ASEAN Economic Progress: ASEAN Economic Cooperation

Published on 9 December 2019

Factor 1: ASEAN economic cooperation to counter the downside of GVC embeddedness

Factor 1: ASEAN economic cooperation to counter the downside of GVC embeddedness

An estimated 66% of ASEAN’s exports are accounted for through its participation in global value chains (GVCs). Figure 10.1 shows that this figure has been increasing since 1990, from 53% in 1990 to 63.9% in 20101 and gradually dipped to 61.0% in 2015 and 60.9% in 2018 (Figure 10.1).

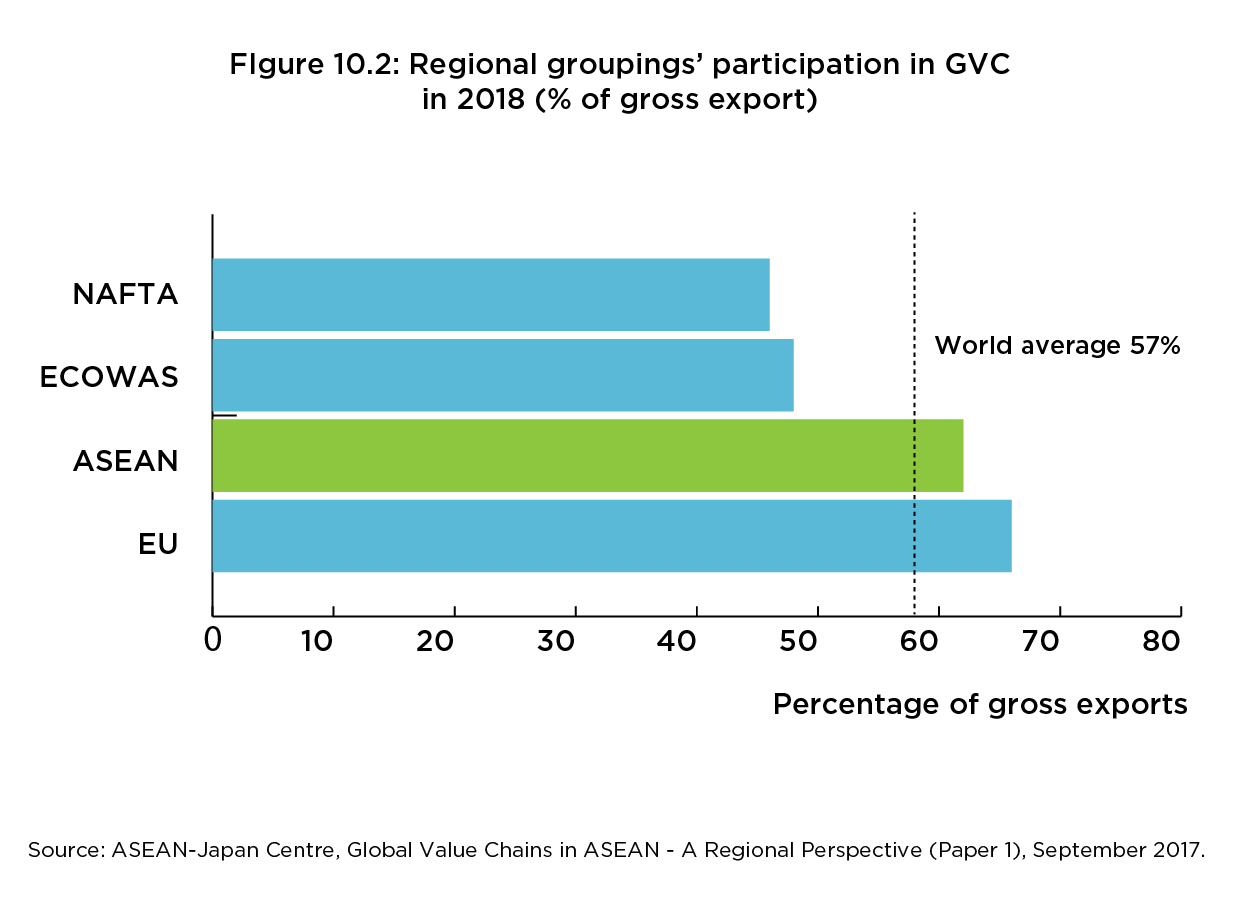

- The extent to which ASEAN participates in GVCs is comparably higher than most other active regional groupings including the North American Free Trade Agreement (NAFTA) area and the Economic Community of West African States (ECOWAS). Only the EU slightly surpasses ASEAN in this regard (Figure 10.2).2

ASEAN’s increasing embeddedness in GVCs is consistent with some of the observations indicated in previous sections.

- Part 3 highlighted the positive aspect, i.e., ASEAN’s global FDI pull as an economic growth driver.

