Singapore: September 2018 trade

HIGHLIGHTS

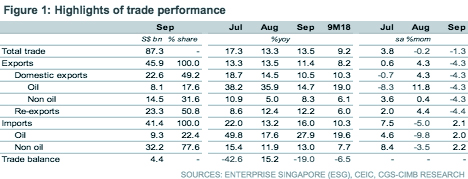

September 2018 trade

- NODX jumped to 8.3% yoy in September after a slower gain of 5.0% yoy in August due to sturdier growth in pharmaceuticals and narrower contraction in electronics.

- MAS raised the slope of the S$NEER policy band last week, confident that the economy is well-placed to weather bumpier external conditions.

- We expect a slight bias for tighter monetary settings at the April policy review.

MAS steepens S$NEER slope

The Monetary Authority of Singapore (MAS) increased the slope of the S$ nominal effective exchange rate (NEER) slightly, while keeping the width and centre of the policy band unchanged, marking a second successive tightening of monetary policy following its April review.

NODX regains momentum in September

Non-oil domestic exports (NODX) expanded at a more robust pace of 8.3% yoy in September (+5.0% yoy in August), driven by faster non-electronics NODX growth (+11.9% yoy in September vs. +7.8% yoy in August), which offset the continued contraction in electronics NODX (-0.9% yoy in September vs. -1.5% yoy in August). The seasonally-adjusted NODX declined 4.3% mom (+0.4% mom in August).

Integrated circuits’ exports break 9-month streak of declines

The collective exports of the five largest electronic items improved by 0.5% in September (-1.2% yoy in August) largely contributed by a jump in growth of integrated circuits (ICs) segment (+11.7% yoy in September) after a 9-month decline. This was sufficient to offset the declines in disk drives (-36.0% yoy), PCs (-22.7% yoy), PC parts (-18.9% yoy), parts of ICs (-41.7% yoy), consumer electronics (-17.9% yoy) and diodes & transistors (-22.5% yoy).

Pharmaceuticals and organic chemicals jump in to the rescue

Healthy non-electronics NODX growth reflected a strong uptick in the chemicals segment (+23.3% yoy), led by strong bump up in pharmaceutical (+67.5% yoy in Sep vs. +33.4% yoy in August) and organic chemical shipments (+63.3% yoy in September vs. +17.7% yoy in August), offsetting a contraction in petrochemical exports (-1.5% yoy in September vs. +3.4% yoy in August).

External demand still driven by advanced economies

The main contributors to NODX in September were the US (+41.5% yoy), the EU (+21.6% yoy) and Thailand (+46.8% yoy). On the other hand, shipments to China weakened (-17.8% yoy), as did exports to regional economies like South Korea (-10.9% yoy), Malaysia (- 4.6% yoy), Taiwan (-4.2% yoy), Hong Kong (-1.1% yoy) and Japan (-1.5% yoy).

Softening external demand may not deter MAS tightening in April

External demand conditions are softening as trade conditions enter a period of uncertainty amid unresolved trade conflicts between the US and China. The SIPMM PMI gauge of the manufacturing and electronics sector decreased by 0.2pt and 0.6pt to 52.4 and 51.4 respectively in September. An alternative Nikkei Singapore PMI fell even more sharply by 1.5pt in September to 49.6, the lowest reading in over two years, weighed down by declines in output, new orders and export sales. The data outturn is in line with our view that Singapore’s GDP growth is likely to slow from an estimate of 3.2% in 2018 to 2.6% in 2019. Nonetheless, the growth and inflation outlook may still nudge the Monetary Authority of Singapore (MAS) into another round of slight S$NEER policy tightening in April 2019.

Originally published by CIMB Research and Economics on 17 October 2018.