Economic Snapshot: ASEAN Focus Jan 2017 | Vietnam

Published date 02 February 2017

by Michael Kokalari, Head of Vietnam research for CIMB Securities

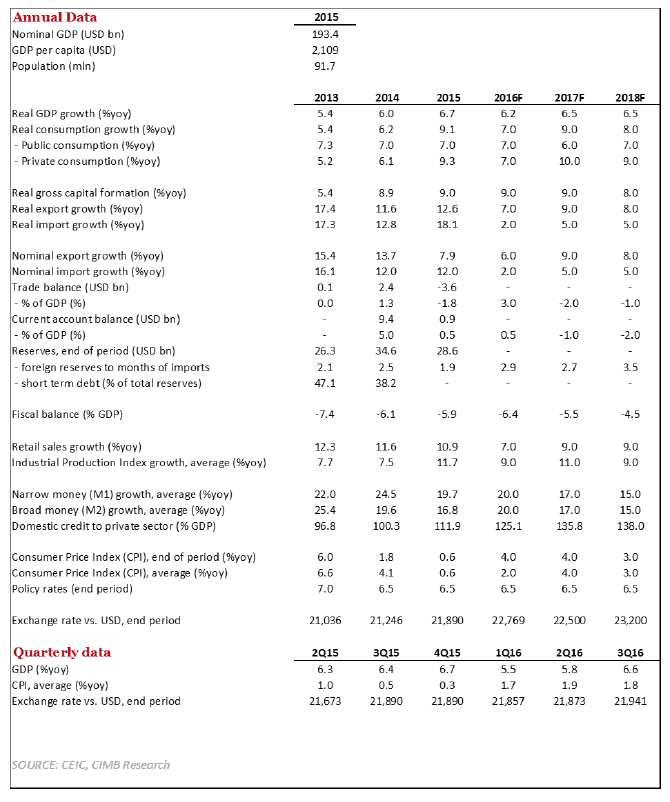

Vietnam’s economy grew 5.9% yoy in 9M16, versus 6.5% GDP growth in 9M15. Two temporary factors, the El Nino weather phenomenon, and weak oil production continued to weigh on growth, causing the lowering of my 2016 GDP forecast from 6.5% to 6.2% (in line with consensus forecasts). Both of those factors are unlikely to have any impact on growth next year, but Vietnam’s 8% domestic demand growth in 9M16 was supported by 17% loan growth, and loan growth is likely to decelerate to 14-15% in 2017 because the country’s banks need to raise capital. For that reason I forecast 6.3% GDP growth next year; I do not believe the economy will be significantly affected by the unexpected election of Donald Trump as the next US President.

Transitory factors still weighing on growth

- Vietnam’s 9M16 GDP growth was held back by an estimated 13% fall in oil production, and by flat agricultural production (17%/GDP), but the four primary drivers of GDP growth this year (and next) all look highly favourable: consumption (60%/GDP), new housing starts (+25% yoy in 9M16), infrastructure development (~6%/GDP), and manufacturing (15%/GDP), which is largely being funded by FDI inflows (+8% yoy in 9M16). The two transitory factors mentioned above have completely abated, and should not impact growth next year, but both still have a lagged impact on the country’s reported growth figures. For example, industrial production grew by just 7% in 9M16 due to the fall in oil production – despite an 11% surge in manufacturing, a 12% increase in electricity production, and a 24% increase in construction steel production.

- Regarding Vietnam’s drought at the beginning of this year, half of the country’s workforce is employed in agriculture – so although agriculture production is rebounding, the impact the drought had on rural consumers dampened overall consumption growth.

2017 outlook: 6.3% GDP growth, assuming banks’ capital raising efforts succeed

- Vietnam’s credit growth is likely to decelerate from 17-18% yoy in 2016 to 14-15% yoy in 2017 because the country’s banks need to raise about US$7bn-10bn of new capital in order to continue expanding their balance sheets, and to prepare for the implementation of the Basel II capital adequacy standard in 2018. Vietnam’s system-wide capital adequacy ratio sat at 13% at the beginning of 2016, but rapid credit growth this year is likely to lower that figure by about 1.5% pts, and the implementation of Basel II would reduce the system-wide CAR by another ~3-4% pts.

