Captures has widened its scope to include news related to all the members of the Regional Comprehensive Economic Partnership (RCEP) agreement which was signed towards the end of 2020. Besides the ASEAN Member States, this includes Australia, New Zealand, China, Japan, and South Korea. The other weekly newsletters under CARI, China-ASEAN Monitor and Mekong Monitor will also be consolidated into the Captures newsletter. We hope this new version of Captures will serve you better and look forward to providing a curation of stories relevant to ASEAN and its trading partners.

THAILAND, CAMBODIA

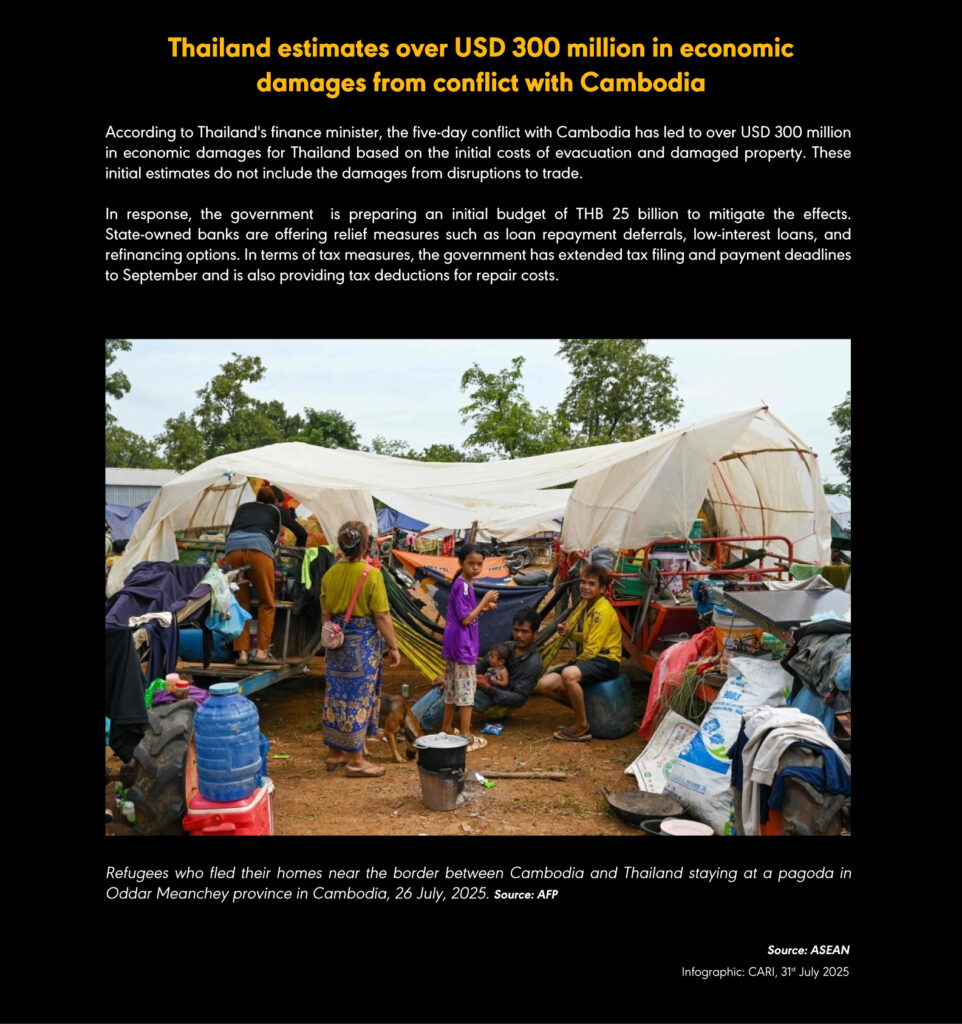

Thailand estimates over USD 300 million in economic damages from conflict with Cambodia

