ASEAN Economic Progress: Vulnerabilities

Published on 15 October 2019

The previous section explored the supportive conditions that have driven regional economic growth. Accompanying such momentum are structural vulnerabilities which are explored in this section.

This part explores the first three out of five vulnerabilities that could curtail ASEAN’s future growth:

Regional productivity to catch up with global standards

Vulnerability 1: ASEAN’s lagging productivity

Vulnerability 1: ASEAN’s lagging productivity

As ASEAN advances to be an international market force, the reality of needing to face global competitive pressures is being increasingly felt. Using the US’s productivity level in 2016 as the basis for comparison, we find that ASEAN’s productivity levels still very much lagged that of the US.

- The exception was Singapore, with productivity levels of 0.7 relative to the US as compared to 0.17 for Malaysia and 0.02 for Vietnam and Cambodia1 (Figure 4.1).

While ASEAN’s labour productivity growth rates have exceeded global rates (as indicated in the previous section on “Drivers” (Parts 2 and 3)), the pace of this growth has varied between different selected ASEAN countries between 2015 and 2018 (Figure 4.2).

In the case of the ASEAN-6 economies, the growth of labour productivity showed varying degree of growth between 2015 and 2018 (Table 4.1). Indonesia maintained consistent labour productivity growth of 3.8% for the periods 2017-2018 and 2015-2016 while Vietnam’s growth maintained at 5.6% for the periods 2017-2018 and 2016-2017 (Vietnam). In the case of Singapore, Malaysia and the Philippines, labour productivity growth rate increased in 2016-2017 but slightly decreased in the period 2017-2018. On the other hand, Thailand saw its labour productivity growth rate decline for two consecutive periods.

Low productivity and inconsistent labour productivity growth should be treated with caution as low productivity may impact profit and investment for businesses; wages for workers; and tax revenues for governments.2

Vulnerability 2: Ageing populations

Vulnerability 2: Ageing populations

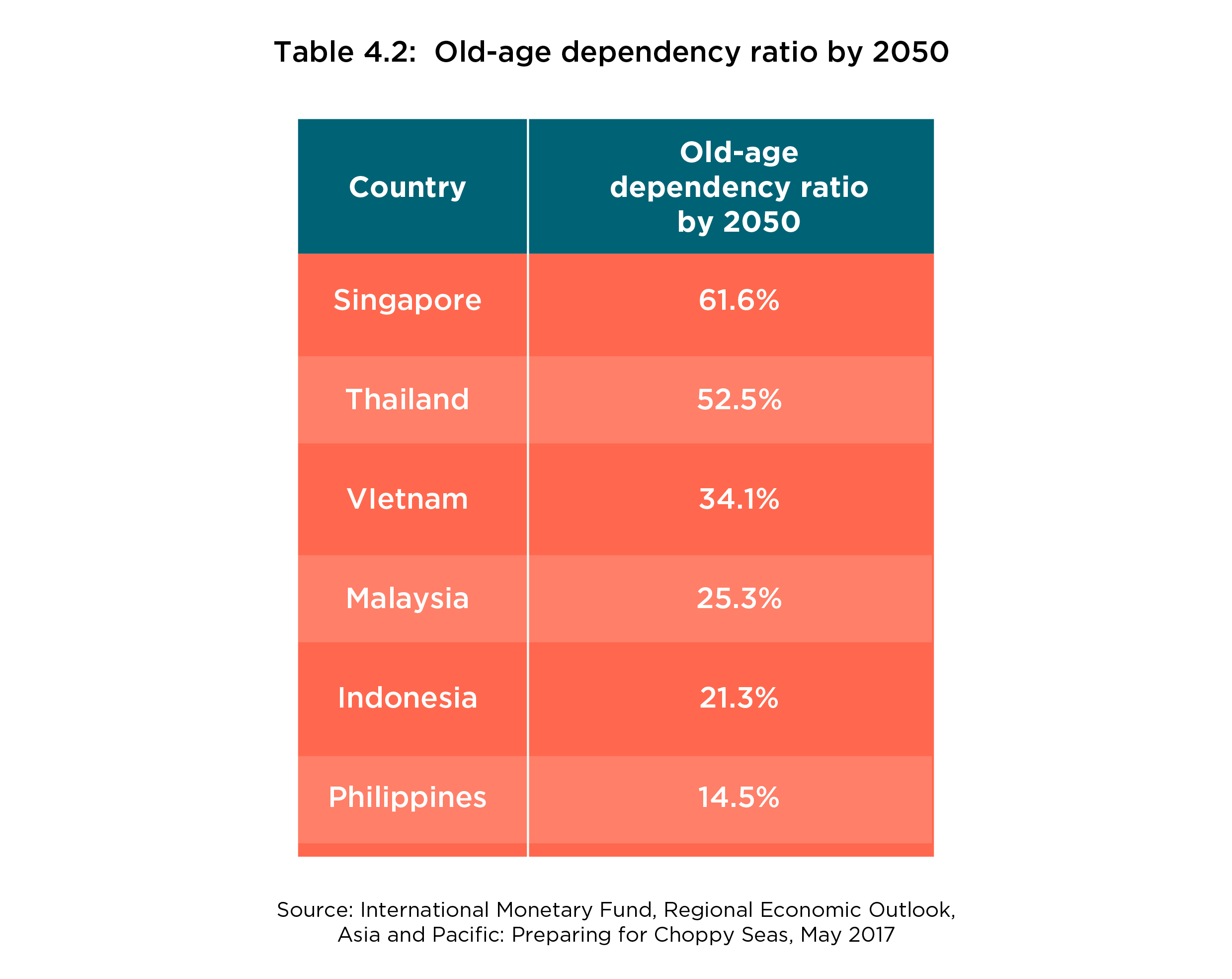

Demographic trends will further exert downward pressure on labour productivity. The percentage of the population over the age of 65 in ASEAN is expected to more than triple by 2050, with corresponding declines in the working age population.

