Economic Snapshot: ASEAN Focus Jan 2017 | Philippines

Published on 26 January 2017

by Arup Raha and Krzysztof Halladin

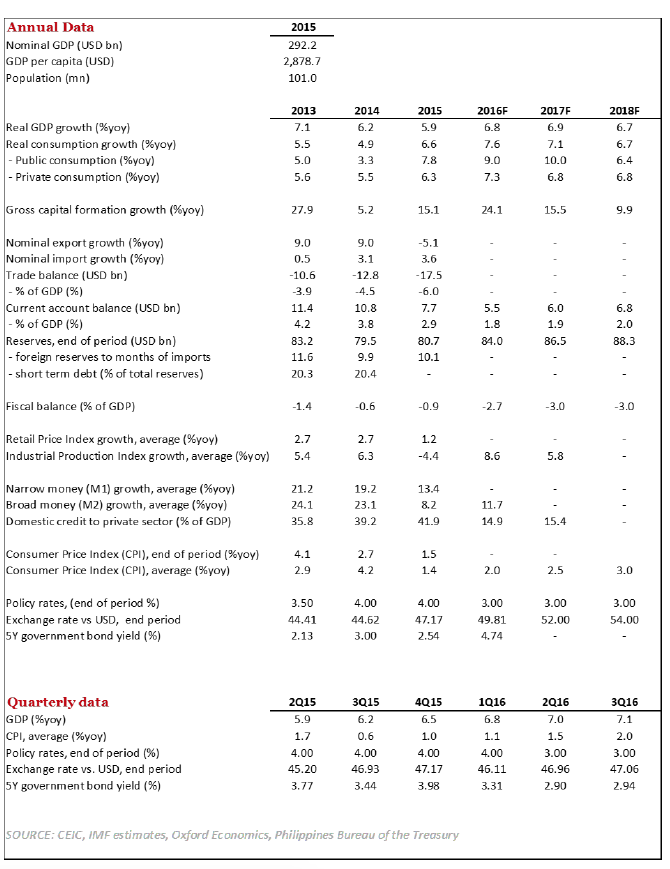

For the past few years, the Philippines has been one of ASEAN’s best economic stories. It has moved towards macroeconomic stability, increased transparency, created fiscal space, and managed to grow at a healthy pace despite external headwinds. These trends should continue through 2017 and 2018. We expect GDP growth of 6.8% in 2016 and for it to be mainly domestic demand led. A small rise to 6.9% is expected in 2017, as infrastructure projects and private consumption continue to support the economy. The robustness of domestic demand should keep import growth strong, which together with moderate export growth, means that the trade deficit should increase. The current account, however, should remain at a healthy surplus thanks to remittances. Inflation was down to a 20-year low of 1.4% at the end of 2015 but has inched up to 2% in 3Q16 this year, mainly driven by increasing food prices. Nonetheless, it should stay well within the BSP’s target range of 2% to 4%. The combination of strong domestic demand and controlled inflation means it is unlikely that the BSP will change monetary policy settings anytime soon. In our view, fiscal policy should be a lot more active and the PHP should further depreciate against the dollar while tracking other regional currencies.

Domestic demand to the fore

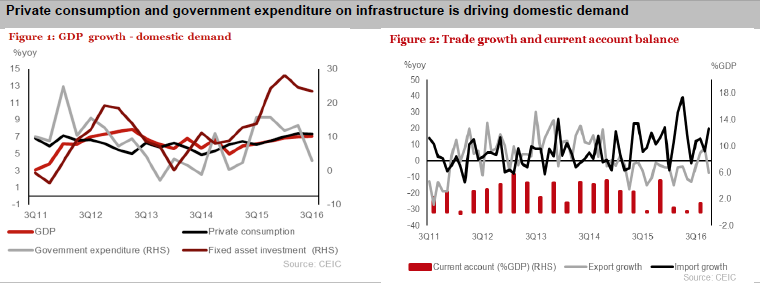

- The economy of the Philippines performed well in 3Q16.The GDP growth for this period amounted to 7.1% yoy triggering the revision of our GDP growth forecast from 2016 from 6.5% to 6.8% yoy. Private consumption and investment were the main drivers of growth in Q3, increasing, respectively, 7.3% and 23.5% yoy.

- Like other ASEAN economies, the Philippines has faced significant external headwinds and export growth, in US dollar terms, had been negative for 17 months. However, it turned positive in September this year with growth of 5% yoy. Import growth, decelerated to a still very-strong 21 % in Q3 compared to 25 % growth in Q2 yoy.

- A flourishing middle class, with growing remittances from Filipinos abroad, supports strong private consumption. However, the main reason behind robust private consumption is the rise in real incomes. Nominal incomes have risen due to overall growth and a steady labour market, while a decline in fuel prices and the overall (stable) inflation rate have allowed it to be captured in real terms.

