Economic Snapshot: ASEAN Focus December 2017 | Thailand

Originally published on 20 December 2017

by Michelle Chia & Lim Yee Ping, Economists, CIMB Equities & Economic Research

THAILAND: Don’t dismiss Teflon Thailand

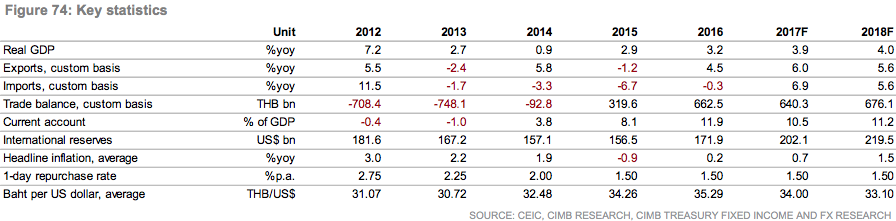

Staying true to its moniker, Thailand has weathered near-term challenges, despite uncertainties clouding the political transition process as well as the year-long mourning period for the late king. A strong uplift in global demand and recovering commodity prices has filtered through to higher exports and tourism receipts. The transition to a self-sustained recovery depends on households and investments playing their part. A turnaround in farm and non-farm incomes portends further improvements in private consumption, while key public investment projects are poised to accelerate. CIMB is forecasting Thailand’s real GDP growth to quicken marginally to 4.0% in 2018 from 3.9% in 2017.

External drivers tip the scales for Thailand in 2017

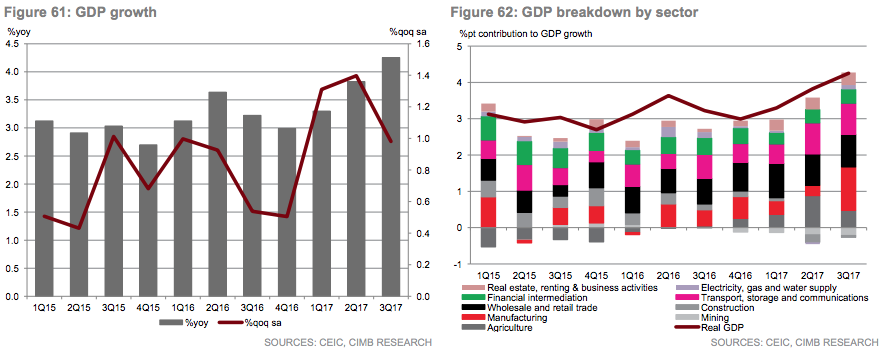

Thailand’s economy recorded growth of 3.8% yoy in 9M17 (+3.2% in 2016), on the back of robust external demand and broadening growth in private consumption, government outlays and investments. Net trade contributions have led the growth performance this year. By extension, export-driven manufacturers have benefited, led by auto and auto parts, electronics and optical equipment, petroleum and petrochemical products, and rubber products – a trend that is expected to persist into 2018 (+2.3% vs. +2.6% in 2017).

Tourism, which accounts for 12% of the economy, has proven a resilient spot for Thailand, even after the limits placed on illegal tours from China in late 2016, the extended military government rule, and the appreciation of the Thai baht. The growth in tourist arrivals from China moderated to 5.3% yoy in 10M17 (+16.6% yoy in 10M16), a steeper slide than the tally for all tourist arrivals (+6.4% yoy in 10M17 vs. +11.3% yoy in 10M16). Visitor arrivals are projected to improve from 35.3m in 2017 to 37.5m in 2018, as tourism activity picks up after the mourning period and during the government’s Amazing Thailand 2018 campaign.

Inflection in household consumption

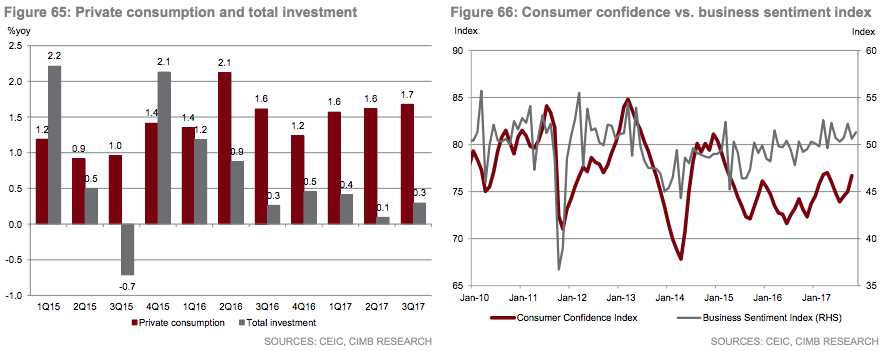

In recent years, private consumption in Thailand has been restrained by high household debt and falling agriculture prices, which impacted farm incomes. Pressure on the latter has eased, with farm incomes rising 9.1% in 10M17 (-0.2% in 10M16), as prices of rubber and palm oil as well as yields from agriculture crops recover after the drought-stricken harvests in 2015-2016. Household debt eased from a peak of 80.4% of GDP in 2015 to 78.4% of GDP in 2Q17, but remains elevated when compared against regional peers. Regulations on consumer loans were tightened in Sep 2017 to limit the growth of unsecured lending by lower-income borrowers, which will help to keep household leverage in check but reduces the consumption appetite amongst leveraged households as they pay down debt.

