We expect GDP growth to remain strong in 3Q18

The latest reading on industrial activities showed better-than-expected growth (Index of Industrial Production, IIP, grew at 14.3% yoy in July and 13.4% yoy in August), which pointed to a sustained expansion in the manufacturing sector. Despite a high base in 3Q17, we expect GDP growth in 3Q18 to remain strong at 6.8% yoy. There could be a positive surprise in 4Q18, which could bring GDP growth to 6.9% for the full year.

Depreciation pressures on the dong have eased but linger

We believe pressures on the dong have eased in the short run as 1) the country has a healthy balance of payments, thanks to a trade surplus and positive FDI inflow; 2) PBOC has undertaken measures to mitigate Rmb depreciation pressure; and 3) market sentiment has improved in the official and black markets. In the long run, we think policy makers will tolerate modest depreciation in the dong amid broad US$ strength.

We do not project a policy rate hike in end-2018

The recent developments in Vietnam’s money market offer a slew of signals on where we are in the interest rate cycle. Interbank rates rose to a record high, bond yields rebounded and there was a small hike in deposit rates. We view this tightening of liquidity in the banking system as a normalisation of monetary conditions. As such, we believe that the SBV will not be rushed into a policy rate hike this year.

Fundamentals remain sound compared to other emerging markets

In many emerging markets, financial conditions have tightened more appreciably, particularly for countries with large current account deficits and high inflation rates. For Vietnam, we believe that the risk is relatively limited since Vietnam has much stronger fundamentals than Argentina and Turkey or even Indonesia and seems less vulnerable to current account pressures compared to other Asian countries.

Be selective to ride an escalating US-China trade war

We think pressure is building for Vietnamese technology exporters, especially computer parts and components. However, we also see a silver lining for domestic exporters of handbags, furniture and fishery products as US tariffs on Chinese imports in these categories are unlikely to be absorbed by the producers, rendering them uncompetitive vis-à-vis Vietnam.

Growth remains robust and broad-based

Vietnam’s GDP growth remains resilient

The Vietnamese economy expanded by 6.8% yoy in 2Q18 after GDP growth of 7.5% yoy in the first quarter (revised up from an initial estimate of 7.4% yoy). Vietnam’s real GDP therefore recorded robust growth of 7.1% yoy in 1H18, led by strong manufacturing activity and domestic consumption. In our previous note, we forecast GDP growth to ease in the second half of 2018. However, the latest reading on industrial activities points to sustained strength in manufacturing. According to the General Statistics Office (GSO), the IIP rose 14.3% in July and 13.4% in August, supported by stronger manufacturing and a rebound in mining activities. As expected, the debut of the Nghi Son Refinery and Petrochemical complex boosted petroleum products output by 60.5% yoy in the first eight months of 2018, bolstering manufacturing growth. Despite an escalating trade war, export growth was sustained in the Jul-Aug period with the launch of Samsung’s Galaxy Note 9 smartphone.

In addition, domestic demand remains resilient, supported by sustained high consumer confidence levels. Retail sales (ex-inflation) grew 8.5% yoy in the first eight months of 2018 vs. 8.4% in the same period the previous year. Despite a high base in 3Q17, we expect GDP growth in 3Q18 to remain strong at 6.8% yoy. Our 2018 economic growth forecast remains unchanged at 6.8% as we maintain our 4Q18 GDP forecast at 6.5%. However, we see the likelihood of a positive growth surprise in 4Q18, which could raise full-year GDP growth to 6.9%.

Depreciation pressures on the dong have eased but linger

The dong turned materially weaker from 20 July 2018. Although the DXY index appreciated only 0.4%, the dong depreciated 1.0% against the US$ over the period 20 July-13 September, largely owing to concerns about Rmb depreciation amid rising trade tensions and the recent economic turmoil in Turkey putting pressure on emerging market currencies, including the dong. Notably, the black market exchange rate broke the upper boundary of the currency band to touch 23,650 dong per US$, expanding the spread between the black market and the official exchange rate to a record high in mid-August 2018.

Figure 6 illustrates key indicators that we use to analyse the exchange rate movement. Although most trend-related indicators reflect negatively on the dong’s stability, we see pressures on the dong depreciation being contained in the short term due to the following reasons:

- Positive current account: Vietnam posted a surprise US$2.2bn trade surplus in August 2018, thanks to the recovery of telephone exports; although there were net outflows in both equity and bond markets in July-August 2018, FDI inflow has continued to support the supply side of US$.

- The People’s Bank of China (PBOC) raised its reserve requirement on some trading of foreign-exchange forward contracts from 0% to 20%, making it more expensive to short the Rmb. This is meant to be part of its counter-cyclical measures to control the Rmb depreciation.

