Economic Snapshot: ASEAN Focus May 2017 | Lao PDR

Published on 24 May 2017

by Debapriya Mukherjee, CFA, Economist, CIMB ASEAN Research Institute

The landlocked economy Lao PDR (Laos) has seen rapid growth in recent years, primarily driven by capital intensive investments in the power sector. Growth remains strong, although it has slowed in 2016, facing headwinds from a subdued growth rate of major trading partners, low global metals prices and a slowdown in agriculture. Inflation has risen but remains contained. Going forward, expect growth to be a tad higher at 6.9%, and moderate inflation. A healthy pipeline of projects in the power sector will keep investments strong and increase electricity production as well as exports. Risks to the domestic economy include a possible reversal of fiscal consolidation, high public debt and weak public banks. On the external front, Laos remains vulnerable to a tightly managed and overvalued exchange rate, low reserves and dollarization.

Growth is slowing but remains elevated; the government balance sheet remains a concern

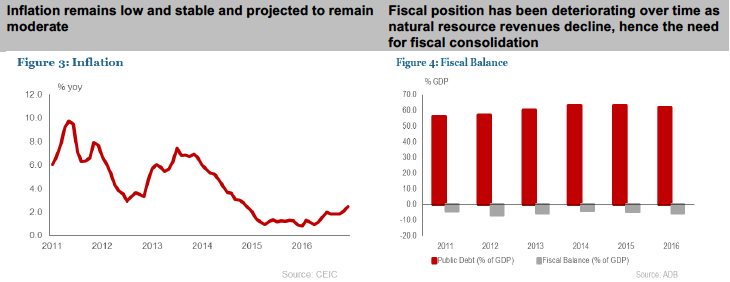

- Economic growth remains strong in Laos, although it has slowed from 7.5% in 2015 to 6.8% in 2016, the result of a slowdown in global trade, lower commodity prices and unfavourable weather conditions which affected agriculture.

- Growth is expected to expand by 6.9% in 2017. The economy should benefit from recovery in commodity prices, primarily mining products. Construction will profit from momentum in the hydroelectric sector with several projects launched at the end of 2016. Output in agriculture is expected to recover following last year’s drought, and output in manufacturing will continue to expand, albeit from a low base.

- Household consumption looks set to remain firm and will benefit from the rise in minimum wage, although it could be hit by fiscal consolidation measures.

- The fiscal position remains challenging. Low commodity prices (affecting royalties and taxes on mining) have negatively affected fiscal revenues and widened the deficit. Despite a growing deficit, the magnitude of spending cuts were not commensurate to the shortfall in revenue.

- The Government’s effort in strengthening non-resource taxation, reviewing exemptions and improving public finance management is expected to help improve the fiscal outlook in the medium term.

Inflation remains anchored

- Food prices rose in 2016 owing to unfavourable weather. On a whole, headline inflation has been low and remains contained.

- With a recent edging up of global commodity prices, inflation if expected to rise from 2% in 2016 to 2.3% in 2017.

Current account deficit remains sizeable

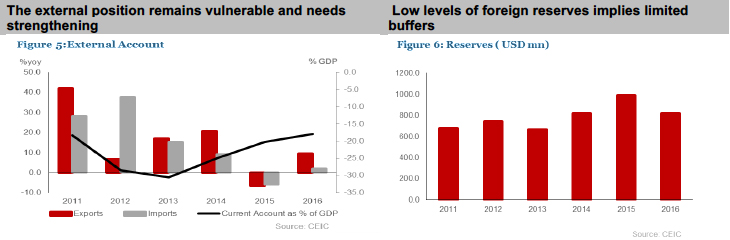

- Exports have rebounded in 2016 as power exports (80% of the electricity produced in Laos is exported) continue to expand, offsetting the loss in revenue from depressed prices of copper and coal. At the same time, a pronounced increase in imports of capital goods was observed in 2016, owing to rising hydropower investment projects as well as railway projects commissioned in recent years.

- The current account deficit remained high at 18% of GDP in 2016 but has narrowed down from 20% of GDP in 2014.

- Exports should benefit from electricity development projects and the recovery of economic activity in Thailand (the country’s main trading partner) in 2017. The trade deficit will widen in 2017 as import of capital goods pick up further.

Monetary Policy to target exchange rate stability

- Given the weak institutional capacity, underdeveloped financial system and the level of dollarization in Laos, standard monetary policy tools are ineffective. The central bank (BOL) therefore targets exchange rate stability of the local currency (the kip) against the US dollar as the primary means to control inflation1. Stability of the kip is also important for domestic confidence in the currency.

- Credit growth recovered to around 25% in 2016, mostly in foreign currency lending, which has raised worries about re-dollarization.

- Foreign reserves increased in 2016, but remain a thin buffer at around 1.9 months of imports, which is low by partner country standards. This constrains BOL’s room to manoeuvre in response to external pressures. It is therefore imperative that Laos builds up its reserves to provide a buffer against shocks and for macroeconomic stability.

- The real effective exchange rate has appreciated (estimated at between 20% and 40%2). The continued real appreciation, in addition to the supply side constraints, reduces the competitiveness of exports.

Risks and other issues

- The economic growth of Laos is heavily reliant on natural resources. Hence there is a need for diversification to reach a more inclusive and sustained growth, particularly to achieve its goal of graduating from Least Developed Country (LDC) status by the 2020s.

- The country remains vulnerable to external shocks owing to twin deficits on fiscal and current accounts. The fiscal pressure and limited reserves buffer undermines the ability to mitigate adverse shocks. A failure to consolidate the fiscal position and bring down public debt could undermine confidence in the government’s macro policy framework, raise public debt further and worsen the country’s external position.

1 The BOL targets exchange rate stability through a peg that keeps the value of the kip within a narrow trading band against the dollar, with a fluctuation permitted of plus or minus 5%

2 As per IMF Staff calculations, which could be attributed to the nominal appreciation of the kip with respect to major partner country currencies (renminbi and baht)

Disclaimer: All rights reserved. No part of this report may be reprinted or reproduced or utilised in any form or by any electronic, mechanical or other means, now known or hereafter invented, including photocopying or recording, or in any information storage or retrieval system without proper acknowledgement of CIMB ASEAN Research Institute. The views, responsibility for facts and opinions in this publication rests exclusively with the authors and their interpretations do not necessarily reflect the views of CIMB ASEAN Research Institute.

![]()