- By 2050, the old-age dependency ratio will likely reach 61.6% for Singapore and 52.5% for Thailand3 (Table 4.2).

- For other middle income countries such as Vietnam and Malaysia, their old-age dependency ratios are expected to reach 34.1% and 25.3% by 2050 respectively. For economies such as Indonesia and the Philippines, their respective old-age ratios are projected to be lower within the same time frame (Table 4.2).4

Demographic impacts may be felt more strongly in Thailand as its productivity level is only about one-tenth that of Singapore. Its population of 65 or above has been forecasted to approach 30% by 2030, close to that of high-income nations. Meanwhile, Thailand’s GDP per capita reaches only about 15% of these same high-income countries.5

Vulnerability 3: Rising salaries and wages

Vulnerability 3: Rising salaries and wages

Apart from the significant productivity level variance between much of ASEAN and developed economies and concerns over declining productivity growth rates, rising remuneration is another source of concern. While higher minimum wages can boost the purchasing power of consumers, pay increases that outpace economic and price growth can have a detrimental effect on the earnings of businesses, thereby making foreign investors less inclined to invest.

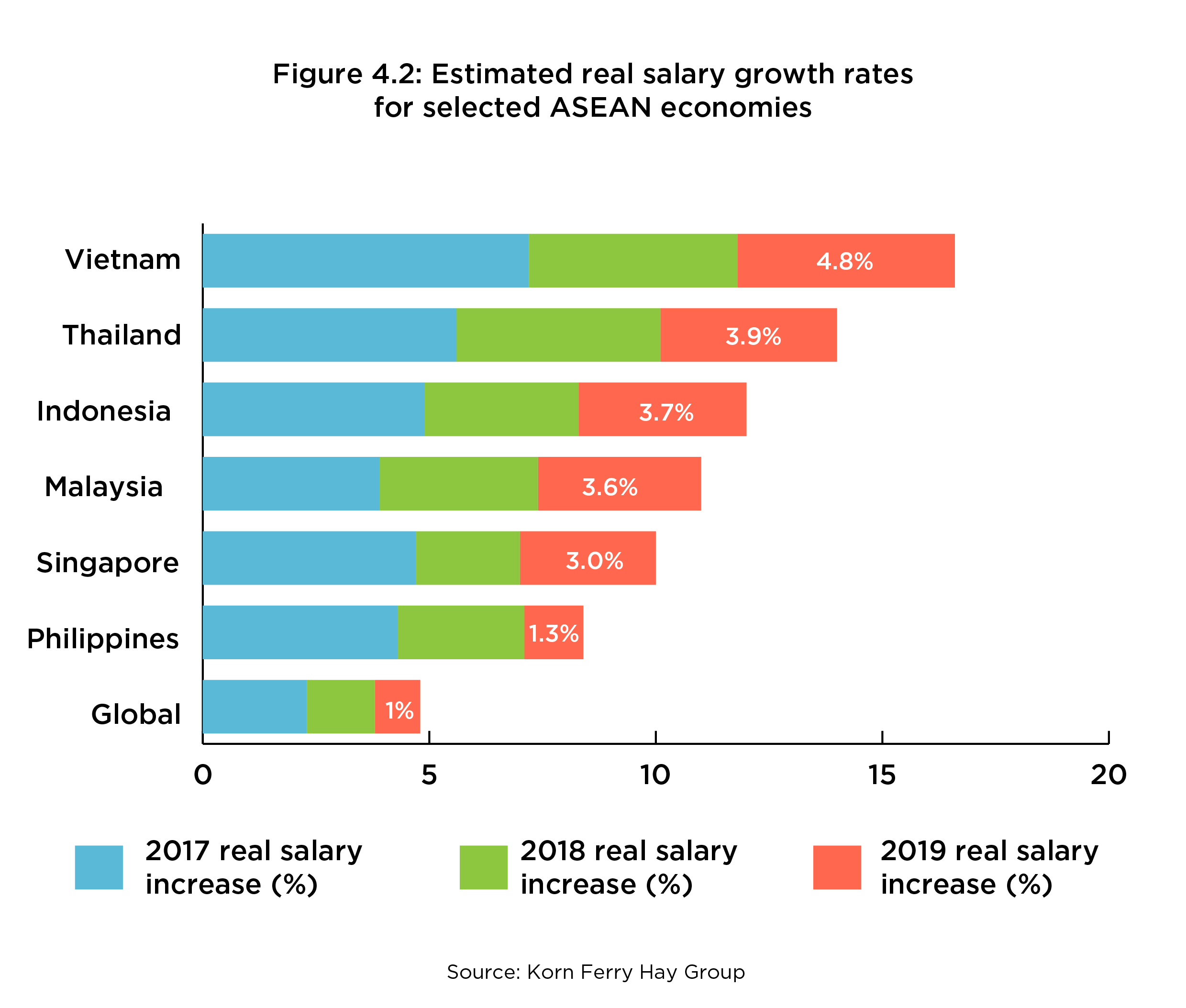

- For example, when analysing projected salary rises for skilled workers, estimates show that Vietnam (4.8%), Thailand (3.9%), and Indonesia (3.7%) would face the highest real salary increases in ASEAN in 2019 (Figure 4.2).

- This is consistent with projections that Asia as a whole would experience the highest real salary increase globally in 2019 although the salary growth rate for a few ASEAN countries (such as the Philippines and Thailand) are expected to be lower in 2019 compared to 2018.6

The latest independent forecast issued in January 2019 revealed that real-salaries globally are expected to grow an average of 1.0% in 2019, down from 1.5% for 2018.7

Minimum wages in Southeast Asia have also grown sharply due to rising costs of living and to boost domestic consumption. Governments have also been reportedly implementing minimum wage hikes to build up public support.

- In Cambodia, the government-set monthly minimum wage was US$170 in 2018, an increase of 11.1% from 2017 and nearly triple the 2012 level.

