cautious about raising rates in the fear that if such a move was premature, and resulted in a downturn in the economy, its policy options were limited. Moreover, a quick policy reversal would put its credibility in question.

However, with unemployment at 4.4% and wages starting to rise, the economy is at, or near, full employment. Further, Personal consumption expenditure (PCE) inflation is edging up towards the 2% target. As such, regular rate rises are more likely now though the pace is likely to be constrained by the presence of debt and low productivity growth.

The March hike was possibly a signal that the Fed was now firmly on the path to tightening. However, one should recall that expectations regarding rate increases were similar at the start of 2015 and 2016, and yet the Fed delivered only one hike each year (both in December). This, along with the uncertainty over the US administration’s policies, might be why investors are cautious. Hence the median path of hikes illustrated in the Fed’s statement of economic projections diverge with the one indicated by overnight indexed swap rates.

But that also leaves the risk of a sudden adjustment. More hawkish rhetoric by the Fed, supported by hard economic data or tax cuts (or an increase in probability of one) might trigger quick catch up in markets’ long-term expectations driving the dollar up.

Although the Fed has appeared far more comfortable tightening by increasing interest rates, there will come time when it needs to start shrinking its balance sheet. The signaling of this process has already started (i.e. minutes of April Fed meeting) yet there are no details as to how it will be conducted. We expect that the decision about unwinding will come closer to the end of Ms. Yellen’s term, to allow a smoother transition to the next Fed chair.

Our expectation is for two more rate increases this year and two to three more next year, but the actual outcome will depend crucially on fiscal policy (will there be stimulus, how much will it be, and what form will it take?) and hence comes with a fair amount of uncertainty.

The divergence in monetary policy between the Fed and the BOJ is likely to continue. Similarly, the ECB is expected to stay with quantitative easing, even as the Fed raises rates, though the amount of monthly asset purchases is likely to decline further.

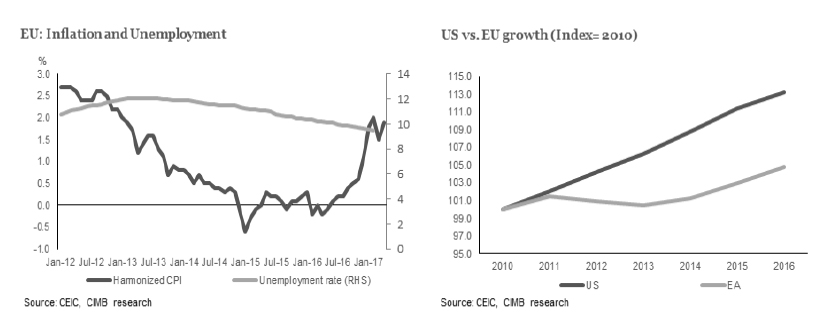

In the EU, economic activity and sentiment has improved. Inflation is picking up and the unemployment rate is declining. Does this warrant monetary tightening? Economic data and sentiment are particularly sound in German where officials are hawkish, worrying about possible overheating. Although, we believe there will be further reduction of asset purchases closer to the end of year, rate hikes are unlikely, and the consensus is that any rate increases are more a 2H18 story.

When Mr. Draghi became president of the ECB in 2012, his first decision was to reverse rate hikes. He is likely to remain dovish, so as not make the mistake of his predecessor who started tightening too early, resulting in the Euro Area sliding back into recession. Moreover, even if GDP growth this year in the Euro Area is higher than in the US, the index of GDP growth since 2010 shows greater slack in the EU and hence for the divergence in rates to persist.

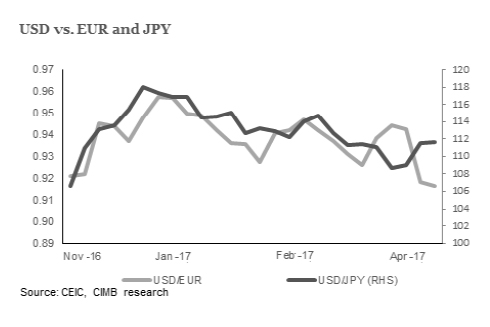

Although the main risk of the French election has faded, there are still some possibly risky events to observe: the election in Germany in September and potentially a new election in Italy. To this add the unresolved issues around Brexit and the Greek debt. Our forecast is EUR/USD 1.08 at the end of 2017.

