HIGHLIGHTS

No revision to State Budget 2018 (APBN 2018)

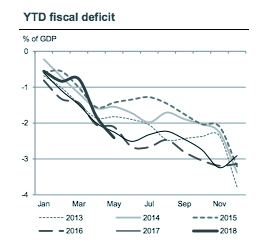

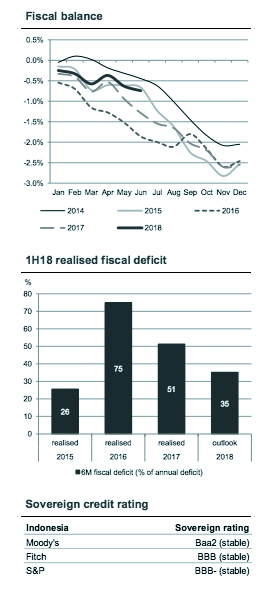

- With 1H18 fiscal deficit remaining healthy at -0.75% of GDP (vs. full-year target of 2.19% of GDP), the government has decided not to revise its State Budget 2018.

- Redirecting additional revenue to fund higher energy subsidy and social assistance implies current account deficit (CAD) remains a risk to rupiah and monetary policy.

- No change to our 2018 forecasts for inflation (+3.4%) and GDP growth (+5.3%).

Fiscal deficit at -0.75% of GDP in 1H18

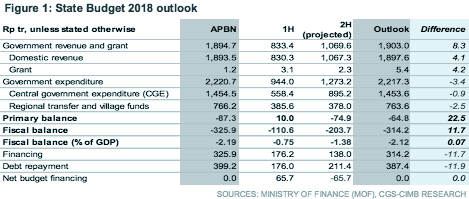

1H18 fiscal deficit came in at Rp111tr, or -0.75% of GDP, the smallest level in three years, as a result of stronger growth in government revenue and grant (Rp833tr, 44% of APBN, +16% yoy) relative to government expenditure (Rp944tr, 43% of APBN, +6% yoy). Given the healthy deficit position, government decided not to revise the State Budget 2018, although its estimates on macroeconomic assumptions have changed.

