CARI Captures Issue 754: Extreme El Niño weather patterns to impact rice and palm oil production in Southeast Asia

Captures has widened its scope to include news related to all the members of the Regional Comprehensive Economic Partnership (RCEP) agreement which was signed towards the end of 2020. Besides the ASEAN Member States, this includes Australia, New Zealand, China, Japan, and South Korea. The other weekly newsletters under CARI, China-ASEAN Monitor and Mekong Monitor will also be consolidated into the Captures newsletter. We hope this new version of Captures will serve you better and look forward to providing a curation of stories relevant to ASEAN and its trading partners.

ASEAN

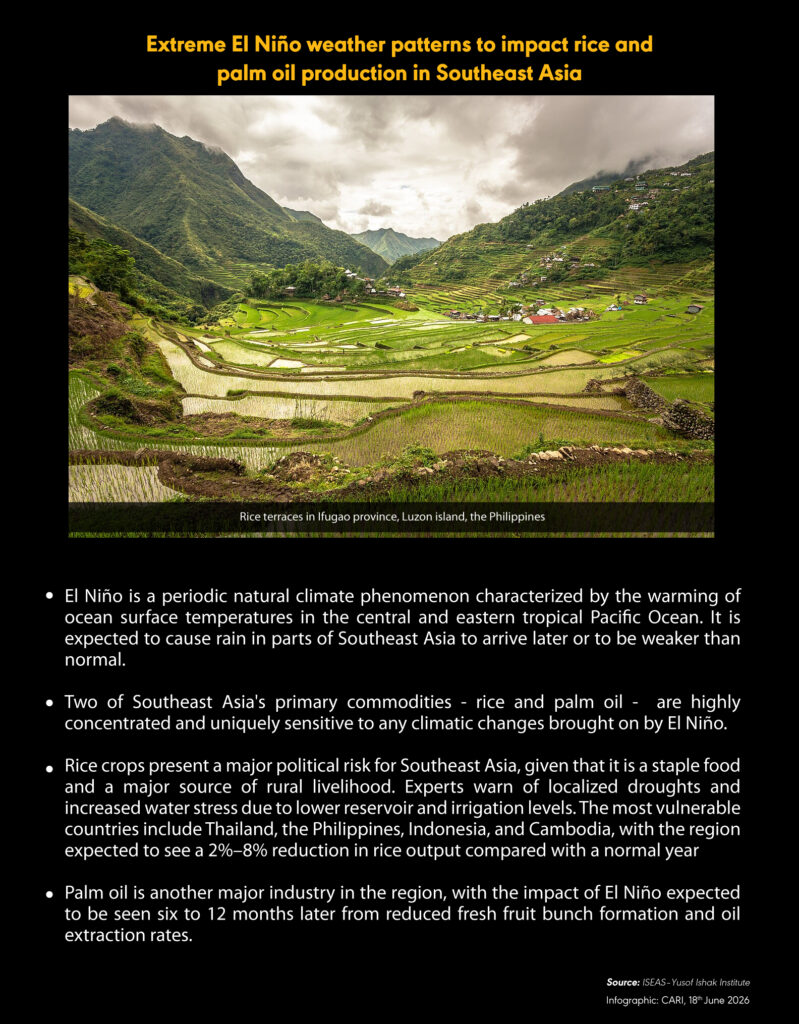

Extreme El Niño weather patterns to impact rice and palm oil production in Southeast Asia

(15 June 2026) Southeast Asia is expected to face El Niño conditions before August, with the World Meteorological Organization forecasting the pattern to persist until at least November, increasing the risk of hotter and drier weather across the region. Experts warned that delayed or weaker monsoon rains could disrupt agricultural production, particularly for rice and palm oil, two commodities highly concentrated in Southeast Asia that are especially vulnerable to climate shocks. The ISEAS–Yusof Ishak Institute said rice output could decline by 2%–8% compared with a normal year, with Thailand, the Philippines, Indonesia and Cambodia most exposed. Palm oil supply, particularly in Indonesia and Malaysia (both of which account for about 85% of global palm oil supply), could also face reduced production, although impacts may emerge six to 12 months later through lower fruit bunch formation and oil extraction rates. Analysts noted that rising fertiliser and gas costs linked to the Iran war have already increased food prices, and that they could rise further due to El Niño-related supply concerns. The Global Heat Health Information Network warned that fears of shortages could drive food inflation, forcing central banks to maintain elevated interest rates despite higher borrowing costs for businesses and strained government budgets. Inflation remained elevated in May, reaching 6.8% in the Philippines and 5.6% in Vietnam, while Indonesia faced cost-of-living pressures following a 32% increase in some non-subsidised fuel prices. The Global Heat Health Information Network said the combination of climate-related disruptions and geopolitical pressures could intensify fiscal strain, increasing the risk of protests, labour strikes and political instability, particularly as several Southeast Asian countries are already experiencing public discontent over living costs and governance issues. Governments still have time to strengthen water management, food stockpiles, targeted subsidies and farmer guidance, but the window for effective intervention is narrowing.

