HIGHLIGHTS

2H18 Outlook: A summer of discontent

- The resilience of the global economy will be tested by tightening monetary conditions, risks of greater international trade and investment friction, and geopolitical uncertainty.

- Markets have become attuned to risks of tighter global financing conditions and volatile FX adjustments to highly leveraged economies with large external imbalances.

- We expect monetary policy divergence between countries subject to macro volatility (Indonesia) vs. highly leveraged and trade-exposed economies (Malaysia, Thailand).

Global: Engines of growth tested by confluence of risks

The extended recovery means advanced economies have closed their output gaps and are reaching full employment, precipitating further withdrawal of monetary policy accommodation, particularly in the US and Eurozone, to prevent overheating. Other risks have surfaced or intensified in recent months that could derail growth prospects, including 1) a disorderly unwinding of global liquidity, 2) the erosion of rules-based global trade order, 3) elevated oil prices reducing real purchasing power, 4) geopolitical uncertainty and election cycles in the US, India, Indonesia and Thailand.

ASEAN: In for a bumpy ride

We expect some degree of policy divergence ahead as regional central banks balance the risks to growth with macro stability. Economies with more fragile external balances could come under sharper balance of payment and currency pressure, necessitating a policy response. This is particularly so for Indonesia, where we expect more hawkish biases to monetary policy. Highly-leveraged and trade exposed economies (Malaysia and Thailand) could pursue a more balanced policy mix to manage shocks to the economy.

Malaysia: When the going gets tough, the tough get going

The Pakatan Harapan government wasted little time in delivering its election promises, significantly repositioning Malaysia’s fiscal policy agenda. The growth outlook (+5.2% in 2018) remains intact as stimulus to consumers make up for the cutbacks in government spending and infra works. While implementation will be demanding, the government is likely to land within an acceptable range from the 2018 budget deficit target of 2.8% of GDP. Questions over longer-term fiscal sustainability, however, remain unanswered. External risks may delay the next Overnight Policy Rate (OPR) hike to 2019.

Indonesia: Sailing through a storm

The rupiah has come under pressure in recent months, plagued by volatility of capital flows amid rising external pressures. The currency weakness prompted a shift in Bank Indonesia’s (BI) monetary policy stance to a hawkish bias, which was followed by a swift cumulative 100bp rate hike in May/Jun, underscoring BI’s determination to arrest the slide of the rupiah. As the signs of external uncertainties abating are nowhere in sight, more rate increases could be on the table, depending on the rupiah’s movement. We expect the 7-day Reverse Repo Rate to increase to 5.75% by end-2019. On the growth front, we project the GDP to expand +5.3% yoy in 2018F and +5.2% yoy in 2019F, underpinned by robust investment activity, while private consumption growth is likely to remain steady.

Singapore: Guarded against external risks

Singapore’s growth trajectory remains strong, aided by the export-driven manufacturing, broadening gains in services and the bottoming of construction sector weakness. The Monetary Authority of Singapore (MAS) is adopting a prudent stance to head off risks from slowing external drivers, global trade tensions and tightening financial conditions. We maintain our expectations that MAS will keep its guidance for a “gradual and modest appreciation” of the S$NEER in Oct.

Thailand: Progress may be hindered

Thailand’s upgraded growth outlook (+4.3% in 2018), anchored by gains in both domestic and external demand, is balanced by greater concerns over the US-China trade spat. Markets may have to wait longer for domestic political uncertainty to clear, as the timeline for elections may be delayed again. Amid heightened uncertainties, we expect the policy mix to remain accommodative, and the BOT to keep the policy rate at 1.50% in 2018.

GLOBAL OUTLOOK IN 2H18

Global economic momentum intact but brace for volatility

While data points tracking the expansion of global trade and industrial activity have corroborated with expectations of a moderation in momentum following last year’s acceleration, the external environment remained generally supportive of economic growth in both the advanced and developing economies in 1H18. Global indicators of trade and industrial activity remain robust, having rebounded after a patchy start to the year. Indicators of business sentiment, such as the global manufacturing PMI (53.1 in May), are down from a peak in 4Q17, but still above the 50-pt level that marks expansion, primarily boosted by robust growth in the industrial, technology, consumer and telecommunication sectors. PMI readings of the service sector globally also perked up in 1H18, as domestic drivers of growth become more entrenched. Legs in the cyclical upswing and fiscal stimulus in the US led the IMF to revise its forecast of global GDP growth higher to 3.9% in 2018 and 2019, from 3.7% previously.

Nevertheless, risks have surfaced or intensified in recent months that could derail growth prospects and disrupt financial markets, including:

- Higher oil prices dampening purchasing power.

- The erosion of rules-based global trade order amid the escalation of trade disputes between the US and major trading partners, principally China.

- Geopolitical uncertainty arising from Brexit, election cycles and nuclear adversaries.

- Disorderly unwinding of global liquidity and dislocation of capital exerting pressure on economies with debt and balance of payment fragilities.

Crude oil prices have rallied in 1H18 (Brent: +17% YTD) due to higher petroleum products demand, a weaker than expected supply response by North American shale, and output losses in Iran, Libya and Venezuela. Oil prices are likely to remain above the US$70/bbl handle with risks to the upside as projections by the International Energy Agency indicate the global crude market appears balanced going into 2019 with limited spare capacity after the alliance of Opec and major non-Opec producers struck a deal on 22 Jun to increase production. The oil output agreement did not stipulate a specific target and country allocation for output expansion, and estimates have ranged from 0.6mbpd (Iran) to 1mbpd (Saudi). The alliance is managing the upward march in oil prices to prevent demand destruction, as higher oil prices are likely to raise headline inflation as energy prices are passed through to consumers.

