LIFTING-THE-BARRIERS REPORT 2013 | CAPITAL MARKETS

Published date: November 2013

TABLE OF CONTENT

(Click any topic to read the related section)

- Introduction

- Current Status

- Next Steps

- Opportunity for Growth

- Key Considerations

- Network ASEAN Forum: Post-roundtable Considerations on Capital Markets

- Clarify the benefits

- Increase transparency

- Fix the easy things first

Introduction

Capital markets are a critical driver of economic growth, channelling private savings toward promising public and private investment opportunities. The nations of ASEAN individually recognise the value of a well-functioning domestic capital market, and have worked to facilitate its development through supportive regulatory and economic policy. Capital markets across member nations have grown rapidly as a result.

Opportunity for further growth remains; ASEAN policymakers have recognised the benefits that can arise from linking smaller domestic capital markets into a broader regional community. Such a regional market is better able to link lower-cost financing opportunities to higher-returning investment needs, increasing efficiency of financial intermediation and benefiting economic growth in the underlying economies.

Under the ASEAN Economic Community (AEC), the ASEAN Capital Markets Forum (ACMF) unites regional policymakers, market participants, and stakeholders to develop a roadmap for greater coordination across ASEAN capital markets. The roadmap seeks to align national efforts towards common goals, towards clear targets in 2015 and 2020.

This process is challenging; integration will require significant adjustment to domestic currency, capital account and taxation polices across individual ASEAN markets. Further, integration will subject both local issuers and financial intermediaries to different (and more competitive) market standards. Across member economies, there will be clear “losers,” while the benefits may be longer-term and diversified across multiple participants. Successful execution will require clear communication, consistent political support, and well-designed and transparent policy initiatives to support and prepare domestic industry for integration.

To support this process, we believe ASEAN policymakers and market participants must address two key topics as soon as possible. First, an integrated ASEAN capital market will require a stable domestic investor base, including institutional and retail investors; coordination in efforts to promote this will be valuable. Secondly, market participants must support policymakers in clearly and transparently identifying the most pressing barriers to beneficial harmonisation, as well as resultant costs. Recommendations stemming from addressing these two issues can supplement and support execution of the current roadmap.

Current status

The “ASEAN Capital Market” is comprised of ten distinct domestic markets across the Member States. Each of these markets is defined by separate currencies, separate, sovereign legal and supervisory regimes, and differing levels of maturity in development (Figure 1).

Broadly, the individual markets fall into four “tiers” of development.

Financial Hub (Singapore):

With a freely convertible currency, favourable taxation regime, and established legal and financial infrastructure, Singapore is a capital markets hub within ASEAN as well as broader Asia. The domestic market features a wide range of products and participants, and the off-shore market has critical scale in participants, infrastructure and assets under management

Established domestic markets (Malaysia, Thailand):

The domestic markets of Malaysia and Thailand maintain a broad base of local issuers and investors, with domestic institutions achieving scale. Malaysia maintains regional leadership in Sharia-compliant products and a robust fixed income market; however both countries lack significant OTC derivative activity. Foreign investors have considerable access, however some restrictions remain through listed company ownership quotas (both) and capital controls (Thailand)

Emerging domestic markets (Indonesia, Philippines):

Indonesia and the Philippines share fast growth across listed equity and fixed income markets. However, concentrated domestic issuer and investor bases lead to lower levels of participation and capitalisation than the “established” ASEAN markets. Domestic institutional investors are newly emerging, and minimal capital controls create a positive environment for foreign investors. At this developmental stage, product demand remains concentrated in “basic” equity and bond products, with limited derivatives activity

Nascent markets (Brunei, Cambodia, Laos, Myanmar, and Vietnam):

The remaining markets of ASEAN feature capital markets at the early stages of development. Infrastructure regulatory frameworks are currently being established, and domestic investment institutions are of small scale. Brunei aside, capital controls limit the role of foreign investors in these markets