- Vietnamese banks’ prospects of raising new capital are quite good, as evidenced by the recent decision of Singapore’s GIC to buy 8% of Vietcombank, the biggest listed bank. However, the banks have been slow to initiate capital raising efforts – partly because they are focusing on growth, now that the country’s NPL crisis has been more-or-less resolved (Vietnam’s NPL’s fell from 17% in 2012 to below 3% at present). As a result, we expect retail lending to grow by about 40% in 2016 and 30% in 2017, which should help fuel 30% automobile sales growth in both years, and outstanding mortgages to grow 18% in 2016 and 14% in 2017 (which should help fuel 15% growth in housing starts next year).

- Assuming banks are able to raise sufficient capital to grow their loan books by about 15% in 2017, I would expect 6.3% GDP growth, driven by 8% consumption growth, 10% growth in manufacturing output, and 8% growth in investment (which I expect to come in at 35%/GDP). Consumption growth is likely to remain around 8% (unchanged from 2016), despite a deceleration in loan growth because the savings rate is likely to fall from 30% in 2016 to about 25% in 2017 as an increasing number of locals come to gain confidence in the current state of the economy (over half of surveyed consumers believe Vietnam’s economy is currently in a recession, according to AC Nielsen).

Not worried about the Trump administration

- Despite Mr. Trump’s anti-trade rhetoric, I expect Vietnam’s exports to grow by 7% yoy in both 2016 and 2017, and that about ¼ of Vietnam’s overall exports will continue to be shipped to America (Vietnam is ASEAN’s biggest exporter to the US). America’s “Pivot towards Asia” may be over under Mr. Trump, but its “Pivot towards Vietnam” is likely to accelerate given: (1) Mr. Trump’s open enmity towards China, and 2) the recent shift of the Philippines and Malaysia closer to China. I think it is very unlikely that Mr. Trump will push to impose stiff tariffs on products imported from Vietnam.

- Vietnam was touted as the biggest beneficiary of the TPP, but in my view the benefits of the TPP were overestimated, so I are not concerned that the TPP is now probably dead. I have always been sceptical of claims by the World Bank and others that the TPP could add 0.5% to Vietnam’s GDP growth rate because only about 15% of Vietnam’s overall exports are garments and other items that carry high tariffs (c.17-20%). Technologyrelated items, such as cell phones, electronics etc. now comprise 30% of Vietnam’s overall exports, and such items were unlikely to get much of a boost from the TPP (the fact that wages in Vietnam are about ½ those in China, with an equally skilled workforce is much more important).

Expect loose monetary policy, neutral fiscal policy and a steady VND exchange rate

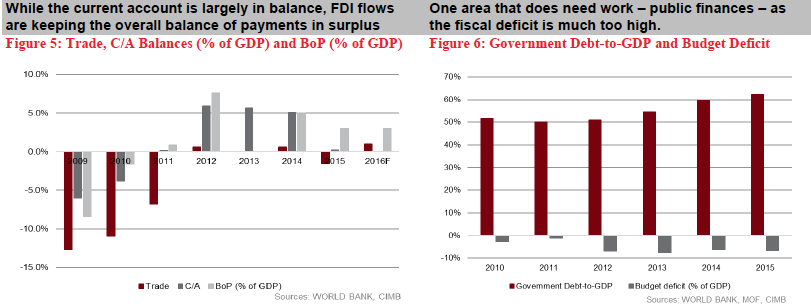

- The monetary and fiscal policies the government pursued this year are likely to linger into 2017. Specifically, I expect relatively loose monetary policy to continue next year (M2 growth was 17% in 9M16), in order to help facilitate the disposal of bad debts at the Vietnam Asset Management Company (VAMC). Less than 10% of the US$11bn NPLs which local commercial banks transferred to the VAMC have been resolved. That said, we also expect relatively high real rates (policy rates are 6.5%, while inflation is below 3%), which will help support the currency. Finally, the government needs to rein in its ~5.5%/GDP budget deficit because the country’s government debt-to-GDP ratio is likely to reach 65% next year, which is its statutory maximum level. Tax revenues grew 13% yoy in 9M16 due to better enforcement, and we expect the introduction of a property tax in 2017.

Risks and Other Issues

- Some investors are concerned that Mr. Trump’s policies may have an impact on Vietnam’s growth prospects, but the biggest risk to the economy in my view is that the banks do not raise sufficient capital to continue growing their loan books

- Regarding oil production, oil prices have now recovered to a level well above Vietnam’s US$30-35 production costs, so PetroVietnam, the national oil company is aggressively resuming its E&P activity (drilling new wells, etc.), but those efforts will take some time to be reflected in the nation’s growth statistics.

![]()