- Myanmar’s minimum wage was increased by 33% starting in May 2018, rising from US$2.65 to US$3.54 per eight hour work day.8 It was also reported that, ten of Myanmar’s 550 garment factories have shut down in the same year, with high labour costs in part to blame.

- Laos’ minimum wage rose by 22% in 2018 compared to the previous year, and tripled from their 2012 level.

- In the Philippines, the daily average minimum wage rate, which as of August 2018 was between US$4.80 – US$9.61, is among the highest in ASEAN, ranking above competitors Indonesia and Vietnam.9

Vulnerability 4: Significant infrastructure gaps

Vulnerability 4: Significant infrastructure gaps

a) Rising infrastructure needs

The gap in infrastructure may implicate economic growth since infrastructure fuels the economy. For many ASEAN countries, the main hurdle facing their ongoing growth has been the underdeveloped state of infrastructure. Indeed, current ASEAN leaders such as President Joko Widodo of Indonesia and President Rodrigo Duterte of the Philippines have made massive infrastructure investments the landmark policies of their respective administrations. That being said, while infrastructure spending growth has outpaced GDP growth for many ASEAN countries, the quantum of infrastructure spending is still arguably inadequate to meet infrastructure needs, as we will observe in this proceeding article.

Rapid economic growth, demographic and social changes in the region have increased infrastructure needs: namely in power, utilities, the social sector (housing, health, and education), transportation, logistics, and digital connectivity. Government infrastructure spending patterns have reflected this demand. The Philippines, Vietnam and Thailand recorded infrastructure spending growth of above 10% from 2012-16 (Figure. 5.1). Indeed, when looking at all the selected ASEAN countries listed in Figure 5.1, infrastructure spending in six countries between 2012 and 2016 was growing faster than their overall economies.10

- As argued in a 2017 report, infrastructure spending growth has a direct positive correlation with tangible GDP growth (with the exception of Thailand). This is due to the fact that a higher investment in infrastructure allows a country to increase its output, thereby boosting growth (Figure 5.1).11

