LIFTING-THE-BARRIERS REPORT 2013 | CONNECTIVITY

Published date: November 2013

TABLE OF CONTENT

(Click any topic to read the related section)

- 1. The ASEAN connectivity market

- 2. Recommendations for connectivity policies in ASEAN

- 2.1 Intra-ASEAN roaming and IDD

- 2.2 Mobile advertising

- 2.3 Mobile payments

- 2.4 Competitive intensity

- 3. Final Remarks

1. The ASEAN connectivity market

ASEAN as a region is characterised by the diversity of its membership countries, with wide ranging levels of economic development and degrees of cultural influences, but deeply interconnected at the core.

Connectivity and telecommunications play a critical role in bridging this diversity, driving levels of connectedness across nations and further uplifting ASEAN economies as a key economic enabler.

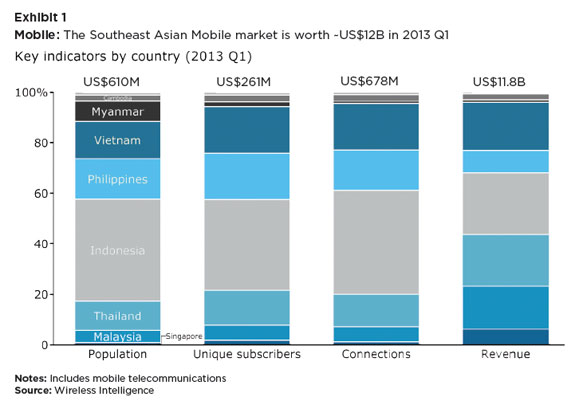

The mobile segment (voice and data) is the major contributor to the ASEAN connectivity market. Mobile revenue represents more than two thirds of the revenue pools in all markets except Singapore, where only ~50% of revenue is from mobile. In total, the ASEAN mobile market generated ~US$12B in Q1 2013 alone, with positive growth momentum over the last three years (from 2.5% to 12.1% depending on country).

In the last three years, revenue growth has been driven by the increase in mobile penetration rates, which have now reached above 100% in all member countries. Conversely, the average revenue per user (ARPU) has declined in all countries except Thailand, where it has remained flat.

A few key drivers have contributed to the ARPU trends:

- Many of the additional connections are due to new users in rural areas, with lower disposable income

- An increasing number of users are using more than one SIM, – either because of poor coverage or to optimise spending – therefore fragmenting their total spend

- Competition between operators has been fierce in all markets, most especially in the prepaid space

- Partially offsetting the above factors, penetration of mobile data has increased, which translates into higher ARPU

Not surprisingly, the decline in ARPU has been steeper in markets with higher pre-paid penetration, faster growth in connections to population ratio, and lower mobile data usage (Indonesia, Philippines and Vietnam).

At the country level, the dynamics of the mobile market are very different due to different stages of maturity. Singapore is the most mature market in the region with a dominant post-paid component and ARPU approaching US$30/month, while neighboring Indonesia is dominated by prepaid and has much lower ARPU, hovering closer to US$3/month. Pre-paid is largely dominant (~75% or more in number of connections) in all countries except Singapore, leading to high churn rates.

Most mobile markets in the region are highly concentrated, often with a dominant incumbent and the top three players controlling more than 80% market share on connections. Most players are centered on their domestic market, with only Axiata, Singtel and Telenor playing in a variety of regional markets in ASEAN, predominantly through minority shareholdings.

A recent critical phenomenon in ASEAN is a strong shift to data on mobile (with many mobile-only/mobile-first internet users). This has happened on the back of strong 3G rollouts by operators in most markets and rapidly declining prices for high-end feature phones or low-end smartphones, meaning touchscreen devices can now be had for average selling price (ASP) at US$75 or less.

With increasing mobile data availability, today’s mobile communication options have gone beyond traditional phone calls and SMS to include Over-the-Top (OTT) services. These new options include email, voice/video over IP (e.g. Skype), status updates (e.g. Facebook, Twitter) and internet-based message services (e.g. Whatsapp, BBM, Line). All these OTT services rely on data access only and benefit users due to the asymmetric pricing for data vs. voice/SMS usage on mobile operator networks. So far, most of these services have been provided by global MNCs with few ASEAN telcos having the relevant scale to push locally controlled OTT services in the region successfully.