INDONESIA

Possible downgrade by MSCI this month could trigger up to USD 13 billion in fund outflows

(15 June 2026) MSCI is due to decide this month whether to downgrade Indonesia from emerging-market to frontier-market status, a move that some analysts estimate could trigger up to USD 13 billion in fund outflows. The Jakarta Composite Index has fallen nearly 31% this year amid concerns over the potential reclassification and investor unease regarding economic management under President Prabowo Subianto. Recent selloffs in Indonesian assets have intensified concerns, with foreign stock outflows approaching USD 4 billion year-to-date. Investors broadly expect Indonesia to retain its emerging-market status, which would help restore confidence and support growth prospects. The chief investment officer at UOB Asset Management Indonesia said progress had been made in improving market transparency, although it remains unclear whether this will satisfy MSCI. The rupiah continues to face pressure from elevated oil prices and a widening budget deficit, while rising state intervention in commodity exports and a corruption probe involving the former head of the government’s free meals programme have further unsettled investors. MSCI could retain Indonesia’s status, keep the market under review, or downgrade it to frontier-market status alongside countries such as Viet Nam and Bangladesh. Vontobel Asset Management said a downgrade would be particularly damaging as capital is returning to emerging markets while allocations to frontier markets remain limited. A reclassification could also prompt similar actions by FTSE Russell and S&P Dow Jones Indices, potentially creating a prolonged process for Indonesia to regain emerging-market status. Despite current concerns, PT Kiwoom Sekuritas Indonesia said Indonesia’s long-term investment case remains supported by its large economy, natural resources and domestic market. Authorities have introduced measures to improve liquidity, transparency and foreign investor access, including naming nine companies with high shareholder concentration to strengthen market confidence.

SINGAPORE

Labour market weakens in first quarter of 2026, with job vacancies declining

(16 June 2026) Singapore’s labour market softened in the first quarter of 2026, with job vacancies declining to 73,300 from 77,700 in December 2025 and 80,100 a year earlier, according to the Ministry of Manpower’s (MOM) Labour Market Report. The vacancy-to-unemployed-person ratio fell to 1.46 from 1.58 in the previous quarter, driven mainly by fewer openings for non-PMET roles, although PMET vacancies increased, including in financial services where openings rose from 4,300 to 5,800. Retrenchments increased to 3,830 from 3,690 in the fourth quarter of 2025, the highest quarterly level since the third quarter of 2023 and the highest first-quarter figure since 2017. Degree holders experienced a rise in retrenchments from 2.6 to 3.1 per 1,000 resident employees, reflecting restructuring in manufacturing, financial services and professional services. MOM said business reorganisation and restructuring, rather than cost-cutting, remained the primary reason for layoffs. The proportion of retrenched residents securing employment within six months improved to 60.7% from 57.4%, with gains among PMETs, degree holders and workers under 30. The number of employees placed on short work weeks or temporary layoffs increased to 1,230 from 960, particularly in construction, manufacturing and lower-skilled occupations. Despite these pressures, total employment grew by 9,400, extending a streak of 18 consecutive quarters of expansion, while resident employment rose by 5,400 jobs. The resident long-term unemployment rate remained unchanged at 0.9%. MOM expects retrenchments to stabilise, with the share of firms planning layoffs falling from 4.4% in February to 3.6% in March.