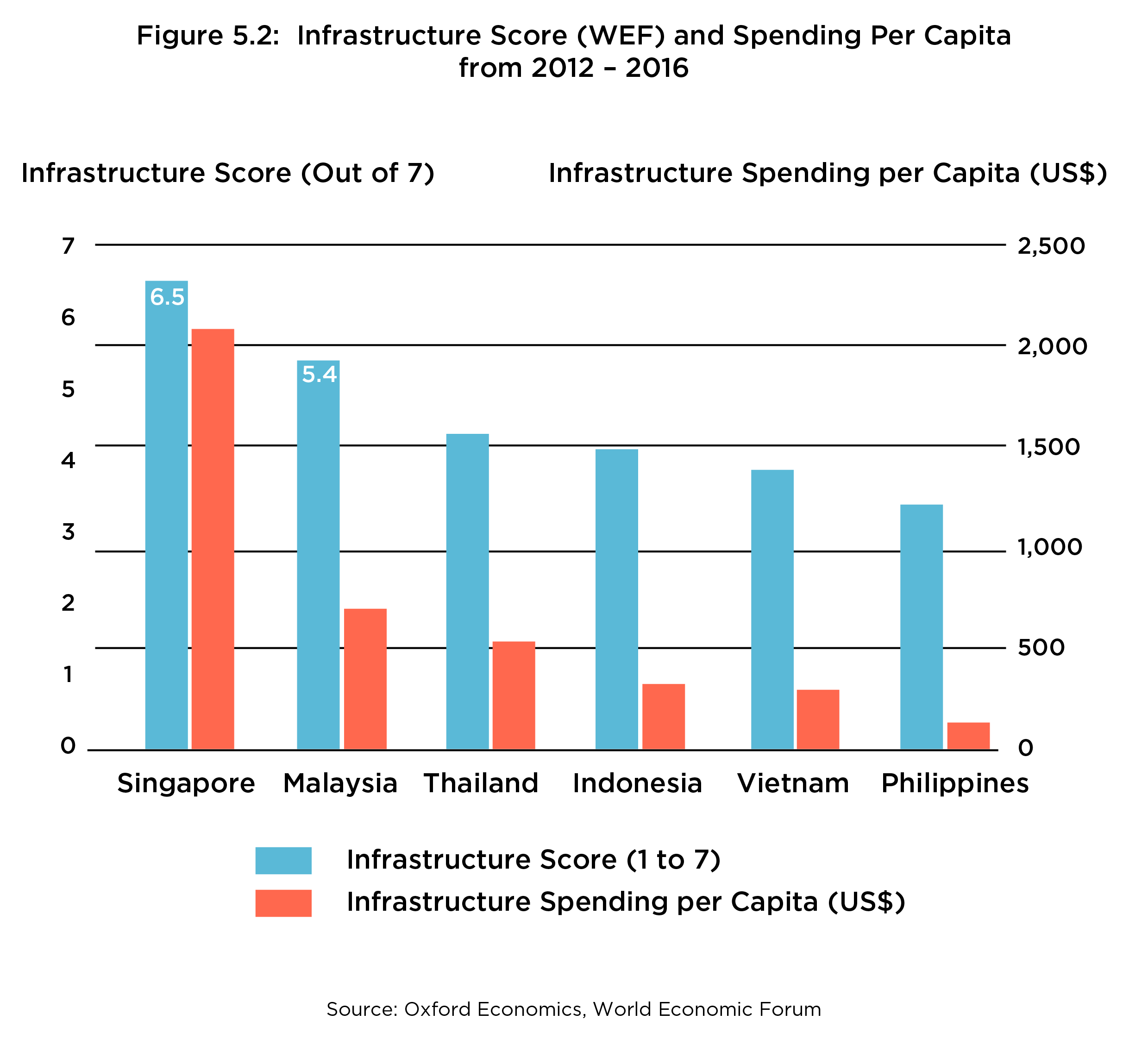

- Using the World Economic Forum’s Infrastructure Score as a guide for the adequacy of infrastructure, we observe infrastructure gaps in various ASEAN countries–save a few such as Singapore and Malaysia (Figure 5.2). The gap is reflected in the variance from the perfect score of 7 in the chart below. 12

Given infrastructure spending and demand patterns, a 2017 report by the Asian Development Bank estimated an annual infrastructure gap of US$92 billion, or 3.8% of Southeast Asia’s total GDP (baseline estimation), from 2016 to 2020 (excluding Singapore, Brunei, and Laos).13

- The same report estimated that the required annual infrastructure spending need for Southeast Asia (again excluding Singapore, Brunei and Laos) would amount to US$147 billion (baseline estimation) for 2016 to 2020.14 The gap, as we will see in the next section on Prospects, is likely to widen further as ASEAN pushes for further economic expansion.

