Thailand: Macro snapshot

HIGHLIGHTS

Macro snapshot

- External demand retreat weighs on trade surplus and manufacturing activity.

- Balance of payments surplus and return of foreign portfolio inflows halt 4- month slide in the baht.

- Constructive growth outlook, budding inflation and financial stability concerns are shepherding BOT towards mild monetary policy tightening in 2019F.

Export-driven manufacturing engine sputters in August

In August, sliding export growth (+5.8% yoy vs. +8.3% yoy in July) and higher imports (+24.2% yoy vs. +12.4% yoy in July) trimmed the trade surplus to US$604m (vs. US$858m in July). Manufacturing production index gains ebbed to the slowest pace since April 2017 (+0.7% yoy in August vs. +4.9% yoy in July) due to setbacks in export-oriented sectors like autos, rubber & plastics, chemicals, apparel, HDD and refined petroleum. Correspondingly, capacity utilisation decreased to 68.5% in August (69.1% in July).

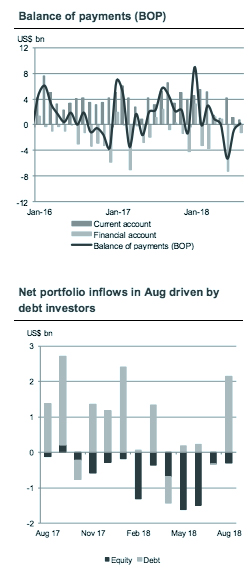

First BOP surplus since May takes pressure off the baht

A narrower trade surplus, tepid gains in tourist arrivals and weaker net income inflows depressed the current account surplus to a 4-year low (+US$0.8bn). Although the financial account registered a greater deficit (-US$1.2bn in August vs. -US$0.4bn in July), strains from the capital markets eased as foreign portfolio inflows turned positive for the first time in five months. Aided by a gentler drag from errors and omissions, the balance of payments (BOP) turned positive for the first time in three months (US$0.2bn in August), easing pressure on the Thai baht, which appreciated 1.5% against the US dollar in August after weakening by 6.6% in April-July.

Gains in consumer spending to cushion external slowdown

Trade conflicts come into sharper focus from September as markets monitor the fallout following the US’s decision to push ahead with 10% tariffs on US$200bn of imports from China. The data out turn in July-August already suggests minor slippage in the industrial and external sectors. Despite external risks, Thailand’s growth profile has been bolstered by the recovery in private consumption, though gains remain unevenly skewed to higher income households as evidenced by higher demand for durable goods vs. non-durable goods.

Anticipation builds for monetary policy normalisation in 2019F

We think the pieces are starting to fall into place for the Bank of Thailand (BOT) to tighten monetary policy mildly in early 2019F. The central bank’s constructive view on the economic recovery, quickening inflation (headline CPI: +1.6% yoy in August vs. +1.5% yoy in July) and renewed concerns that low interest rates are sowing the seeds for excessive risk-taking, particularly in the property sector, prompted more support within the Monetary Policy Committee to raise interest rates. Nonetheless, policy rate hikes are likely to be very gradual and we have just two 25bp increases penciled in for 2019F.

Less fiscal support in FY2019

On 30 August, the National Legislative Assembly (NLA) after the second and third readings approved the budget that will finance FY2019 beginning 1 October. Under the budget, revenue was estimated at THB2.55tr or 2% above FY2018R while current expenditures were projected at THB2.26tr (+1.1%) and capital expenditures at THB660bn (-2.4%). Following the stimulus package enacted earlier this year, the government intends to pull back on fiscal support, targeting a narrower budget deficit of THB450bn (-2.6% of GDP) in FY2019 (vs. THB550bn or -3.4% of GDP in FY2018). As the output gap wanes and inflation accelerates next year, we expect the Bank of Thailand (BOT) to begin tightening monetary policy in early-2019 and reiterate our end-2018 policy rate forecast at 1.50%.

Originally published by CIMB Research and Economics on 1 October 2018.