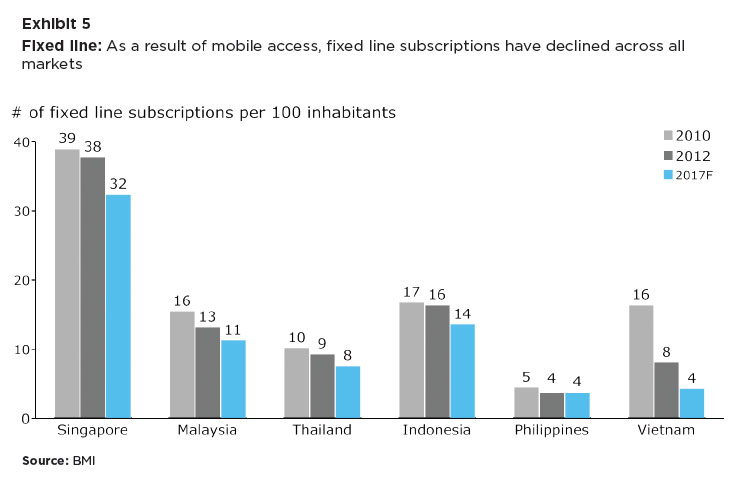

Fixed voice line (PSTN) penetration is on a continuously declining trend across ASEAN, driven by strong mobile adoption rates and, in many markets, limited legacy last-mile infrastructure to residential homes.

In contrast, broadband connection is expected to increase across the region albeit from a very low base. Many governments in ASEAN have realised the need for advanced fibre infrastructure to further create growth and drive a more knowledge-centric economy. For example, Singapore has implemented the Next Generation National Infocomm Infrastructure and Malaysia has started the National High-Speed Broadband (HSBB) Project, both of which aim to support increasing data usage. Indonesia is also pushing their National Broadband Network development for implementation until 2015. A further push on advanced Long Term Evolution (LTE) networks across ASEAN is likely to complement these efforts (with Singapore leading the charge on LTE rollouts).

Going forward, internet and data usage will continue to grow. However, many consumers will prefer mobile to fixed line access, driven by improved efficiency of mobile infrastructure.

2. Recommendations for connectivity policies in ASEAN

As we have seen, the ASEAN communication market has been developing well; ASEAN citizens have been fast adopters of new technologies that improve their lifestyle. However, there are several areas where further regulation could help to reduce boundaries across ASEAN and drive further integration. For this study, three have been prioritised: intra-ASEAN roaming and IDD, mobile advertising, mobile payments. In parallel, ASEAN regulators will have to retain a keen view on competitive intensity – managing price levels in markets while preserving local operators’ ability and scale to invest in next generation technologies.

2.1 Intra-ASEAN roaming and IDD

International roaming and international direct dialling (IDD) have become increasingly relevant as ASEAN becomes ever more connected. An increasing number of pan-regional business travellers and migrant workers create strong demand for these services.

However, relatively high roaming charges (both intra and extra ASEAN) and price variability are currently inhibiting adoption. The segments which face the highest impact are particularly lower/middle-income migrant workers within ASEAN. Intra-ASEAN rates are still high compared to intra-European rates; among operators, regional companies such as Singtel, Axiata, and Telenor have started offering pan-regional roaming plans (e.g. daily “flat fee” data roaming charges with selected partner operators), but so far most efforts have been targeted at higher end business travellers.

Current charges are partially the result of a lack of holistic pricing regulation and the absence of a common regulatory body that can drive any pricing initiatives.

In the EU, regulations have played a key role in managing roaming costs and making markets more open to cross-border competition. Regulations were enforced in three steps between 2007 and 2011 (initially capping wholesale/retail voice charges, later followed by SMS charges and wholesale/retail data charges). While the regional push has yielded significant benefits in reduced charges and increased consumer adoption, telco profits have suffered significantly and the extent of the reduction is one factor blamed for the slow adoption of 4G services across Europe.

In ASEAN, even though multiple bi-lateral initiatives are in place to reduce roaming costs such as those between Brunei and Singapore or between Singapore and Malaysia, there is not any comprehensive “common ground” at the ASEAN level yet. ATRC (ASEAN Telecom Regulatory Council) has adopted an ‘Addendum ATRC Intra-ASEAN Mobile Roaming Rates’ aimed at reducing roaming charges, but it has not been equally used in all member countries.