Trade tensions intensify. At the start of the year, we warned that the relative geopolitical calm that presided over 2017, following the string of surprises in 2016, such as Brexit, the election of Donald Trump to the US presidency and a surge in populist movements across Europe, should not be taken for granted. Trade was the first victim of the year as the US government announced on 22 Jan that it would impose safeguard tariffs of up to 30% on solar imports. President Trump followed that with duties on steel and aluminium imports including from key trade partners, the EU, Canada and Mexico, and sizeable tariffs on imports of autos and auto parts, aimed at the European and Asian carmakers

America First vs. Made in China 2025. The US’s muscular approach intensified when it imposed tariffs on US$50bn of imports from China, of which US$34bn covering 818 products will come into effect on 6 Jul, while another 284 items totaling US$16bn, including electronics and semiconductor imports, are subject to a period of public feedback before implementation. The US could potentially raise the tariff stakes by a further US$400bn if China retaliates, in order to stop what it alleges are unfair economic practices by China in the transfer of technology and intellectual property from US companies. China has promised to levy tariffs to match the US, while removing or lowering import tariffs for items targeted by the US that it sources from other trade partners. The riposte also nulls the agreement forged in high level trade talks in Beijing, in which China promised to cut its trade surplus with the US by US$70bn. More worryingly, President Trump tasked the US Treasury to draft a series of restrictions on inbound Chinese investments in US companies and startups in sectors identified in the Made in China 2025 plan, though he and other US officials later softened their stance by using existing laws that apply to all countries.

Brexit. The clock on Brexit has ticked down to 270 days, when the UK will leave the European Union at 11pm on 29 Mar 2019, fulfilling the outcome from the referendum of 23 Jun 2016. Despite the intervening two years since, the UK government remains far from agreeing to a resolution on the terms of its departure, in particular relating to immigration, trade access, financial regulation and the length of a transition plan, which could lead to the possibility of a ‘cliff edge’ departure next Mar.

European politics. In Italy, the anti-establishment Five Star Movement and League parties emerged from the 4 Mar 2018 election as a coalition to form government. While Prime Minister Conte has downplayed risks of Italy seeking a referendum for an exit from the EU, the coalition are likely to seek to widen the budget deficit to boost the Italian economy against EU fiscal compact and challenge the status quo on trade and immigration. Likewise, Spanish politics was upended in May when the Opposition Socialist party called a no-confidence vote against Prime Minister Rajoy. Parliament voted by a slim majority of 180-170 to replace Rajoy with Socialist leader Pedro Sanchez, who will lead a policy agenda to reverse social spending cuts and improve relations with Catalonia.

In 1H18, North Korea and Iran traded places as the US pulled out of the Iran nuclear deal on 8 May while President Trump met with North Korean leader Kim Jung Un at an historic summit in Singapore on 12 Jun to negotiate a nuclear armistice. Other key events on our watch list: US mid-term elections (6 Nov 2018), Brexit (29 Mar 2019), and general elections in Indonesia (17 Apr 2019), India (Apr-May 2019), and Thailand (by 5 May 2019).

Asset markets and the global economy have absorbed the geopolitical shocks so far as the global economy remains resilient. However, we expect news flow on trade and geopolitics to remain fluid in the coming months, with the potential to cause spikes in volatility in the financial markets, rising risk premiums, depress business sentiment and weigh on global growth, as increasingly fractious political environments may create conditions for escalation of protectionism and policy mistakes. Disunity at the G7 summit in Jun, in which President Trump broke ranks on a joint statement to temper protectionism, underlined frictions in the multilateral framework for safeguarding the existing order of international trade and capital flows.

Unwinding of global liquidity

The extended recovery means advanced economies have closed their output gaps and are reaching full employment, precipitating monetary tightening by central banks and the requisite warnings over volatility in late-stage cycles.

United States. By geography, growth momentum in advanced countries tilted to the US, which has benefited from an extended economic recovery and fiscal stimulus, offsetting the effects of higher commodity prices and interest rates. Tax cuts, which came into effect in Jan 2018, and additional spending passed in Feb 2018 are expected to drive US GDP growth higher, after cooling to 2.2% qoq saar in 1Q18 due to adverse weather. The latest ‘Nowcast’ models by the regional Federal Reserve Banks of Atlanta, New York and St Louis suggest the US economy grew between 2.8% to 3.8% qoq saar in 2Q18.

Despite indications that the US economy is bumping into capacity constraints, with unemployment rate falling further to 3.8% in May and capacity utilisation rising to 77.9% in May, inflation and wage growth remain unusually weak. Nonetheless members of the Federal Reserve FOMC have judged that faster GDP growth and building capacity constraints are sufficient to upgrade the FOMC’s median ‘dot plot’ forecast to four Fed Funds rate (FFR) hikes to 2.25- 2.50% in 2018, three hikes to 3.00-3.25% in 2019 and one hike to 3.25-3.50% in 2020. After the Federal Reserve voted for a second 25bp rate hike for the year on 13 Jun raising the FFR to 1.75-2.00%, two more 25bp rate increases are expected, at the Sep and Dec meetings.

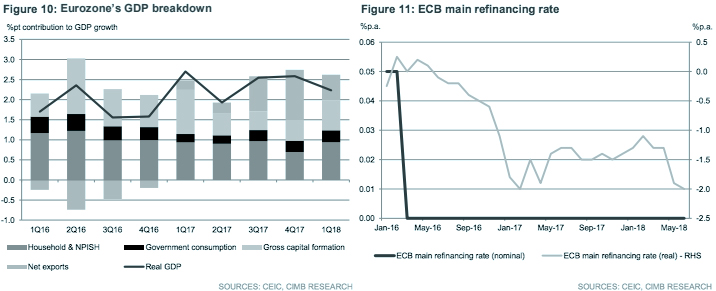

Eurozone. Economic growth in the Eurozone hit a speed bump in 1Q18, but we expect the blip to fade, with the currency area gradually recovering on the back of domestic demand anchored by loose monetary conditions and positive contributions from net exports. Progress on the growth front is likely to bring the Eurozone output gap to parity by this year, encouraging the European Central Bank (ECB) to end its bond purchase programme. On 14 Jun, the ECB announced that it would reduce monthly purchases by half to €15bn per month and conclude bond purchases by Dec. However ECB President Mario Draghi offered dovish forward guidance on the timing of interest rate hikes, which are expected in “summer 2019 at earliest”, reflecting the central bank’s unease with the softer data outturn and potential spillovers from global trade tensions.