- Parts 4-6 highlighted ASEAN’s vulnerabilities owing to its very high and increasing degree of dependence on extra-regional trade and investment flows.

Increasing the share of intra-ASEAN trade and investment flows, a key objective of ASEAN economic cooperation agenda, would be an important strategy to counter some of these vulnerabilities. The following analysis takes a closer look at some of the impacts of ASEAN economic cooperation on intra-regional trade and investment flows thus far.

Factor 2: Intra-ASEAN merchandise trade

Factor 2: Intra-ASEAN merchandise trade

a. Sharp fall in tariff rates

A key tool to enhance intra-ASEAN trade under ASEAN Free Trade Area’s (AFTA’s) Agreement on the Common Effective Preferential Tariff (CEPT) and later the ASEAN Trade In Goods Agreement (ATIGA), has been the lowering of tariffs for goods originating from an ASEAN member country going into another. There has been good progress in this regard.

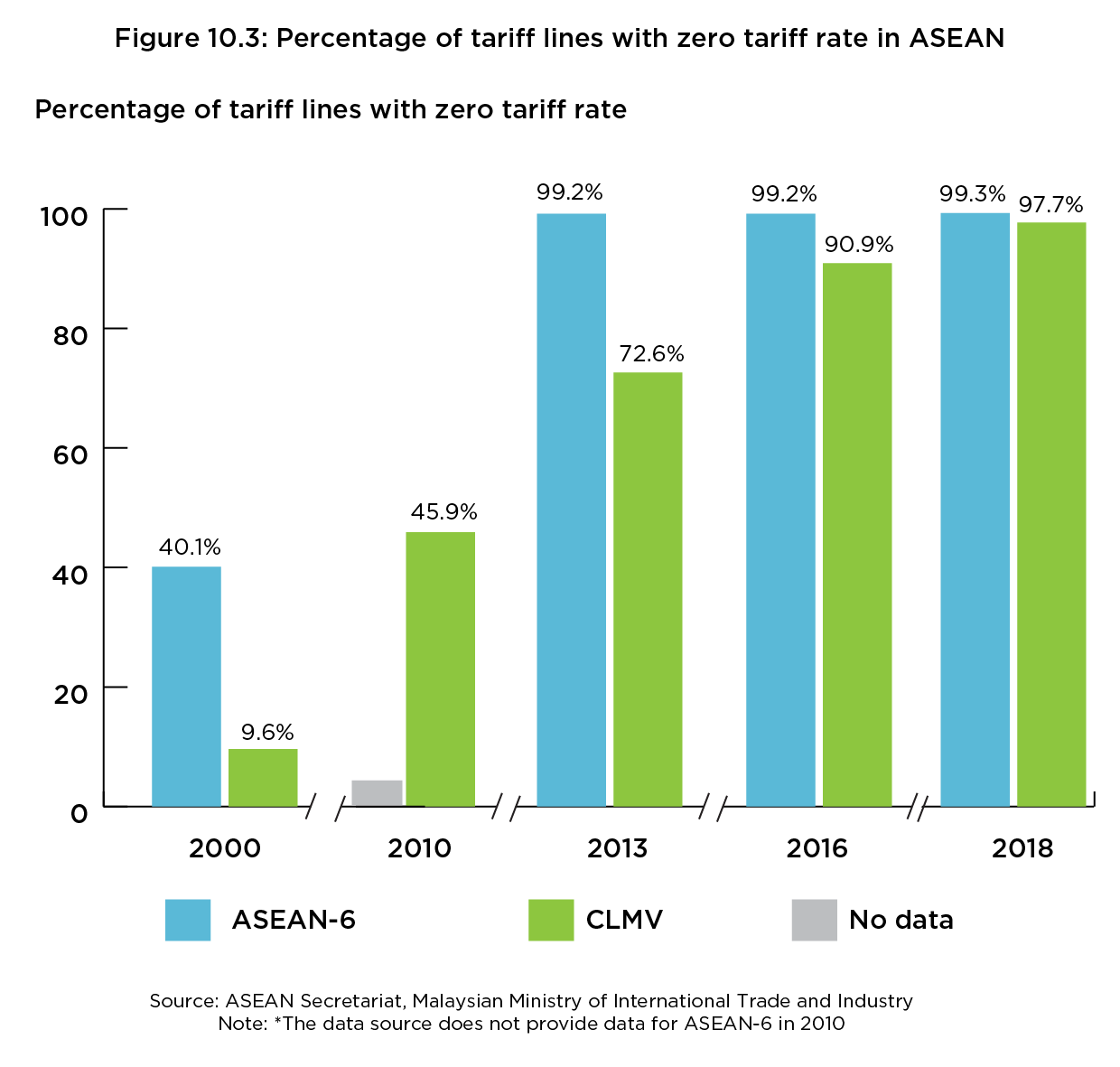

- For example, the number of tariff lines with zero tariff rates for both ASEAN-6 (Brunei, Indonesia, Malaysia, Singapore, Thailand, the Philippines) and CLMV (Cambodia, Laos, Myanmar, Vietnam) countries have increased significantly. This increase is most evident for CLMV countries that have seen the elimination of import duties rise to 97.7% in 2018 (Figure 10.3).