- Sentiment on the dong has improved in the black market. In addition, the spread between the dong and US$ interbank rates has turned positive, reducing the banks’ incentive to hoard US$.

In the medium term, depreciation pressure could reappear if the US-China tariff dispute escalates into a full-blown and sustained trade war. Another risk is currency turmoil in emerging markets, especially evident in Argentina and Turkey. However, Vietnam is well equipped to weather the volatility due to a healthy balance of payments, in our view.

For now, investors are waiting for two more Fed rate hikes in the remaining months of 2018 and several more in 2019. We think policy makers could tolerate some modest depreciation in the dong amid broad US$ strength. Meanwhile, a sharp depreciation is unlikely given the lessons learnt by policy makers in August 2015 where a sharp competitive devaluation of the VND could hurt market confidence and endanger Vietnam’s economic stability. Furthermore, stiff tariffs on Chinese imports into the US imply that Vietnam does not need to match the devaluation of the Rmb to maintain competitiveness versus Chinese exports as was the case in previous rounds of competitive devaluation.

Compared to other Asian currencies, such as the Indian rupee, Indonesian rupiah and Philippine peso, which have been among the worst-performing regional currencies, Vietnam has experienced a relatively small depreciation (just 2.5% YTD). We maintain our forecast of a 3.0-3.6% full-year depreciation vs. the US$ for 2018.

Higher rate environment still on the cards

Interbank liquidity is tightening, driven by pressure on the dong

In our view, pressure on the dong has tightened banking liquidity since July 2018 because of a direct FX intervention by the central bank in selling US$. In mid-July 2018, the State Bank of Vietnam (SBV) sold nearly US$2bn worth of forex to commercial banks, which led to a fall in dong liquidity. In order to counteract this action, the SBV injected liquidity into the banking system via open market operations (OMO). However, we see that the intended neutralisation was not sufficient to bring down interbank rates. The overnight rate is currently at the highest level seen in 2018, hovering at around 4.0-4.5%.

Government bond (G-bond) yields on the rise

The Vietnam government bond market experienced a sharp decline in yields during the first half of the year due to excess liquidity in the banking system which led to easy absorption of government bond auctions. However, as liquidity has tightened and foreign investors have continued their net selling in the bond market, Vietnam bond yields have significantly recovered since the last two months. Yields on 5-year and 10-year government bonds are currently at 4.5% and 5.1%, respectively. Both yields have recovered to the same levels as at the end of last year. The yield spread between Vietnam and US government bonds widened to 212 basis points from its record low of 123 basis points in early 2018. In the primary market, demand for G-bonds has declined with the average winning ratio at around 54.3% in three recent months. Winning yields have also increased; the yield on 10-year government bond posted an increase of 34bp in 3Q18. We think a sharp drop in bond yields in the first half was largely driven by excess liquidity in the banking system. Therefore, tightening interbank liquidity led to a rebound of G-bond yields to their normal levels rather than foreign selling of bonds as was the case in many Asian emerging markets; this is largely because foreign participation in Vietnam’s G-bond market is rather limited. Nonetheless, this and yields’ rise in itself is not a clear signal for any potential policy rate hikes in the near term as yields still remain low relative to historical levels even as the policy rate has remain unchanged.

We are not too concerned about a recent rise in deposit rates

In recent months, many local banks have adjusted up their deposit rates across tenors by 10-30 basis points. There might be concerns about higher funding costs for banks, but we still believe these adjustments will not have a significant impact on local banks’ profitability as well as the outlook for lending rates. We see two main reasons for the recent hike in deposit rates: 1) the SBV only allows banks to use 40% of their short-term capital for long and medium-term loans from 2019 instead of 45% as in this year. Therefore, banks have to raise deposit rates for tenors of more than 12 months in order to attract more long term funding to meet SBV’s requirement for next year; and 2) in first half of 2018, some major banks cut deposit rates to unusually low levels because of excess liquidity. Now, with liquidity tightening, a hike in deposit rates is a necessity. In early August 2018, the SBV issued Directive No.04, which strictly controls credit growth pace and credit quality of the banking system. As the SBV communicated a more conservative monetary policy, we think the SBV has recognised the need for measures to contain rising external risks. In other words, we see SBV’s communication of their monetary policy direction as a strong signal indicating their intention to implement a tighter monetary policy in the future, even if this is accomplished without a hike in policy rates.

What do we expect?