(29 July 2025) Thailand’s Finance Minister stated on 29 July that the initial costs of evacuation and property damage following the five-day border conflict with Cambodia exceed THB 10 billion (USD 300 million), with broader economic impacts expected. The government is preparing a THB 25 billion budget to support reconstruction and stimulate the economy, including support for repairing infrastructure and housing. The Finance Minister noted this figure may be revised upward, particularly once trade disruption costs are fully accounted for. Relief measures being offered by state-owned banks include loan repayment deferrals, low-interest financing, refinancing schemes, and exemptions from banking fees. Tax relief includes extended filing and payment deadlines until September and deductions of up to THB 100,000 for home repairs and THB 30,000 for vehicles. Additionally, THB 100 million has been allocated to each affected province to address local needs, with the possibility of further disbursement.

THAILAND

Finance Ministry revises its 2025 GDP growth forecast to 2.2% from 2.1%

(30 July 2025) Thailand’s finance ministry revised its 2025 GDP growth forecast to 2.2% from 2.1%, supported by strong first-half performance, though it warned of potential deceleration due to U.S. tariffs ranging from 15% to 36%. Export growth is now projected at 5.5%, up from 2.3%. The Bank of Thailand recently adjusted its own growth forecast to 2.3%, near last year’s 2.5%. The Fiscal Policy Office indicated the economic impact from the Cambodian border conflict is minimal, with border trade comprising just over 1% of total exports, though the labour market may be affected due to the 12% share of Cambodian migrant workers. The Industry Ministry estimated exports to Cambodia could decline by THB 60 billion, noting most Cambodian workers in Thailand are unregistered. The Finance Minister confirmed the conflict has not disrupted trade negotiations with the U.S., with a final trade proposal expected to be submitted by 30 July. The Finance Minister expressed hope for a reduced tariff rate, citing lower negotiated levels by Vietnam (20%) and Indonesia (19%). The finance ministry also reduced its 2025 foreign tourist arrival forecast to 34.5 million, down from 36.5 million, compared to the pre-pandemic peak of nearly 40 million in 2019.

SINGAPORE

Straits Times Index marks its longest losing streak in five weeks

(30 July 2025) Singapore’s Straits Times Index declined for the fourth consecutive session on 30 July, falling 0.2 per cent to 4,219.41, marking its longest losing streak in five weeks amid slower second-quarter employment growth. Advance estimates from the Ministry of Manpower showed total employment rising by 8,400, down from 11,300 in the same period last year, with softness noted in outward-oriented sectors. DBS cautioned that labour market conditions may deteriorate further in the second half due to weakening demand in trade-exposed industries. The Monetary Authority of Singapore left monetary policy settings unchanged at its quarterly meeting but warned that global growth momentum is expected to slow through the remainder of 2025 as front-loaded activity wanes and deferred tariffs take effect. Market breadth was negative, with 342 losers versus 222 gainers, and SGD 2.1 billion worth of securities traded. Singapore Airlines led STI losses, falling nearly 2% to SGD 6.90, while Yangzijiang Shipbuilding rose 3.6% to SGD 2.62. Among local banks, DBS declined 0.7% to SGD 48.26, UOB dropped 0.8% to SGD 36.52, and OCBC was unchanged at SGD 17.04.