- Recent data from the ASEAN Secretariat indicates that in mid-2019, 98.6% of import duties have been eliminated from ASEAN as a whole. As of mid-2017, 70% of intra-ASEAN merchandise trade flows were tariff free.3 Average intra-ASEAN tariff rate has decreased 13-fold from 2.58% in 2007 to 0.20% in 2017 (Table 10.1).4

b. Increase in merchandise trade value but not relative importance

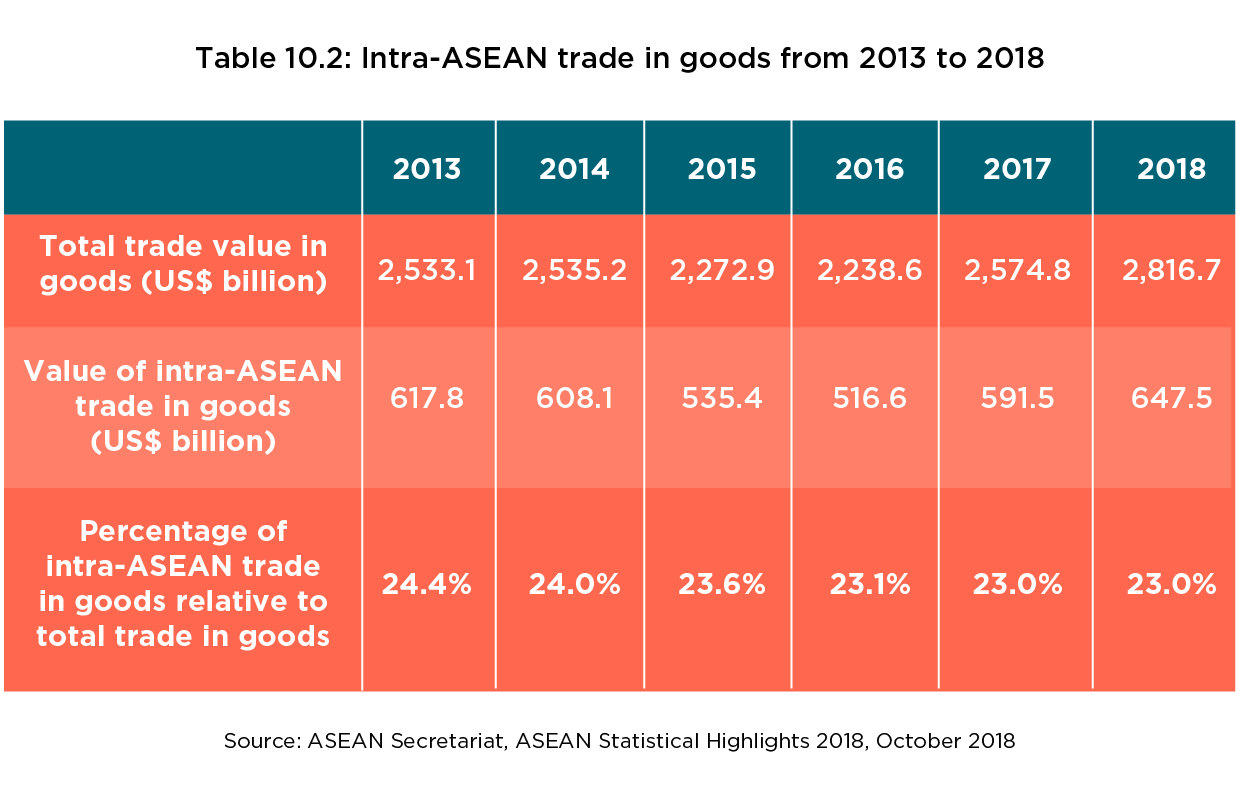

The value of ASEAN’s intra-regional trade in goods has increased by around 25.1% from 2008-2017, reaching almost US$600 billion in 2017.5 However, as a proportion of total merchandise trade, intra-ASEAN merchandise trade flows has remained between 23%-25% between 2013 and 20186 (Table 10.2).