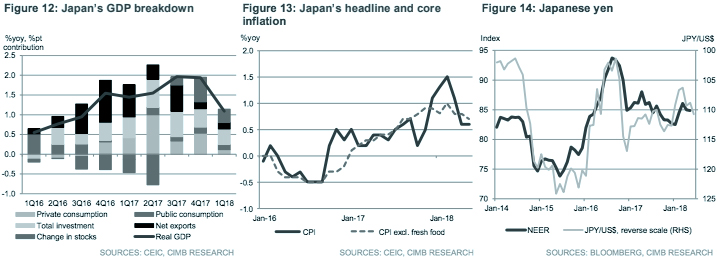

Japan. An eight-quarter run of growth came to a halt, as Japan’s economy contracted 0.6% qoq saar in 1Q18. While we think the weakness was probably overstated at the start of the year due to slippages in domestic demand and weakness in electronics demand, the slowdown is line with incoming headwinds emanating from higher oil prices, slowing gains in the labour market, and VAT hikes in 2019. Growth was not the only setback. Achieving a price stability target has been a more stubborn problem for the Bank of Japan (BOJ) than other central banks, despite a four year campaign to arrest deflation. Headline and core inflation trends have trailed expectations after a spike at the start of the year, leading the BOJ to downgrade its 2018 inflation forecast to 0.5-1.0% vs. “around 1.0%” earlier, and pushing the expected timeline for meeting the central bank’s mandate of 2% to after 2019.

China. Following the National Party Congress in Mar, the government has set a growth target of 6.5% in 2018, unchanged from 2017, but omitted comments encouraging an overshoot, as policymakers balance growth targets with the need to safeguard financial stability, rebalance the economy and manage risks from trade tensions with the US, which have taken a turn for the worst in recent weeks. The People’s Bank of China (PBOC) has cut the reserve requirement ratio (RRR) twice, once in Apr (100bp) and another effective 5 Jul (50bp), taking the RRR for large commercial banks down to 15.5% and for smaller banks to 13.5% pt. Alongside the reduction, the most recent of which is expected to increase bank reserves by Rmb700bn (US$107bn). the PBOC has directed banks to channel the funds towards small and medium-sized enterprises and debt-for-equity swaps, in which banks retire debt to highly leveraged firms in return for equity stakes, as part of the authorities’ campaign to de-risk the financial system since 2016, which has taken on greater urgency in the face of downside risks to growth amid escalating protectionism with the US. It also offsets the impact of a credit crunch brought on by tighter financial conditions on investment spending and the property sector.

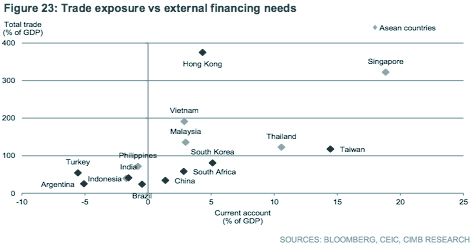

As policy normalisation accelerates in the advanced economies, tightening financial conditions have triggered bouts of bond yield spikes, wider credit spreads, a correction in asset prices and currency weakness in emerging markets. Markets have become more attuned to risks posed by a sharp squeeze in global financing conditions and volatile adjustments in the exchange rate to highly leveraged economies with large external financing requirements – the classic ‘impossible trinity’ dilemma. Rising oil prices add another layer of risk for oil importing economies with narrow current account buffers. Notably, portfolio outflows have been especially sharp in selected countries which are perceived to be exposed to such risks, like Argentina, Brazil and Turkey.

Below, we compare a series of metrics to gauge which countries in Asia may be at risk. Generating economic expansion has generally not been an issue in Asia, with growth rates exceeding those recorded by advanced economies and emerging economies in other continents. Likewise, inflation dynamics have improved in recent years, suggesting that central banks have a good grip on price stability risks. Therefore, macro risks are concentrated in leverage and external balances. Total debt ratios have broadly risen across Asia in the last five years, with the sharpest increases occurring in China, Malaysia, Thailand, and South Korea (we exclude Hong Kong and Singapore as government debt issuances are not used to finance government spending), and echo similar increases in Turkey and Brazil. High leverage exposes economies to higher debt service charges and deterioration in balance sheets, magnifying the impact of macro and financial shocks to the real economy. China is particularly at risk for transmitting contagion to the rest of the region, due to the size of its corporate debt.

Countries that run current account deficits depend on offsetting inflows of capital that are generally sourced from foreign direct investment and portfolio flows. A sudden withdrawal of capital could trigger sharp increases in borrowing costs and currency depreciations with negative spillovers to the real economy. Among the countries above, India, Indonesia and the Philippines run twin deficits, though the current account and fiscal balance shortfalls are much narrower than those of Turkey, Argentina and Brazil. External debt exposures, which were a key fault line during the Asian Financial Crisis when regional currencies depreciated sharply, have risen in Malaysia, Taiwan, Thailand and Vietnam, mirroring the uptrend in Turkey (we exclude Hong Kong and Singapore as they are largely trade-finance related). To note, the increase in Malaysia’s external debt is exaggerated by a redefinition in 2014, which includes non-resident holdings of ringgit-denominated assets. International reserve buffers in Asia remain sufficient to tolerate transitory bouts of financial volatility. However, a disorderly and extended unwinding of capital flows would weigh more heavily on Malaysia and Indonesia than their peers due to: 1) lower levels of reserve coverage against import requirements and external debt, 2) Malaysia’s relatively large foreign ownership of government bonds, and 3) Indonesia high level of foreign currency bonds.

