Indonesia: 2Q18 GDP growth: Better-than-expected

HIGHLIGHTS

2Q18 GDP growth: Better-than-expected

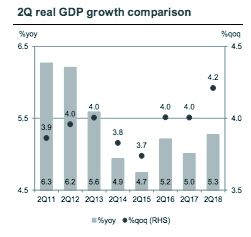

- 2Q18 GDP came in above expectations at 5.3% yoy, the strongest pace since 4Q13.

- Seasonal factors i.e. delay in harvest season to 2Q18 and the Eid al-Fitr celebrations, as well as regional elections contributed to higher economic growth in 2Q18.

- Stable inflation rate and higher income through 13th month salaries and conditional cash transfers helped to lift household consumption during the Eid al-Fitr celebrations.

- We reiterate our GDP growth forecast of 5.3% for 2018 and 5.2% for 2019, respectively (+5.1% yoy in 2017).

Strongest pace of expansion since 2013

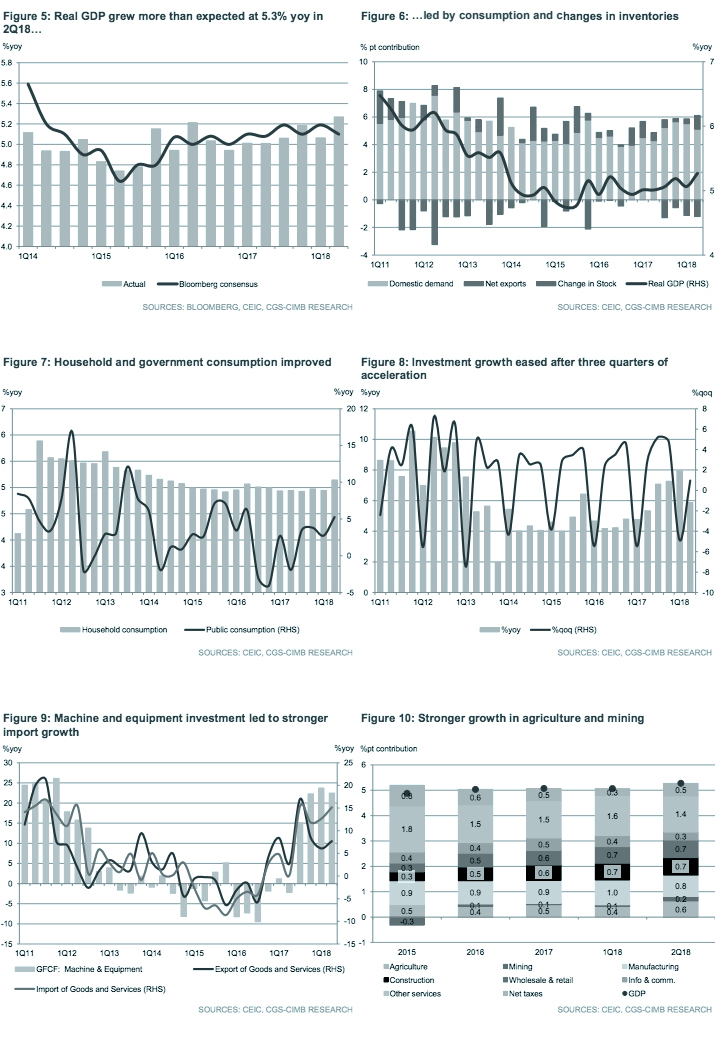

2Q18 real GDP growth quickened more than expected to a 4.5-year high of 5.3% yoy (CIMB: +5.2% yoy; Bloomberg median consensus: +5.1% yoy; 1Q18: +5.1% yoy). On a quarterly basis, GDP grew 4.2% qoq (-0.4% qoq in 1Q18), compared to an average expansion rate of 3.9% in the corresponding quarter in 2011-2017.