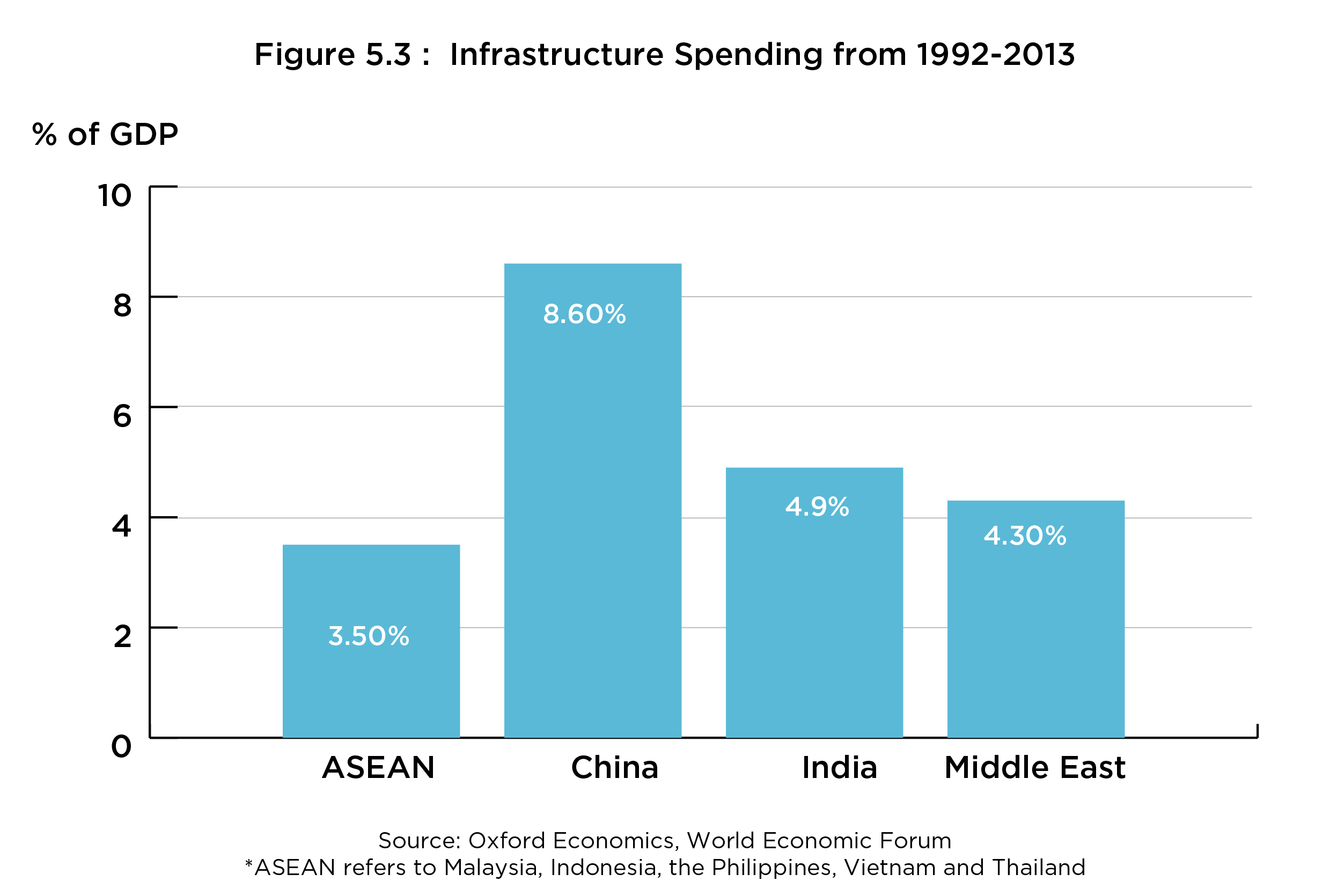

When looking at the infrastructure spending of different regions between 1992-2013, it should be noted that ASEAN remains behind other regions such as China, India, and the Middle East. According to data by the McKinsey Global Institute, selected ASEAN countries such as Malaysia, Indonesia, the Philippines, Vietnam and Thailand only spent an average of about 3.6% of their GDP on infrastructure between 1992 and 2013. (Figure 5.3).15

b) Inconsistent project implementation record

One hindrance to ASEAN’s infrastructure drive has been the region’s relatively inconsistent implementation of said projects. According to a 2018 report by McKinsey Global Institute, a lack of government commitment and a lag in managerial skills have meant an inconsistent infrastructure project implementation record for many ASEAN countries. A McKinsey survey of 7,786 Southeast Asian projects between 2007 and 2017 found that in certain countries, up to 11% of announced projects were cancelled or delayed indefinitely. 16

China’s Belt and Road Initiative (BRI) has been pointed to as a possible solution for ASEAN’s infrastructure gaps. Despite the geopolitical and geo-economic concerns that have been raised about the BRI (including concerns over so-called ‘debt diplomacy’), ASEAN has been the largest recipient of BRI-related investments and construction projects between 2013 and 2018, totalling some US$145.33 billion. This is the equivalent of 24% of the total BRI-related investments and construction projects worldwide within the same time period, which measured at US$602.96 billion. For context, ASEAN’s share of BRI-related projects was roughly three times the size of Europe’s, and with a slight lead over Sub-Saharan Africa. 17

However, the actual implementation record for BRI projects remains mixed. According to the American Enterprise Institute’s (AEI) Global Investment Tracker, by total costs, Malaysia ranked the highest in terms of ‘troubled’ BRI-related Chinese investments and construction projects, at US$5.44 billion between 2013 and 2018 (Figure 5.4). The AEI Global Investment Tracker defined ‘troubled’ projects as those in which said projects became impaired or failed after a commercial agreement was struck. 18

Vulnerability 5: Extra-regional trade dominates

Vulnerability 5: Extra-regional trade dominates

High trade-to-GDP ratio

ASEAN’s share of global exports has rose from 2% in 1967 to 7% in 2016, indicating greater penetration of ASEAN products into global markets.

- Consistent with this development, the contribution of trade-to-GDP has increased significantly in the region, with the trade-to-GDP ratio doubling from 43.1% in 1967 to 87.0% in 2016.19 In 2018, ASEAN’s trade-to-GDP ratio rose even further to 93.1%.20 A breakdown of the trade-to-GDP ratio for the whole ASEAN region can be seen in Figure 6.1.