- Thus, despite the progress in tariff reduction and removal, the proportion of intra-ASEAN trade in goods has remained below 25%.7

- The ASEAN Economic Community’s (AEC’s) goal to double intra-ASEAN trade from 2017 to 2025 means that more aggressive measures are needed to boost regional trade. Nonetheless, as alluded to above, it is not just the intra-ASEAN trade value that should be increased but equally important is its relative importance in comparison with extra-ASEAN trade, as reflected in intra-ASEAN trade as a proportion of total trade flows.

c. Role of non-tariff barriers

Analysts have suggested that among others, the proliferation of non-tariff measures (NTMs), which include a mix of import-related and export-related policies, could account for these intra-ASEAN trade patterns.

- According to a 2016 research paper, the number of NTMs in ASEAN had increased from 1,634 measures to 5,975 measures during the period 2000-2015.8 According to the UNCTAD database, the number of NTMs in ASEAN in 2019 was at 9,502 measures.9 This, however, is a stark contrast to the number of NTMs in the ASEAN Integration Report 2019, which stated that as of 24 May 2019, the number is 5,889.10

- Based on both sets of numbers, the bulk of the types of NTMs consist mainly of technical barriers to trade (TBT) and sanitary and phytosanitary (SPS) measures. A more detailed breakdown of NTMs by type based on the ASEAN Integration Report 2019 is as follows: 42.9% of NTMs were technical barriers to trade (TBTs), 32.9% of NTMs were sanitary and phytosanitary (SPS) measures, and 12.9% were export-related measures. Both TBTs and SPS collectively composed 75.8% of total ASEAN NTMs.11

While we recognise that NTMs are not synonymous with non-tariff barriers—and hence, only provides an indicative perspective—what is generally observed and agreed upon, is that significant reduction in these measures could be instrumental in enhancing regional trade by way of reducing trade costs. Tackling SPS measures for instance, would include addressing norms related to discriminatory treatment of certain products, discrepancies in standards across markets and the lack of transparency in assessment procedures.

