Economic Snapshot: ASEAN Focus Jan 2017 | Indonesia

Published on 25 January 2017

by Adrian Panggabean, Chief Economist, CIMB Niaga

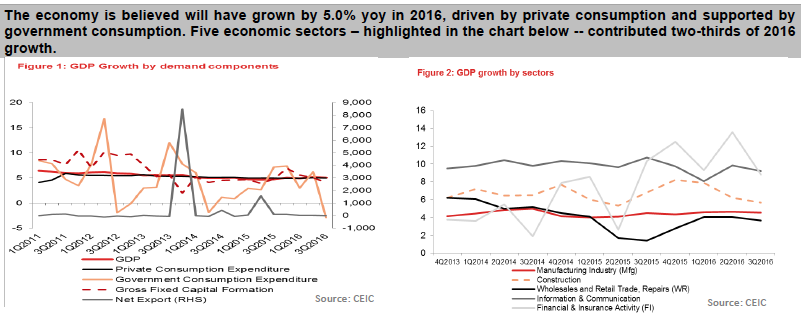

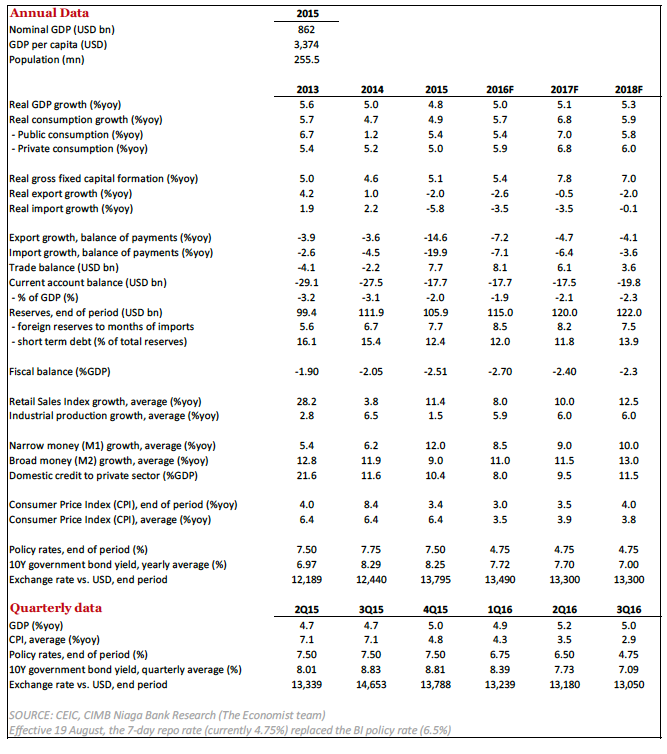

Indonesia, affected by external headwinds, has seen its pace of economic activity stabilize around 5% growth since 2014. By the end of 2016, the Indonesian economy will have grown by another 5%, driven by private consumption and supported by public consumption. Core inflation has trended down. October saw the lowest core inflation rate since 2000. Given the relative stability of the IDR, the monetary authority, Bank Indonesia (BI), cut rates 6 times in 2016, and the policy rate, the 7-days reverse repo rate, now stands at 4.75%. I believe the rupiah is still undervalued against the USD, and on the back of budgetary realignment and a pickup in growth momentum, I expect the IDR to gradually appreciate in 2H2017. The economy should grow by 5.1% in 2017 and the year-average inflation is seen at 3.9% yoy.

Private consumption – the main driver of Indonesia’s growth

- In the first nine months of 2016 the economy had grown 5.04% yoy, driven by household consumption and supported by government expenditure that grew by 2% yoy. Household consumption, explaining more than half of this growth, remained as Indonesia’s growth engine, thanks largely to a sizeable middle class population. The savings rate of the average Indonesian is slightly above 30%, and that has cushioned household spending during periods of economic weakness. The 2% yoy growth in government spending took place despite two rounds of budget cuts in the past 6 months, on the back of weak revenue collection.

