Malaysia: May 2018 trade

HIGHLIGHTS

May 2018 trade

- Despite a sharp fall in total trade, the trade balance remained healthy at RM8.1bn

- Trade activity likely suffered from a high base and the 14% yoy decline in working days due to GE14.

- Headline imports eked out a marginal gain due to a sharp increase in imports for reexport purposes, in spite of the slump in end-use imports.

- We forecast exports to grow 7.7% in 2018 but trade tensions, the start of US-China tariffs on 6 Jul, and a slowdown in China and the global manufacturing cycle are risks.

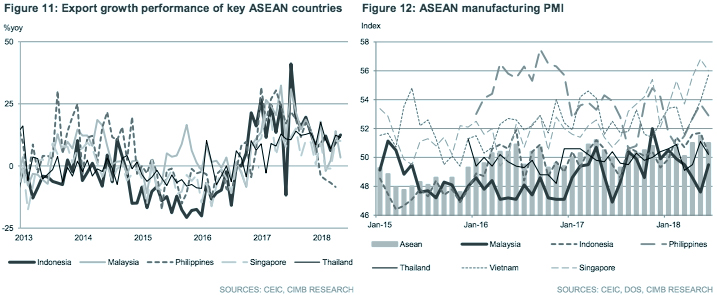

The expansion of trade activity dulled in May

Total trade growth eased sharply to +1.8% yoy in May (+11.8% yoy in April), weighed down by 1) a high base effect, and 2) fewer working days during the election month. The expansion in gross exports came in weaker-than-expected at +3.4% yoy (CIMB: +7.0% yoy, Bloomberg consensus: +6.4% yoy; April: +14.0% yoy), but still outpaced the 0.1% yoy gain in gross imports (CIMB: +4.9% yoy, Bloomberg consensus: +0.2% yoy, April: +9.2% yoy). Hence, the trade surplus remained healthy at RM8.1bn (CIMB: RM7.4bn, Bloomberg consensus: RM10.5bn, RM13.0bn in April).

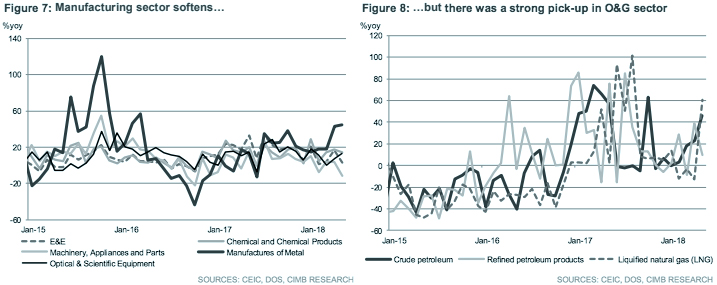

The surge in O&G exports…

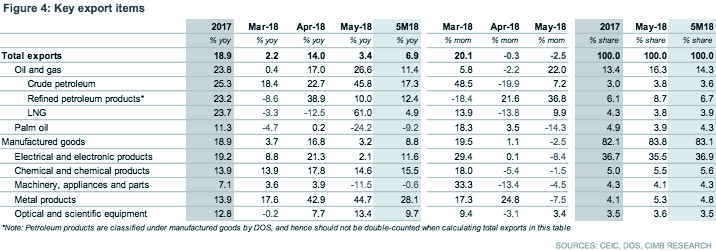

O&G exports (+26.6% yoy in May vs. +17.0% yoy in April) were the clear outperformer in May, with LNG exports rebounding 61.0% yoy (-12.5% yoy in April), after three months of declines, due to higher volumes (+68.7% yoy). Higher oil prices supported crude petroleum exports (+45.8% yoy vs. +22.7% yoy in April) and refined petroleum product (+10.0% yoy vs. +38.9% yoy in April). On the other hand, lower export volumes and CPO prices were a drag on palm oil exports (-24.2% yoy in May vs. +0.2% yoy in April).

… outshines manufacturing exports

The expansion in manufacturing exports lost steam in May (+3.2% yoy vs. +16.8% yoy in April) amid weaker performance in key sectors such as E&E (+2.1% yoy vs. +21.3% yoy in April), machinery, appliances and parts (-11.5% yoy vs. +3.9% yoy in April), as well as chemicals (+14.6% yoy sv. +17.8% yoy in April). The moderation in Malaysia’s E&E exports tracked that of Singapore, despite continued double-digit growth in global semiconductor sales. We think the export values (in local currency terms) may have been eroded by the ringgit’s appreciation against the US$.

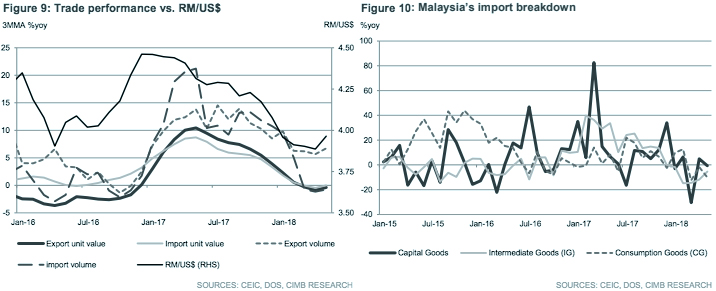

Import demand plagued by uncertainty on political landscape

All three import groups contracted during the start of the fasting month: intermediate goods (-5.3% yoy vs. -11.8% yoy in April), capital goods (-0.7% yoy vs. +4.9% yoy in April), and consumption goods (-10.2% yoy vs. -1.8% yoy in April). In May, there were 3 days or 14% fewer working days than the same month last year due to three public holidays declared during GE14, as well workers taking more time off to travel for the mid-week vote. The import declines may also reflect the more cautious sentiment among manufacturers and consumers after changes in the domestic political landscape and post-election uncertainty

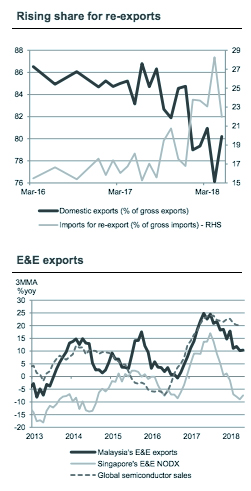

Sharp rise in share of imports for re-export purposes since 2017

Despite the slump in end-use imports, headline gross imports still eked out a marginal increase due to the gain in imports for re-exports (+21.4% yoy vs. +84.3% yoy in April). The share of imports for re-exports has increased since mid-2017, suggesting that Malaysia was reaping the benefits from 1) the rise in global trade activity, and 2) perhaps playing a greater role as a regional distribution centre and a port for transshipments.

Global trade outlook clouded by mounting trade tensions

We maintain our 2018F gross export estimate at 7.7%. Risks to the downside include an escalation of trade tensions following the implementation of US$34bn tariffs effective 6 July, a sharper cyclical slowdown in the manufacturing cycle, and growth risks in China.

Originally published by CIMB Research and Economics on 05 July 2018.