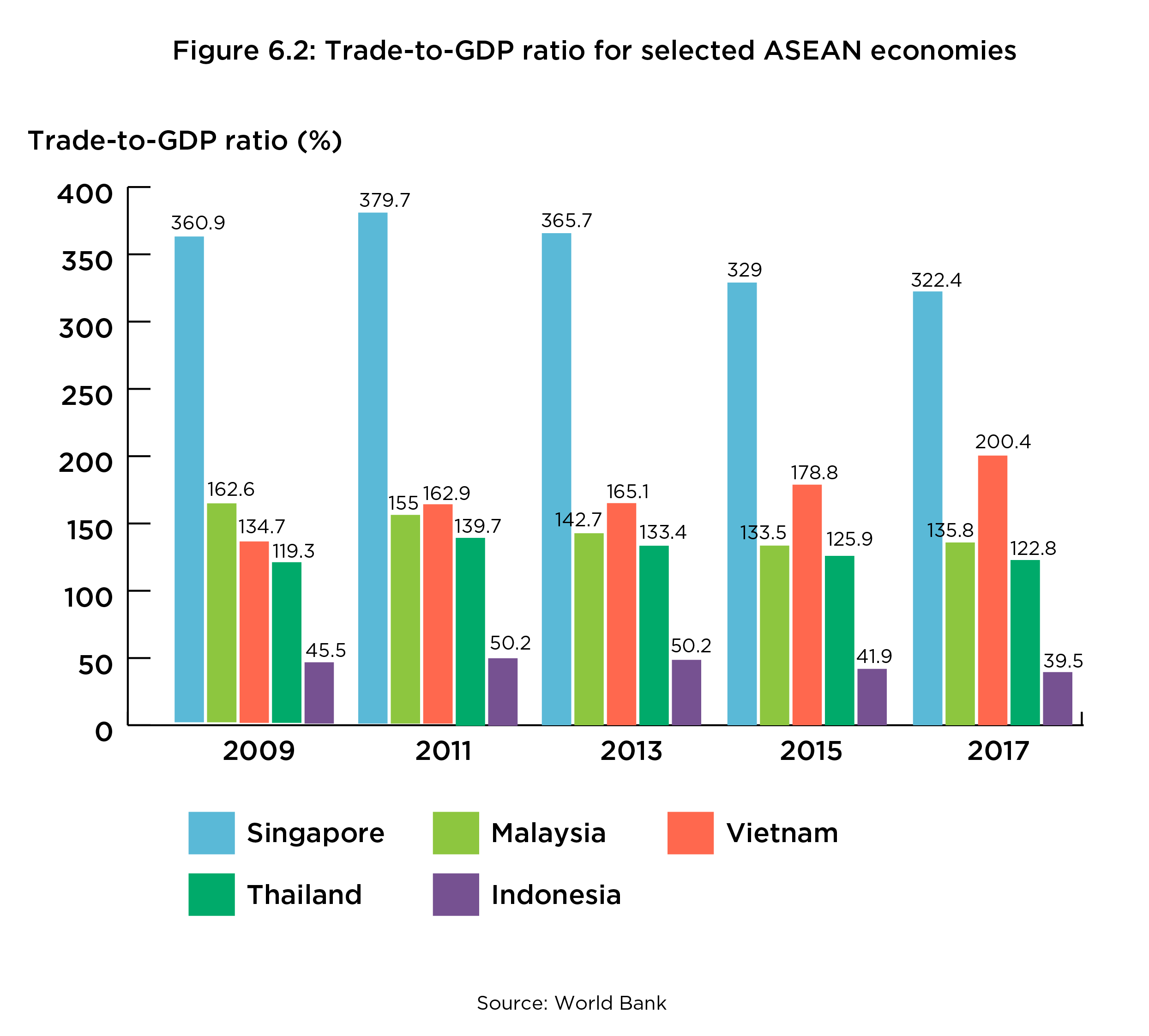

- In Figure 6.2 below, a breakdown of trade-to-GDP ratio of selected ASEAN countries is shown. This gives an idea of how trade-dependent ASEAN’s most prominent economies are, with Singapore overwhelmingly having the highest trade-to-GDP ratio among them.

Narrow concentration of trading partners, especially China

According to the ASEAN Secretariat, the value of ASEAN’s trade in goods increased by around 35.4% from 2008 to 2017, reaching around US$2,574.8 billion. Extra-regional trading relationships have played a dominant role to fuel this growth.