Nonetheless, expect prospects for private consumption to improve in 2018 (+3.4% vs. +3.3% in 2017) as labour market conditions recover and consumer confidence picks up after the end of the year-long mourning period for the late king. In Aug 2017, the government approved THB41.94bn of aid for 11.7m poor households, who will receive THB200-300 a month to buy subsidised consumer necessities. They will also be eligible for THB1,500 a month in transport subsidies and THB500 for selected public buses and train routes. Additionally, to encourage consumer spending, the government approved a year-end tax deduction of up to THB15,000 (US$453) between 11 Nov and 3 Dec 2017, which it estimates will improve consumption by THB10bn in lieu of THB2bn in tax revenue. In the year ahead, expect growth in government consumption expenditures to accelerate to 3.5% in 2018 from 2.2% in 2017.

Capex plans held back by spare capacity

Business sentiment in Thailand has gradually improved over the last two years as political uncertainty diminishes under the military government. Foreign direct investments (FDI) improved to a net inflow of US$6.0bn in 9M17 (vs. US$0.8bn in 9M16) as outflows of FDI tapered. A pick-up in demand and efforts to improve the investment climate in the country could encourage growth in private investments (+3.8% in 2018 vs. +2.2% in 2017).

The strong upswing in external demand has lent a helping hand to the manufacturing sector, which had been struggling with spare capacity. Capacity utilisation increased from 59.9% in Jan to 63.4% in Sep, before declining to 60.2% in Oct, a transitory dip that attributed to fewer working days and closures during the anniversary commemorations. Expectedly, the export-oriented industries that have enjoyed improving demand also experienced the biggest lifts to capacity utilisation, namely autos (90.0% in Sep), electrical machinery (76.5%), and office machinery (74.2%). On the other hand, expect appetites to take on investments to remain weak in sectors where capacity utilisation remains relatively low, such as tobacco (27.5%), furniture (34.1%) and textiles (43.4%) until demand returns or consolidation occurs.

Taking another crack at public investments

The scheduled rollout of public investment projects was more protracted than expected, resulting in a weakened contribution to GDP growth (-0.2% yoy in 9M17 vs. +9.9% yoy in 2016), due to delays to the pre-approval process, financing and land acquisition. Government officials have indicated confidence that the hold-up is likely to be resolved by next year. Expect a swift remedy in 2018, and project public investments to increase 9.8% in 2018 (vs. +0.1% in 2017). Thailand still has ample fiscal space, with public debt at just 41.8% of GDP in 2017, well below the 60% of GDP debt ceiling set by the Ministry of Finance. The government has set the Fiscal Year (FY) 2018 budget deficit at THB450bn, or 2.6% of GDP.

In addition to accelerating government disbursements, the launch of the THB100bn Thailand Future Fund in 2018 expects to raise THB44bn to fund two expressways. Apart from the key rail, highway, airport and port projects specified under the Transport Infrastructure Development Master Plan 2015-2022, the government also plans to implement investments in the Eastern Economic Corridor (EEC), with the EEC Act that governs its implementation set to be operational by early 2018. In Nov 2017, the Board of Investment of Thailand (BoI) approved the following measures to encourage investments in the EEC: 1) corporate income tax (CIT) exemption for an additional two years, 2) 50% tax deduction for five years for entrepreneurs in special industries and 3) 50% CIT exemption for five more years if entrepreneurs are classified in targeted industries.

External financing conditions remain healthy

On the back of an expansion in the goods and services surplus, expect the current account surplus to expand further from 10.5% of GDP in 2017 to 11.2% of GDP in 2018, which keeps Thailand well buffered from external financing risks. Improvements in the services account surplus and a smaller drag in net foreign direct investment has improved the balance of payments position, and reinforced international reserves by US$28.7bn this year to US$200.5bn.

No rush to hike

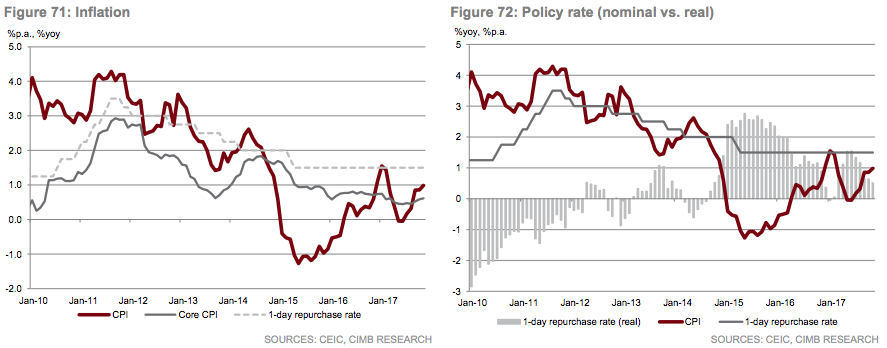

Inflation remains non-threatening and is forecast to rise from 0.8% in 2017 to 1.4% in 2018, after imputing increases in oil prices and excise taxes on selected consumption goods like cigarettes and alcohol. The inflation outlook is expected to settle at the lower end of the Bank of Thailand’s (BOT) 1% to 4% target.

Although BOT has upgraded its assessment of the Thai economy, it does not appear in a hurry to hike the benchmark 1-day repurchase rate, which has been left unchanged since a 25bp cut in Apr 2015. Aside from still-benign inflationary pressure, BOT may opt for patience, casting one eye on indebted households and the other the strength of the Thai baht, which has appreciated 9.8% YTD against the US$ and 3.7% YTD in effective exchange rate terms. Therefore, expect BOT to keep the policy on hold at 1.50% in 2018.

Appendix: Thailand

Disclaimer: All rights reserved. No part of this report may be reprinted or reproduced or utilised in any form or by any electronic, mechanical or other means, now known or hereafter invented, including photocopying or recording, or in any information storage or retrieval system without proper acknowledgement of CIMB ASEAN Research Institute. The views, responsibility for facts and opinions in this publication rests exclusively with the authors and their interpretations do not necessarily reflect the views of CIMB ASEAN Research Institute.

![]()