Factor 3: Intra-ASEAN services trade

Factor 3: Intra-ASEAN services trade

a. Much room for services trade to grow

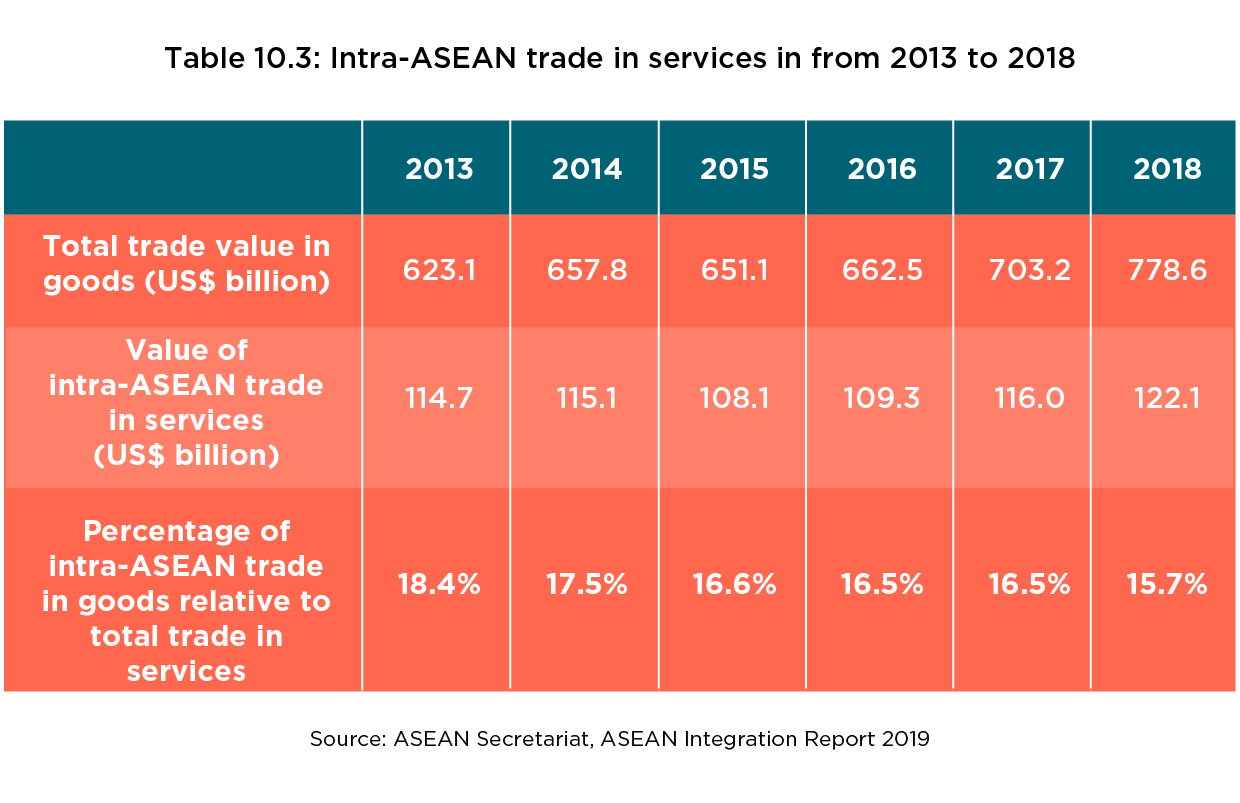

- Intra-ASEAN services trade constituted less than 20% of total services trade between 2013 and 2017, moderated to 16.5% in 2016 and 201712 and decreased slightly to 15.7% in 201813 (Table 10.3).

- There is much room for this segment to grow in tandem with merchandise trade. In 2018, for instance, services trade constituted only around 27.8% of GDP,14 a proportion which was not representative of the fact that the services sector accounted for slightly more than 50% of ASEAN’s economy between 2012 and 2016 and peaked at 53.1% in 201615 (Table 10.4).

b. Role of services trade impediments

ASEAN governments have undertaken several measures to support regional trade in services as reflected in the initiatives related to the ASEAN Framework Agreement on Services (AFAS) and the ASEAN Trade in Services Agreement (ATISA). However, further relaxation of services trade restrictions is clearly required.

- An analysis of historical data has shown that the average Services Trade Restrictions Index (STRI) for the region has been 60% higher than the global average.16

- Existing quantitative measures of impediments to trade services (such as the STRI) have thrown light on the general degree of restrictiveness imposed by the respective ASEAN countries on all trading partners.

- These quantitative measures do not however explain, especially on the basis of proportions (relative importance), why extra-regional trade relationships have remained persistently stronger than intra-regional trade.