Well-managed roaming rates are likely to have broad positive economic effects through the improvement of ASEAN-wide communications, while at the same time lower charges will not necessarily be detrimental to mobile operator profitability, due to demand elasticity. Moreover, guidelines on roaming rates can create a more level playing field for national-only carriers who are seeing increased competition from pan-regional players with attractive regional roaming propositions on their linked operators.

Devising a new regional framework to address high roaming and IDD charges is crucial to develop connectivity in the region, but entails a fine balance between multiple competing forces:

- first, consumers demand lower prices, as the need to travel and communicate across borders increases. In this sense, legislative bodies around the world have come to see the EU approach as a sort of blueprint to drive roaming costs down;

- second, any pricing guidelines should allow telcos to earn a fair profit that they can reinvest in new infrastructure. As a lesson from EU roaming price regulation, telcos under excessive price pressure are slower to roll out newer technology platforms (e.g. 4G). This is extremely critical in ASEAN given the currently lower penetration of mobile data and strong expected growth, combined with the lack of wired infrastructure, which will require significant infrastructure build-up in the near future;

- finally, increasing competition from OTT services is another major factor impacting the future of roaming. Exhibit 7 illustrates how OTT messaging services have very quickly replaced SMS usage in ASEAN, and a similar dynamic is likely to take place through substitution of voice roaming with OTT voice services. Getting ahead of this trend could significantly benefit ASEAN mobile operators and retain profits in the ASEAN region (vs. usually global OTT offers)

Taking future roaming rate evolution in a joint public/private dialogue across ASEAN appears to be the best path forward to address the many competing interests — this will enable continued improvements in connectivity across ASEAN and ultimately strengthen ASEAN operators, if done right.

ASEAN as a region is seeing strong momentum in mobile advertising spending, due to the increasing penetration of smartphones and current under-investment in mobile advertising.

As seen in Exhibit 4 earlier, ownership of smartphones has reached 83% in Singapore, 30% in Malaysia, and has been growing strongly in all other countries, and this dynamic is likely to continue, driven by the increase in disposable income and the availability of more affordable smartphones at lower ASPs.

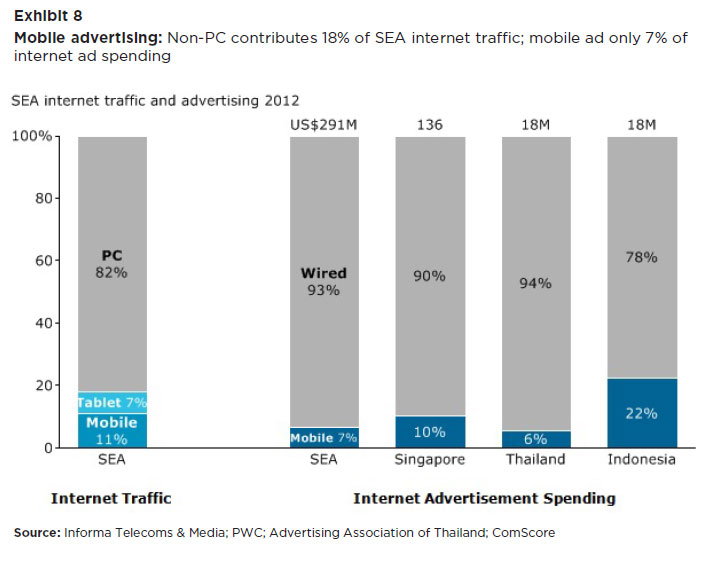

On the other hand, mobile advertising is still in the early stages in ASEAN. Out of the total spending on internet advertising, only 7% is in mobile, whereas mobile already accounts for ~18% of total internet traffic and this share is likely to increase because the growth in broadband connections is slower than the growth in mobile data connections (Exhibit 8).

This under-investment, combined with accelerating adoption of smartphones, points to a sharp increase in mobile advertising in the next 5 years. Analysts expect mobile advertising spending CAGR to be from ~20% up to ~40% until 2017.

To further develop this advertising platform, several factors affecting advertisers, telcos, OTT service providers, and consumers need to be considered:

- advertisers will increasingly recognise the attractiveness of mobile advertising and will increasingly gravitate towards this channel;

- distributors of mobile advertising, i.e. OTT and telcos, will ramp up competition for advertisement delivery. OTT providers have an advantage in content and smartphone applications. However, telcos are in a unique position to collect relevant consumer data necessary for highly targeted advertisements;

- finally, consumers will likely have heightened attention to privacy protection and lower tolerance for irrelevant (or inappropriate) advertising content.