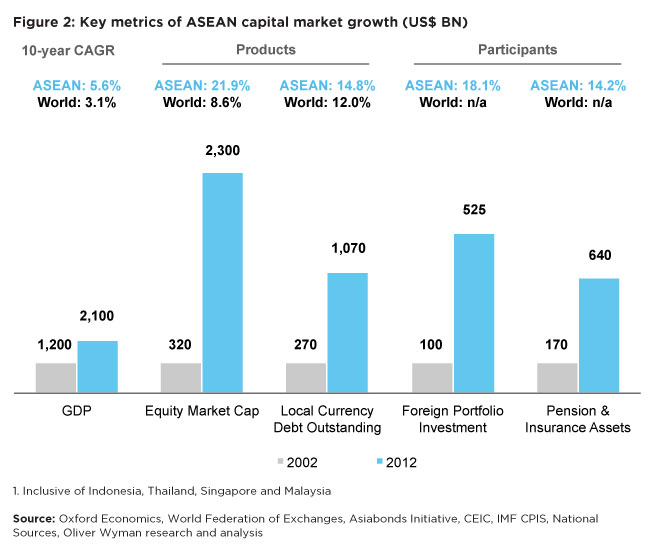

Collectively, ASEAN Capital Markets have experienced rapid growth over the past decade, across multiple critical dimensions (Figure 2).

- Equities: The combined market cap of ASEAN exchanges (as of end-2012) reached US$2.3 TN, creating the 5th largest equity pool in the Asia-Pacific region

- Fixed Income: Local currency fixed income markets have also expanded significantly in recent years, creating Asia-Pacific’s 4th largest market by issued amount outstanding, behind Japan, China and Korea

- OTC Derivatives: Excluding Singapore due to its role as a regional financial trading hub, ASEAN onshore OTC derivative markets are still at a nascent stage. However, daily traded volumes have increased over three-fold over the past decade across Indonesia, Malaysia, Philippines and Thailand – laying the base for future development

- Issuers: Expanding ASEAN capital markets have broadened the issuer base across local and foreign companies (particularly in Singapore). The number of listed companies across ASEAN increased 30% over the decade, supported by partial privatisation efforts in markets such as Indonesia and Malaysia. Further, fixed income issuance is supported by rising credit standards across ASEAN (particularly the upgrade of Indonesia and Philippine sovereign ratings to investment-grade)

- Intermediaries: While global banks have long been established in ASEAN markets, the emergence of true “pan-ASEAN” players based in the region is a relatively new development. In recent years, players such as CIMB, DBS Vickers, Hong Leong and Maybank/Kim Eng have emerged with explicit strategies to link regional capital markets, forming a “single point of access” for ASEAN investors and issuers

- Investors: ASEAN accounts for the third-largest collection of liquid deposits in the Asia-Pacific region (behind China and Japan), emerging as a major wealth “hub” in Asia-Pacific. This increase in wealth supports the emergence of regional institutional investors, including formalised insurance and pension sectors – particularly in the large markets of Indonesia, Malaysia and Thailand. Further, international portfolio investment increased by over ~525% in the past decade, across equities and local sovereign debt

- Integration: Across major ASEAN markets, national policymakers promote the growth of “champion” exchanges to boost the profile of local capital markets. As a result, trading and clearing institutions are consolidating domestically, including the mergers of the Jakarta and Surabaya Stock Exchanges (2007), Hanoi and Ho Chi Minh (2013), and Philippines equity and debt exchanges (2013)

- Operations: Major ASEAN exchanges in Malaysia, Singapore and Thailand recently invested in new trading and/or clearing systems. These systems now rank among the fastest in the world, facilitating the growth of high-speed trading, Direct Market Access and new clearing approaches to attract foreign institutional investment

- ASEAN Trading Link: Launched last year, the ASEAN Trading Link integrates equities markets across Malaysia, Singapore and Thailand to allow investors a single platform for trading ASEAN equities. Future plans entail expansion to exchanges in Indonesia, Philippines and Vietnam