Factor 4: Intra-ASEAN FDI

Factor 4: Intra-ASEAN FDI

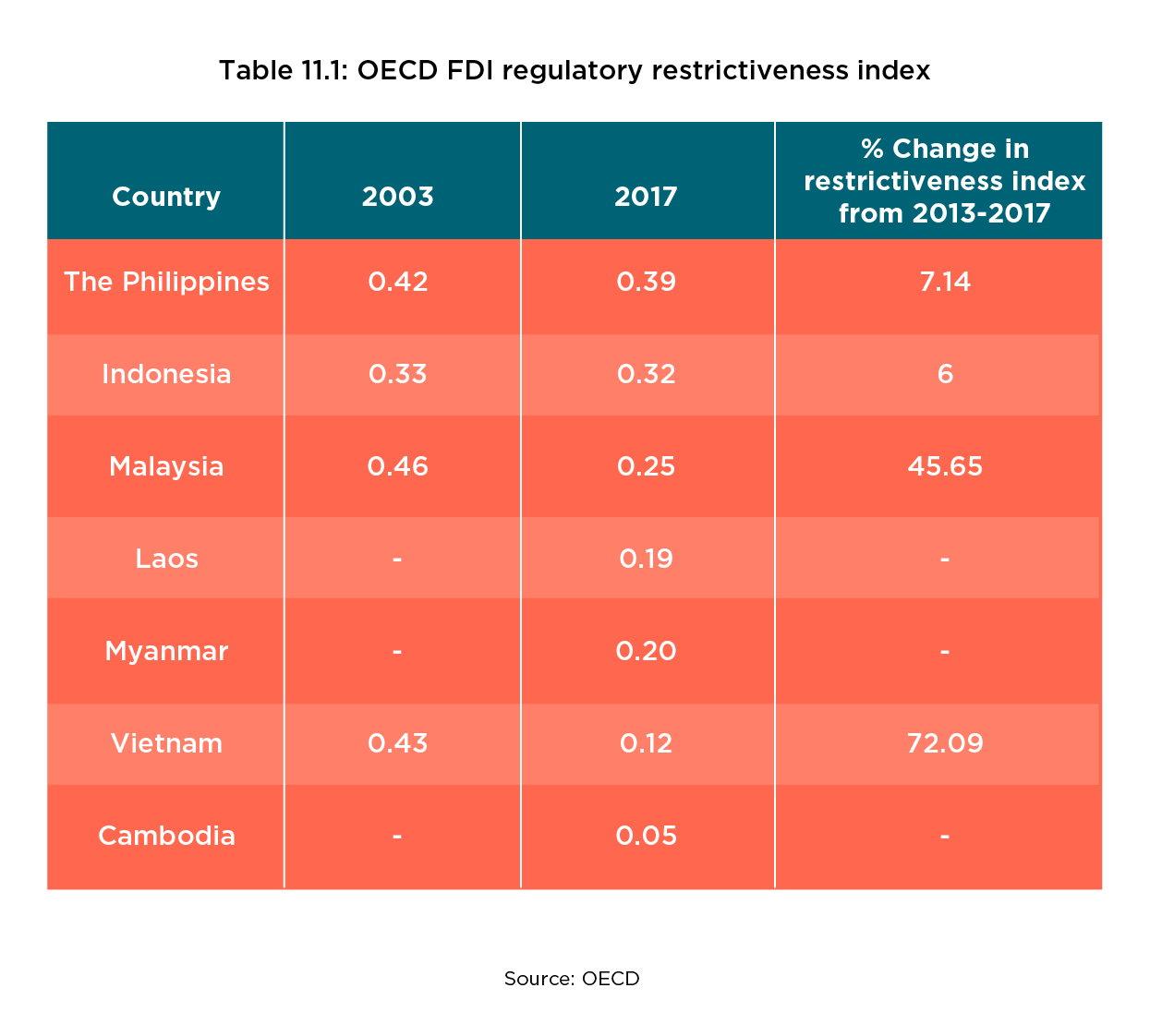

The OECD FDI Regulatory Restrictiveness Index provides insight into the extent of country-level FDI restrictiveness although there were data gaps for certain countries in the year 2003.17 Data shows that FDI regulatory restrictiveness has generally decreased across the board from 2003 to 2017, especially for Vietnam and Malaysia which experienced more than 45% decrease in restrictiveness (Table 11.1).

Although the slight decrease in the Philippines’ score to 0.39 and Indonesia’s score to 0.32 in 2017 (Table 11.1) is a welcome development, the data nonetheless suggests that relative to other countries and regions, the average ASEAN FDI regulatory restrictiveness level of the seven ASEAN countries in 2017 (Table 11.1) is 0.20 which is higher compared to the average FDI restrictiveness for non-OECD countries (0.12)18 and OECD countries (0.07) in the same year.

Significant increase in intra-regional FDI flows

While the FDI restrictiveness levels are still higher for certain ASEAN countries, by global standards, the declining trend in restrictiveness could be one reason behind the increase in regional FDI flows, both extra-regional and intra-regional flows combined.