INDONESIA

Indonesia preparing third stimulus package in 2025 amidst slowing economy

(29 July 2025) Indonesia is preparing a third stimulus package in 2025 aimed at supporting regional economies, domestic tourism, and transportation, with full details to be released by the Coordinating Ministry for Economic Affairs. Indonesia’s Finance Minister reaffirmed the government’s commitment to maintaining GDP growth near 5%, though DBS and other analysts project growth easing to 4.8% this year, citing weaker consumption, falling foreign direct investment, and global trade risks, including U.S. tariffs. The stimulus will exclude wage subsidies, which end in August, and DBS warns this could blunt its impact, especially for low-income households. The economy grew 4.87% in Q1, the slowest first-quarter growth in over three years, and FDI dropped 6.95% year-on-year in Q2 to IDR 202.2 trillion—the sharpest decline in five years. Bank Indonesia cut rates by 75 basis points so far this year and plans further measures to boost liquidity, though economists argue monetary easing alone is insufficient. President Prabowo is targeting 8% growth through programmes including 3 million homes annually and free school meals, supported by extended property tax breaks. However, economists warn that fiscal constraints, limited stimulus coverage, and structural challenges such as regulatory uncertainty and high logistics costs are dampening investment and household spending. Proposals involving state-directed lending and subsidised housing loans risk undermining financial stability.

MALAYSIA

US to announce trade deals with Malaysia, Thailand, and Cambodia

(31 July 2025) Prime Minister Anwar Ibrahim stated that Malaysia is awaiting an official announcement from U.S. President Donald Trump on 01 August regarding the country’s tariff rate under ongoing trade negotiations, which must be finalized before higher tariffs take effect on 01 August. Anwar confirmed he spoke directly with Trump, who commended Malaysia’s involvement in mediating the recent Thai-Cambodian conflict. Malaysia, previously facing a 25% tariff, has concluded negotiations, and a joint statement is expected from the U.S. Trade Representative and Malaysia’s Ministry of Investment, Trade and Industry. Trade Minister Zafrul Aziz confirmed the deal is finalised pending Trump’s formal response. The U.S. has agreed to 19% and 20% tariffs with the Philippines and Viet Nam respectively, while transshipped goods face a 40% levy. Cambodia and Thailand also reached agreements following ceasefire talks, though Cambodia’s Deputy Prime Minister denied knowledge of a final deal. Singapore will face a 10% baseline tariff with no sectoral exemptions, which Prime Minister Lawrence Wong described as manageable. Trump has confirmed attendance at the ASEAN Summit in Kuala Lumpur in October, which Malaysia will chair.

MALAYSIA, SINGAPORE

Johor town Kluang eyes spillovers in investments and businesses from Johor-Singapore Special Economic Zone (SEZ)

(31 July 2025) Since the Johor-Singapore Special Economic Zone (SEZ) was formalised in January, Kluang—located over 100km from Johor Bahru—has seen a 30% rise in investor and business enquiries, especially in manufacturing, logistics and tourism. Businesses such as Kluang Coffee Powder Factory and logistics firm SSAT are expanding capacity and projecting sales increases of up to 50% and 15% respectively. Local authorities have identified Kluang as a potential satellite city to the SEZ, with infrastructure upgrades including the Gemas-Johor Bahru Electrified Double Track Project and RTS Link expected to enhance connectivity and position Kluang as a logistics hub. Land costs in Kluang remain competitive at MYR 158 per sq ft compared to MYR 393 in Johor Bahru. However, business leaders have warned of potential infrastructural strain and called for comprehensive zoning and infrastructure planning. Agro-tourism operators such as Zenxin Organic Park and UK Farm anticipate long-term gains if the SEZ incorporates agritechnology and food production. Other Johor districts such as Muar, Batu Pahat, and Segamat are yet to see significant spillover but have been identified as potential secondary beneficiaries depending on transport connectivity and local sector strengths. Johor recorded MYR 30.1 billion in approved investments in Q1 2025, the highest in Malaysia, and the state government continues to emphasise equitable development across all 10 districts.

INDONESIA

Trade surplus projected to decline to USD 3.45 billion in June 2025

(31 July 2025) Indonesia’s trade surplus for June is projected to have declined to USD 3.45 billion from USD 4.3 billion in May, according to a Reuters survey of 17 economists. The anticipated narrowing is attributed to a 6.5% year-on-year increase in imports, up from 4.14% in May, alongside a continued rise in exports, which are expected to have grown 10.41% in June, compared to 9.68% the previous month. The country has maintained a monthly trade surplus since 2020, though the surplus has been gradually moderating amid weakening global demand. The official figures, along with July’s consumer price index data, will be released by Indonesia’s statistics bureau on Friday.