- New infrastructure: A range of new market infrastructure players emerged in ASEAN over the past decade. As a financial hub, Singapore pioneered the region’s first OTC CCP (AsiaClear) and major dark pool initiative (Chi-East). While Chi-East ultimately failed, it remains a valuable test of the regional regulatory and trading environmentOn the other end, Cambodia and Laos saw national stock exchanges launched in 2011. Furthermore, securities law legislation currently underway in Brunei and Myanmar are to support the future launch of domestic exchanges within these markets

- Domestic sector promotion: Local regulators across ASEAN continue to support the development of local capital markets through regulatory initiatives. Indonesia, Malaysia, and Thailand issue periodic Capital Markets Master Plans (CMMP) to build consensus around policy and legal reforms against a fixed timeline, while Singapore has an explicit target of developing an international financial centre

- Institutional investor regulation: Indonesia, the Philippines and Thailand are enhancing national healthcare and pension schemes, creating sizable domestic asset management institutions with the potential to act as “cornerstone” investors in local markets. Furthermore, as domestic insurers across ASEAN slowly liberalise asset allocation guidelines we expect these institutions to play larger roles in domestic equity and corporate debt markets across the region

- Cross-border harmonisation: Under the guidelines of the ASEAN Capital Markets Forum, ASEAN markets are to work towards increased harmonisation of rules related to issuance, supervision and licensing of market professionals. To date, progress has been made on harmonisation of market professional qualifications and rules for expedited secondary listings; however, this remains limited in application to Malaysia, Thailand and Singapore

Next steps

Through domestic and collective regional efforts, ASEAN nations are already moving to address many of the key issues required to drive future capital markets growth. Domestic markets will need to continue current efforts to implement agreed Capital Markets Master Plans and promote domestic investment institutions. We also expect domestic policymakers to pursue broad cross-border capital markets development opportunities outside of ASEAN – for example, Malaysia’s common bond settlement platform with Hong Kong.

At a regional level, ASEAN member countries are working to implement the objectives of increased integration identified under the ASEAN Economic Community (AEC) framework for 2015

- Free flow of investment

- Freer flow of capital

- Free flow of talent

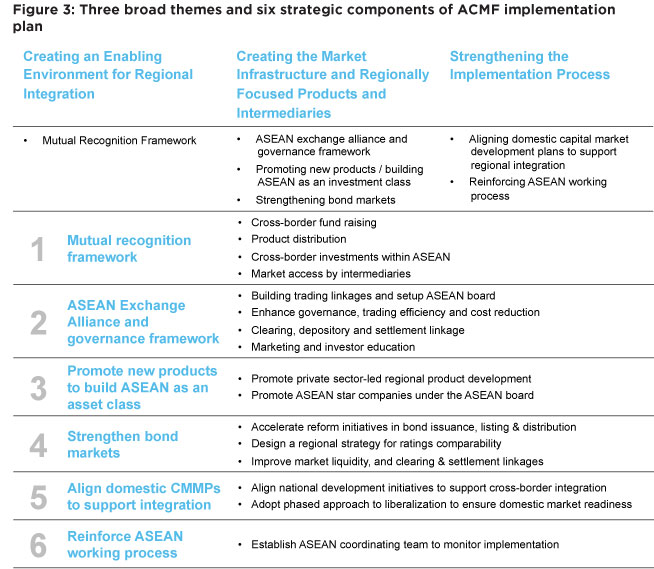

Key to this effort is the implementation roadmap outlined by the ASEAN Capital Markets Forum (ACMF), emphasising coordination on market access, linkages and liquidity. This roadmap is structured around three broad themes, and six strategic components (Figure 3).