INDONESIA

Weakening rupiah sparks shrinkflation and consumer downgrading in Indonesia

(11 June 2026) Signs of economic strain are becoming more visible in Indonesia as street food vendors reduce portion sizes rather than raise prices, reflecting rising ingredient costs and weakening consumer purchasing power. The trend of shrinkflation and consumer downgrading has intensified as the rupiah fell past IDR 18,000 per US dollar last week and inflation continued to rise despite extensive fuel subsidies. While officials highlighted first-quarter annual economic growth of 5.61% and May inflation of 3.08%, concerns have grown over the rupiah’s status as Asia’s worst-performing currency this year and the Jakarta Composite Index’s position as the world’s weakest-performing major equity benchmark. Indonesia’s Finance Minister maintained that economic fundamentals remain strong, citing growth in car, motorcycle, electricity and cement sales. Retail car sales rose 8.8% in the first five months of 2026, while motorcycle sales increased 0.7%. Bank Indonesia has raised its policy rate by 75 basis points to 5.5% since 20 May, including a 25-basis-point increase at an emergency meeting, to support the currency. Banking sector stress indicators worsened, with gross non-performing loans rising to 2.17% in April from 2.05% in December and the 90-day delinquency rate at online lenders increasing to 4.62% from 4.32%. Indonesia also recorded its smallest trade surplus in more than six years in April as import values rose due to the weaker rupiah. An economist at the University of Indonesia warned that the government’s response risks creating a credibility problem and said the weakening currency should have prompted a greater sense of urgency. BMI attributed pressure on the rupiah partly to domestic factors, including commodity export policies, amendments expanding Bank Indonesia’s mandate, continued fuel subsidies and governance concerns linked to corruption cases. BMI warned that fuel subsidies could push the fiscal deficit above the legal ceiling of 3% of GDP and said investor concerns over governance and fiscal discipline remain unresolved.

MALAYSIA, THAILAND

Thai seafood traders face growing uncertainty following Malaysian ban on shrimp and seabass exports

(16 June 2026) Thailand’s shrimp exporters and farmers are facing growing uncertainty after Malaysia’s temporary ban, effective from 01 June, on imports of five Thai shrimp and prawn varieties led Malaysian customers to postpone or suspend orders, increasing storage costs and forcing exporters to seek alternative markets with different regulatory and product requirements. The dispute followed Thailand’s tighter inspections and import restrictions on Malaysian sea bass over chemical residue concerns, prompting Malaysia to impose reciprocal biosecurity measures and require an additional Certificate of Analysis for Thai sea bass. Malaysia imports approximately 6,000–8,000 tonnes of Thai shrimp annually, representing about 5% of Thailand’s total shrimp exports, and prolonged restrictions could lead to domestic oversupply, lower farm-gate prices and loss of export market share, although the Thai Shrimp Association expects any immediate price decline to remain limited while exporters redirect shipments. Thailand’s Agriculture and Cooperatives Minister proposed policy-level talks with Malaysia on 17 June, although discussions remain at the working level. Thailand has shortened its review of Malaysian sea bass inspection procedures, aiming to reduce testing times from around 15 days to about seven days while maintaining food safety standards, and pledged to monitor shrimp prices and support affected farmers. Thailand’s Department of Fisheries is preparing measures to strengthen the shrimp industry, such as reducing production costs, promoting technology and clean energy adoption, and encouraging domestic shrimp consumption. Malaysia’s Fisheries Department stated it is still awaiting Thailand’s response to its shrimp safety concerns before assessing compliance with Malaysian biosecurity requirements. Industry representatives and analysts called for the dispute to be resolved through scientific evidence, mutually recognised standards and closer bilateral cooperation, while urging Southeast Asian governments to strengthen regional food supply resilience instead of relying on protectionist measures.

VIET NAM

Viet Nam to maintain 10% economic growth for 2026 despite widening trade deficit and inflationary pressures

(17 June 2026) Viet Nam will maintain its 10% economic growth target for 2026 despite a widening trade deficit and inflationary pressures. The country’s trade deficit is estimated to have reached USD 15 billion in the first half of the year, compared with a trade surplus of USD 7.6 billion in the same period of 2025, primarily due to higher fuel import costs resulting from the war in the Middle East. Authorities said export growth is expected to accelerate during the second half of the year, narrowing the full-year trade deficit. Vietnam recorded a trade deficit of USD 13.8 billion in the first five months of 2026, compared with a surplus of USD 5.1 billion a year earlier. Higher fuel costs have also pushed annual inflation to 5.6% in May, exceeding the government’s full-year target of 4.5%. Viet Nam is also facing external trade pressure after the Trump administration alleged that the country distorts trade through excess capacity, intellectual property violations and the use of goods made with forced labour. Earlier this month, the United States proposed tariffs of up to 12.5% on imports from 60 countries, including Viet Nam, after determining they had failed to curb trade in goods produced with forced labour. Viet Nam said the US assessment did not fully or accurately reflect its mitigation efforts.