With this in mind, regulators can play a pivotal role in encouraging and orchestrating this market by focusing on three important initiatives:

- Define minimum guidelines for consumer privacy across services/markets, notably covering: right to access and delete personal data, sensitive information sharing, use of data for advertising purposes, resale of data to third parties, security of consumer data storage, and record keeping

- Set up consumer-friendly opt-in/opt-out policies to address advertising concerns, mirroring policies in developed markets

- Create or designate national authorities to monitor behaviours and resolve potential conflicts

Mobile payments are an emerging trend with potential to create added value for consumers, telco operators, the financial services sector and merchants across the region.

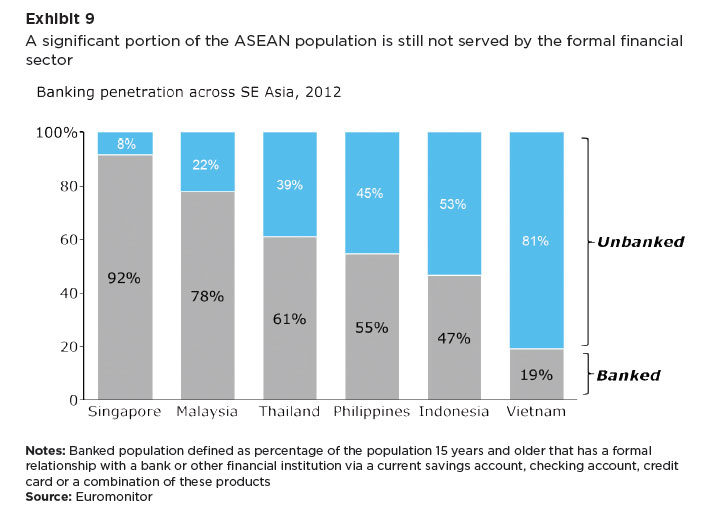

In ASEAN, a significant portion of the population is still not served by the formal financial sector, as shown in Exhibit 9. While the share of banked population has been growing only slightly in the past few years, the number of mobile subscribers has increased sharply, creating an opportunity to serve via the mobile channel customers not reached by traditional financial services (Exhibit 10).

Opportunities in mobile money are along three categories of usage:

a) Transaction services like M-wallet which gives access to a stored value account, mobile top-ups and mobile wallet-to-wallet transfers (P2P), enable traditional payments (e.g. paying utility bills, remittances)

b) Mobile commerce services through new mobile payment technologies (e.g., QR codes), mobile merchant payment technologies (e.g. mobile POS, P2P on the spot), mobile shops / portal services (e.g. online shopping, online games, virtual products etc.) and mobile marketing services (e.g. customer loyalty, mobile ads, coupons offers etc.)

c) Mobile banking offerings like banking enquiries, accessing accounts, mobile loan applications or disbursements, seeking insurance

Experience from credit cards and debit cards shows that scale adoption of new payment channels can take up to about 20-30 years. In ASEAN, the current adoption of mobile financial services is still in early stages, but most operators have launched initiatives in this space.

A healthy ecosystem is the key to unlock the mobile payment opportunity. However, this requires a flexible but clear regulatory framework that assigns roles to each player, and a strong government commitment ensuring players can justify the investment needed:

- Consumers can have a payment option that is secure, fully portable, and easy to use, without the need to open a bank account. Unlike other forms of plastic money (credit/debit cards), mobile payments can also be used for transactions between individuals such as remittances from abroad, reimbursements to friends, payments for small services, etc.

- Telcos can unlock an additional revenue streams and leverage mobile payment services to differentiate themselves in the market and increase customer loyalty; by providing more added-value services, carriers can address the issue of high churn in price-sensitive markets and move towards more value-based competition;

- Financial services companies would benefit by expanding their reach to the unbanked segment, creating a new revenue stream as intermediaries for mobile payment services; moreover, conversion from cash to electronic money is likely to drive familiarity and adoption of other products (e.g. credit/debit cards); financial inclusiveness could grow significantly as a side-benefit

- Merchants can expand their customer base, increase security of transactions, and diminish risks associated to cash

Regulators can help foster the development of mobile payment services in ASEAN by:

- providing a regulatory framework that clarifies roles, boundaries and pre-requisites for telco operators, financial services companies, and merchants

- managing and monitoring transaction fees, consumer privacy, forbidden uses and applicable controls to protect customers, ensure broad participation, and prevent bad behaviours such as fraud, money-laundering, illegal lending/gambling, etc.

