Singapore: June industrial production

HIGHLIGHTS

June industrial production

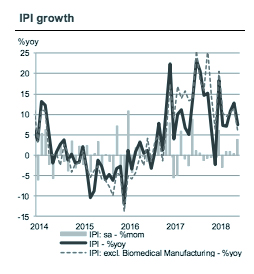

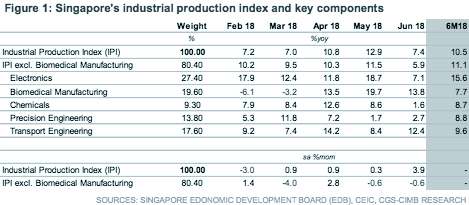

- IPI expanded at a slower pace of 7.4% yoy in June, due to subdued growth in the electronics, chemicals and biomedical clusters.

- Cumulative manufacturing growth (+10.2% yoy in April-June vs. +11.8% yoy in April May), suggests minor tweaks to the advanced GDP growth of 3.8% yoy in 2Q18.

- While external developments have not significantly dented the manufacturing sector, global trade tensions remain a risk to the medium-term outlook.

Slower IPI expansion, but ahead of forecasts

The industrial production index (IPI) expanded by a slower pace of 7.4% yoy in June, ahead of expectations (CIMB: +5.4% yoy, Bloomberg consensus: +3.3% yoy), and following an upward revision to growth in May of 12.9% yoy. Manufacturing activity excluding the volatile biomedical sector mirrored the headline trend, growing at a slower pace of 5.9% yoy in Jun (+11.5% yoy in May). On a seasonally-adjusted basis, the IPI expanded 3.9% mom (+0.3% mom in May).

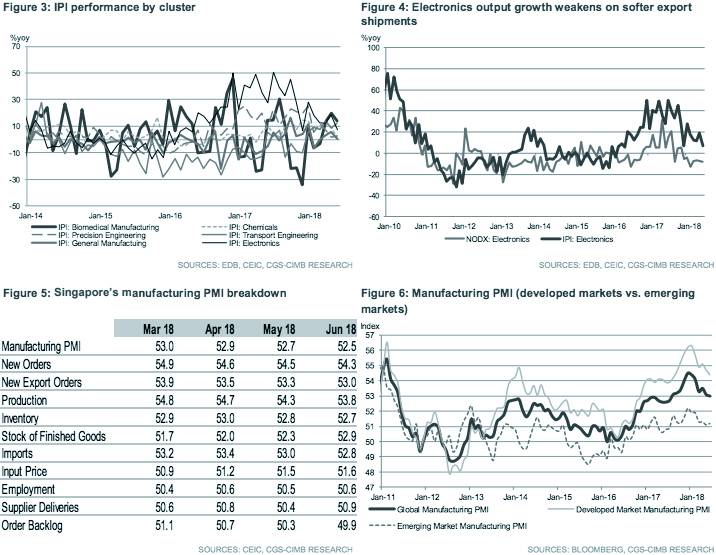

Electronics output growth weakens on softer export shipments

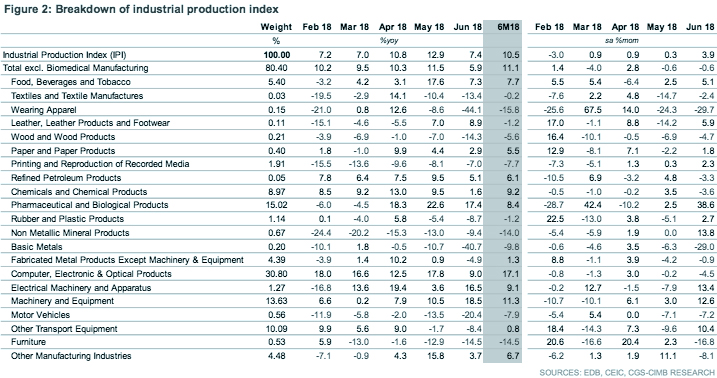

Electronics output growth moderated significantly to 7.1% yoy in June (+18.7% yoy in May), amid broader demand weakness for Singapore’s electronics exports (-7.9% yoy in June). Weighing on the sector were subdued semiconductor output growth (+10.2% yoy vs. +29.0% yoy in May), declines in the computer peripherals (-10.1% yoy vs. -12.0% yoy in May) and data storage segments (-9.9% yoy vs. -2.4% yoy in May). A pick-up in consumer electronics (+5.4% yoy vs. -24.6% yoy in May) and electronic modules output (+9.2% yoy vs. -10.9% yoy in May) were insufficient to counter wavering demand elsewhere.

Chemicals sector expansion more muted in June

Expansion in the chemicals sector lost pace in Jun (+1.6% yoy vs. +8.6% yoy in May) due to slower demand growth for petrochemicals and petroleum. The specialty chemicals segment continued to contract by 2.6% yoy in Jun (-1.2% yoy in May) and production of ‘other chemicals’ plummeted by 6.2% yoy (+11.9% yoy in May). However, transport engineering recorded robust growth (+12.4% yoy vs. +8.4% yoy in May), primarily led by the marine & offshore engineering segment. Furthermore, precision engineering also grew by 2.7% yoy in June (+1.7% yoy in May), helped by the precision modules & components segment.

Biomedical sector contribution moderates

The prognosis for the biomedical manufacturing cluster was less rosy in June (+13.8% yoy vs. +19.7% yoy in May) due to more subdued increases of pharmaceutical drugs production (+17.4% yoy vs. +22.6% yoy in May). The medical technology segment also experienced toned down gains of 1.9% yoy (+13.1% yoy in May).

Manufacturing outlook still clouded by global trade developments

Growth in the manufacturing sector broadly held up last quarter (+10.2% yoy in April – June vs. +11.8% yoy in April – May), suggesting only minor tweaks to the advanced GDP growth reading of 3.8% yoy in 2Q18, when the revised reading is released in Aug. While external risks have yet to significantly dent Singapore’s near-term manufacturing outlook beyond the anticipated cyclical slowdown in demand, trade relations between the US and China remain uncomfortably tense, particularly as the US prepares to raise the ante with at least US$400bn of additional tariffs on Chinese exports to the US.

Originally published by CIMB Research and Economics on 26 July 2018.