Our observations are that the SBV has tightened by 1) reducing interventions in the OMO market; 2) requiring banks to control their lending according to credit growth limits set by the SBV; and 3) targeting credit growth at a maximum of 17% for 2018, lower than the 18.2% recorded last year. While we stress that the recovery of interbank rates and bond yields alone is not a clear signal for a hike in policy rates, it is a helpful starting point to assess the outlook for interest rates, especially from 2019 onwards. For now, domestic inflation is stable and the dong has only depreciated slightly against the US dollar. If the dong faces greater pressure and inflationary expectation rises beyond the 5.0% threshold, the SBV might be forced to hike rates. Against the backdrop of rising global uncertainty led by lingering concerns about emerging market financial turmoil, increasing global trade tensions and monetary policy tightening by the central banks in developed countries in 2019 and beyond, we believe SBV’s policy rate hike is likely to happen next year. We now project a 50bp hike in policy rates in 2019, bringing the discount rate and refinancing rate to 4.75% and 6.75%, respectively.

Emerging market financial turbulence is unlikely to have a huge impact on Vietnam

Turkey and Argentina are experiencing a bout of financial instability against the backdrop of rising US rates and the effects of a resurgent US$. The instability is evident in the sharp depreciation of the Turkish lira and Argentine peso, which have fallen by 65.0% and 105.2% YTD, respectively. Weak fundamentals, as evidenced by high inflation and sizeable current account and budget deficits have contributed to the erosion of confidence in these economies and are spurring anxiety in financial markets that tightening credit cycle conditions globally may spread to a broader set of frontier and emerging economies, including Vietnam. As we see in Figure 11, Turkey and Argentina seem vulnerable according to all indicators. For Asia frontier and emerging countries, we think a high current account deficit and high inflation rate might trigger a large currency depreciation. For Vietnam, we believe that the risk is relatively limited since Vietnam has much stronger fundamentals than Argentina and Turkey, and seems less vulnerable in its current account balance compared to other Asian countries such as Indonesia, the Philippines and India.

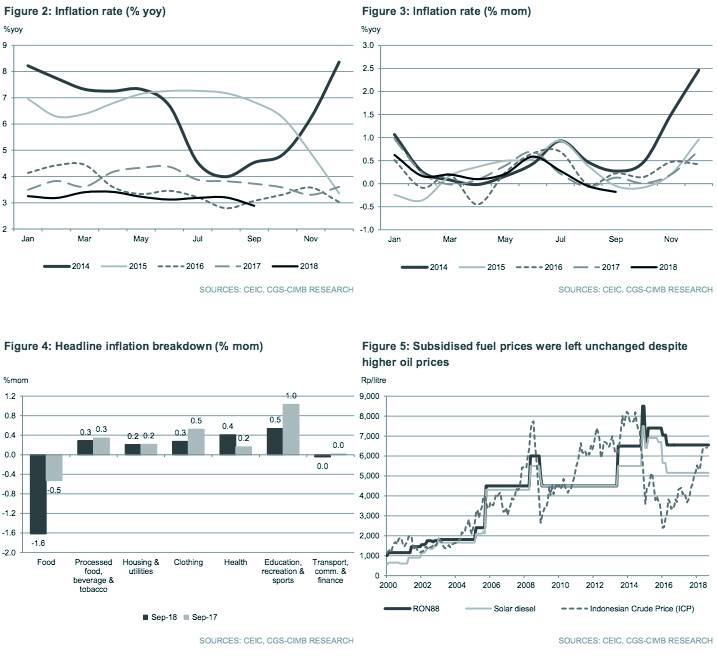

In particular, Vietnam’s August headline inflation eased to just under 4.0% from 4.5% in Jun 2018, due to a decline in government-administered healthcare costs. Although we see broad inflationary pressures in food and transportation prices, we expect administrative controls and monetary tightening from the SBV to keep inflation under control this year (the SBV’s target of below 4%). If successful, this will be well below levels seen in Argentina and Turkey. Other vulnerability indicators show a mixed picture. Vietnam is more vulnerable than peers in terms of external debt and import cover. However, it is important to note that external debt risk is contained as concessional loans account for around 40% of government guaranteed external debt. Regarding import cover, traditional “rules of thumb” that have been used to guide reserve adequacy suggest that countries should hold reserves covering 100% of short-term debt or the equivalent of three months’ worth of imports. But for FDI-dependent economies like Vietnam that operate in downstream stages of the export manufacturing value chain, we think these traditional measures of reserve adequacy have limited relevance as a sizeable portion of Vietnam’s imports are inputs for manufactured exports. If exports slow down due to a full-blown of trade war, import deceleration will follow, thereby mitigating the risk of a balance of payments crisis.