The escalation of geopolitical and trade tensions therefore poses an acute policy challenge for countries running high levels of debt, twin deficits and at risk of portfolio outflows. Policymakers in economies where trade intensity (and therefore exposure to a trade war) is lower would likely prioritise macro stability. Therefore, we expect a stronger upward bias to policy rates in India, Indonesia and the Philippines. The case is less clear for countries in the middle of the pack (Malaysia, Vietnam, South Korea), as disruptions to global trade could prove sufficiently damaging to growth for central banks to consider not making sharp interest rate adjustments.

ASEAN: Interest rate and currency forecasts

In ASEAN, we expect Bank Indonesia to lead the cycle of rate hikes with the policy rate increased to 5.75% by end-2019 due to vulnerabilities in its external financing requirements and rupiah fragility. Bank Negara Malaysia (BNM) and the Bank of Thailand are likely to follow with one upward policy rate adjustment in 2019. Singapore’s exposure to global trade and the ensuing uncertainty surrounding the trade outlook likely pushes back against further normalisation of monetary policy by the Monetary Authority of Singapore (MAS). Against this backdrop, CIMB Treasury FX Research is expecting the ASEAN currencies to appreciate against the US$ in 2H18, with the Malaysian ringgit forecast to see the largest gains among the four MIST economies under our coverage.

MALAYSIA

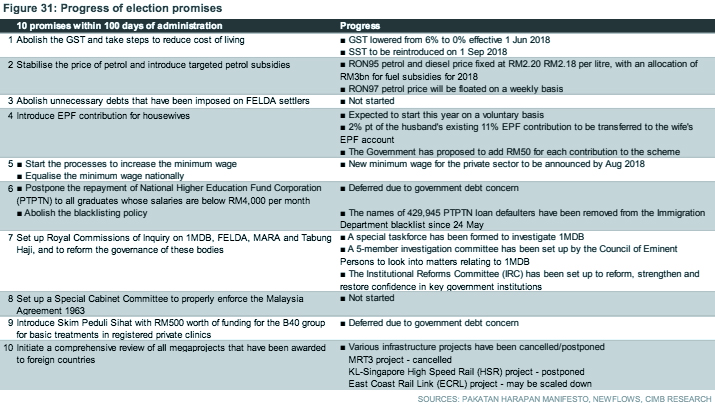

The newly elected Pakatan Harapan government wasted little time in getting to work on its list of election promises for the first 100 days and significantly repositioning Malaysia’s fiscal policy agenda. Cutbacks to government spending and infrastructure works mean risks to growth lie to the downside. Despite implementation risks, we think the government is likely to land within an acceptable range of the budget deficit target of 2.8% of GDP in 2018. Questions over longer-term fiscal sustainability, however, remain unanswered. External risks may delay the next OPR hike to 2H19.

GE14 ushers in a New Malaysia

The 14th General Elections (GE14) ushered in a watershed moment for Malaysia, as the incumbent Barisan Nasional government was unseated for the very first time since the country’s independence by Pakatan Harapan, a relatively new coalition of four political parties. Once established, the new government immediately introduced swift overhauls, as well as major changes to leadership positions in the government and public offices in a bid to strengthen governance and transparency in the public sector. The new government also appointed a Council of Eminent Persons, comprised of former senior public and government officials, to spearhead economic reforms and guide policy direction.

Economic impact of fiscal reforms

The Pakatan Harapan government wasted little time in getting to work on its list of election promises for the first 100 days and significantly repositioning Malaysia’s fiscal policy agenda. Among measures, we expect the reduction of the Goods and Services Tax (GST), the expected reintroduction of the Sales and Services Tax in Sep, the delays or cancellation of mega projects, rationalisation of government spending and fuel subsidies to wield the largest effects on growth and government finances. Cumulatively, we expect the cancellation of infrastructure projects to exert a drag on GDP growth of about 0.6-0.7% pt p.a in 2018 and 2019. We are maintaining our GDP forecasts of 5.2% in 2018 and 5.0% in 2019, as we expect the stimulus from the GST reduction (net of SST), fuel subsidies, cash handouts and bonuses for civil servants to offset the drag from government expenditure and mega project delays/cancellations.

- (MRT3) projects on our 2018 and 2019 GDP growth forecast is minimal as we had not factored in a significant boost from the HSR and MRT3 into our GDP growth forecast for 2018 given that construction works were only expected to commence in 2H19. Post-2020, we estimate that both projects would have added about 0.6% pt to headline GDP growth, offsetting the diminishing contributions from LRT3 and MRT2 which would have been reaching completion.

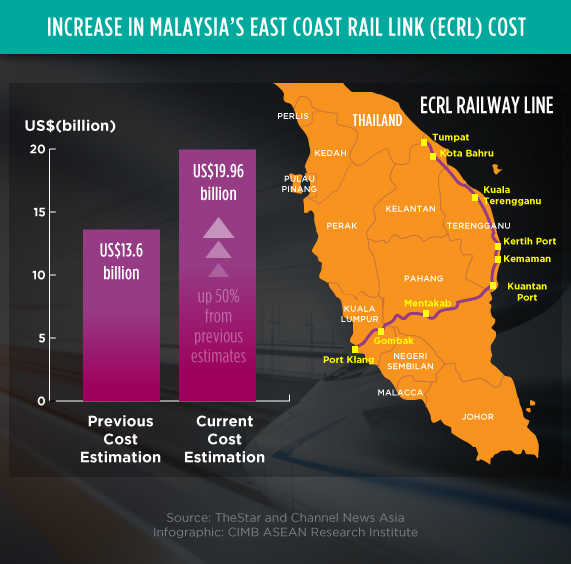

- Potential impact of ECRL to our 2018 and 2019 GDP growth forecasts is -0.2% pt p.a. As the project will likely face delays due to the government’s intention to renegotiate the terms of the project, we have removed the 0.2% pt contribution that had been headline GDP growth in 2018 and 2019.