RCEP Monitor

CHINA

Private home prices remained effectively flat in June 2025

(30 July 2025) Hong Kong private home prices remained effectively flat in June, rising 0.03% month-on-month following an identical increase in May, according to the Rating and Valuation Department. This follows a 0.5% rise in April, which ended a four-month decline. Year-to-date, prices have fallen 0.9%, reaching their lowest level since 2016 and reflecting a nearly 30% drop from the 2021 peak. The recent stabilisation is attributed to more affordable mortgage rates, with the one-month HIBOR falling below 1.2% since May, down from over 3.5% during the past two years. Despite the removal of property purchase restrictions and relaxed down payment rules in 2023, demand has remained subdued amid a weak economic outlook and emigration of professionals. Brokerages such as Morgan Stanley and HSBC forecast a market bottom, while realtor JLL maintains a negative outlook, projecting a 5% decline in mass residential prices this year and no sustained recovery until 2026, when housing inventory is expected to normalise. Market forecasts for 2025 remain mixed, with potential price movements of ±5% depending on interest rate trends and U.S.-China trade tensions.

CHINA

China’s manufacturing sector contracts for fourth consecutive month in July

(31 July 2025) China’s manufacturing sector contracted for the fourth consecutive month in July, with the official Purchasing Managers’ Index (PMI) falling to 49.3 from 49.7 in June, below the 50-point threshold indicating growth, and underperforming Bloomberg’s forecast. The National Bureau of Statistics attributed the decline to seasonal factors and adverse weather, including floods and high temperatures, while Capital Economics highlighted softening demand and falling new export orders, citing renewed tariff pressures. Domestic demand also showed signs of weakness amid persistent challenges such as low consumption, youth unemployment, and a property sector debt crisis. The manufacturing slowdown coincided with stalled trade negotiations between China and the US, as a 90-day tariff truce nears expiry on 12 August without a new agreement in place.

SOUTH KOREA, UNITED STATES

US announces trade agreement with South Korea with 15% tariffs set on Korean exports

(30 July 2025) U.S. President Donald Trump announced a “Full and Complete” trade agreement with South Korea that sets a uniform 15% tariff on South Korean exports to the U.S., including a reduction from the previously threatened 25% on auto exports. As part of the deal, Trump stated South Korea would provide USD 350 billion for U.S.-owned and controlled investments, although Seoul described this as a facilitation fund for Korean firms entering U.S. sectors such as shipbuilding, semiconductors, batteries, biotechnology, and energy. Of the total, USD 150 billion is earmarked for shipbuilding cooperation. U.S. Commerce Secretary Howard Lutnick claimed 90% of the investment’s profits would benefit Americans. The agreement follows a similar investment-based deal with Japan, which remains under dispute. South Korea resisted U.S. demands to open its beef and rice markets but did not secure concessions on steel or semiconductors. Additionally, Seoul agreed to purchase USD 100 billion in U.S. LNG and energy products. Trump confirmed U.S. exports to South Korea would remain tariff-free. The deal raises questions over the relevance of the existing U.S.-South Korea FTA, which had already eliminated most tariffs. South Korea’s goods trade with the U.S. in 2024 totalled over USD 197 billion, with a USD 66 billion U.S. trade deficit. South Korea’s Kospi index rose 0.5% following the announcement.

|

15 participating countries |

20 chapters |

2.2 billion |

US$26.2 trillion |

28% |

| ASEAN member states, Australia, China, Japan, South Korea, New Zealand | trade in goods and services, investment, intellectual property, e-commerce, competition, SMEs, economic and technical cooperation, and government procurement | combined population, 30% world’s population | combined GDP, 30% global GDP | global trade (based on 2019 figures) |