Neither Turkey nor Argentina are important export markets for Vietnam, therefore, the impact of a sharp depreciation of the Turkish lira and Argentine peso on Vietnam’s trade is not significant. However, Argentina is Vietnam’s largest source market for corn and animal feed products, accounting for 50.8% and 46.2% of total imports of these two products into Vietnam in 2017, respectively. Therefore, domestic animal feed companies (DBC VN Equity, Not Rated) could benefit from the plummeting peso, and thereby lower their production costs. Since Turkey and Argentina do not compete directly with Vietnam in terms of exports to a significant degree, we do not believe that Vietnam will lose export market share to these countries as a result of the devaluation.

The escalating US-China trade war remains the biggest unknown

In our view, the big risk that markets may not yet have fully factored in is the growing threat of a trade war between the US and China, whose effects would ripple through regional supply chains. With the US$50bn of tariffs becoming a done deal for both countries, the focus is now on the next US$200bn of Chinese goods and US$60bn of US goods that are targeted for additional tariffs. In the latest development, President Trump announced 10% tariff hikes on an additional US$200bn of Chinese goods, starting from 24 September 2018 with the tariff expected to kick up to 25% from 01 January 2019. If implemented, the latest round of tariffs would cover half of the total Chinese goods imported into the US and nearly all of US goods exports to China in 2017.

Vietnam was in the top 15 list of the US’s import partners with around US$46bn worth of imports in 2017. The US was ranked 3 rd in Vietnam’s list of top trading partners with total trade of US$51bn in 2017. China, on the other hand was Vietnam’s top trading partner with a total trade value of US$94bn in 2017. The US was Vietnam’s largest export destination in 2017 (19.4% of total exports) while China was Vietnam’s largest import partner (27.5% of total imports). In this report, we access the list of the whole package of tariffs for Chinese goods including: 1) the US$50bn that was already implemented; and 2) the proposed US$200bn awaiting official implementation by the US. In our view, the direct impact on Vietnam from the US tariff on Chinese goods is relatively insignificant for the US$50bn list as most of the products on this list are comprised of intermediate inputs and capital equipment; consumer goods made up only 1% of the list; the total value of Vietnam’s export products that are exposed to this list was around US$4.4bn, only accounting for 2.1% of Vietnam’s total exports in 2017.

However, we are concerned about the next set of tariffs worth US$200bn on Chinese goods. We estimate the total value of Vietnam’s export products that are exposed to the US$200bn list to be around US$13.5bn, which is equivalent to 29.3% of Vietnam’s total exports to the US and 6.3% of Vietnam’s total exports in 2017. In our view, the impact of the ongoing US-China trade war on Vietnam could be four-pronged:

- Direct decline in demand for intermediate goods used in the production of China’s exports to the US (negative). Indirect decline in demand for final consumer goods due to rising costs for US consumers (negative).

- Potential rise in demand for alternative sources if the US needs substitutes for Chinese goods (positive).

- Indirect impact on Vietnam’s exports to China as a result of slower Chinese economic growth denting Chinese consumption (negative).

Figures 13 &14 illustrate the types of goods subject to the US tariffs. The list has been expanded to target consumer products. Figure 15 shows the potential products from Vietnam that are exposed to the US$200bn list. Vietnam is one of the top suppliers of furniture (PTB VN Equity, Not Rated) and handbags (GIL VN Equity, Not Rated), after China. Therefore, Vietnam could become an alternative sourcing destination for the US, thereby benefiting exports. The US tariffs on Chinese agricultural products could also indirectly benefit Vietnam. In fact, Vietnam’s exports of agricultural products, fishery products (VHC VN Equity, Not Rated), vegetables & fruits will benefit the most if the US needs substitutes for Chinese imports. Moreover, these measures would directly raise the price of the Chinese goods that are subject to the tariffs and therefore encourage Vietnamese exporters to raise prices as well.

In contrast, companies that produce intermediate goods used in the production of China’s exports to the US may see softer demand. The imposition of direct tariffs on telecommunication equipment and computer exports is likely to hurt Vietnam’s exports of these products. Since some of these products are reprocessed and re-exported to China in the form of semi-finished products, tariffs on Chinese goods may harm Vietnamese exports as they might cascade up the value chain. However, in the case of telephone exports, most Vietnamese exports are final products. Therefore, the impact will not be significant, in our view. Computer parts & components might be affected the most. For other types of products (auto parts, electrical transformers, plastics, lamps, steel, aluminium), we assume that they are not sold as raw or intermediate products to be re-exported to the US. In other words, they are more subject to Chinese end consumption which could suffer indirectly due to a sharper slowdown in China’s economy due to the trade war.

Originally published by CIMB Research and Economics on 27 September 2018.

