Singapore: 2Q18 GDP (revised)

HIGHLIGHTS

2Q18 GDP (revised)

- The revised 2Q18 GDP data was marginally higher at 3.9% yoy on improved growth in the export-oriented manufacturing sector.

- Domestic demand strengthened on account of higher capex in transport equipment and stable consumer spending.

- We reaffirm our annual GDP forecast of 3.2% in 2018, which falls within the official MTI forecast range of 2.5% to 3.5%.

- Uneven gains in domestically-oriented services sector and risks to the external outlook suggest that MAS will maintain a “gradual and modest” S$NEER appreciation.

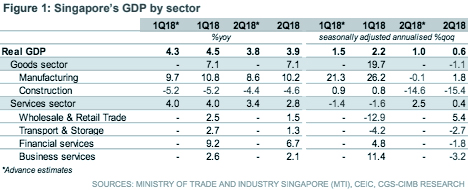

Marginal upward revision to 2Q18 GDP growth

Revised data from the Ministry of Trade and Industry (MTI) revealed that Singapore’s economic expansion in 2Q18 was slightly better than initial estimates, as real GDP growth was revised higher to 3.9% yoy from an advance reading of 3.8% yoy (CIMB: 3.8% yoy, Bloomberg: +4.1% yoy). 1Q18 GDP growth was bumped up to 4.5% yoy from 4.3% yoy, following an upward adjustment in 1Q18 sequential growth to 2.2% qoq seasonally adjusted annual rate (SAAR) (advanced: +1.5% qoq SAAR) and consequently a downward revision in 2Q18 to 0.6% qoq SAAR (advanced: +1.0% qoq SAAR).

Transport equipment capex spur investments

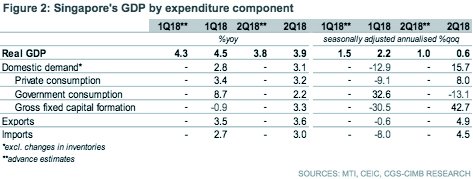

Domestic demand was more robust in 2Q18 (+3.1% yoy vs. +2.8% yoy in 1Q18) principally driven by a surge in investments (+3.3% yoy vs. -0.9% yoy in 1Q18). The private sector was responsible for much of the rise (+5.6% yoy vs. -0.4% yoy in 1Q18), lifted by higher capex in transport equipment, with increased activity in hangars and shipyards complemented by upgrades to the local transport system.

Households and external demand chip in with solid outturns

Private consumption growth moderated slightly to 3.2% yoy in 2Q18 (+3.4% yoy in 1Q18) supported by a recovery in motor vehicle sales and broader retail segment as a healthier labour market and wage gains improved household purchasing power. However government consumption eased in 2Q18 (+2.2% yoy vs. +8.7% yoy in 1Q18) as outlays for defence and national development tapered. External demand, as measured by net export growth, softened slightly (6.8% yoy vs. +8.0% yoy in 1Q18) due to a pick-up in import growth.

Growth outlook still hinged on export-driven manufacturing sector

Upward revisions to the growth contribution from the manufacturing sector in 2Q18 (+10.2% yoy vs. +8.6% yoy in advance estimate) stemmed from gains in the biomedical (+15.5% yoy) and transport engineering segments (+11.7% yoy), and were sufficient to offset weaker services and construction growth. The services sector grew at a slower pace in 2Q18 (+2.8% yoy vs. +3.4% yoy in advance estimate) due to slower growth in all segments except accommodation and food services (see table to the left). Construction activity contracted in 2Q18 (-4.6% vs. -4.4% yoy in advance estimate), due to a pullback in the public sector. We expect property cooling measures unveiled in July to interrupt the recovery in residential construction, which posted a less severe contraction in 2Q18.

MAS policy stance likely on hold

We reaffirm our annual GDP forecast of 3.2% in 2018, which falls within the official MTI forecast range of 2.5% to 3.5%. Uneven gains in the domestically-oriented services sector and risks to the external outlook suggest that MAS will likely retain a cautious stance on monetary policy. We expect MAS to maintain a “gradual and modest” pace of appreciation for the S$NEER at the Oct 2018 monetary policy meeting. CIMB Treasury and Markets Research expects the Singapore dollar to depreciate to S$1.37 per US dollar in 3Q18 and appreciate to S$1.36 per US dollar in 4Q18.

Originally published by CIMB Research and Economics on 13 August 2018.