Thailand: Macro snapshot

HIGHLIGHTS

Macro snapshot

- Despite strong current account gains due to healthier net inflows in the services and income accounts in June, overall BOP weakened due to greater financial outflows.

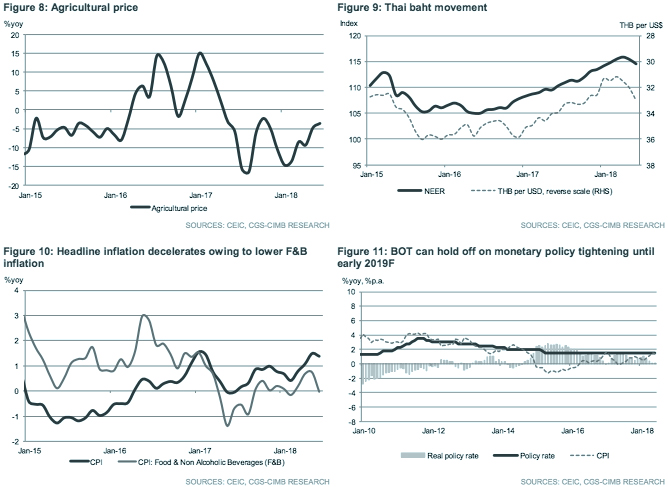

- Farm incomes grew at a slower pace in June due to contraction in agricultural prices and lower agricultural production.

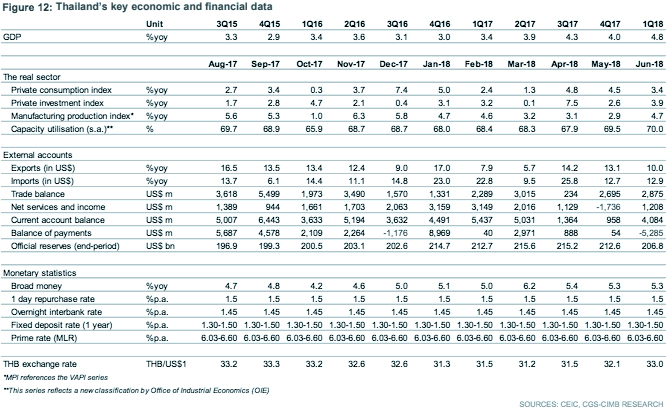

- With June’s inflation at the low end of BOT’s target range, it can afford to hold off monetary policy tightening until early 2019F, in our view.

- We expect the policy rate to remain at 1.50% through end-2018F.

Exports moderating but manufacturing sector is improving

Export growth softened in June (+10.0% yoy vs. +13.1% yoy in May), mainly due to moderation in automotive shipments from an elevated level (+7.0% yoy vs. +19.6% yoy in May). Conversely, import growth strengthened slightly to 12.9% yoy in June (+12.7% yoy in May), primarily supported by fuel imports (+62.5% yoy vs. +26.2% yoy in May). Manufacturing activity picked up, with the Value Production Index (VAPI) rising 4.7% yoy (+2.9% yoy in May), buoyed by food & beverages, rubbers & plastics as well as cement & construction. Seasonally-adjusted capacity utilisation in the manufacturing sector also improved to 70.0% in June from 69.5% in May.

Current account thrives but financial outflows weaken BOP

Thailand’s current account improved significantly in June, registering a surplus of US$4.1bn (+US$1.0bn in May) on the back of higher net inflows from services and income accounts (+US$1.2bn vs. -US$1.7bn in May). Tourist arrivals rose 11.6% yoy in June to 3.0m. However, the nation’s financial account worsened to a deficit of US$7.0bn (+US$0.1bn in May) due to net outflows by Thai equity portfolio investors and ‘other investments’, resulting in a deterioration of the overall balance of payment (BOP) position (-US$5.3bn vs. +US$0.1bn in May).

Farm incomes to watch out for given the heavy downpours

Nominal farm incomes rose at a slower pace in June (+4.3% yoy vs. +8.0% yoy in May), dragged down by the persistent weakness in agricultural prices (-3.6% yoy vs. -4.8% yoy in May) and the slowdown in agricultural production growth (+8.2% yoy vs. +13.5% yoy in May). While the peak harvest season remains a few months away, the country’s provinces have been warned to brace for heavy downpours and flood risks.

Courting investments in the EEC

Thailand recently sought Chinese investment via the Belt and Road Initiative to help fund a five-year development plan worth THB1.7tr in the Eastern Economic Corridor (EEC). In 1Q18, the value of foreign direct investment applications from China approved by the country soared 1,482.2% yoy to THB14.3bn. Another initiative was signed by Thailand and the Japanese prefecture of Mie to establish the Mie-Thai agro-industrial cooperation centre at the EEC of Innovation (EECi) in Rayong, focusing on advanced food and food processing.

Policy rate to hold as inflation remains at low-end of target range

The Bank of Thailand’s (BOT) Monetary Policy Committee (MPC) voted 5-1 to leave the policy rate unchanged at its MPC meeting on 20 June, when the committee had its first extensive discussion on the conditions and timing for monetary policy normalisation. Inflation decelerated slightly in June (+1.4% yoy vs. +1.5% yoy in May), primarily owing to lower food inflation. Yet, it remains at the low end of BOT’s target range of 1-4%, suggesting that the central bank can hold off on monetary policy tightening until early 2019F. We reiterate our forecast that the policy rate will remain at 1.50% through to the end of 2018F.

Originally published by CIMB Research and Economics on 31 July 2018.