It is clear that the BOJ is likely to stay with its current stance. Despite its upgrade of growth prospects, the inflation target of 2% is unlikely to be reached by 2018, given that in March core CPI was only 0.2% yoy. The forecast of inflation for FY 2017 was cut to 1.4%. Given the low yielding nature of the JPY, there may still be significant upside on the USD/JPY. Our forecast is USD/JPY 115 at the end of 2017.

The Renminbi: a brief respite

We have maintained for some time that the RMB was likely to weaken in long run under almost all circumstances. That position remains unchanged. Nevertheless, in the last 3 months outflows from China have eased. This is a result of a weaker dollar and effective capital controls. The PBoC’s tightening of Inter-bank repo rates has also alleviated some outflow pressures.

However, in the longer term, with the Fed hiking further, outflow pressures will still be significant. Given China’s Debt to GDP ratio of around 260%, PBoC will be reluctant to increase the benchmark rate in response to higher US rates. In any case, the narrowing of interest rate differentials with US is not the only reason for our expectations of RMB depreciation.

As highlighted before2, the Chinese story is of a structural slowdown being cushioned by fiscal stimulus and credit expansion. The key question was when China would shift emphasis from growth to dealing with the prevalent credit bubble. We think that we are close to that time with tightening measures already starting to show up. But, financial stabilization means deleveraging and hence lower domestic growth.

Yet, at the same time, the authorities cannot give up the ghost of growth, especially heading into the 19th Congress in the autumn. So fiscal policy, to the extent possible, will be simulative. And perhaps, more importantly, the currency will be kept weak to help exports.

Given the current situation, and the markets’ change in emphasis away from growth to stabilization, the authorities have two choices. And under both scenarios, the RMB will be weak. If they still focus on credit-fueled growth and try and meet growth targets, the RMB will weaken as capital outflows are likely to increase. If they change focus to stabilization and deleverage, growth will suffer domestically. They would, then, like to keep the RMB weak by design to get the external sector help cushion that softening of domestic demand. We expect the RMB to be around 7.00 to the USD at the end of 2017, with a faster rate of depreciation to start after the autumn congress.

ASEAN: Resisting the outflows

In the face of rising US yields, a stronger dollar, and a weaker RMB – affecting Asia in different ways – the standard response of Asian currencies will be to weaken versus the US dollar.

As a first cut, ASEAN currencies cannot afford to meaningfully strengthen versus the RMB as they are part of various supply chains that terminate in China. Higher product prices mean that they could possibly lose their place in the chain. As such, Asian currencies should track the RMB to some extent. In any case, it determines one important parameter in their value.

There are several forces at play that are likely to affect oil prices. On the supply side, there is the OPEC and Russia agreement to cuts in production. On the demand side, the expected increase in economic activity in US. Both sides have uncertainties around them. Attracted by rising prices US drillers are adding oil rigs, with total number in May being twice as big as one year ago. There are also some doubts about effectiveness of the OPEC agreement. All in all, although we expect some increase in the oil price, we don’t think it will be significant.

The remainder of likely changes in Asian currency values will depend on how well they deal with the potential outflows that are triggered by higher US yields. There are four main buffers to outflows: raising policy rates, increasing bond yields, weakening currencies, or using reserves.

The extent to which each shock absorber can be used depends on how much policy space exists around that variable. We still believe that, currently, raising policy rates is not an option for any ASEAN economies. Domestic demand is not strong and inflation, although it has edged up recently, is mainly cost push. The feasibility of using other 3 buffers differs between the economies so we will consider case by case for each county. But before that, a few words on Singapore.