- Potential downside of Pan Borneo to 2018 and 2019 GDP growth is – 0.2% pt. We think Pan Borneo has a strong development case for proceeding, perhaps with delays or a scaling down. In the worst case of cancellations or a construction halt, we would have to cut GDP growth contribution by about 0.1% pt in 2018 and 2019.

- Potential downside of fiscal cuts to 2018 and 2019 GDP growth is a cumulative -0.6% pt over the two years. We think it will be a challenge for the government to meet its RM10bn target for expenditure cuts to maintain the fiscal deficit target at 2.8% of GDP.

We estimate that households will receive a stimulus from GST cuts net of SST, fuel subsidies and cash handouts in 2H18 that could boost private consumption’s contribution to GDP growth by about 0.3-0.7% pt in 2018 and 2019.

Balancing the fiscal impact of reforms

The policy changes have been viewed as ‘credit-negative’ for the fiscal position. The Ministry of Economic Affairs is due to unveil the mid-term review of the 11th Malaysia Plan on 18 Oct while the Budget 2019 will be tabled by the Finance Minister on 2 Nov. The former will address the Pakatan Harapan’s medium-term economic policy targets while the latter is expected to tackle concerns from markets and sovereign ratings agencies on how the government intends to manage the loss of a large government revenue base in the GST (RM21bn in 2018). Several fiscal offsets have been mooted to plug the shortfall. The government expects to collect RM4bn from the Sales and Service Tax (SST), which is expected to borrow heavily from the previous iteration that was retired in 2015. The government plans to cut RM10bn of government expenditure through rationalisation of spending, elimination of political appointees, consolidation of overlapping ministries and government agencies, and improvements in procurement and tender processes. With additional oil-related revenue and higher dividend payments from Government Linked Companies, we think the government could still meet the Budget 2018 deficit target of 2.8% of GDP.

Monetary policy mix to remain accommodative

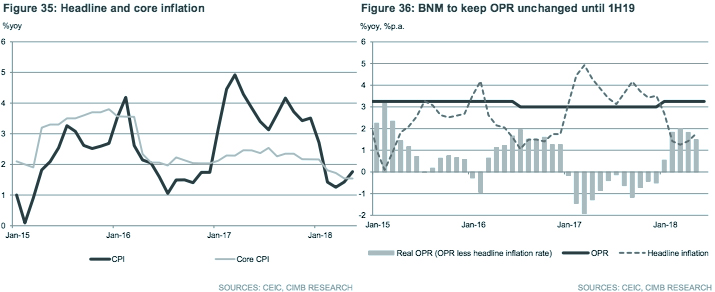

Adjusting for price changes from the GST cut, expected introduction of the Sales and Service Tax (SST) in Sep, fixed RON95 petrol and diesel prices, and subdued administrative price increases, we project headline inflation in 2018 to moderate sharply to 1.3% (+3.8% in 2017), undershooting Bank Negara Malaysia’s (BNM) policy target of 2-3%. With inflation subdued, and potential external shocks from global monetary policy tightening, trade tensions, and geopolitical uncertainty, we expect BNM to exercise restraint against raising the Overnight Policy Rate (OPR) again this year. We reiterate our forecast for the OPR to remain at 3.25% for the remainder of 2018F, and expect the next interest rate hike to be delayed to 2H19F.

INDONESIA

Rupiah has come under pressure in recent months, plagued by the volatility of capital flows on the back of rising external pressures. The currency weakness prompted a shift in Bank Indonesia’s (BI) monetary policy stance to a hawkish bias, which was followed by a swift cumulative 100bp rate hike in May/Jun, underscoring BI’s determination to arrest the slide of the rupiah. As the signs of external uncertainties abating are nowhere in sight, more rate increases could be on the table, depending on the rupiah movement. We expect the 7-day Reverse Repo Rate to increase to 5.75% by end-2019. On the growth front, we project the GDP to expand +5.3% yoy in 2018F and +5.2% yoy in 2019F, underpinned by robust investment activity, while private consumption growth is likely to remain steady.

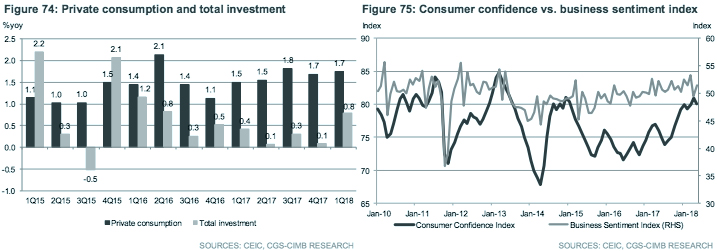

Growth momentum to pick up in the next few quarters

The Indonesian economy started the year 2018 with a lower-than-expected GDP growth of 5.1% yoy in 1Q18 (+5.2% yoy in 4Q17), amid slower public consumption growth. A much-anticipated recovery in private consumption growth did not materialise (+5.0% yoy in 1Q18 vs. +5.0% yoy in 1Q15-4Q17), as a delayed harvest season and shortage of fuel supplies dampened household spending in the F&B and transport & communication segments. On a different note, investment growth continued to shine (7.9% yoy in 1Q18 vs. 7.3% yoy in 4Q17), with outlay on machine, vehicle and equipment being the outperformer for the past three quarters.