ASEAN

ASEAN’s GDP growth rate to reduce slightly in 2018 according to the latest ADO report

(26 September 2018) The latest Asian Development Outlook (ADO) report noted that Southeast Asia’s GDP growth rate for 2018 would decrease slightly to 5.1% from 5.2% in 2018. In its April report, the Asian Development Bank projected that the growth rate for Southeast Asia in 2018 would be at 5.2%. Southeast Asian growth is projected to dip slightly this year due to factors such as moderation in export growth, softer domestic demand, subdued agriculture, higher inflation, net capital outflows, and a worsening balance of payment. Of all the ASEAN countries, only Brunei Darussalam (2.0%) and Thailand (4.5%) look set to outperform the April projections for 2018. Cambodia (7.0%) and Singapore (3.1%) will likely meet April projections, according to the outlook. As for the projected growth rates in 2019, the GDP growth rates for Laos, Myanmar, Malaysia and the Philippines are expected to fall while those of Brunei, Cambodia, Indonesia, Singapore and Vietnam will remain the same. Thailand is the only nation which is forecasted to see an increase in its GDP rate (4.3%).

ASEAN

Trade war and household debt build-up to undermine ASEAN’s strong economic growth prospects

(27 September 2018) The escalating trade conflict between the United States and China and uncertain global economic climate could threaten growth prospects of Southeast Asian nations, according to the Trade and Development Report (TDR) published by the United Nations Conference on Trade and Development’s (UNCTAD). Increase in household debt and corporate debt in Southeast Asia could threaten Southeast Asia’s growth potential. Although Cambodia, Indonesia, Malaysia, Myanmar, the Philippines and Thailand had been posting strong economic growth, these nations have also raised their non-financial sector debt ratios by an average of almost 20 percentage points. Nevertheless, growth in ASEAN nations remains steady due to strong domestic demand, rising private consumption and infrastructure investments, especially in countries such as Indonesia and the Philippines. The UNCTAD report analyses current economic movements and significant international policy matters and comes up with ways to solve them.

MYANMAR

Discovery of a new well to attract oil and gas investments into Myanmar

(26 September 2018) The discovery ShweYee Htun-2 appraisal well at offshore block A-6 near Rakhine State, which can produce natural gas for commercial purposes will draw more oil and gas investments into Myanmar. Myanmar’s Ministry of Electricity and Energy (MOEE), however, did not specify the timeframe on when the profit sharing contract (PSC) for development of the well would be signed. Union Minister of the MOEE U Win Khine said the government could purchase 25% of the natural gas generated from the well for domestic consumption at a cheaper rate, but negotiations for the price still has to be made. The ministry will be inviting tenders for exploration and production activities at unoccupied and relinquished offshore and onshore oil and gas blocks during the first and second quarters of 2019.

VIETNAM

New free trade deal with EU set to see new European investors in Vietnam

(26 September 2018) Director of the Organization of La Francophonie’s Asia-Pacific office Eric-Normand Thibeault expects that once the EU-Vietnam Free Trade Agreement (EVFTA) is approved, a new generation of investors from Europe will penetrate into the Vietnamese market. According to the European Chamber of Commerce (EuroCham) in Vietnam, higher engagement from EU investors can be expected when the EVFTA takes effect. A representative from the Vietnam Central Economic Commission stated that many European investors are interested in the manufacturing sector as Vietnamese firms lack the capital and technology. Also, the free trade deal will boost Vietnam’s potential to emerge as one of the top spots in the world for investors in the garment and textile industries. Chairman of the Vietnam Textile and Apparel Association (VITAS) Vu Duc Giang said the sector attracted US$2.8 billion of FDI in the first half of 2018.

INDONESIA

Market turbulence to impact positive Indonesian bank trends

(26 September 2018) In a report by credit rating agency Fitch Ratings, Indonesia’s improvement in banks’ asset quality is likely to be affected by currency depreciation and higher domestic interest rates. However, the margins are expected to remain steady due to high core capital ratios, which will act as a shield against market pressures. The strain on the Indonesian Rupiah has seen an immediate response from Bank Indonesia (BI), which has hiked its policy rate by a cumulative 125 basis points (bps) since May 2018. Fitch expects BI to increase its policy rate by a further 25 bps in the second half of 2018 and 50 bps in 2019.

SINGAPORE

Singapore unveils new technology to facilitate cross-border trade

(26 September 2018) Singapore’s Networked Trade Platform (NTP) will enable cross-border trade connection via technology. The platform, which was launched on 26 September 2018, combines four government certification services needed for trading in and out of Singapore. NTP will also add 25 value-added services by third-party firms geared towards trade. The new platform focuses on raising productivity by digitalizing the paper trail, improve competitiveness by providing accurate data analysis and generate opportunities for third-party service providers. The NTP was developed by the Singapore Customs and the Government Technology Agency of Singapore (GovTech) over four years, and supported by over 20 ministries, government agencies and working groups.