- The steady growth in investments reflects a continuation of the Aquino government’s commitment to building infrastructure. The Duterte government has doubled down on that commitment and are expected to raise infrastructure spending to 5% of GDP from the 2.2% average during the Aquino years. Moreover, the desire to improve infrastructure is one of the reasons for President Duterte’s pivot towards China. His October trip to China gained 24bn USD of investment promises in sectors such as infrastructure and mining.

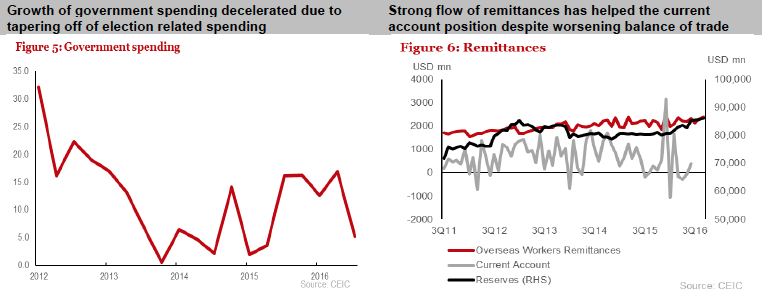

- Although the government consumption slowed from 13.5% (Q2) to 3.1%(Q3) following the tapering off of the election related spending, we expect it to pick up in 2017 as the proposed budget for 2017 is 11.6% higher the previous one. The government outlays should provide momentum to the economy in next 2 years.

- The Nikkei ASEAN manufacturing PMI for Philippines in December was 55.7 which is the highest reading among ASEAN Economies.

Trade: Rebound in exports, imports decelerating but still strong

- After 17 months of negative growth, in September, export (in USD terms) left negative territory largely because of an increase in exports of electronics (3.6% yoy) and agriculture products (24% yoy). On the other hand, imports decelerated from 25% (Q2) to 21% (Q3), with imports of capital goods slowing from 71.6% (Q2) to 22.7% (Q3). We expect export growth to be moderately positive as the global economy stabilizes in 2017. One might expect bigger exports to China following President Duterte’s pivot (in September, exports to China had already increased 34%). As the large infrastructure outlays are anticipated, then we expect imports to keep increasing faster than the exports, leading to further deterioration of the trade account.

- Notwithstanding the fact that trade deficit is expected to decrease, we expect the current account to maintain a surplus of 1.8 % of GDP in 2016, mainly due to the continued strength of remittances, which remain above 10% of GDP.

Inflation edging up but still within the target; PHP to be weaker

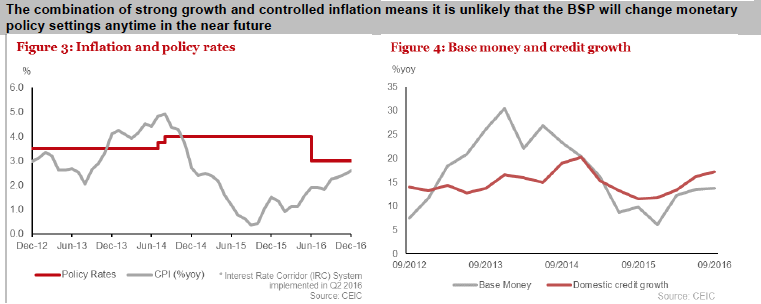

- CPI increased in 3Q16 to 2% in comparison to Q1 when it amounted to 1.1%. The rise was mainly driven by food inflation which, in annual terms, doubled between January and October (from 1.7% to 3.4%). This was, however, caused by adverse weather conditions. For instance, the price of vegetables increased by 12.3% in October, ramification of typhoons Karen and Lawin.

- Even with the latest print, inflation should stay well within the BSP’s target range of 2% to 4%. The combination of strong growth and controlled inflation means it is unlikely that the BSP will change monetary policy settings anytime soon.

- During the broad emerging market currencies sell off following the US election, the currency weakened past the PHP50/USD, level not seen since global financial crisis. Due to supply chain dynamics, the currency needs to move in step with regional currencies so we expect further weakening of PHP in 2017.

Fiscal deficit to widen; foreign reserves are solid

- In the first nine months of 2016 government revenue went up 2.6% yoy but expenditures rose by 14.1%. With high infrastructure spending expected the fiscal deficit is set to widen to 2.7% in 2016 and to 3% of GDP in 2017.

- Reserves declined slightly between September (86.2 bn) and October (85.8 bn), though still covering 10 months of imports.

Risk and other Issues

- Because of strong macroeconomics fundamentals, the main risk is political. Foreign investors have been worried about some President’s Duterte’s statements and actions. There was a huge outflow of capital in September.

- A clampdown of outsourcing in the US could affected the economy as many multinational companies have back-office operations in the Philippines. Moreover, around 33% of all remittances in 2015 came from US.

![]()