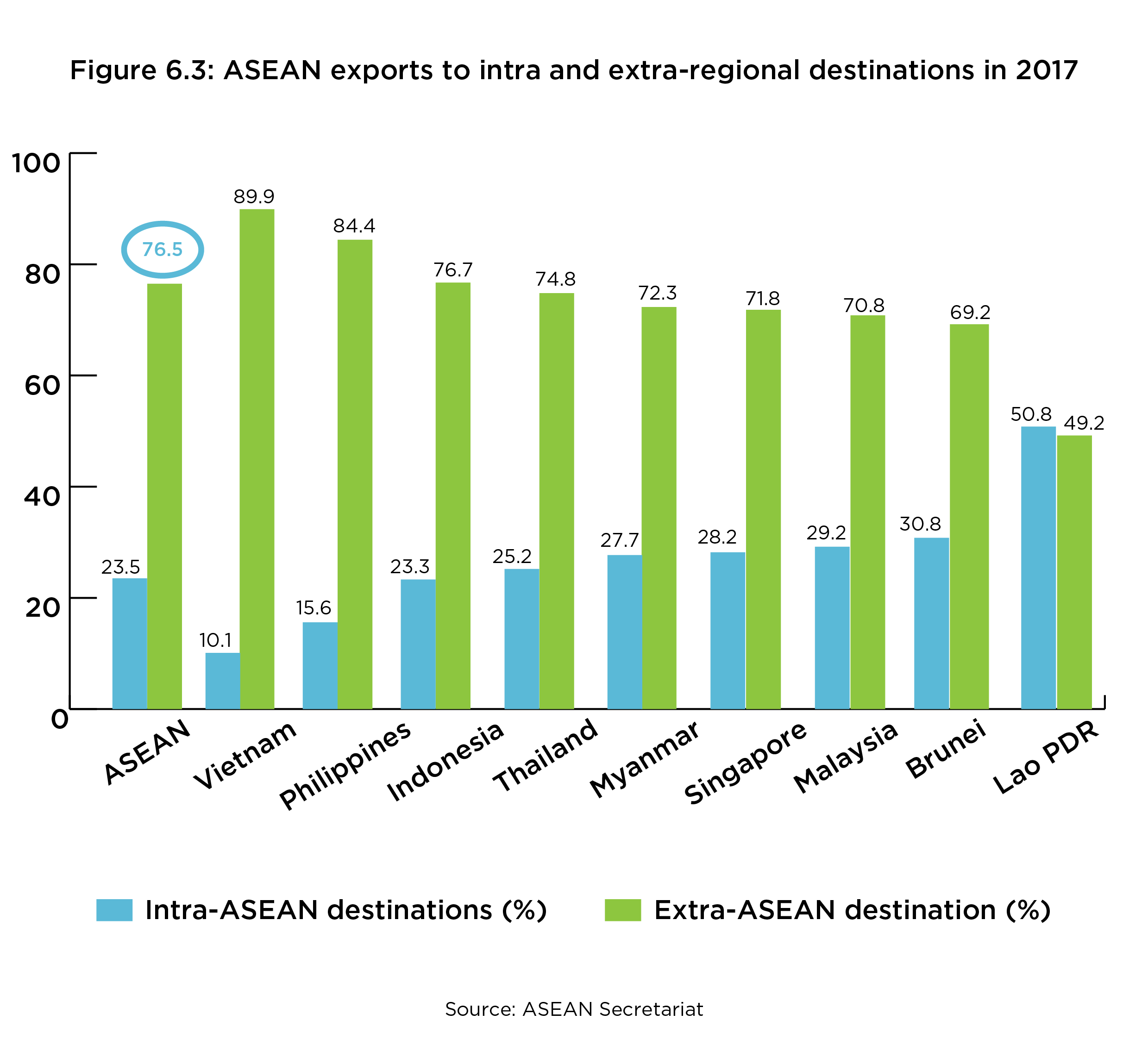

For example, around 76.5% of exports from ASEAN in 2017 was with extra-ASEAN partners (Figure 6.3). Out of which, 53.6% of exports was with China, EU, US, Japan, South Korea, and Australia/New Zealand combined, which is around 30% more than the exports to intra-ASEAN destination.21

According to the ASEAN+3 Macroeconomic Research Office (AMRO), by 2035, China is expected to continue to account for 22% of ASEAN’s trade whereas ASEAN is forecasted to account for 18% of China’s total trade.22

