Economic Snapshot: ASEAN Focus Jan 2017 | Singapore

Published date 31 January 2017

by Arup Raha & Song Sen Wun

Advance estimates of 4Q16 GDP growth signal an economy that may be recovering. We partially agree; yes, there is recovery but the pace implied by the 1.8% yoy and 9.1% qoq clip in 4Q16 may have been misleading. The headwinds for the Singapore economy remain in place for now as growth in Singapore’s major trading partners continue to stay below average. Barring the unexpected 4Q advance estimate, based on October and November data, the economy only managed to expand an estimated 1.5% yoy in the first nine months of 2016 vs. 2.1% for the same period in 2015. Not much upside on growth can be expected until the global economy recovers. The Monetary Authority of Singapore (MAS) has a similar take, expecting growth between 1-2% in 2017. In October 2016, MAS maintained its neutral stance on monetary policy, citing the uncertain external environment We expect this stance to persist for some time. Given this stance, and our view that the Fed will likely raise rates 2-3 times in 2017, the USD/SGD pair should weaken to about 1.48 by the end of 2017 and the 3m SIBOR should be around 1.25%.

No respite from sluggish global demand

- Preliminary data indicates a tale of two very different quarters in 2H16. The economy contracted by a seasonally-adjusted 1.9% quarter-on-quarter annualized basis, in 3Q but bounced back with 9.1% growth in 4Q. Year-on-year, 3Q16 GDP slowed to 1.2% from 1H16’s 2.1% pace, on weaker manufacturing and services. Both of them had strong rebounds in 4Q16 with services growing 9.4% qoq and manufacturing growing 14.6%. While the 4Q numbers are definitely an improvement, base effects and a bounce in some of the volatile areas of the economy have exaggerated the magnitude.

- Given Singapore’s small and open economy, global growth has a more-than-proportional impact. For the third time this year, the IMF has lowered its forecast of global trade volume since its first forecast in January (in its April, July and October World Economic Outlook), by a total of 1.1-pt to 2.3% for 2016 and by 0.3-pt for 2017 to 3.8% (2.6% growth in 2015).

- The services producing industries account for 66% of the economy and the sector was estimated to have grown 9.4% qoq in Q4 after contracting for 3 straight quarters. It is estimated to have grown by 0.9% in 2016. Year-on-year, the services sector 0.6% in Q4 and 0.9% for 2016. For the year, at least until the Q4 bounce, according to MITI, growth was “weighted down primarily by the wholesale and retail trade sector while other services such as accommodation, information & communications as well as education, health & social services remained resilient”.

- The hospitality sector saw double-digit gains in tourist arrivals over the first half of the year, (+13% yoy), especially from China, India and a handful of neighbouring ASEAN countries. However, this did not translate into significantly higher overall spending because of cutbacks in spending from businesses and MICE markets due to the subdued business sentiment. In the first half of 2016, tourism receipts grew by 12% yoy to reach S$11.6bn. In the second half of the year, the pace of international arrivals softened was actually modestly negative yoy in October.

- Various business surveys suggested a mixed outlook for the economy. The purchasing managers’ index (PMI) published by the Singapore Institute of Purchasing & Material Management pointed to a more stable environment for manufacturing in September (50.1) and October (50.0) after fourteen consecutive months of contraction. It improved further to 50.2 in November and then 50.5 in December. However, the composite Nikkei Singapore PMI stood at 50.5 in October, down from the 19-month high of 52.9 in September. Although the headline composite index signaled a further improvement in business conditions, it was the slowest upturn in conditions for five months. Assuming improved economic conditions in the US, a stable Europe and stabilising China, we are projecting GDP growth of 2-2.5% for 2017 and 2018.

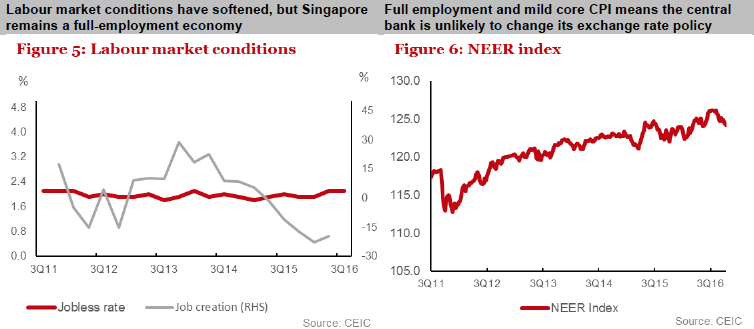

Labour market conditions weakens in Q3

- On the surface, despite the uneven performance of the economy, its seems that Singapore’s domestic economic conditions remain relatively resilient, if the overall jobless rate is any guide. Singapore’s seasonally adjusted jobless rate stood at 2.1% in Q3 2016, the same figure as in the previous quarter, preliminary estimates showed. However, total employment is estimated to have contracted by 3,300 in Q3, following slower growth in the previous two quarters. It was the second contraction since 2008/2009 recession and the weakest quarterly result since the March quarter 2015.

Neutral monetary policy stance and weaker currency

- After surprising the markets in April by setting a zero rate of appreciation for the Singapore dollar’s nominal effective exchange rate, the Monetary Authority of Singapore (MAS) has maintained that policy stance. For the foreseeable future, we think that the MAS will keep the current stance unchanged given that the GDP growth and core inflation outcome are within their forecast range and the external environment remains difficult. Core inflation, which excludes accommodation and private road transportation, was 0.9% in September. MAS expects it to average around 1% in 2016 before rising to 1–2% in 2017.

- Given a neutral policy stance and the expectation that regional currencies will weaken versus the USD, the SGD should follow suit. We expect the USD/SGD pair to weaken to 1.48 by the end of 2017. The 3m SIBOR is forecasted to reach 1.25% by the end of 2017 on the back of 2-3 interest rate increases by the Fed.

Risk and other Issues

- The largest risk though is uncertain nature of global economy growth that is likely to a profound impact on Singapore’s economy.

- On a positive note, global trade appears to be stabilizing, as are oil prices. Singapore benefits from both. Moreover, the Indonesian economy and, to some extent the Malaysian economy are also recovering and boosts Singapore’s role as a regional hub for transport, entrepot trade etc. Over the medium term it is doing well to position itself as hub for Fintech.

- Nonetheless, there are clear downside risks to 2017 growth forecasts given the uneven global growth amidst persistent geo-political risks.

![]()