The roadmap is comprehensive, and has seen several recent successes. The recently agreed frameworks on expedited review for secondary listings (March, 2012) and cross-border securities offering standards (April, 2013) significantly reduce the barriers for ASEAN listed companies to cross-list across Malaysia, Singapore and Thailand. Issuers need only complete one standardised prospectus, and can expect faster and transparent approval process for cross-listing. Thus, issuer companies may now access the combined investor base of all three markets, reducing potential funding costs and (indirectly) increasing cross-border participation of ASEAN institutional investors. Furthermore, this structure gives rise to potential product opportunities, such as ASEAN-focused ETFs targeted at retail investors, to increase participation.

However, this partial implementation of the roadmap creates its own challenges. While some process barriers have been reduced, cross-listed companies may still be subject to separate legal requirements and taxes, and may face challenges in repatriating raised capital. Discrepancies in pricing between the multiple listings will create arbitrage opportunities; however, local intermediaries will not be able to trade against these as they still face restrictions in operating across other ASEAN markets. Thus, these opportunities will be left to larger global and regional banks, with branch presence in each of Malaysia, Singapore and Thailand, to capture.

Similar challenges belie the recently launched ASEAN Trading Link; while trading is successfully underway, marketing efforts could be further coordinated to boost retail participation, and agreement on clearing and settlement interoperability is yet to be achieved. As such a structure may have disproportionate impact on individual market participants, quick agreements here may be difficult to achieve.

Clear and consistent resolution of these issues is critical; as the more “advanced” of the ASEAN members in capital markets, Malaysia, Singapore and Thailand present a test case to the rest of the region. Any negative impacts from partial or unbalanced implementation of the roadmap initiatives may increase the reluctance of other members to support this, or future efforts.

Opportunity for growth

- OTC market development:

ASEAN fixed income markets have progressed significantly, with outstanding bond volumes across Malaysia and Singapore already in line with developed Asian and Global bond markets (as a multiple of GDP). However, OTC market development remains limited, with limited trading of interest investors continue to grow, “organic” hedging demand for these products is expected – particularly in Indonesia and Malaysia, which feature rapidly regionalising corporates - Broadening investor base:

Retail participation in ASEAN markets lags Asia-Pacific peers; 9% of Singaporeans invest in domestic equities, compared to 35% of Hong Kong citizens and 17% of Australians. This disparity affects turnover activity and thus market liquidity; up to 60% of turnover on the KRX is driven by retail investors, compared to 20% on Bursa Malaysia. Lacking this balance, many ASEAN markets need also concentrate on building the domestic institutional investor class. Singapore and Malaysia aside, ASEAN institutional investors are limited in scale and conservatively invested as compared to broader regional peers. Lacking these developments, ASEAN capital markets will remain exposed to a degree of volatility from the ebb and flow of foreign investment - Enhancing liquidity:

Across high-level measures of capital market development such as equity market capitalisation as a multiple of GDP, the largest economies of ASEAN are in line with peer markets in Asia. However, ASEAN markets lag regional peers in measures of liquidity (Figure 4). Increasing retail participation will go some way towards addressing this issue; however a deeper analysis of domestic market policy is also necessary - Furthering integration:

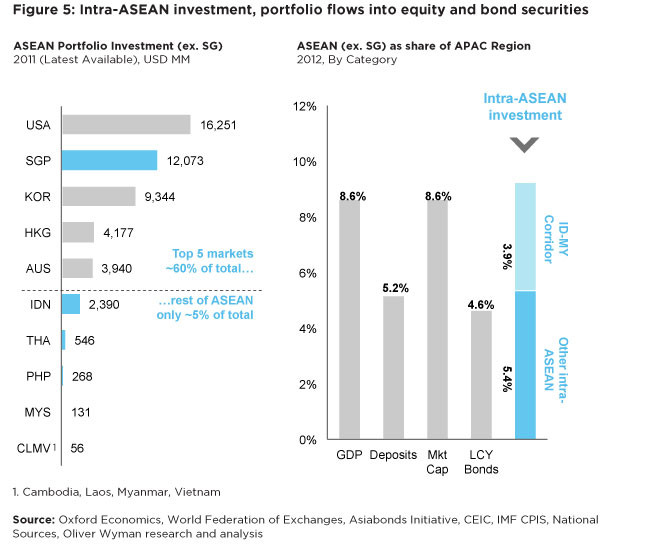

Despite increased efforts to promote ASEAN as an investment class, intra-ASEAN investment remains muted. Less than 5% of cross-border investment from ASEAN nations is in other ASEAN nations (excluding Singapore, given its role as an investment hub). Further, over 40% of intra-ASEAN cross-border investment is captured within the Indonesia-Malaysia corridor, which suggests the predominance of linguistic and cultural links over true integration. (Figure 5) To increase this figure, ASEAN policymakers will need to confront the “tough” questions on harmonisation of withholding taxes, exchange and clearing infrastructure, and broker consolidation. Further, investment in “soft” initiatives such as retail investor education to increase awareness of ASEAN companies as attractive investment options will be increasingly necessary

If these issues can be satisfactorily addressed, we believe the benefits to growth in regional capital markets can be substantial (Figure 6). Increased integration, wider product offerings and a larger investment base supports increased liquidity. Increasing ASEAN market liquidity to levels comparable with other developed Asia-Pacific markets could yield 25–30% uplift to overall ASEAN capital markets trading activity.

Key considerations

To realise this potential, we believe ASEAN policymakers and market participants need to converge on two overarching questions, outlining a unified vision for the regional capital market.

- How do we develop and enlarge a stable pan-ASEAN investor base?

- What work remains in order to achieve a more harmonised, integrated ASEAN capital market?

To each of these questions, stakeholders will need to consider several key questions.

#1: How do we develop and enlarge a stable ASEAN investor base?

- ASEAN nations have already pursued multiple initiatives to strengthen the regional investor base (e.g. the ASEAN Trading Link, cross-listings, mutual recognition)

- For what segments of the market (e.g. domestic vs. foreign, retail vs. institutional, specific markets) have these measures been most effective? Have they had any negative impacts?

- What technical/practical barriers exist to extending these initiatives further across ASEAN?

- What measures should ASEAN nations take individually to strengthen investor bases?

- Can we improve transparency/reporting to better pinpoint gaps?

- How can nations individually strengthen the role of domestic institutional investors?

- Should domestic institutions (e.g. SWFs, Pension Funds) play a role in stabilising markets?

- What 2nd-order impacts are created (e.g. more risk across insurance sector)

- What measures can ASEAN nations take collectively to strengthen investor bases?

- Benefit of post-trade linkage on intra-region trading/clearing activity?

- ASEAN investor “Passport” (e.g. UCITS-type implementation for ASEAN?)

- Should there be a regional “stability fund” to help manage short-term volatility across ASEAN markets? How would this operate?

#2: What work remains in order to achieve a more harmonised, integrated ASEAN capital market?

- How do we view the current progress along the AEC 2015 initiatives?

- How effective have policymakers been at clearly articulating challenges/conflicts?

- What steps have been taken to address concerns of national interest (particularly concerning obvious disparities in capital markets development between ASEAN nations)?

- Do we still believe the original AEC 2015 goals are realistically achievable?

- What would a “realistic” integrated ASEAN capital market look like, structurally?

- Where would capital likely flow from and to, initially? What infrastructure would mediate this?

- Which parties would benefit the most directly, and on what scale?

- What are the “red lines” which major nations are unlikely to cross? (e.g. full opening of capital account within ASEAN, open competition with domestic brokers)

- What practical steps can we take to reduce the current barriers in the next 18 months?

- Which barriers yield the greatest impact for the cost? What can the private sector lead, vs. the public sector?

- In case certain parties (e.g. sectors, nations) are expected to face disproportionate impact, can we coordinate to support them?

- What monitoring and enforcement mechanism do we need to see through these efforts?