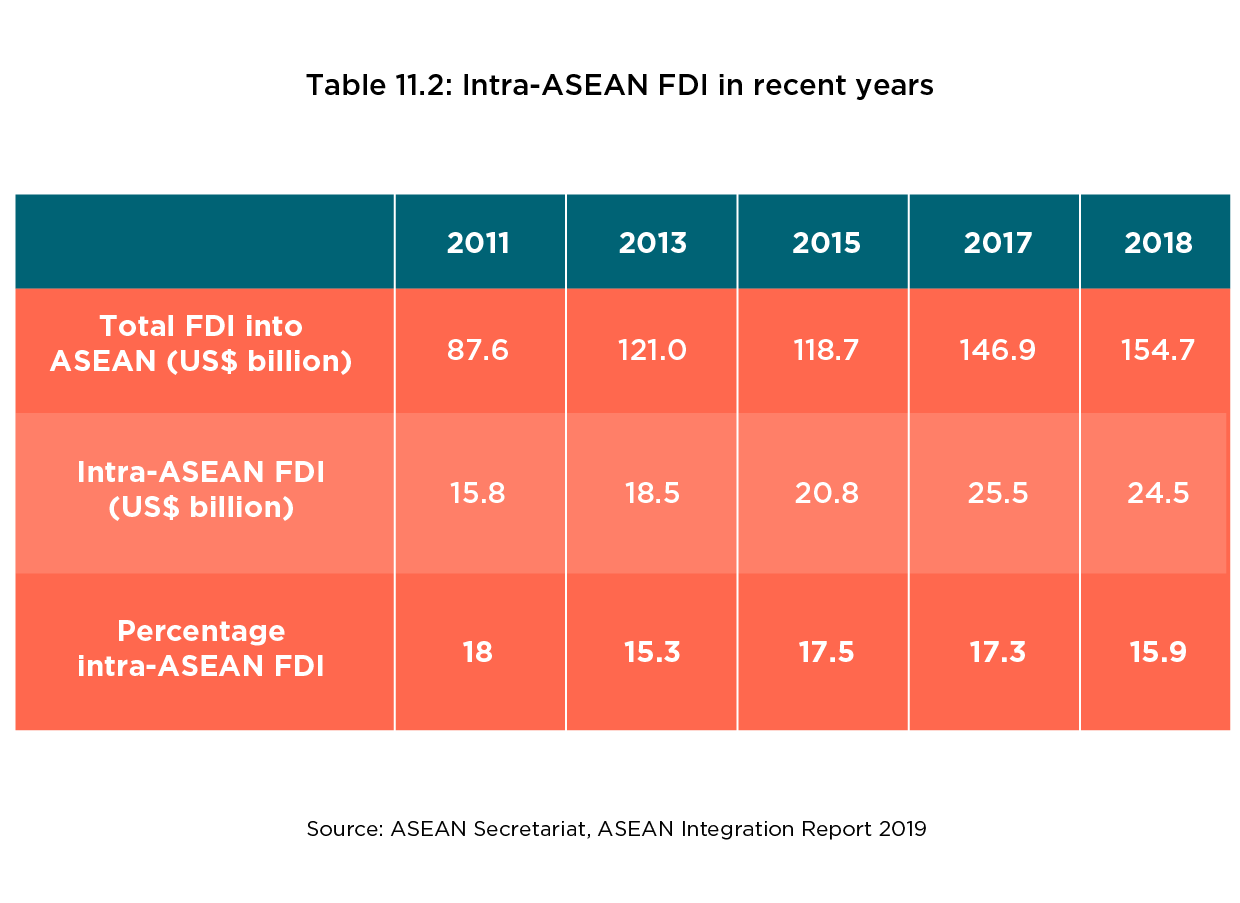

Consistent with this development, the value of intra-regional FDI increased by around 200% from 2008 to 2017.19 Since the 2008 Global Financial Crisis, intra-ASEAN FDI reached more than US$15 billion annually.20

As shown in Table 11.2, intra-ASEAN FDI reached a high of US$25.5 billion (17.3% of total FDI) in 2017.21 The amount fell slightly to US$24.5 billion (15.9% of total FDI) in 201822 (Table 11.2) but has remained the largest source of FDI into the region.23

The three largest sources of intra-regional investments in 2018 were Singapore (68.8%), followed by Thailand (10.4%) and Malaysia (7.2%).24

- These countries collectively provided 86.4% of intra-regional investments in 2018.25

- Indonesia received the largest share of intra-ASEAN investment in 2018 which was measured at US$11.8 billion (48.0% of total intra-ASEAN investment).

- The other three large recipients were Singapore (13.6%), Vietnam (11.4%) and Myanmar (8.4%).26

The proportion of the intra-ASEAN component, however, has generally been unchanged, hovering between 15%-20% of total FDI inflows27< between 2010 and 2018.28<

It remains to be seen if intra-ASEAN FDI can continue to grow to match the proportions observed in other active regional economic groupings. For instance, intra-EU FDI has exceeded extra-EU FDI flows for most of the EU’s investment history.29<

Summary

Despite progress in ASEAN economic cooperation since the creation of the ASEAN Free Trade Area (AFTA) 27 years ago, the relative share of intra-ASEAN trade and FDI flows appear to have not increased in the past decade. Around a quarter of merchandise trade comes from intra-regional merchandise trade and this proportion has been fairly unchanged in 2017 and 2018. While the value of intra-regional FDI inflows has grown significantly, the proportion has remained generally unchanged at less than 20%.30

The following section concludes our 11-part series of the report titled “A Snapshot of ASEAN Economic Growth Progress: Drivers, Vulnerabilities, Prospects and ASEAN Economic Integration”.

Conclusion

The preceding overview of economic progress in ASEAN countries has raised some key points:31

- ASEAN’s economic growth trajectory largely appears to be on track despite challenges imposed by external economic and geopolitical developments and domestic demographic trends.

- The possible derailment from this trajectory is dependent on, among others, increased pressure as a result of trade tensions, the inability to address manpower (productivity, salaries and wages) competitive pressures, as well as physical and technological infrastructure needs.

- At over 90% of GDP, trade is ASEAN’s lifeblood, with merchandise trade being its key component. It is estimated that services trade only constitutes around a quarter of ASEAN’s GDP.

- Though the values have increased—trade has multiplied 2.3 times to US$2.8 trillion in 2018 within a period of 13 years and FDI reached an all-time high of US$154.7 billion in the same year—the intra-ASEAN share has remained relatively low and unchanged, especially in the past few years. Intra-ASEAN merchandise trade constituted 23%-25% of total trade while the intra-regional proportion for FDI was 15%-20% of total flows in the last eight years.

Having very high external dependencies is not necessarily a red flag in a globalised world. Nonetheless, ASEAN needs to be cautious; for example, around 77% of merchandise trade is with extra-regional markets, many of which show high economic correlations with each other. The grave uncertainties around the strategic and economic outcomes arising from the unresolved US-China trade conflict is just one example of this vulnerability.

The test of true resilience, however, does not just derive from ASEAN’s capacity to successfully mount counter-cyclical strategies to withstand economic risks. Longer-term resilience must also effectively ride the vagaries of, as indicated previously, geopolitical dynamics, protectionist-related threats and inter-generational changes brought on by demographic trends and disruptive technologies.

