HIGHLIGHTS

Consumers to reap the benefits of a (likely) people centric budget

- Consumers stand to gain the most from the shift in budget focus to favour boosting household purchasing power during an election year.

- The biggest increases are slated to come from energy subsidies, which benefit households of all segments, and conditional cash transfers to vulnerable households.

- We make no changes to our forecasts for GDP growth (2018F: 5.3%; 2019F: 5.2%) and inflation (2018F: 3.4%; 2019F: 3.7%).

Shifting budget priorities ahead of Presidential Election

As the Presidential Election draws closer, the budget focus has shifted in favour of supporting household purchasing power, diverging from infrastructure development in the first three years of Jokowi’s administration. In fact, the state budget’s priorities took a Uturn as early as 2H17, when the government kept fuel prices unchanged despite a recovery in global oil prices, reversing from earlier moves to follow a more market-based mechanism. More pro-consumer policy doses were injected in 2018, with greater disbursements of targeted cash transfers and food aid, as well as allowances and bonuses for civil servants. These measures will most likely continue in an election year. The 2019 State Budget will be unveiled on 16 August.

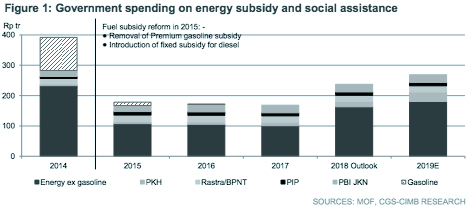

Energy subsidy and social assistance to rise to 5-year high in 2019

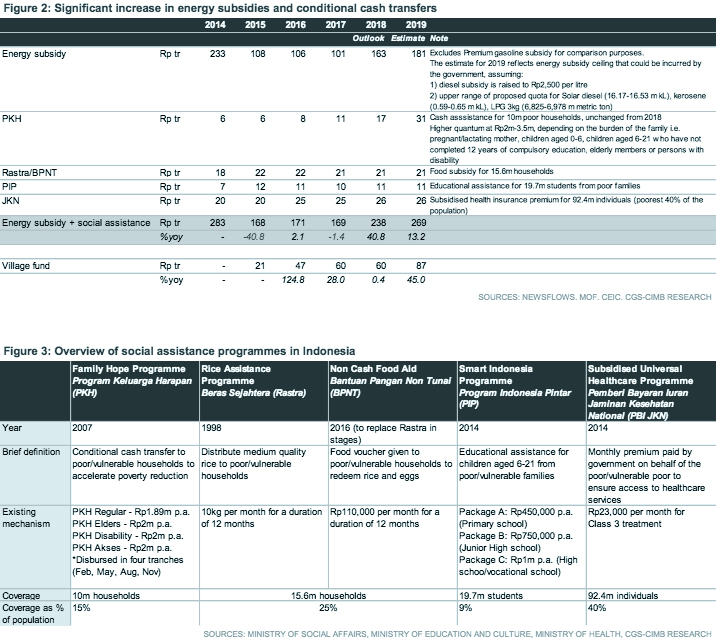

We estimate that government expenditure on energy subsidies and social assistance could increase as much as 13% to Rp269tr in 2019, after a projected 41% increase to Rp238tr in 2018. The bulk of the increase in these two years come from energy subsidies, following the government’s commitment to keep fuel prices unchanged, as well as conditional cash transfers (PKH) to poor and vulnerable households.

