Economic Snapshot: ASEAN Focus May 2017 | Vietnam

Published on 24 May 2017

by Debapriya Mukherjee, CFA, Economist, CIMB ASEAN Research Institute

Vietnam’s economy grew 6.2% yoy in 2016, versus 6.7% in 2015, weighed down by a slowdown in the agriculture and mining sectors. There was a further moderation to 5.1% growth in 1Q17. Nonetheless, on the back of strong FDI and the fading of some temporary headwinds, growth is expected to rebound and average 6.2% for 2017. Vietnam has been a recipient of strong and steady FDI inflows over the last few years and the trend should continue in 2017. Manufacturing and services sectors remain the green shoots. Inflation is expected to be within target. On the fiscal front, consolidation remains a high priority and achieving it requires tax reforms as well as better revenue administration. External debt remains vulnerable to real depreciation and current account shocks. Overall, expect a favourable medium-term outlook for Vietnam.

Growth weighed down by transitory factors

- Despite a drought hit agriculture and slowdown in mining, economic growth in Vietnam averaged 6.2% in 2016. Manufacturing and services sector provided a fillip to the growth story.

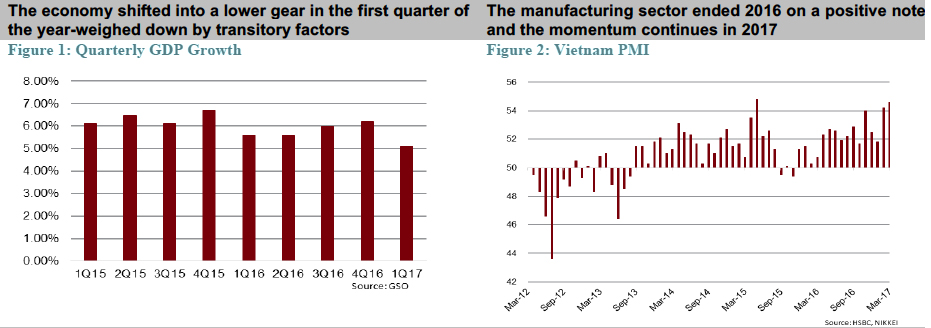

- GDP growth decelerated from 5.5% in 1Q16 (and 6.1% in 1Q15) to 5.1% in 1Q17. Oil production fell 14% yoy, as low oil prices prompted the government to cut back production. The decline led to a 10% fall in Vietnam’s mining production, which accounts for 10% of GDP.

- Consumption fell from 7.5% yoy in 1Q16 to 6.2% in 1Q17, which is a bit worrying given that consumption constitutes 65% of GDP. As Vietnam continues to have one of the highest consumer confidence rankings in the world, therefore, the decline in the rate of consumption growth could be attributed to seasonal effects, as the Vietnamese Tet New Year Holiday was particularly early this year.

- Construction activity slowed from 9% in 1Q16 to 6% in 1Q17, due to the fact that industrial construction (factories, and other production facilities) was flat. Residential construction grew at a robust 10% yoy, indicating that confidence among home buyers is still high.

- Manufacturing output grew 8% in both 1Q16 and in 1Q17, despite the slowdown in Samsung’s production. This reflects the strength of the manufacturing story in Vietnam, which is also reflected by an increase in Vietnam’s PMI survey from 54.2 in February to a 22-month high of 54.6 in March.

- In 2017, economic activity will average 6.2%. Manufacturing and services remain buoyant. Production in agriculture has also rebounded, though at a moderate pace.

The FDI-driven export growth story continues to power ahead despite the US withdrawal from TPP

- The value of newly registered, planned FDI projects soared 92% yoy in 1Q17 to US$7.7 bn, but those newly planned projects included Samsung’s planned US$ 2.5 bn display factory. Excluding that, newly registered FDI projects still grew by an impressive 30% yoy. These figures could indicate that firms began to hold back on actually following through on their prior FDI commitments immediately after Mr Trump was elected and he withdrew the US from the TPP, but then as a more benign picture emerged, company executives felt free to resuming committing to new projects.

- Vietnam’s exports grew 13% yoy in 1Q17, which was an acceleration from the country’s 9% export growth in 2016, enabled by robust FDI inflows.

- High tech exports grew 6% yoy because of the retooling of the Samsung smartphone production line (in 2016, high tech items contributed nearly 1/3 of Vietnam’s overall exports).

- Vietnam ran a US$ 1.9 bn trade deficit in 1Q17 because import growth surged from 5% yoy in 2016 to 22% in 1Q17. At first glance, the statistic may seem alarming, but the vast majority of Vietnam’s imports are used as intermediate inputs for exports (about 70% of Vietnam’s imports are attributable to FDI companies). Furthermore, imports of machinery and equipment surged 28% yoy in 1Q17, which is a strong, positive leading indicator that manufacturing growth will remain robust this year.

- The current account surplus will narrow as FDI inflows draw in imports of capital goods and manufacturing inputs. Consumer goods imports have also been rising, primarily automobiles.

Inflation remains stable

- Inflation in Vietnam is currently being driven by administrative price hikes especially for health and education services.

- Headline CPI inflation increased 5% in 1Q17 yoy, partly on account of higher energy and food prices – core inflation grew 1.7% yoy during the same period. The recent easing of global food and fuel prices and a strong dollar may result in imported inflation.

- On the whole, expect inflation to average 4% in 2017.

Expect a gradual pace of fiscal consolidation

- Fiscal policy has been relatively loose in recent years; the fiscal deficit was at a high of close to 6.6% in 2016. The single most important reason is the rapid increase in recurrent expenditures. The government seeks to increase its revenue from domestic taxes and fees and sell its stakes in equitized companies.

- The government remains committed to fiscal consolidation as concerns grow about the likely negative impact on investor confidence if Vietnam’s debt-to-GDP ratios surpass the safety limits set by the authorities. However given its ambitious infrastructure development plans, growing welfare costs and revenue shortfall resulting from phased cuts to import duties, the pace of fiscal consolidation will be gradual.

- Monetary policy can stay loose as long as inflation is within target.

- Exchange rate will depreciate in line with other regional currencies.

Risks and Other Issues

- Domestically, delayed implementation of structural and fiscal reforms (to rein in public debt) as well as vulnerability in the financial sector (slow NPL resolution progress) are the primary risks to the economy.

- On the external front, risks of protectionist measures undermine Vietnam’s trade position.

Disclaimer: All rights reserved. No part of this report may be reprinted or reproduced or utilised in any form or by any electronic, mechanical or other means, now known or hereafter invented, including photocopying or recording, or in any information storage or retrieval system without proper acknowledgement of CIMB ASEAN Research Institute. The views, responsibility for facts and opinions in this publication rests exclusively with the authors and their interpretations do not necessarily reflect the views of CIMB ASEAN Research Institute.

![]()