Indonesia: September 2018 BI meeting

HIGHLIGHTS

September 2018 BI meeting

- Bank Indonesia (BI) lifted its policy rate by 25bp after a similar move by the US Federal Reserve (US Fed) overnight.

- BI to issue guidelines for domestic non-deliverable forward (DNDF) as a new hedging instrument to deepen the onshore foreign exchange market.

- We expect another 25bp increase in policy rate to 6.00% in 4Q18F, following closely in the US Fed’s footsteps, to allay the downward pressure on rupiah.

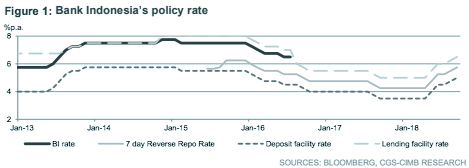

The fifth rate hike in less than five months…

Bank Indonesia (BI) raised its 7-day Reverse Repo Rate (7DRRR) by 25bp to 5.75%, in line with the Bloomberg consensus expectation, but against our forecast of no change. This represents the fifth hike in less than five months, amounting to 150bp cumulatively

… amid continued monetary policy normalisation in the US

The decision followed the 25bp increase in the Federal Funds Rate (FFR) to 2.00-2.25% by the US Fed overnight. Despite brewing US-China trade tensions, the Fed maintained its FFR projection through 2020F, which translates into one more rate hike before yearend, three in 2019F and one in 2020F. In the Philippines, the central bank raised its policy rate further by 50bp on 27 September 2018 amid risks arising from inflation, currency weakness and a current account deficit.

Expansion of hedging instruments to deepen forex market

BI announced the launch of domestic non-deliverable forwards (DNDF) as a new hedging tool for companies and investors as a means to curb rupiah volatility. The settlement of DNDF will be done in the domestic foreign exchange market and in rupiah, and the DNDF must be backed by underlying transactions such as investments, exports or imports.

Import-reduction measures

The reluctance of the government to mitigate a surging O&G trade deficit by raising fuel prices ahead of the Presidential election in April 2019 suggests that the current account deficit (CAD) remains a key risk. While we see the postponement of import-intensive projects, which directly lowers imports of capital goods, as more effective in reducing CAD, the impact may only be realised in 2019F. The impact from the import tax hike will be small as the affected goods only account for ~4% of total imports, whereas the expansion of the B20 biodiesel mandate to the non-public service obligation (PSO) sector and the domestic sale of crude oil to Pertamina are limited remedies for the CAD, in our view, as they translate into lower O&G and CPO exports. BI sees CAD at 2.5% of GDP in 2019F, compared to 2.6% of GDP in 1H18.

Hawkish stance stays; 7DRRR to reach 6.00% by end-2018F

BI’s monetary policy stance remains hawkish amid continued monetary policy normalisation in the US. The reliance on external financing and high foreign participation in the government bond market imply the need to maintain attractive yield differentials. As the US Fed is primed for a further 25bp FFR increase in December, we expect BI to react with a 25bp rate increase in 4Q18F, sending the policy rate to 6% by the end of the year.

Originally published by CIMB Research and Economics on 27 September 2018.