Malaysia: June 2018 trade

HIGHLIGHTS

June 2018 trade

- Trade surplus surprised on the downside on strong acceleration in gross import growth, and weaker-than-expected expansion in gross exports.

- Taxable goods and services shrink from 60% of CPI basket under GST to 38%.

- We expect 2Q18 GDP growth to ease further to 5.2% due to stronger pick-up in import volume.

- Regional trade performance in 2H18 will be key to watch out for with the start of US-China tariffs in July and companies mulling factory relocation out of China.

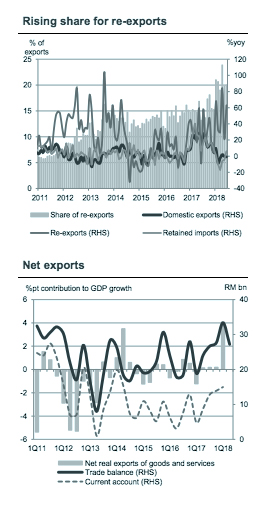

Growth in imports outperformed exports for the first time in 2018

Trade surplus narrowed surprisingly to a 13-month low of RM6.0bn in June (CIMB: RM11.1bn, Bloomberg consensus: RM9.3bn; RM8.1bn in May), as gross imports outperformed gross exports for the first time this year. Import growth quickened to +14.9% yoy (CIMB: +7.1% yoy, Bloomberg consensus: +15.3% yoy; May: +0.1% yoy), double the +7.6% yoy pace for gross exports (CIMB: +7.8% yoy, Bloomberg consensus: +10.3% yoy; May: +3.4% yoy). Re-exports have been the key driver of trade performance in 2018, without which the performance of domestic exports (-0.8% yoy in June vs. -0.3% yoy in May) and retained imports (+6.2% yoy vs. -4.6% yoy in May) is more subdued.

Moderating O&G exports the key drag on export performance…

O&G export growth (+7.6% yoy in June vs. +26.6% yoy in May) was dragged by 31.2% yoy decline in LNG exports (+61.0% yoy in May) due to technical issues at Petronas’s LNG facility in Bintulu. Shipments of crude petroleum and refined petroleum products collectively rose 35.4% yoy (+18.9% yoy in May) on the back of higher oil prices. We expect O&G exports to pick up in the coming months on 1) the commencement of LNG deliveries to a Japanese company under a 10-year agreement in August, and 2) the resumption of Bentara crude exports after field upgrade which bumps up production from 50,000bpd in 2015 to 150,000bpd currently.

… but manufacturing exports came to rescue

Stronger growth in key industries helped to lift manufacturing export growth (+12.7% yoy in June vs. +3.2% yoy in May): E&E (+6.9% yoy vs. +2.1% yoy in May), chemicals (+31.6% yoy vs. +14.6% yoy in May), machinery, appliances and parts (+10.4% yoy vs. – 12.2% yoy in May), as well as optical and scientific equipment (+30.9% yoy vs. +13.4% yoy in May).

Broad recovery in end-use imports after the tumble in May

End-use import demand improved broadly on the back of festive celebrations and zerorated Goods and Services Tax (GST). The growth was led by capital goods (+14.1% yoy vs. -0.5% yoy in May), consumption goods (+4.9% yoy vs. -10.2% yoy in May), and intermediate goods (+3.1% yoy vs. -5.3% yoy in May).

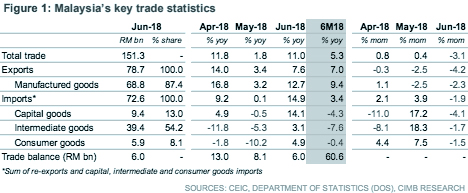

Real GDP likely received less support from net exports in 2Q18

The positive contribution of net exports to GDP growth likely eased in 2Q18 (+4.0% pts in 1Q18) as the increase in 2Q18 trade surplus (+12.9% yoy to RM27.2bn) paled in comparison to 1Q18 (+76.8% yoy to RM33.4bn). We expect GDP growth to ease further to 5.2% (+5.4% yoy in 1Q18). National accounts and balance of payments data for 2Q18 are due to be released on 16 August.

No de-escalation in US-China trade tension yet

Global trade tensions are heating up with the US now studying the possibility of raising the proposed import tariffs on US$200bn worth of Chinese goods from 10% to 25%. Given the start of US and China tariffs on 6 July, we are watching out for July’s regional trade performance to ascertain the degree of trade disruption or whether there are potential winners from the displacement of demand in the targeted goods.

Originally published by CIMB Research and Economics on 3 August 2018.