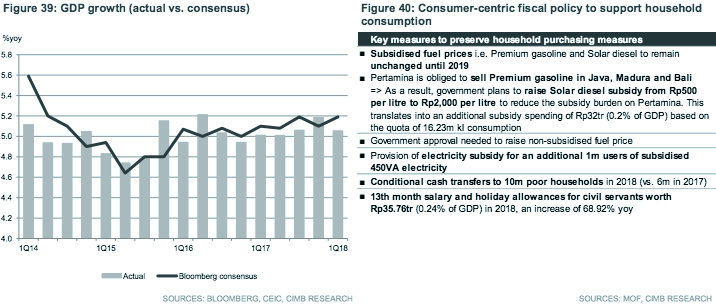

Despite the lacklustre growth, we maintain our 2018 GDP growth forecast at 5.3% yoy, as we expect the growth momentum to pick up over the next few quarters. We expect consumption spending to improve via the following events: 1) the 18th Asian Games that will be held in Jakarta and Palembang from 18 Aug to 2 Sep; 2) the annual IMF-World Bank meeting in Bali in Oct; and 3) pre-election spending in the run-up to the regional elections (27 Jun 2018) and the Presidential election (17 Apr 2019).

Household consumption will also receive a boost from fiscal measures that have tilted towards maintaining household purchasing power ahead of the Presidential election. Policies such as unchanged subsidised fuel and electricity prices and food price ceilings will extend the low inflation environment, seen since 2016, well into next year, translating into better real wage growth. Income growth, especially among the low-income households, will also be complemented by budget measures such as conditional cash transfers to poor households (10m in 2018 vs. 6m in 2017) as well as provision of electricity subsidies to additional 1m households. The 13th month salary and holiday allowance for civil servants have been supportive of consumer spending during the Lebaran month.

We believe investment growth will remain the bright spot, supported by the government’s infrastructure projects as well as improving investment climate. Of the 222 projects and 3 programmes identified as National Strategic Projects (PSN), the Committee for Acceleration of Priority Infrastructure Delivery (KPPIP) has estimated that 13 projects worth Rp46.8tr and 25 projects worth Rp118.8tr will be completed in 2018 and 2019, respectively. This compares to 10 completed projects (Rp61.5tr) in 2017 and 20 completed projects (Rp33.3tr) in 2016.

Capital outlays will also be supported by the continuous efforts undertaken by the government to improve investment climate. These include the revision and expansion of tax incentives, income tax reduction for SMEs as well as the simplification of foreign worker visa application. Under the Jokowi administration, the realised foreign direct investments (FDI) rose from an average of 2.6% of GDP in 1Q10-3Q14 to 3.2% of GDP in 1Q14-1Q18, whereas the realised domestic direct investments (DDI) gained from 1.1% of GDP to 1.8% of GDP over the same period. With close correlation between growth rates in FDI, investments in machine & equipment and import of capital goods (Fig 43), import of capital goods is likely to rise in tandem as the government welcomes more FDI into the country.

Making room for more subsidy and social expenditure

As the Presidential election draws nearer, the fiscal policy will likely remain consumer-centric (Fig 40), in our view. This entails a higher subsidy bill and social expenditure through 2019. That said, we do not expect the subsidy policy to lead to a substantial increase in fiscal deficit position, as we expect the higher subsidy expenditure can be partly funded through the windfall of higher O&G revenue. In 5M18, subsidies and social assistances collectively accounted for more than a fifth of central government expenditure (21.9% vs. 16.3% in 5M17). Though subsidy reform has stalled, we view this as a strategic shift to improve Jokowi’s electability in exchange for policy continuity for the next five years. Against the backdrop of rising external uncertainties, we expect the government to maintain a prudent fiscal deficit target at well below its fiscal limit of 3% of GDP. Hence, this may come at the expense of other expenditure i.e. capital spending to make room for higher subsidy and social spending. The prudent approach has so far been reflected in a lower deficit position YTD (-0.64% of GDP in 5M18 vs. – 0.96% of GDP in 5M17) and a more conservative GDP growth target for draft State Budget 2019 (5.2-5.6% vs. 5.4-5.8% previously).

Price risks are contained, for now

The decision to keep fuel prices unchanged temporarily alleviates the inflationary pressure from oil price shock, whereas price ceilings and imports to tackle supply shortages have kept food inflation broadly under control. Hence, we expect the inflation rate to remain stable at 3.4% yoy in 2018 and 3.7% yoy in 2019 (3.3% yoy in 1H18), in line with Bank Indonesia’s target range of 2.5-4.5%. However, the widening gap between retail and market fuel prices indicates greater possibilities of larger price adjustments post-2019, implying the medium-term inflation outlook could potentially overshoot the BI’s inflation target of 2.0-4.0% for 2020-2021.

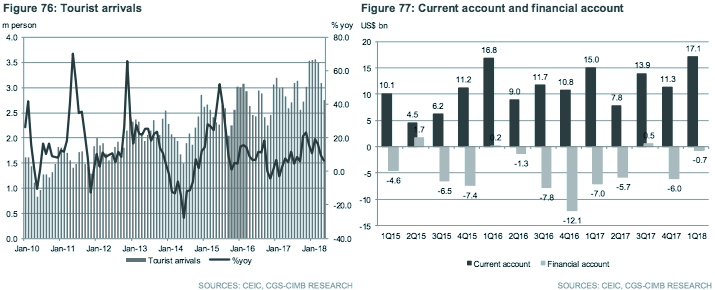

Higher CAD and external uncertainties heighten BOP risk

We expect the recovery of domestic demand and diminishing commodity terms of trade to depress the trade balance, hence leading to a wider current account deficit (-2.5% of GDP in 2018F and -2.3% of GDP in 2019F), hitting the upper limit tolerable by Bank Indonesia (BI). The CAD, nonetheless, still remains manageable compared to the peak of -3.2% of GDP in 2013.

A wider CAD makes Indonesia more dependent on external financing, whereas the relatively high foreign holdings of outstanding government bonds relative to other countries (Indonesia: 38.1%; Malaysia: 25.9%; Thailand: 15.6%) indicate greater vulnerability of the rupiah to the reversal of capital flows, which are a function of external developments. As heightening external uncertainties have prompted foreign portfolio outflows in the bond market, the Indonesian 10-year bond yield has increased ~148bp YTD. Nonetheless, the spread of ~494bp against the US Treasuries of similar maturity is still narrower compared to the 3- year average of about 555bp.