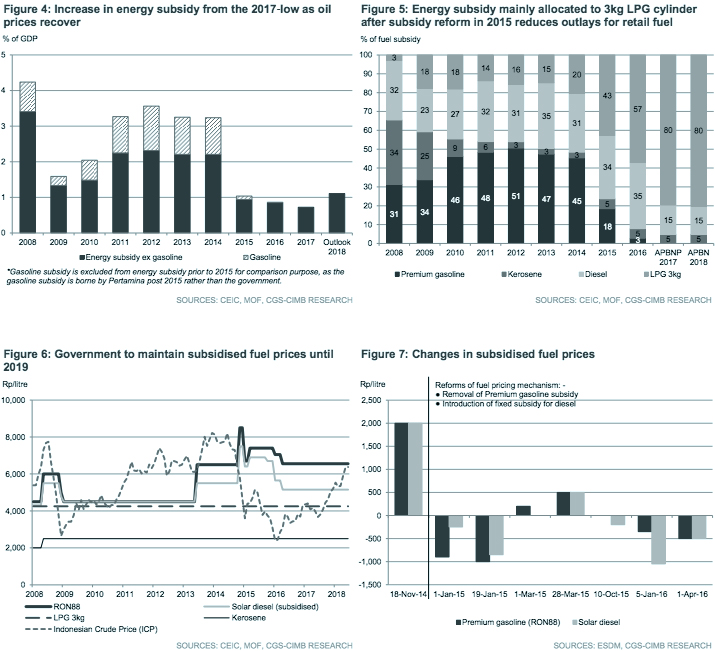

Unchanged fuel and electricity prices to keep inflation rate low

Collectively, fuel and electricity expenditure accounted for a sizeable 8.6% of average monthly expenditure per capita as at September 2017, rising from 7.4% as at September 2016 following electricity tariff hikes in 1H17. We expect the decision to maintain fuel and electricity prices to dampen inflation risks until 2019, implying that the inflation rate is likely to stay within Bank Indonesia’s target range of 2.5-4.5%. We reiterate our average inflation forecast of 3.4% for 2018F and 3.7% for 2019F, respectively.

Higher cash transfers to boost low-income household consumption

Currently, the flat rate cash transfer of Rp1.89m p.a. is equivalent to 83% of the minimum monthly wage in Indonesia, relatively low compared to 120% in Malaysia. Higher allocations to the conditional cash transfer programme (Rp31tr in 2019F vs. Rp17tr in 2018F) through the adoption of a variable rate of cash transfers depending on the burden of low-income family should help boost low-income household consumption.