Outlook on macroeconomic assumptions

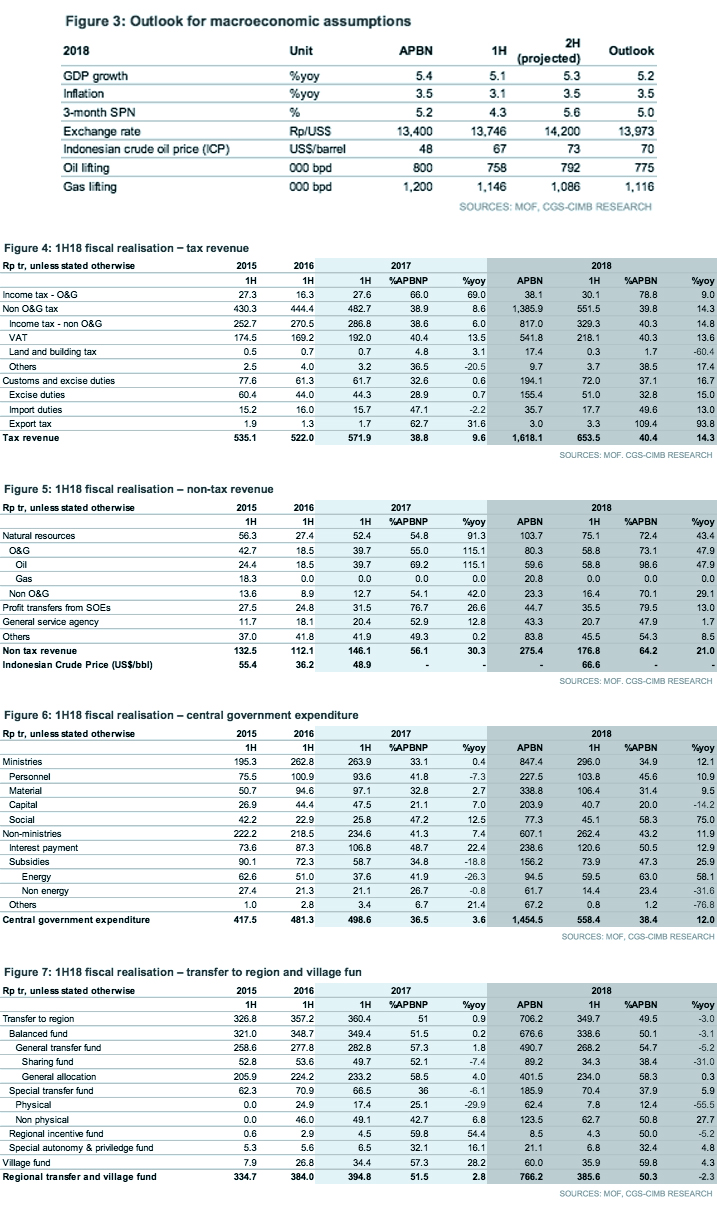

The government now expects GDP growth to come in at 5.2% in 2018 (vs. 5.4% in APBN), based on an oil price assumption of US$70 per barrel (vs. US$48 per barrel in APBN) and an exchange rate close to Rp14,000 per US$ (vs. Rp13,400 per US$ in APBN). The inflation outlook remains at 3.5% as prices remained under control in 1H18.

Revenue boosted by rising commodity prices and trade activity

Higher-than-expected commodity prices, in particular oil and coal, raised resource-related revenue collection in 1H18, such as O&G income tax (Rp30tr, 79% of APBN, +9%) and natural resources receipts (Rp75tr, 72% of APBN, +43%). Stronger trade activity, especially import growth, lifted import duties (Rp18tr, 50% of APBN, +13% yoy) and, partly, VAT (Rp218tr, 40% of APBN, +14% yoy).

Higher energy subsidy and social assistance…

The revenue windfall was redirected to fund higher energy subsidy (Rp60tr, 63% of APBN, +58% yoy) and social assistance (Rp45tr, 58% of APBN, +75% yoy), which collectively accounted for ~19% of central government expenditure. Capital spending took a backseat (Rp41tr, 20% of APBN, -14% yoy). To maintain subsidised fuel prices at current levels until 2019 and alleviate subsidy burden on Pertamina, the government announced in June that diesel subsidy would be raised from Rp500 per litre to Rp2,000 per litre. Taking into account the impact of higher oil prices on LPG subsidy, as well as higher allocation for electricity subsidy, the Ministry of Finance (MOF) projects energy subsidies to go up to Rp164tr in 2018, Rp69tr higher than APBN 2018.

…to support household purchasing power

The subsidy allocation is likely to remain elevated, as there are plans to raise diesel subsidy further to Rp2,500 per litre in 2019. We are not overly concerned about the government’s ability to absorb the additional energy subsidy, given that it could partly be compensated by higher O&G revenue, as we have highlighted in our previous report. The cumulative O&G fiscal balance (O&G revenue less energy subsidy) increased to Rp29tr in 1H18 compared to Rp14tr in 3M18.

No change to our inflation and GDP growth forecast

Channeling extra revenue to finance government spending, rather than lowering fiscal deficit, may keep pressure on the current account deficit (CAD) position; hence, we expect currency or monetary policy tightening risks to persist until 2019. As fiscal focus is diverted towards supporting household purchasing power from infrastructure development previously, we expect consumption growth to improve in 2H18, but investment growth could still be backed by ongoing infrastructure projects. We reiterate our inflation forecast of +3.4% and GDP growth projection of +5.3% for 2018.

Originally published by CIMB Research and Economics on 23 July 2018.

(Interview starts at time code 1:20:18)

(Interview starts at time code 1:20:18)