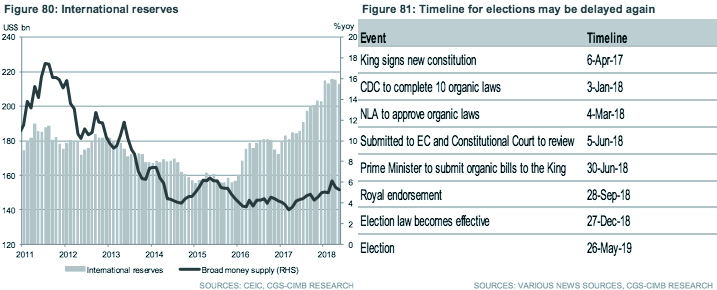

On a positive note, reserves remained ample at US$122.9bn in May, despite declining by US$7.3bn YTD. Based on our calculation, the reserve coverage ratio to potential short-term liabilities (calculated as the sum of short-term external debt by remaining maturity, outstanding foreign holdings of stocks and government bonds as well as non-residents’ deposits) was also higher at 63% compared to a trough of 48% during the 2013 taper tantrum and 5-year average of 59%.

A pre-emptive and ahead of the curve policy rate response

Rising rupiah vulnerability prompted a shift in Bank Indonesia’s (BI) monetary policy to a hawkish stance. Cumulatively, BI has raised the policy rate by 100bp in just six weeks, reversing half of the 200bp reduction delivered in 2016-2017. To mitigate the impact of rate increases on economic growth, BI loosened macroprudential policy for the property sector (see Fig 53). BI’s firm monetary policy stance to react pre-emptively and stay ahead of the curve to stem the depreciation of the rupiah suggests the possibility of more rate hikes, especially with the US Fed expected to continue to raise its policy rate. We expect the 7DRRR to increase to 5.75% by end-2019.

SINGAPORE

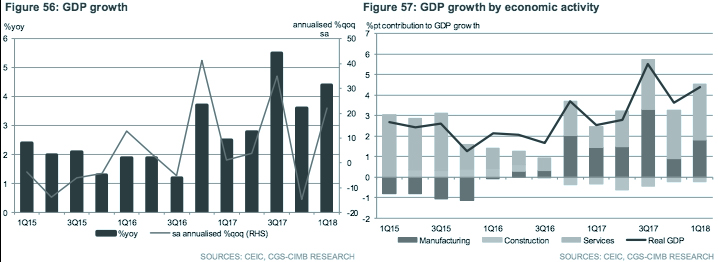

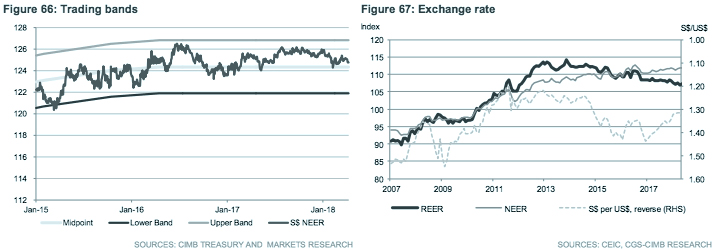

Singapore’s growth trajectory remains strong, aided by the externally-driven manufacturing sector and broadening gains in the services sector. Contraction in the construction sector has likely bottomed out as the property market recovers and higher oil prices support increased O&G capex. The Monetary Authority of Singapore (MAS) is adopting a prudent stance to head off risks from slowing external drivers, global trade tensions and tightening financial conditions. We maintain our expectations that MAS will keep its guidance for a “gradual and modest appreciation” of the S$NEER in Oct.

GDP growth forecast at 3.2% in 2018

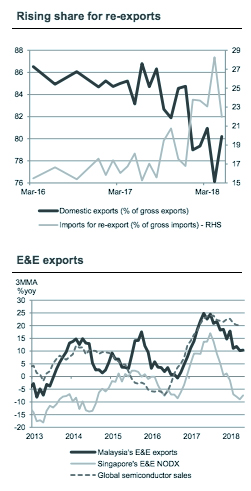

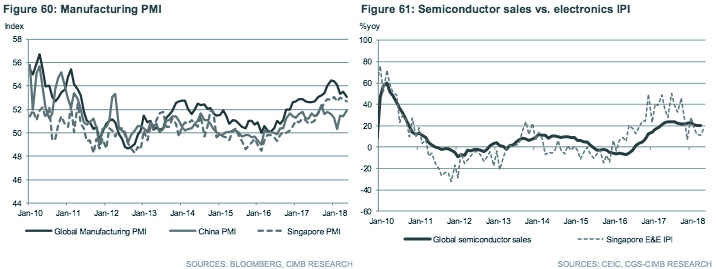

The growth trajectory remains strong as Singapore’s economy expanded 4.4% yoy in 1Q18 (+3.6% yoy in 4Q17) driven by broad-based gains in manufacturing activity as well in improvements in the services sector, particularly financial services and business services. The externally-driven manufacturing has been impressively strong, with the industrial production index up 9.8% yoy in 5M18, led by robust demand for electronics (+16.9% yoy in 5M18), despite a high base in 2017. While we expect the manufacturing sector to remain a key engine of growth this year, global demand for electronics is likely to moderate in 2H18 based on lower growth rates in global electronic shipments. Concerns on the trade front, with the US and China threatening to levy tariffs on a broad range of manufactured goods, would further dampen trade activity.

Construction activity could have bottomed out after the sector contracted 5.0% yoy in 1Q18 (-5.0% yoy in 4Q17), on the back of property market gains and higher oil prices. Sentiment in the property market is improving, with property prices rising for the fourth consecutive quarter (+3.4% qoq in 2Q18), strong demand from homebuyers, robust en-bloc activity and increased landbanking by developers. Meanwhile, the recovery in oil prices could spur higher capex and job tenders for the oil and gas industry.