Now more than ever, the region requires ASEAN economic integration to more aggressively deliver on the promise of a single market and production base, and the seamless connectivity of people, capital, goods and services.

The comprehensiveness of the AEC Blueprint/Consolidated Strategic Action Plan (CSAP) 2025 reflects that ASEAN governments recognise that collaborative efforts are required to support domestic capacity-building of respective countries and to strengthen ASEAN’s collective market potential. Through the wide partnerships of private and public sector stakeholders, the AEC Blueprint/CSAP 2025 tackles “sensitive” areas of reform in a more proactive manner—including more purposefully reducing non-tariff measures, simplifying rules of origin, deepening trade facilitation measures, and harmonising standards and regulations—all of which would address some of the challenges highlighted previously.

In order to support the implementation of the AEC 2025, the ASEAN Integration Monitoring Office (AIMO) has formulated a Monitoring and Evaluation Framework that aims to monitor both the outcomes of integration and planned activities in the CSAP. The important work of tracking progress must be supported by all relevant stakeholders in the region. Only then can the multi-sectoral commitment to embark on integration efforts be infused with the necessary momentum. In short, all of ASEAN needs to help fortify the AEC Blueprint/CSAP 2025 with both the commitment and necessary due diligence to ensure that a balance is achieved between an ASEAN-centric development approach with the continued efforts to pursue the necessary extra-regional economic partnerships that have served it well so far.

1 ASEAN-Japan Centre, Global Value Chains in ASEAN – A Regional Perspective (Paper 1 (Revised) January 2019).

2 Ibid

3 PwC, The Future of ASEAN: Time to Act, May 2018.

4 ASEAN, “ASEAN Community Progress Monitoring System 2017 – Tariff Liberalisation,” October 2018.

5 ASEAN Secretariat, ASEAN Statistical Yearbook 2018, December 2018.

6 ASEAN, ASEAN Integration Report 2019, October 2019.

7 Ibid.

8 Ing, Lili Yan, Santiago Fernandez de Cordoba, and Olivier Cadot. “Non-tariff measures in ASEAN.” (2016).

9 United Nations Conference on Trade and Development, TRAINS database, accessed in October, 2019.

10 ASEAN, ASEAN Integration Report 2019, October 2019.

11 Ibid.

12 ASEAN Secretariat, ASEAN Statistical Highlights 2018, October 2018.

13 ASEAN, ASEAN Integration Report 2019, October 2019.

14 ASEAN, ASEAN Key Figures 2019, October 2019.

15 ASEAN Secretariat, ‘ASEAN Services Report 2017: The Evolving Landscape’, August 2017.

16 World Bank Group, Regionalism in Services: A Study of ASEAN (by Gootiiz, B. and Mattoo, A.), November 2015. Note: The Services Trade Restrictiveness Index (STRI) only covers some ASEAN countries and for selected time periods.

17 The FDI Regulatory Restrictiveness Index (FDI Index) measures statutory restrictions on foreign direct investment across 22 economic sectors. Restrictions are evaluated on a 0 (open) to 1 (closed) scale. The overall restrictiveness index is the average of sectoral scores. Data was unavailable for Laos, Myanmar and Cambodia in 2003.

18 OECD, FDI Regulatory Restrictiveness Index, accessed November 2019.

19 ASEAN Secretariat, ASEAN Statistical Highlights 2018.

20 PwC, The Future of ASEAN: Time to Act, May 2018.

21 ASEAN Secretariat, ASEAN Integration Report 2019, October 2019.

22 Ibid.

23 ASEAN Secretariat and UNCTAD, ASEAN Investment Report 2019, October 2019.

24 Calculated based on data from ASEAN Investment Report 2019.

25 Ibid.

26 Ibid.

Note: Collectively, Indonesia, Myanmar and Vietnam received 68% of intra-ASEAN investments in 2018

27 Ibid.

28 The value of FDI flows would have increased in tandem with the growth in total FDI flows.

29 PwC, The Future of ASEAN: Time to Act, May 2018.

30 The FDI Regulatory Restrictiveness Index (FDI Index) measures statutory restrictions on foreign direct investment across 22 economic sectors. Restrictions are evaluated on a 0 (open) to 1 (closed) scale. The overall restrictiveness index is the average of sectoral scores.

31 The estimates are based primarily on 2018 data.

(Note: The term “ASEAN” can refer to either the collection of economies in this region or the intergovernmental institution which was established through the ASEAN Charter of 1967 or both.)

Research Director: Jukhee Hong

Editorial Team: Kwong Mook Shian, Mohd Imran Said Mohd Shamsunahar, Gan Bo Ren, Nor Amirah Mohd Aminuddin, Aznita Ahmad Pharmy, Janet Leong