- Gross fixed capital formation went up by 4.9% yoy in the first nine months of 2016, against 5.3% yoy in 1H2016. Private investment slowed as credit growth slid to 6.4% yoy in September 2016 from 9.6% yoy in January 2016. Global trade, soft through 2016, was reflected in export growth, which fell by 4.0% yoy in 9M2016.

- The economy is likely to have grown by 5.0% yoy in 2016; I expect a similar pace of 5.1% in 2017.

Trade surplus in 9M2016 on the back of slower global demand

- Amidst slower global and domestic demand, Indonesia’s trade balance registered a USD2.1bn surplus in 3Q2016, a modest increase from the 2Q2016 figure of USD1.9bn. This brought Indonesia’s trade surplus to USD5.7bn in the first nine months of 2016, against USD7.2bn surplus recorded during the same period in 2015.

- Given the current trend, I expect the trade balance to remain in surplus – about $7 billion — at the end of 2016, alongside the upward momentum in the economy. While export revenues are likely to increase due to firmer commodity prices, a rise in import growth due to improvement in household consumption is likely to offset some of that gain in the trade balance.

- Foreign exchange reserves rose over most of 2016 to US$115.7bn in September. However, the two rounds of global uncertainty – first due to firmer UK growth numbers in October and then the US election results in November – and consequently higher yields abroad led to a decline in reserves in those months. Inflows picked up again in December and reserves ended the year at over US$116 billion. As the analysis (in the article “Currency Outlook” shows, reserves in Indonesia are more than adequate to cover the various risk metrics devised by the IMF. As such it lowers the pressure on policy rates to deal with external shocks.

Room for monetary policy accommodation is still available

- In September 2016 headline inflation accelerated to 3.1% yoy or 0.2% mom, which brought ytd average inflation to 3.6% in the first nine months of 2016. Core inflation continued to head south, registering its lowest yoy growth in the past 15 years. Combined with the facts that: (i) manufacturing capacity is currently 30-35% below its potential, implying very little inflationary pressure in the pipeline and; (ii) interest rate differentials between Indonesia and its peers still provide space, albeit tight, for further monetary authority accommodation in the next 6 months. Our base case, however, does not have a cut factored in as external uncertainty, and consequently currency volatility, may not allow it.

Expectations are for a stable IDR

- In 2017, I expect the rupiah to average at IDR13,40 per USD with an year end value of 13,300. This relatively strong trend of the IDR is driven by productivity improvement, GDP growth, and capital inflows.

- Portfolio flows into Indonesia are expected to remain strong in 2017. A resilient economy with improving growth prospects and continued reforms make Indonesia’s (already high) yield even more attractive. Further, firmer commodity prices provide another link between portfolio inflows, the prospect of realization of FDI, and the rupiah.

Risks and Other Issues

- The spike in yields that followed Mr. Trump’s victory in US election exemplified the kind of external risks that still shadow the Indonesian economy. Mr. Trump’s foreign policy posture, his economic agenda, and the new administration’s appetite for globalization, will shape Indonesia’s external risk profile going forward.

- Other risks would include: (i) China, continuing its economic reform agenda resulting in slower growth. Plus, China’s high debt could affect regional risk premia; (ii) Brexit vs the Eurozone will have some impact on Indonesia via trade and exchange rate channels.

- The tax amnesty program has given significant boost to tax revenue with total redemption fee of IDR95 trillion up to end-November 2016. Redemption fees were derived from the declared and repatriated assets, which as of end-November 2016 amounted to around IDR3,950 trillion. To put these figures into perspectives, the total declared and repatriated assets are around 30% of Indonesia’s estimated 2016 GDP. The total redemption fees are 0.8% of 2016 GDP, 2.8% of 2016 budget or 35% of 2016 fiscal deficit. By any standards Indonesia’s achievement in its tax amnesty program is impressive. Participation rate of tax amnesty, however, is still low, with only 2% of total taxpayers participated in the program so far. In general, I believe tax amnesty bodes well for the improvement in tax administration. In the medium term, we believe serious reform in the areas of tax registration, collection, and enforcement are keys to bring about significantly higher tax to GDP ratio.

![]()