Seasonality at play

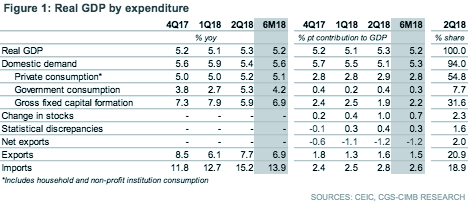

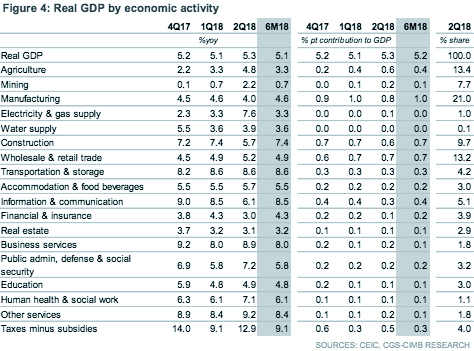

Seasonality could be at play in the latest GDP reading. First of all, a late harvest season lifted agriculture output growth from +3.3% yoy in 1Q18 to +4.8% yoy in 2Q18. Secondly, we think the long festive holiday in Jun may have affected activities in the manufacturing (+4.0% yoy vs. +4.6% yoy in 1Q18), construction (+5.7% yoy vs. +7.4% yoy in 1Q18), and financial & insurance (+3.0% yoy vs. +4.3% yoy in 1Q18) industries, all of which saw moderation in growth rates. Thirdly, the Eid al-Fitr celebration and regional elections spurred private consumption (+5.2% yoy in 2Q18 vs. +5.0% yoy in 1Q18), which in turn lifted the wholesale and retail trade, F&B, as well as transport sectors.

Private consumption growth at a four-year high

By expenditure, the key surprise came from the stronger contribution of inventory accumulation to GDP growth (+1.0% pt in 2Q18 vs. +0.4% pt in 1Q18), which may be driven by businesses stockpiling in anticipation of higher costs due to rupiah weakness, a trend that is unlikely to sustain towards the end of the year. On a positive note, household spending on F&B, equipment, transport & communication as well as restaurant & hotel was stronger during the quarter, whereas non-profit institution consumption was lifted by regional election spending. The recovery in household consumption was supported by a stable inflation rate and improved purchasing power following the 13th month salaries and allowances to civil servants, as well as conditional cash transfers from the government.

Investment growth takes a backseat after three quarters of acceleration

Government spending growth doubled to 5.3% yoy (+2.7% yoy in 1Q18) on higher social assistance expenditure and the low base effect last year, when the disbursement of 13th month salary to civil servants was delayed to 3Q17. Investment growth eased to 5.9% yoy in 2Q18 after three quarters of acceleration beyond 7% yoy, on the back of slower growth in buildings & structures, vehicles and other equipment. However, outlays on machine & equipment remained strong (+22.7% yoy vs. +23.5% yoy in 1Q18), in line with the delivery of train sets for infrastructure projects which also spurred import expansion.

No change to our GDP growth forecast

Real GDP grew 5.2% yoy in 1H18 (+5.1% yoy in 4Q17). We expect economic activity to improve further in 2H18, supported by 1) 18th Asian Games from 18 Aug to 2 Sep; 2) annual IMF-World Bank meeting in Bali in Oct; and 3) low and stable inflation rate until 2019. Hence, we reiterate our GDP growth forecast of 5.3% for 2018 and 5.2% for 2019, respectively. Key downside risks include a tighter monetary policy by Bank Indonesia (BI) which could dampen consumption desire.

Household consumption expanded 5.1% yoy in 2Q18, the fastest pace since 2Q14, as seasonal festivities that were accompanied by the long holiday, 13th month salary and allowances as well as low inflation boosted spending on F&B, equipment, transport & communication as well as restaurant & hotel, whereas regional elections raised non-profit institution consumption growth. The surge in government consumption was partly lifted by the low base effect last year, when the disbursement of the 13th month salary to civil servants was delayed.

Investment growth eased to 5.9% yoy in 2Q18 after three quarters of acceleration beyond 7% yoy. Outlays were weaker in buildings & structures, in line with weaker construction growth during the quarter. Capital expenditure on machine & equipment remained resilient (+22.5% yoy in 2Q18 vs. +23.7% yoy in 1Q18).

A late harvest season lifted agriculture growth to +4.8% yoy from +3.3% yoy in 1Q18. Mining activity was supported by O&G and metal ores on the back of rising global commodity prices. The long holiday in Jun contributed to slower expansion in manufacturing, construction, financial & insurance industries. Stronger consumption and festive celebration lifted the output growth in wholesale and retail trade, accommodation and food & beverage, as well as transport sectors.

Originally published by CIMB Research and Economics on 06 August 2018.