- selectively guiding which services/platforms should be open to different technologies/standards (to create a level playing field, prevent customer lock-in, and stay on top of technology evolution) vs. where a common standard is needed (to ensure interoperability and stimulate investment)

Maintaining competition in ASEAN is crucial for a healthy development of the connectivity market. Currently, markets in ASEAN are concentrated, with fierce competition both among operators (notably in pre-paid) and between telco operators and OTTs. However:

- competition is primarily based on price (rather than value/quality of service), which, in combination with deregulated interconnect charges and on-net/off-net price differences, creates dysfunctional market behaviours, e.g. multi-SIM;

- some remaining barriers to competition create unnecessary inefficiency in the market, e.g. number portability is not fully applied within ASEAN countries, increasing the hassle for professional users to switch between operators.

A comprehensive look at competitive dynamics in the connectivity market should encompass a few aspects.

- Spectrum and licence allocation. Spectrum allocation in ASEAN countries is a key regulatory activity and significantly impacts competition – the number of spectrum blocks put up for auction, the number of players accepted and the price levels for spectrum all impact market dynamics. A good example is the recent Malaysian decision to award nine LTE licenses, which will lead to new mobile data challengers in the market. Spectrum remains a key competitive asset for mobile operators, as it is a key driver of network performance. Recent efforts have kicked off to harmonise mobile broadband between Singapore, Brunei, Indonesia and Malaysia which are looking to run 4G services on airwaves that will be freed up when analog TV broadcasts are switched off in the region by 2020. This ‘digital dividend’ will allow the use of a common 700MHz frequency band in the region which could enable travelers to easily roam with their smartphones in the future.

- Interconnect rates. Regulators set a variety of interconnect rates (mobile-to-mobile, mobile-to-fixed, SMS) to compensate telcos for using each other’s networks – this is often a key lever to reduce the benefits of incumbency and enable competition. While the fees paid differ across markets, a general trend to reduce interconnect charges is emerging, with Thailand being the latest example, where AIS, DTAC and True Corp have agreed to lower their fees supported by their regulator, NBTC.

- Fibre roll-out. Next generation national broadband networks are a key priority for most ASEAN countries and rollout paths differ significantly. Given the significant costs in upgrading/building fibre networks (beyond the level where it is economically attractive for telcos outside of high value geographies), varying forms of public/private partnerships can be taken. Examples include Singapore, which opted for structural separation and the government paying for the rollout (driving stronger levels of retail competition), or Malaysia, which provided additional funding to Telekom Malaysia, who in turn is offering wholesale access at regulated rates.

3. Final Remarks

ASEAN has a healthy connectivity market with headroom for growth over the next few years, but is facing similar transitions as developed markets. Regulators can definitely play a role to further maintain a healthy competitive environment, stimulate growth and deployment of new infrastructure and services, thereby enhancing connectivity and integration across ASEAN and learning from the evolution in more advanced markets.

There are three specific areas where regulatory action can be most effective in the near future.

- Roaming rates are still a barrier to widespread cross-ASEAN connectivity. Carefully managing roaming rates (and termination costs) would enable broader adoption and integration of ASEAN connectivity markets, while ensuring attractive enough operator profitability to drive further investments into next generation infrastructure.

- Mobile advertising is a significant growth opportunity across ASEAN, but requires a solid regulatory structure to ensure no future problems will arise (particularly around privacy) and a healthy marketplace can develop.

- While still at an early stage of development, mobile payment services have the potential to address the needs of many consumers across ASEAN (particularly the unbanked population). Regulators can foster deployment and adoption of these services by defining guidelines on roles and responsibilities in the ecosystem.

Finally, maintaining healthy levels of competition is instrumental to connectivity growth. Regulators will need to retain a keen eye on dynamics in their respective marketplace and trends emerging across the region. Ensuring a strong future evolution for connectivity across ASEAN should involve an open dialogue and cooperation among regulators and private industries. NAF and similar platforms can offer a basis to collect input for policy making and to keep a finger on the pulse of the ASEAN connectivity market.

![]()

RELATED REPORTS

- AN ANALYSIS OF THE ASEAN COOPERATION IN INFORMATION AND COMMUNICATIONS TECHNOLOGY (ICT)

- LIFTING THE BARRIERS REPORT FOR ASEAN CONNECTIVITY