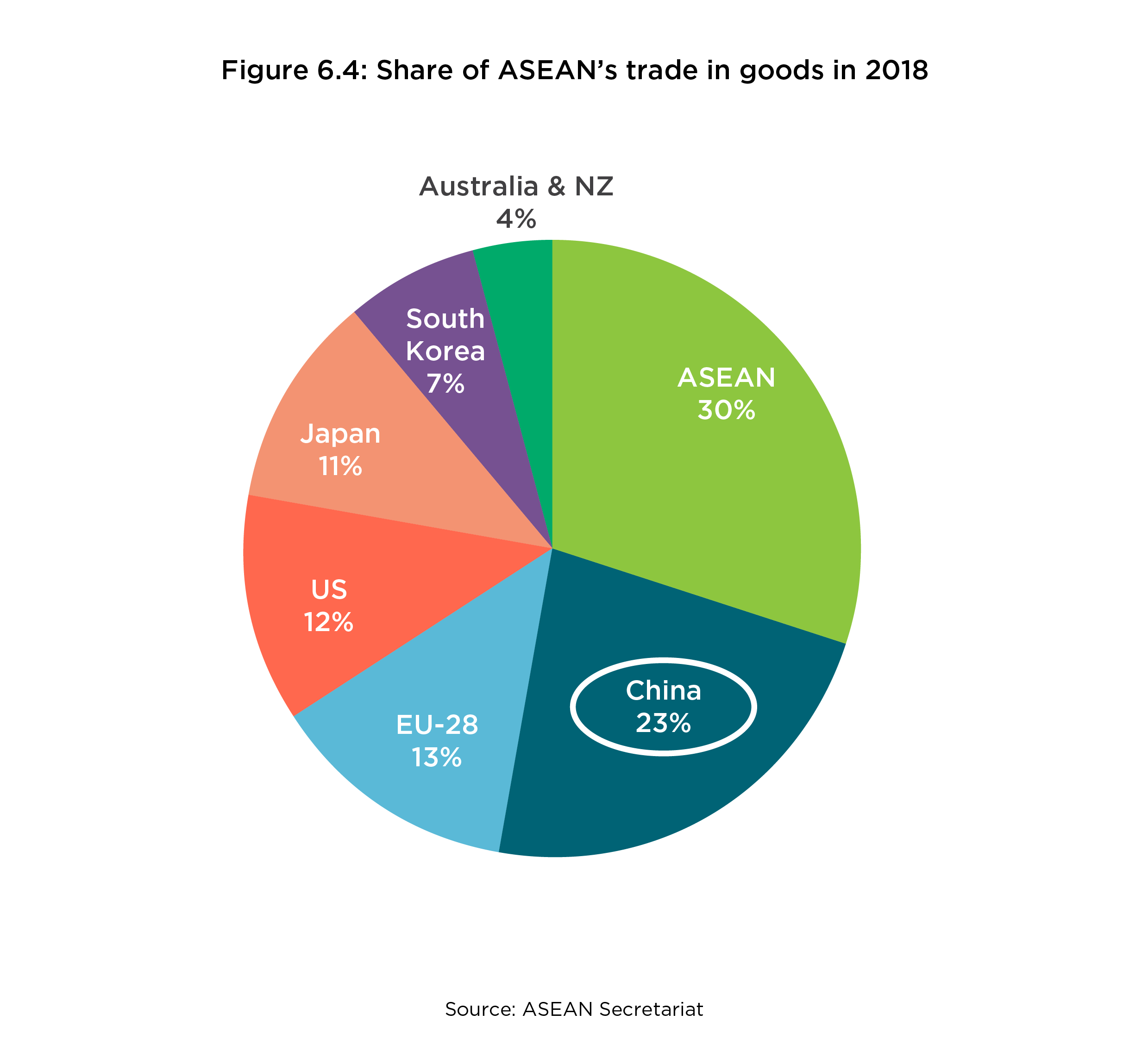

- In 2018, trade with China represented 23% of ASEAN’s total trade with its most significant trading partners23 (Figure 6.4).

Summary

Close to 90% of ASEAN’s GDP is dominated by trade, in particular, merchandise trade. About 77% of its exports is with extra-regional trading partners dominated by six markets, namely China, EU, US, Japan, South Korea, Australia and New Zealand.24 Such a high degree of dependence on markets, which have shown significant economic correlations with each other, renders ASEAN vulnerable to global economic volatility, as is evident presently. This aspect aside, there are other challenges for ASEAN.

For instance, regional productivity levels have generally remained below that of developed economies, such as the US, while labour productivity growth has been inconsistent across the region. Accompanying this are other issues such as rising wages and widening infrastructure gaps. ASEAN’s economic prospects given these vulnerabilities are addressed in the next section, Prospects.

1 International Labour Office data.

2 ILO, “Why is labour productivity important in economic integration?”, January 28, 2015.

3 PwC, The Future of ASEAN: Time to Act, May 2018; International Monetary Fund, Regional Economic Outlook, Asia and Pacific: Preparing for Choppy Seas, May 2017. Note: Old-age dependency ratio is defined as ratio of population aged 65+ per 100 of the population 15-64.

4 Ibid.

5 PwC, The Future of ASEAN: Time to Act, May 2018.

6 Korn Ferry, Korn Ferry 2019 Salary Forecast Shows Smaller Real-Wage Increases Across Most Parts of the World, January 2019.

7 Korn Ferry, Korn Ferry 2019 Salary Forecast Shows Smaller Real-Wage Increases Across Most Parts of the World, January 2019.

8 Nikkei Asian Review, ‘Minimum wages surge across Southeast Asia’, October 2018, ASEAN Briefing, ‘Minimum Wage Levels Across ASEAN’, published by Dezan Shira & Associates, August 2018.

9 Ibid.

10 PwC, Understanding infrastructure opportunities in ASEAN: Infrastructure Series Report 1, 2017.

11 Ibid.

12 Ibid.

13 ADB, Meeting Asia’s infrastructure needs, 2017. Note: According to ADB, the total infrastructure spending in 2015 in Southeast Asia (excluding Singapore, Brunei Darussalam and Lao PDR) was US$55 billion.

14 Ibid.

15 McKinsey Global Institute and McKinsey’s Capital Projects and Infrastructure Practice, Bridging global infrastructure gaps, June 2016.

16 McKinsey Global Institute, ‘Outperformers: Maintaining ASEAN Countries’ Exceptional Growth’, September 2018.

17 American Enterprise Institute, China Global Investment Tracker, April 2019.

18 Ibid.

19 ASEAN Secretariat, ‘Celebrating ASEAN: 50 Years of Evolution and Progress, A Statistical Publication’, July 2017.

20 ASEAN Secretariat, ASEAN Statistical Leaflet 2018, October 2018.

21 ASEAN Secretariat, ASEAN Statistical Highlights 2018, October 2018; ASEAN Secretariat, ASEAN Statistical Yearbook 2018, December 2018.

22 South China Morning Post, “Trade war will drive Chinese investment in ASEAN to US$500 billion by 2035, think tank says”, December 2018.

23 ASEAN Secretariat.

24 ASEAN Secretariat.

(Note: The term “ASEAN” can refer to either the collection of economies in this region or the intergovernmental institution which was established through the ASEAN Charter of 1967 or both.)

Research Director: Hong Jukhee

Editorial Team: Kwong Mook Shian, Mohd Imran Said Mohd Shamsunahar, Gan Bo Ren, Nor Amirah Mohd Aminuddin, Aznita Ahmad Pharmy