Network ASEAN Forum: Post-roundtable Considerations on Capital Markets

On August 24, 2013, a select group of financial services and legal professionals active in ASEAN capital markets met to consider the next stages of capital market development in the region. This group consisted of representatives from both foreign and ASEAN member country-based investment firms and asset managers (the “buy-side”), securities firms and financial intermediaries (the “sell-side”), and securities exchanges, regulators, third-party advisors and legal service providers (“market infrastructure and support”).

Through lively discussion and debate, the assembled group of market practitioners yielded a broad consensus on the current development trajectory of capital markets in ASEAN

- Strong alignment with the view that increased coordination across the individual capital markets of ASEAN member countries is beneficial to the continued growth of the regional economy

- However, a clear concern with the rate of tangible progress towards further integration – particularly when compared to the objectives outlined in the roadmap developed by the ASEAN Capital Markets Forum and the end aspirations of the ASEAN Economic Community by 2015. Substantial technical barriers, such as complex and unaligned taxation regimes, remain not only unresolved, but lack transparency as to how they may eventually be resolved

- Recognising the political complexities in aligning multiple stakeholders across a broad range of issues, and the potential conflict with national interests, some market participants have raised concerns that the end goals of the roadmap may not be credible in the proposed timeframe

- Participants understand and accept that many of these barriers are indeed challenging, and will require the support of political figures in member country markets to resolve. However, there remain a few near-term “quick fixes” which remain unaddressed. Achieving progress in these matters could go a long way towards maintaining credibility and support for the integration process, while building momentum for further, more substantial, reforms

Given this context, we recommend that ASEAN policymakers consider three supporting actions to drive forward tangible progress on the Roadmap and move closer to achieving the original aims of the AEC 2015 initiatives.

- Clarify the benefits:

With the participation of market participants, policymakers must establish and publicise a clear, credible and quantitative evaluation of the potential economic benefits accruing to individual ASEAN member countries as a result of capital markets integration. Ideally, these benefits could be attributed to the level of key economic sectors (e.g. domestic small-to-medium sized enterprises). This evaluation can guide prioritisation of efforts, to areas where the upside is clearest and implementation most straightforward - Increase transparency:

Policymakers need to present an “honest” assessment of the challenges limiting further integration – including the political challenges arising from anticipated negative impacts on certain sectors (e.g. consolidation among sub-scale domestic brokers). These challenges are already implicitly recognised by many market participants; thus, failure to take this into full account in the current roadmap may risk impairing the credibility of the overall integration project - Fix the easy things first:

In the near-term, policymakers should also seek to reach rapid consensus on a few relative “quick fixes,” which if implemented can help to maintain support for reforms

Clarify the benefits

Integration of ASEAN capital markets is widely expected to yield broad benefits to member economies, including

- Increased attractiveness of the ASEAN region as a destination for investment – in turn reducing the cost of capital for locally based enterprises seeking to invest in growth

- Increased fluidity of capital within ASEAN borders, enabling both investors and enterprises equal access to opportunities across the region

While this is undoubtedly a benefit to the ASEAN economy as a whole, it is likely that individual market segments and industries will be differently advantaged through different aspects of integration. Care must be taken to understand in detail the various economic impacts of each aspect of capital market integration pursued, particularly as some reforms may be more challenging to implement.

With the cooperation of academic researchers and market participants, ASEAN policymakers will be able to develop a more tangible assessment of the benefits of capital markets integration across economic sectors. With this information openly available, relevant domestic and cross-border policies can be prioritised so as to focus regulatory efforts on those reforms where the benefit/challenge trade-off is the most optimal.

Increase transparency

As highlighted during the Roundtable discussions, as we move towards a more integrated ASEAN capital market a fair number of key considerations remain unaddressed. While many of these considerations are rooted in technical issues, it is well recognised that many also involve substantial political implications.