MALAYSIA

Malaysia cautious over product dumping due to trade wars diversion

(26 September 2016) Malaysia’s International Trade and Industry Minister Darell Leiking said Malaysia will take cautious steps to avoid product dumping in the local market due to diversion from the trade wars. He also urged ASEAN member states to work together to withstand any effects from the escalating trade war between the United States and China. He said with a population of 640 million, ASEAN market has enormous potential and ASEAN countries should invite other nations to invest and trade in Southeast Asia.

THE PHILIPPINES

Remove productivity constraints to achieve poverty-free society by 2040

(25 September 2018) A World Bank report has urged the Philippines to remove limitations affecting the country’s productivity, namely restrictions on foreign investments. By doing so, it will help the Philippines to achieve its vision of a poverty-free society by 2040. In the report titled “Growth and Productivity in the Philippines: Winning the Future”, the World Bank said the Philippines would be able to generate better-paying jobs and lower poverty rate if it better uses its resources such as human capital, natural resources, technology and knowledge. The report noted that if the Philippines were to achieve its vision by 2040, it would need to triple its income per capita to around US$3,500 in the next two decades. The Philippines’ economic growth should be at an annual average of 6.5% in the next 22 years compared to its average growth rate of 5.3% since 2000.

LAOS

Government to revise Laos’ economic growth target

(28 September 2018) Laos’ government is looking to adjust its economic growth target due to global challenges. Deputy Prime Minister Somdy Duangdy said the government is unlikely to achieve the 7% growth target. In 2017, the GDP was at 6.9%, but it is now estimated to decline to 6.5%. Economic analysts from the government stated that the escalating trade conflict between the United States and China has resulted in global uncertainty in trade, investment, finance. According to a recent report by the Asian Development Bank (ADB), Laos economic growth is set to moderate in 2018 because sectors such as mining and agriculture are expected to underperform.

THAILAND

Bangkok is the top destination for international overnight visitors in 2017

(28 September 2018) The seventh annual Mastercard Global Destination Cities Index (GDCI) ranked Bangkok as the No.1 global destination city for international overnight visitors in 2017, the fifth time in six years. Phuket and Pattaya were listed in the global top 20 destination cities at 12th and 18th positions, respectively. With 20.05 million international overnight visitors in 2017, Bangkok edged out London with 19.83 million visitors. Thailand’s Tourism and Sports Ministry projected that 37-38 million foreigners would be travelling to the country in 2018 and it is expected to generate US$61.8 billion in tourism revenue. According to the ministry, in the first eight months of 2018, 25.88 million foreign tourists visited Thailand, a 9.9% increase from the same period last year, generating US$41.7 billion, an increase of 12.9% year-on-year.

HIGHLIGHTS

August 2018 industrial production

- Singapore’s industrial production index (IPI) expanded 3.3% yoy in August

- The country recorded weaker readings in the electronics, biomedical, petrochemical and transport engineering clusters.

- We expect MAS to stand pat on its monetary policy in October due to Singapore’s weaker growth profile and benign inflation outlook in 2H18F.

Momentum in manufacturing sector slows in August

The IPI softened to 3.3% in August, below market expectations (CGS-CIMB: +3.9% yoy, Bloomberg consensus: +4.7% yoy, Jul: +6.7% yoy). Manufacturing activity ex biomedical rose at a slower clip of 3.0% yoy in August (+5.8% yoy in July). On a seasonally-adjusted basis, the IPI declined further by 2.0% mom, after contracting 1.2% mom in July.

Electronics IPI moderates further but semiconductor rebound

The streak of slowing electronics output growth prolonged into a third straight month in August (+3.6% yoy vs. +5.1% yoy in Jul), dragged down by computer peripherals (-27.0% yoy), data storage (-13.5% yoy) and consumer electronics (-3.3% yoy). The pick-up in semiconductors (+7.8% yoy), which account for 62% of the electronics cluster, and other electronic components (+19.4% yoy) were silver linings, reinforcing improvements in Singapore’s forward-looking electronics PMI (52.0 in August vs. 51.6 in July) and new orders (53.5 in August vs. 52.9 in July).

Slower demand deals a blow to biomedical cluster

Biomedical manufacturing output eased sharply in August (+4.2% yoy vs. +10.4% yoy in July), pulled down by lower production of pharmaceutical & biological products (+8.7% yoy vs. +14.1% yoy in July), as well as contraction in the medical technology segment (-8.2% yoy vs. -0.1% yoy in July).