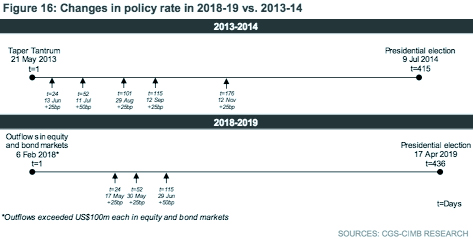

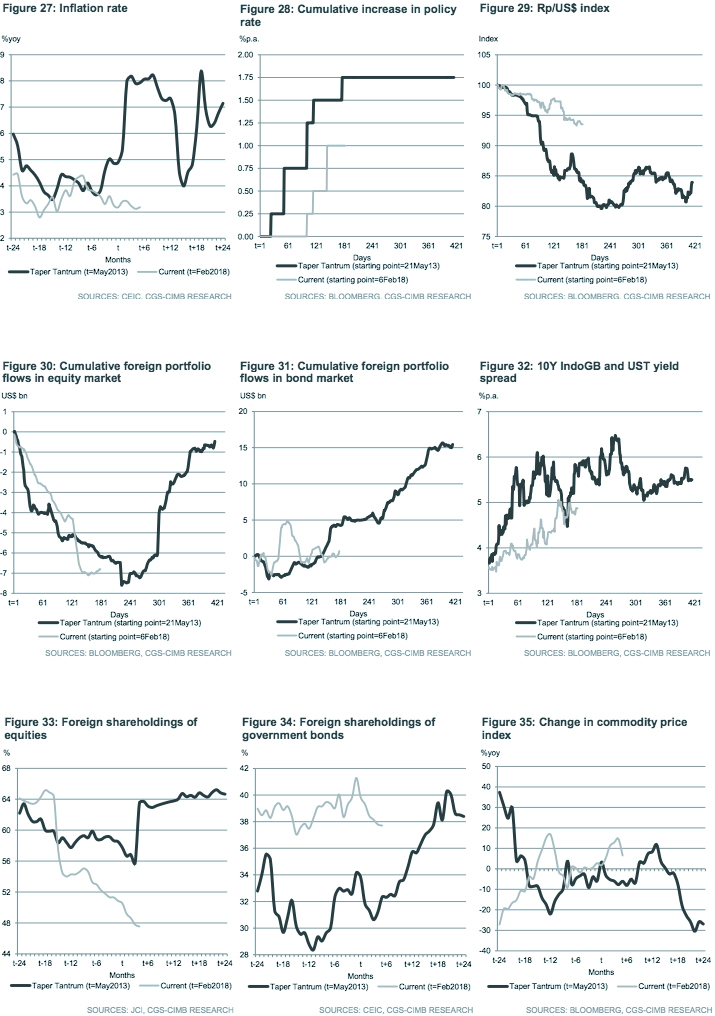

2018-19 vs. 2013-14: no déjà vu?

In addition to a more consumer-centric budget this time around, the recovery in selected commodity prices (such as coal) and easing macroprudential measures in the property sector should help to support the country’s economic growth. This is in stark contrast to 2013-14, when monetary policy tightening by Bank Indonesia (BI) was accompanied by a more stringent macroprudential policy in the property and automotive sectors, as well as upward adjustments in fuel prices. We reiterate our GDP growth forecasts of 5.3% for 2018F and 5.2% for 2019F, respectively.

Consumers to reap the benefits of a (likely) people-centric budget

Shifting budget priorities ahead of Presidential Election

Energy subsidy and social assistance to rise to 5-year high in 2019

As the Presidential Election draws closer, the budget focus has shifted in favour of supporting household purchasing power, diverging from infrastructure development in the first three years of Jokowi’s administration.

We estimate that government expenditure on subsidy and social assistance could increase by as much as 13% to Rp269tr in 2019, after a projected 41% increase to Rp238tr in 2018. The bulk of the increase in these two years come from energy subsidies, following the government’s commitment to keep fuel prices unchanged, as well as conditional cash transfers (PKH) to poor and vulnerable households.

Unchanged fuel and electricity prices to keep inflation rate low

Several changes have been announced to support this pro-consumer policy. They include 1) a price cap on domestic sales of coal to PLN, where coal accounts for about 55% of PLN’s electricity supply costs; 2) a mandate for Pertamina to supply Premium gasoline in Java, Madura, and Bali areas; and 3) a fourfold increase in diesel subsidy from Rp500 per litre to Rp2,000 per litre for the rest of 2018, which is higher than the initial plan of Rp700-1,000 per litre, as well as plans to raise it further to Rp2,500 per litre in 2019.

These changes aim to re-shuffle the subsidy burden between the government, state-owned enterprises (Pertamina and PLN) as well as coal miners. The Ministry of Finance (MOF) revised the allocation for fuel subsidies to a four-year high of Rp163.5tr in 2018, up 73% from Rp94.5tr in the State Budget 2018, after taking into account a higher oil price assumption of US$70 per barrel and a rupiah exchange rate of close to Rp14,000 per US$ (vs. US$48 per barrel and Rp13,400 per US$ under the State Budget 2018).

An overhaul of the fuel subsidy mechanism in 2015 was intended to reduce the massive fuel subsidy spending by linking retail fuel prices to oil price movements in the market. While the government has been quick in passing the savings to households when oil prices were declining in 2015-2016, the subsequent recovery in oil prices has not been followed by a commensurate upward adjustment in pump prices. As a result, Premium gasoline and Solar diesel pump prices were last adjusted downwards in April 2016, when oil prices were still declining. At Rp6,450 per litre and Rp5,150 per litre respectively, current Premium gasoline and Solar diesel pump prices are 31-49% below market prices, based on our estimates.