For example, in implementing the AEC 2015 objective of freer capital flows across the borders of ASEAN member countries, we must also consider how capital flows from non-ASEAN nations will be managed. In this regard, a fully “free” intra-ASEAN capital market would by definition adopt the regime of its most liberal member. Thus, ASEAN policymakers must account for the differences in approach between a small, financially-focused developed economy such as Singapore, and larger emerging economies at a different state of development (e.g. Indonesia, or Myanmar). Any potential approach must consider both technical considerations, (e.g. can we “tag” specific external flows to a specific market?), with political ones, (e.g. is it acceptable for Singapore to sit under a separate regime or timeframe from Myanmar?).

Market participants are sympathetic to these political realities, however simultaneously require a clear vision and expected deadlines in order to manage their own business plans. As a result, many market participants are forced to develop their own views regarding the political challenges to implementation of treated initiatives, and the resultant impact on roadmaps and timelines. The existence of multiple timelines – an “official” target, and “anticipated” timelines perceived by individual market participants, undermines credibility of broader initiatives. Further, it opens the possibility for an uneven playing field, as certain players may have greater access to inside information in guiding their strategies.

Therefore, it is essential that policymakers are increasingly transparent about such challenges – particularly as many are reasonably anticipated. Policymakers can take several clear actions to do so

- Openly address the political aspect of key considerations early in the roadmap process, and allow time for resolution in implementation

- Ensure clear ownership for resolution of certain political challenges, creating a clear point of contact for market participants

- Hold regular open forums with key industry stakeholders to discuss emerging challenges and implications for implementation progress

- Design clear enforcement mechanisms to ensure challenging issues are addressed, rather than delayed indefinitely – for example, fixed topic-specific senior-level forums, with a detailed mapping of all stakeholders involved

Fix the easy things first

Market participants are broadly sympathetic to the reality that many of the critical issues limiting further integration of ASEAN capital markets (e.g. differentiated tax regimes) are complex, involve political considerations, have disproportionate impact on different parties, and as a result are unlikely to be resolved quickly. Global analogies to large cross-border capital market integration efforts (e.g. the European Economic Community) speak to the need to avoid a “rushed” approach to deal-making and integration.

However, participants identified several select “friction points” which either build upon previous achievements to-date under the ACMF roadmap, or otherwise appear to be relatively uncontroversial. Resolution of these “quick fixes” would achieve several key benefits for the overall integration process

- Reinforce confidence that progress is continuing to be made

- Generate tangible benefits for market participants (against relatively low cost in effort)

- Maintain momentum among policymakers and market participants in driving further progress on more substantial, challenging issues

Several potential “quick fixes” for policymakers to consider are:

- Building on existing efforts to harmonise listing requirements, domestic regulators can further simplify the cross-listing process – easing process management, increasing document interchangeability and ultimately reducing cost to issuers:

- Permit English-language document submission across all ASEAN markets, allowing a single set of interchangeable documents to be used

- Converge on a uniform response time to submissions and requests, simplifying the process of managing multiple cross-listings simultaneously

- Simplifying tax collection for investors across multiple geographies through a single payment point

- Recognising that tax policy will not be harmonised in the near future, ASEAN markets can initially work towards assigning cross-border investors a unique “ASEAN” taxpayer ID, and create a single processing utility towards which all national billings are to be submitted, and all payments made (and further distributed)

- Increased coordination in investor education, as many retail investors across ASEAN remain less familiar with regional companies, member countries can coordinate with leading ASEAN brokers to host information sessions on the composition and merits of local indices, on a bilateral basis

![]()

RELATED REPORTS

- AN ANALYSIS OF THE ASEAN PRIORITIES ON IMPROVING GOOD GOVERNANCE

- LIFTING-THE-BARRIER REPORT 2013 FINANCIAL SERVICES

- LIFTING-THE-BARRIER REPORT 2014 FINANCIAL SERVICES AND CAPITAL MARKETS

- LIFTING-THE-BARRIER REPORT 2015 FINANCIAL SERVICES & CAPITAL MARKETS