Mixed performance across other industries

Gains in the chemical sector toned down in Aug (+5.7% yoy vs. +7.6% yoy in July), despite robust growth in specialty chemicals (+14.2% yoy), as petrochemical capacity was idled by plant maintenance shutdowns resulting in output declining 2.4% yoy. Precision engineering production picked up in August (+5.6% yoy vs. +2.4% yoy in July), driven by a sharp uptick in optical instruments. Meanwhile, transport engineering output eased to 4.7% yoy in August (+16.2% yoy in July) due to slower activity in land transport and aerospace.

Sticking to the script

The consensus view on the Monetary Authority of Singapore’s (MAS) next course of action is mixed, with markets split between calling for a pause on or a further tightening of its monetary policy. We tilt to the view that MAS will retain its guidance for a ‘modest and gradual’ appreciation of the S$NEER in October given the weaker growth profile and benign inflation outlook in 2H18F.

Originally published by CIMB Research and Economics on 27 September 2018.

Photo Credit: National Public Radio

TRADE, ECONOMY, AND INVESTMENT

MEKONG

Thai government mulls cross-border trade zone in the Golden Triangle

(24 September 2018) The Thai government is conducting a feasibility study to set up a cross-border economic zone in the Golden Triangle area under the Lancang-Mekong Cooperation scheme, which would enhance economic links for Thailand, Myanmar, Laos and China. The Director-general of the Trade Negotiations Department Auramon Supthaweethum said his department would be looking at a location in Chiang Rai, Thailand, for the zone and this matter would be discussed with the Thai Chamber of Commerce and the Federation of Thai Industries in October 2018. The Lancang-Mekong Cooperation framework was introduced in 2015 in order to advance multifaceted cooperation at the sub-regional level among Cambodia, China, Laos, Myanmar, Thailand and Vietnam. Under the cooperation scheme, these countries seek to boost trade to US$250 billion by 2020. In 2017, the trade value in the region was at US$220 billion, and growth was at 16% year-on-year.

Read more>>

VIETNAM

Vietnam’s Ministry of Planning and Investment (MPI) to stop granting investment certificates for foreign firms that use old technology

(25 September 2018) The Vietnamese government would not issue investment certificates for projects using old technologies which could affect the environment. The Minister of Planning and Investment Nguyen Chi Dung said Vietnam is currently prioritising high-quality foreign direct investment (FDI), which emphasises environmentally friendly projects using new technologies that are in line with the Fourth Industrial Revolution. The Ministry of Planning and Investment (MPI) tasked the relevant government agencies to be stringent when issuing investment certificates. The agencies would also inspect, examine and supervise foreign investments involving vast lands and utilising the minimum investment rates. According to the Foreign Investment Agency (FIA) under MPI, FDI commitments in Vietnam in 2017 was at US$35.9 billion which was equivalent to an increase of 44.4%. FDI commitments was US$24.35 billion in the first eight months of 2018, up 4.2% year-on-year. Up to 20 August 2018, disbursement of FDI projects increased to US$11.25 billion, a jump of 9.2% year-on-year.

Read more>>

CAMBODIA, THAILAND

Cambodia-Thailand trade hits US$4 billion in the first seven months of 2018

(22 September 2018) According to a report provided by the Thailand embassy in Cambodia, the trade volume between both countries was US$4.6 billion in the first seven months of 2018. It is an increase of 34.4% compared to the first seven months of 2017. Cambodia’s imports of goods and services from Thailand was worth US$4.1 billion during the first seven months of 2018, an increase of 40.6% compared to 2017, but Cambodia’s exports to Thailand decreased 1.2% from US$506 million in 2017 to US$ 500 million in 2018.

Read more>>

THAILAND

World Bank reports that safer roads could boost Thailand’s GDP by 22%

(24 September 2018) A World Bank report said Thailand should ensure that its roads are safe in order to achieve long-term economic growth. The report entitled “The High Toll of Traffic Injuries: Unacceptable and Preventable” indicated that if road traffic injuries in Thailand could be brought down by 50% and adequate road safety were to be maintained for 24 years, the country’s GDP would increase by 22%. According to the Thai Road Safety Centre, 15,256 people died in road accidents in 2017. Nearly 79% of the deceased were males and most were from 16 to 25 years old. A researcher of the World Bank report said that if the road-accident casualty rate could be reduced from now to 2038, 138,168 deaths could be prevented. This would result in an increase of income equivalent to 22.2% of Thailand’s 2014 GDP.