Barring the materialisation of external shocks, we expect Singapore’s economy to register a 3.2% expansion in 2018, broadly in line with the upgraded official forecast by the Ministry of Trade and Industry (MTI) from 2.5% to 3.5%. Risks to the outlook include disruptions to the trade cycle from increased protectionist policies by major trade nations, tighter financial conditions arising from global monetary policy normalisation, geopolitical uncertainty, and a sudden loss of momentum in the economies of the US and China.

MAS unlikely to tighten monetary policy further

As expected, the Monetary Authority of Singapore (MAS) steepened the slope of the S$ nominal effective exchange rate (S$NEER) policy band at its policy review in Apr allowing for a “gradual and modest appreciation”, but keeping the width and centre of the band unchanged. MAS had last reduced the slope of appreciation in the S$NEER in Oct 2015 and Apr 2016 as inflationary pressures waned.

Going forward, we expect the Monetary Authority of Singapore (MAS) to adopt a prudent stance to head off risks from slowing external drivers, global trade tensions and tightening financial conditions. Given Singapore’s dependence on trade, we are watching the developments between US and China closely as they prepare to enact US$50bn of tariffs, set to take effect in stages from 6 Jul. A potential escalation of retaliatory duties of up to US$400bn as well as threats to impose selective restrictions on investments bode poorly for global trade and Singapore’s growth outlook. Meanwhile, inflation dynamics remain weak (+0.4% yoy in May) despite improvements in domestic labour market conditions. We maintain our expectations that MAS will stay put on a “gradual and modest appreciation” of the S$NEER in the Oct policy review. However, if the brinksmanship between the US and China causes global trade momentum to slow sharply, putting Singapore’s growth outlook at risk, we expect MAS to stand ready to recalibrate policy settings to support the economy. CIMB Treasury and Markets Research expect the Singapore dollar to appreciate to S$1.33 per US dollar by end-2018.

THAILAND

Thailand’s positive growth outlook, anchored by gains in both domestic and external demand, is balanced by greater concerns over the US-China trade spat. Additionally, markets may have to wait longer for domestic political uncertainty to clear, as elections in 2019 may be delayed again. Amid heightened external uncertainties, we expect the policy mix to remain accommodative, including for the BOT to maintain the policy rate at 1.50% in 2018.

External drivers tip the scales for Thailand in 2017

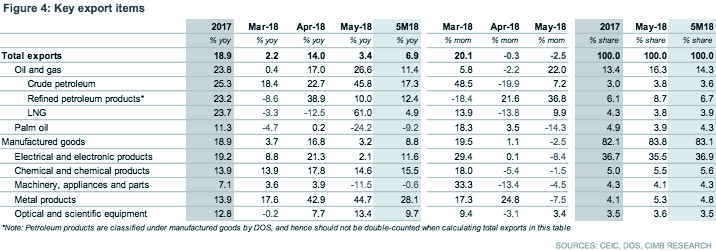

Coming off strong GDP growth of +4.8% yoy in 1Q18, Thailand’s economy is exhibiting signs of broadening growth drivers in the domestic sector. The external sector continue to anchor contributions to the economy, particularly core industries such as electronics, auto and auto parts, rubber and petrochemicals however export momentum slowed at the start of the year, leading us to dial down net export contribution. Weakness in the goods sector was offset by higher tourist arrivals, which have risen by 12.6% yoy in 5M18 to 16.5m, driving an increase in tourist receipts.

Improvements in public investments were anchored by the Eastern Economic Corridor (EEC). Since the approval of the EEC bill in Feb, the Board of Investment (BOI) has recorded significant progress on investment and infrastructure outlays in the EEC, with 81% of application values to the BOI in 1Q18 attributed to the EEC. The recovery in consumer spending is deepening, but gains in farm and rural household incomes continue to lag.

Government consumption, fuelled by the THB150bn supplementary budget passed in Mar, adds a layer of support for these lower-income households. Of the total fiscal stimulus, the government has allocated THB24bn to restructure parts of the agriculture sector suffering from depressed commodity prices and THB76bn for welfare transfers and job creation in the provincial regions. The Thai government has again delayed plans to raise the value-added tax rate from the current rate of 7% until the end of the next fiscal year in Sep 2019 to support the domestic economy.

The GDP growth forecast from the National Economic and Social Development Board (NESDB) for 2018 has been revised higher from 3.6-4.6% to 4.2-4.7% (CIMB: +4.3% in 2018) on the back of the upside surprise in 1Q18 GDP numbers.

Risks to Thailand’s macro outlook

Protectionism poses adverse risks for Thailand, which has leaned on external demand to support growth. Threats by the US and China to levy tariffs on manufacturing goods and expand protectionism to non-tariff measures, such as investment restrictions, could dampen international trade and investment conditions, tilting the growth outlook to the downside. On the domestic front, political uncertainty may linger for a while longer, as the timeline for elections could be delayed again from the latest target of Feb 2019, after Deputy Prime Minister Wissanu Krea-ngam cited a time frame of 24 Feb to 5 May 2019 as possible polling dates to accommodate the completion of necessary constitutional and legislative procedures.

No rush to hike

Headline inflation accelerated further to 1.5% yoy in May, reflecting higher oil prices, while healthier private consumption lifted core inflation to 0.8% yoy in May. The Bank of Thailand (BOT) tweaked its headline inflation forecast higher to 1.1% in 2018 (from 1.0%) and its core inflation forecast to 0.9% in 2019 (from 0.8%), though the prognosis remains shy of the central bank’s price stability mandate.

The BOT is likely to extend its pause on the benchmark 1-day repurchase rate to support economic growth, manage risks to the buildup of household debt, and provide a buffer against escalating trade tensions. We reiterate our year-end policy rate forecast of 1.50%, implying no change to the policy rate in 2018.

Originally published by CIMB Research and Economics on 03 July 2018.