Economic Snapshot: ASEAN Focus May 2017 | Indonesia

Published on 26 May 2017

by Adrian Panggabean, Chief Economist, CIMB Niaga

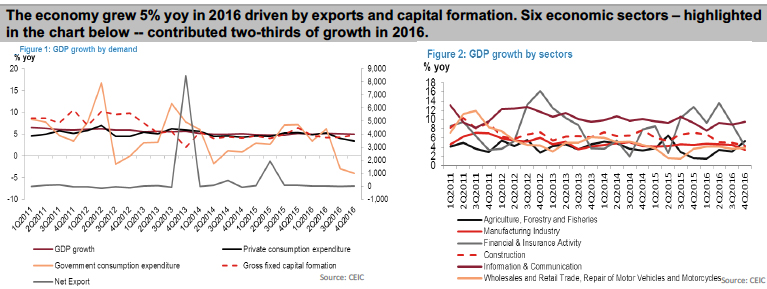

The Indonesian economy grew by 5% in 2016, mainly driven by gross fixed capital formation and the external sector. A similar growth rate was observed in 1Q17. I expect export growth to continue to be strong despite the possibility that Chinese demand may dampen in 2H17. Moreover, an improving terms-of-trade should help income growth and hence consumption demand. Inflation has ticked up to 4.2% in April 2017 after averaging at 3.5% in 2016, but do not believe that will prompt any tightening measures from the central bank. I believe the IDR is still undervalued against the USD and should appreciate on the back of budgetary realignment and an improving current account balance. The economy is forecast to grow by 5.1% yoy in 2017 and inflation expected to rise to 3.9% yoy. Barring any serious external upheaval, policy rates should remain unchanged.

GDP growth has been supported by trade

- In 2016, the economy grew by 5% yoy, with the main drivers being gross fixed capital formation and trade. The growth rate remained at 5% 1Q17. In April, exports grew by 12.6% yoy (USD terms), following a 24.3% increase in March. In volume terms, exports grew at 8% in Q1. Government expenditure showed signs of a pickup in 1Q17 as it grew 2.7% after declining in the preceding two quarters. In 2016, growth in private consumption was steady at 5%; opposing factors were at work with downward pressure from inflation and a boost from income growth. I expect a similar clip in 2017.

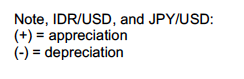

- Growth in the six sectors that make up around 65 – 70% of the economy was largely unchanged in 2016. The sectors are: (i) manufacturing; (ii) wholesale and retail trade; (iii) information and communications; (iv) construction; (v) finance and insurance; and (vi) agriculture. The mining sector showed positive growth in 2016, supported by increase in prices of commodities such as crude oil, palm oil, copper, and nickel. However, growth in the sector fell in 1Q17.

- Investment growth seems to be driven by capital formation, rather than by the change in stock (inventory). Gross fixed capital formation grew at 4.8% yoy in 1Q17, the same pace as in 4Q16. The government has boosted investment in infrastructure and introduced reforms to revive Indonesia’s appeal to private investors. The growing expenditure on capital is another indication that Indonesia’s economy may be in the initial phase of the upswing in a new business cycle.

- I expect GDP to grow by around 5.1% in 2017. While exports are unlikely to maintain their current pace, domestic demand may pick up the slack. The government is leveraging on its policy space to support domestic economic growth. there is a fair amount of policy support for the domestic economy. On the monetary side, the creation of liquidity in the banking sector via the provision of statutory reserves, the strengthening of monetary operations, and creation of the opening of greater provision of the segmentation of interbank liquidity, will help to repair the monetary transmission mechanism. On the fiscal side, there has been the broadening of tax base and the sharpening of the fiscal expenditure has been redirected to priority sectors such as infrastructure to support economic growth. No more spending cuts are expected this year as revenue collection was is on track to reach the government’s target.

Trade surplus should remain healthy

- In 2016, Indonesia had a trade surplus of USD8.8 billion. This trend continued into 1Q17 with a surplus of USD3.93 billion, the highest first-quarter surplus since 2012. In March 2017, in USD terms, exports grew 23.6% and imports were up 18.2% yoy.

- I now expect the trade balance to post a USD10 billion surplus in 2017. Exports should be supported by an improving terms-of-trade as commodity prices are firmer, but the current demand from China is unlikely to be sustained. Imports may rise at an even faster rate due to an improvement in household consumption. Hence the monthly trade surplus may decline in the remainder of 2017 but is likely to remain positive.

Further rate cuts on hold because of external factors

- Inflation averaged 3.53% in 2016, much lower than the 6.36% rate in 2015. This is the lowest average core inflation rate in the last fifteen years.

- However, inflation has started creeping up, averaging over 3.5% in 1Q17 and close to 4.2% in April. I expect headline inflation to average close to 4% in 2017. Most of the inflationary pressure is cost-push due to rising global commodity prices but I expect prices to taper off this year. An appreciating currency should also help keep inflation in check.

- As such, I do not expect Bank of Indonesia (BI) to make any moves on rates this year, even if the US Fed raises rates. The domestic economy is not ready for higher rates. Any adjustment to external developments is likely to be done via the currency.

- The money market rate may go down despite a steady policy rate after the introduction of variable rate tender for Bank Indonesia’s monetary operations. I believe that the 3-month IDR Jibor is likely to decrease to 6.25% at the end of 2017 from the current 6.80%.

Expectations are for a stable IDR

- In 1Q17, the exchange rate averaged at IDR13,352 per USD, slightly stronger than my forecast of IDR13,425, but much stronger than market consensus of IDR13,800. I expect a stronger IDR in 2Q17.

- I expect the IDR to be at 13,300 per USD at the end of 2017, supported by an improving current account balance, stable GDP growth, receding inflation outlook and sound fiscal management. This strengthening of the Rupiah is expected despite an expectation of two more rate hikes by the US Fed, coupled with a non-response from BI.

Risks and Other Issues

- Risks that should be anticipated are mainly global: a moderation of global growth, policy uncertainty in the US and geopolitics.

- S&P have recently upgraded Indonesia’s sovereign rating to BBB-, with a stable outlook, making it investment grade according to all 3 major ratings agencies. Being investment grade should attract significant funds especially in the bond market.

Disclaimer: All rights reserved. No part of this report may be reprinted or reproduced or utilised in any form or by any electronic, mechanical or other means, now known or hereafter invented, including photocopying or recording, or in any information storage or retrieval system without proper acknowledgement of CIMB ASEAN Research Institute. The views, responsibility for facts and opinions in this publication rests exclusively with the authors and their interpretations do not necessarily reflect the views of CIMB ASEAN Research Institute.

![]()