Read more>>

MYANMAR

International firms invited to tender bids for BRI projects

(21 September 2018) Myanmar’s Union Minister of Commerce U Than Myint has called upon foreign enterprises to tender bids for the Belt and Road-related projects in Myanmar and assured investors that the process would be conducted transparently and fairly. He said China would be providing loans for the projects, but international investors and development agencies will be invited to take part in the implementation process. Recently, Myanmar and China inked a Memorandum of Understanding (MoU) on the establishment of the China-Myanmar Economic Corridor (CMEC), which is a key part of the Belt and Road Initiative (BRI) routes. Myanmar’s Ministry of Planning and Finance said that it signed an “umbrella agreement” with China while agreements on individual projects will have to be negotiated by the respective ministries in future. The CMEC covers a highway development from China’s Yunnan Province to Kyaukphyu via Mandalay and the Mandalay-Yangon-Mawlamyine route, as well as collaborations in 15 sectors including infrastructure development, investment, energy, agriculture and tourism.

Read more>>

About Greater Mekong Subregion (GMS)

The Greater Mekong Subregion (GMS) Economic Programme was launched by the Asian Development Bank in 1992 connecting five developing ASEAN countries, namely Cambodia, Laos, Myanmar, Vietnam and Thailand, and Chinese provinces of Yunnan and Guangxi Zhuang Autonomous region. The region has some of the most robust economies sharing the Mekong River Basin thanks to its reform and liberalisation. The subregion is growing at a faster pace than the whole of East Asia and the Asia Pacific as the GDP growth rate for 2017 was at 6.4 percent, according to the World Bank. The population at the subregion as of 2016 is at 340 million while the GDP at PPP is at US$3.1 trillion in 2016. In 2015, trading within the region was at US$444 billion.

Photo credit: The National Interest

Economy, Investment and Trade

Philippines and Fujian look to boost economic relations

(22 September 2018) The Philippines is looking to improve its economic ties with the Chinese province of Fujian. During a business networking conference organized by the Fujian government, Trade Secretary Ramon M. Lopez urged businesses from Fujian to expand operations in the Philippines, as the Philippines’ macroeconomic fundamentals are strong and the government is initiating reforms to help companies to do business. Filipino and Chinese firms inked 15 cooperation and joint-venture agreements during the conference and those agreements cover industry, agriculture, tourism and real estate. Fujian governor Tan Dengjie said the Philippines is a crucial investment point for Fujian. China and the Philippines’ bilateral relations have improved under Philippines President Rodrigo Duterte and in 2017, China was billed as the Philippines’s top trading partner, fourth- largest export market and top import supplier. Philippine exports to China grew by 25.81 per cent, from US$6.37 billion in 2016 to US$8.02 billion in 2017.

Read more>>

China and Singapore sign seven agreements on arts, entrepreneurship and intellectual property

(20 September 2018) China and Singapore sealed seven bilateral cooperation agreements on arts, entrepreneurship, intellectual property and research during the 14th Joint Council for Bilateral Cooperation (JCBC) co-chaired by Singapore’s Deputy Prime Minister Teo Chee Hean and Chinese Vice-Premier Han Zheng. Several parties signed and exchanged six Memorandums of Understanding (MOU) and one Strategic Framework Agreement during the event on 20 September 2018. Some of the initiatives under the agreements are the replication of Tianjin Eco-city government-to-government project; exchanges and cooperation between artists and art groups from China and Singapore; establishment of a National University of Singapore research institute in Chongqing; and collaboration in industries such as advanced manufacturing, biomedicine and nanotechnology applications.

Read more>>

Malaysia and China’s bilateral trade increases 10.5 per cent in 2017

(25 September 2018) Bilateral trade between Malaysia and China was at US$96 billion in 2017, which is an increase of 10.5 per cent compared to the previous year, according to Sabah Director of the Malaysia External Trade Development Corporation (Matrade) A. Rashid Mohd Zain. It also accounts for 18.7 per cent of accumulated trade between China and ASEAN. A. Rashid disclosed that high-quality Malaysian products and goods are highly sought after by the Chinese market. The Chinese government is encouraging reputable companies from Malaysia to develop two-way investment. With the escalating trade war between China and the United States, China is keen to work with ASEAN member states including Malaysia to protect global free trade.

Read more>>

First continuous beam block construction for China-Laos Railway completed on the Mekong River

(22 September 2018) The concrete casting for the first block of the Luang Prabang Bridge, which is part of the China-Laos Railway, was completed on 17 September 2018. CPC party secretary of the China Railway No.8 Engineering Group (CREC-8)’s railway project department Yan Haiyong said that the 1.46 km railway bridge, is an integral part of the railway project. He said the beam block is built on a stringent technical standard. The length of the block is 12 metres, and it consumes a concrete volume of 266 cubic metres. The China-Laos Railways is the CREC-8’s first foreign railway project and also the first to connect with China’s railway network. The project is 414 km long and is set to be completed by December 2021.

Read more>>