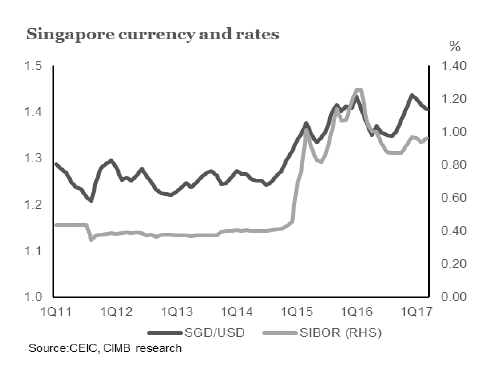

Improved export growth has supported the NEER (nominal effective exchange rate) this year. At the April meeting, MAS decided to keep policy unchanged. With policy in neutral mode, the SGD should move in tandem with its trading partners. Eventually, in the longer term, when the USD strengthens, the depreciation premium on the SGD is likely to increase, manifesting itself in higher rates. But so far, we expect SGD to stay around 1.40 to USD at the end of 2017.

As mentioned in the January Snapshot, the Malaysian ringgit depreciated at the end of last year because the other 3 variables – policy rates, bond yields, reserves – were constrained in how much they could adjust. With private domestic demand relatively weak, BNM could not raise rates. Similarly, with high household debt, especially in mortgages, households would be sensitive to rising long-term rates. And while reserves were just about adequate, they were relatively lower (by IMF adequacy standards) than those of other ASEAN countries.

Malaysia also had a relatively high foreign holding of government bonds which made it more vulnerable to outflows. However, the presence of foreign money in the bond market has decreased recently from around 35% to around 30%. Indeed, a big chunk of foreign capital left Malaysia because BNM effectively stopped foreign banks trading ringgit NDFs, offshore contracts used to hedge exposure to the currency. As the Malaysian onshore market was not liquid enough to hedge currency exposure, some investors divested their holdings of Malaysian bonds for they couldn’t hedge the currency risk. BNM has already put some measures to allow foreign investors to deepen the market, hoping to revive the interest in debt. This is likely to lead to a continued strengthening of the ringgit in the near term.

With the growth outlook improving and increasing inflows from trade and to Malaysian equities, we expect any depreciation of the MYR to occur closer to the end of year, largely keeping pace with RMB movements. We expect USD/MYR at 4.45 at the end of 2017.

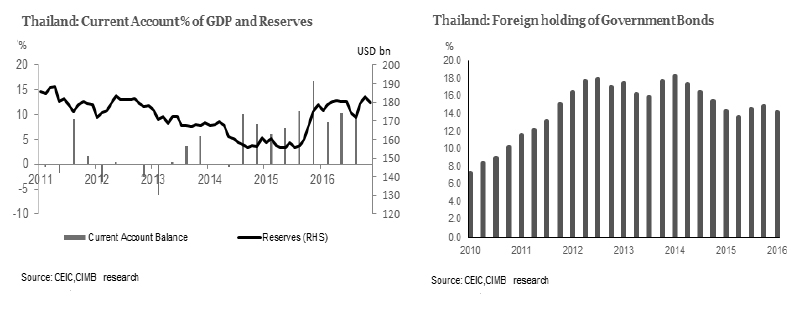

Thailand has consistently had a large current account surplus for the last 2 years. This persistent surplus has meant that means that Thailand has built up a robust position in foreign reserves, which might act as a buffer in case of outflows pressures. Moreover, foreign holdings of government bonds is relatively low (~15%), which makes Thailand less susceptible to outflows.

The currency is unlikely to be under much pressure and any movements will largely come from policy decisions to keep exports competitive within the supply chain. In April, the Bank of Thailand cut its weekly issuance of 3 and 6 month bills to curb excess capital inflows and currency speculation.

In the last 4 months, THB has appreciated against USD and was one of the best performing Asian currencies. The Thai Baht is benefiting from political stability, a pick-up in exports and an improving growth outlook. This has attracted equity inflows, and more recently bond inflows from investors likely wanting to benefit from a steepening yield curve. We expect only slight deprecation of THB to 35 against USD at the end of 2017.