The downward adjustments of subsidised fuel prices in 2015-16 resulted in falling fuel expenditure from 5.1% of average monthly expenditure per capita as at March 2015 to a low of 3.9% as at September 2016, before rising to 4.5% as at September 2017. On the other hand, the increase in electricity tariffs in 1H17 lifted electricity expenditure by 32.9% yoy and raised its share of overall expenditure by 0.6% pt yoy to 3.0% as at September 2017. Collectively, fuel and electricity expenditure accounted for a sizeable 8.6% of average monthly expenditure per capita as at September 2017, compared to 7.4% as at September 2016. Unchanged fuel and electricity prices significantly remove inflation risk (and hence improve the cost of living) until 2019, implying that the inflation rate is likely to stay within BI’s target range of 2.5-4.5%. We reiterate our inflation forecast of 3.4% and 3.7% for 2018 and 2019, respectively.

Higher cash transfer to boost low-income household consumption

The budget allocation for Family Hope Programme (PKH) could be raised by as much as 79% yoy to Rp31tr in 2019 (vs. Rp17tr in 2018) in a bid to support consumption among the low-income households. Studies have shown that the Family Hope Programme (PKH), launched by the government in 2007, plays a significant role in reducing poverty. The country’s poverty rate declined to 9.82% (25.95m people) as of Mar 2018, the first single-digit rate since the Asian Financial Crisis (AFC).

According to the Ministry of Social Affairs, the number of beneficiary families is expected to remain at 10m in 2019, but the quantum of cash transfers will be adjusted higher to Rp2m-3.5m per annum. The quantum will vary according to the burden of the family, after taking into account non-income indicators such as pregnant/lactating mother, the number of children aged 0-6, children aged 6-21 who have not completed 12 years of compulsory education, elderly family members, as well as persons with disability. The approach differs from other countries in the region (such as Malaysia and Singapore) which mainly utilise income indicators like household income, as the verification of household income can be difficult in Indonesia given the prevalence of the informal sector. Currently, the flat cash transfer of Rp1.89m p.a. is equivalent to 83% of minimum monthly wage in Indonesia. Raising the quantum to Rp2m-3.5m per

annum translates to 88-154% of minimum monthly wage, on par with the 120% in Malaysia.

2018-19 vs. 2013-14: no déjà vu?

Improved fiscal buffers since its flagship subsidy reform in 2015 (at the expense of SOEs) have enabled the government to raise its subsidy and social assistance spending to mitigate the impact of rising interest rates in response to external risks, just as the Presidential Election draws closer in 2019. This is in stark contrast to 2013-14, when monetary policy tightening by Bank Indonesia was accompanied by a more stringent macroprudential policy in the property and automotive sectors, as well as upward adjustment in fuel prices to rectify a worsening twin deficit position, as unsustainable subsidy bills heightened the risks of the fiscal deficit breaching the 3% constitutional limit. In both cases, an externally-driven capital rout, rupiah weakness and eventually tighter monetary policy started around 14 months before the Presidential Election.

In addition to a more consumer-centric budget this time around, the recovery in selected commodity prices (such as coal) and easing macroprudential measures in the property sector should help to support the country’s economic growth. The government’s plan to expand the B20 biodiesel usage to all diesel-engine vehicles in Sep, if successfully implemented, should help lift demand for palm oil and work to boost CPO prices, hence boosting household incomes in the rural areas. Currently, the B20 biodiesel is only mandatory in the public service obligation (PSO) segment i.e. subsidised diesel.

Household consumption growth on equipment and leisure has steadily improved from a trough of 4.1% yoy in 1Q17 to a 3.5-year high of 4.8% yoy in 2Q18, whereas consumption growth on apparels, footwear, and maintenance was stronger at 4.5% yoy in 1H18 compared to an average expansion pace of 3.2% yoy in 2016-2017. Meanwhile, F&B consumption growth was little changed, expanding in the range of 5.1-5.4% yoy in the past three years, hinting at a preference towards discretionary spending relative to staple consumption as income improves and inflation remains stable. We reiterate our GDP growth forecasts of 5.3% for 2018F and 5.2% for 2019F, respectively.

Originally published by CIMB Research and Economics on 08 August 2018.