Indonesia has enough buffers to counter capital outflows. Although foreign holdings of government bond is relatively high (39% in April), the level of public debt to GDP (27.9%) is relatively low3. Moreover, given that household debt to GDP (16.7%) is also much lower than in Thailand or Malaysia, there is space to increase bond yields, which are already quite attractive. FX reserves have increased since the beginning of the year, from around 110 billion USD in December 2016 to around 117 billion USD in April 2017. As investment growth was drag on GDP growth for the last 3 year, one of the current aims of economic policy is to boost investments. A stronger Rupiah helps to achieve this goal4.

Indonesia has enjoyed a trade surplus of USD7.7 billion and USD8.8 in 2015 and 2016, respectively. Although Indonesia has a current account deficit, it has been narrowing. In 2015, it was 2 % of GDP while in 2016 the number was 1.8%. We expect the current account deficit to continue to narrow on improving exports.

At the end of 2017, we expect the rupiah to be at around 13,300 to USD, supported by an improving current account balance, stable GDP growth, lower inflation (through increasing real rates), sound fiscal management, and expected ratings upgrade. These factors would likely generate capital inflows, especially in the bond market, and provide a counter balance to any outflow triggered by rising US rates.

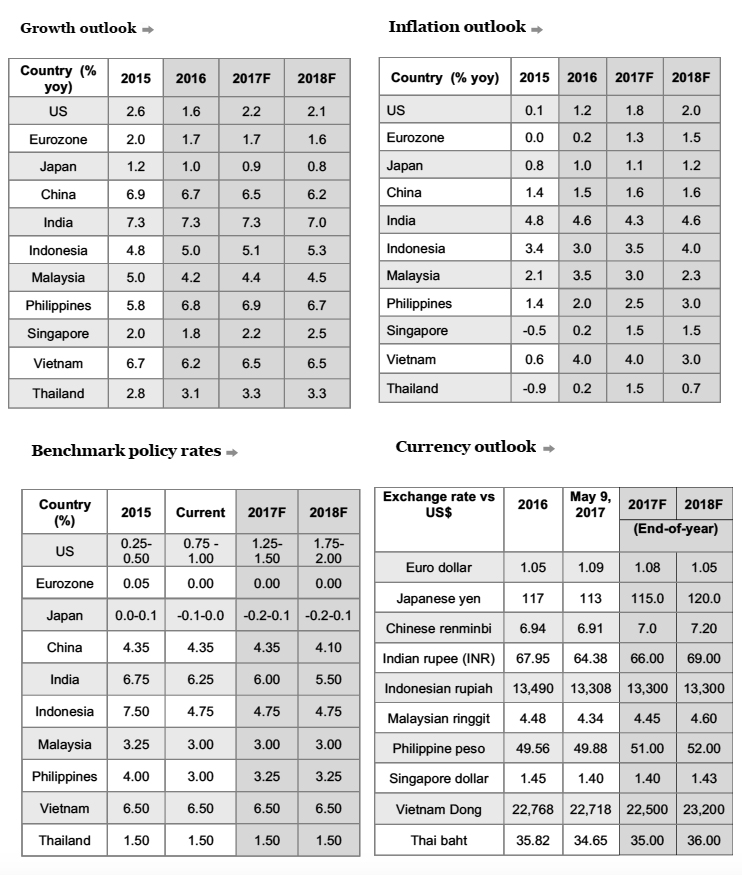

Our forecasts are below.

Global & Regional Forecasts

1 “Economic Snapshot: ASEAN Focus”, January 11, 2017, CIMB

2 “Economic Snapshot: ASEAN Focus”, January 11, 2017, CIMB

3 Thailand 41.2 % and Malaysia 53.2%

4 For example, through lower prices of imports

Disclaimer: All rights reserved. No part of this report may be reprinted or reproduced or utilised in any form or by any electronic, mechanical or other means, now known or hereafter invented, including photocopying or recording, or in any information storage or retrieval system without proper acknowledgement of CIMB ASEAN Research Institute. The views, responsibility for facts and opinions in this publication rests exclusively with the authors and their interpretations do not necessarily reflect the views of CIMB ASEAN Research Institute.

![]()