TIMOR-LESTE, MALAYSIA

Malaysia and Timor-Leste explore strategic cooperation across multiple sectors

(16 June 2026) Malaysia and Timor-Leste discussed expanding bilateral cooperation in strategic sectors during Timor-Leste President Jose Ramos-Horta’s special visit to Malaysia, including economic development, trade, investment, human capital development, education and Technical and Vocational Education and Training (TVET). Prime Minister Datuk Seri Anwar Ibrahim said both sides also explored new opportunities to support sustainable economic growth and create broader prospects for younger generations in both countries. The leaders reaffirmed their commitment to strengthening bilateral relations through strategic cooperation for mutual benefit. Anwar also emphasised the importance of enhancing regional ties based on solidarity, mutual respect and shared responsibility to promote peace, stability and prosperity within ASEAN. Ramos-Horta arrived in Malaysia on 13 June for a five-day special visit. Bilateral trade between Malaysia and Timor-Leste totalled USD 18.72 million in 2024, comprising Malaysian exports of USD 18.37 million and imports of USD 0.35 million.

RCEP Monitor

CHINA

Chinese listed banks continue to face pressure from shrinking net interest margins

(12 June 2026) Chinese listed banks continue to face pressure from shrinking net interest margins, with 46 of 58 commercial banks listed in mainland China and Hong Kong reporting lower margins in 2025 than in the previous year. Fifty of the 58 banks, or 86%, recorded net interest margins below the industry warning threshold of 1.8%, marking the fifth consecutive year that the proportion has increased. Agricultural Bank of China reported a first-quarter 2026 net interest margin of 1.26%, below its previous record low of 1.28% in 2025. Natixis said Chinese banks have lost the ability to generate the capital needed to support economic growth. Weak borrowing demand, intensified loan competition, and lower lending rates, linked to China’s prolonged property downturn and subdued consumer sentiment, have contributed to margin compression. China Merchants Bank reported a 2025 net interest margin of 1.87%, above the warning line, but its former president said the margin is expected to decline further this year. All four major state-owned banks reported lower margins in 2025, including China Construction Bank, whose margin fell by 0.17 percentage points to 1.34%. Falling profitability is raising concerns about banks’ capacity to absorb bad loans. Listed banks reported non-performing loans of CNY 2.4 trillion (USD 354 billion) at end-2025, up 5% year-on-year, although the official average non-performing loan ratio fell for a seventh consecutive year to 1.3%. However, Japan Research Institute estimated the bad loan ratio at 9.3%, up from 7.8% a year earlier, arguing that asset quality deterioration is not fully reflected in official figures. They also noted that consumer sentiment has remained weak since 2022, while retail sales growth slowed to 0.2% in April from 1.7% in March. Policymakers face a trade-off between supporting growth and protecting bank profitability, as further monetary easing could compress margins further. Beijing is targeting economic growth of 4.5% to 5% this year, while BNP Paribas said interest rate cuts are unlikely unless growth risks falling below that range.

CHINA

Retail sales decline 0.6% year-on-year in May 2026, first contraction since December 2022

(15 June 2026) China’s retail sales declined 0.6% year-on-year in May, the first contraction since December 2022 and below expectations for flat growth, signalling continued weakness in consumer spending despite the Labour Day holiday and earlier trade-in subsidies. Urban fixed-asset investment contracted 4.1% in the first five months of 2026, exceeding the expected 2.0% decline and worsening from the 1.6% contraction recorded in January–April, with real estate investment falling 16.2% and manufacturing investment contracting for the first time since December 2020. Infrastructure investment rose 0.6%, while industrial output increased 4.5% in May, exceeding the 4.3% forecast and improving from April’s 4.1% growth. The National Bureau of Statistics said the imbalance between strong supply and weak domestic demand remained acute, with businesses facing significant operational pressure, and called for technological development and stronger employment support. The national unemployment rate improved marginally to 5.1% in May from 5.2% in April. Economists said the weak retail data increases pressure on Beijing to introduce additional measures to support consumption, with further policy adjustments expected after second-quarter GDP data. China’s economy is expected to slow to 4.2% growth in the second quarter from 5.0% in the first quarter, reflecting persistent weakness in property and consumer demand despite resilient exports and manufacturing. Producer inflation accelerated to its fastest pace in almost four years in May as higher energy and commodity costs raised input prices, while consumer inflation remained subdued at 1.2%, indicating companies continued to absorb higher costs rather than pass them on to consumers.

AUSTRALIA

Reserve Bank of Australia keeps cash rate unchanged at 4.35%, states that future hikes possible

(16 June 2026) The Reserve Bank of Australia kept its cash rate unchanged at 4.35% in a unanimous decision, while stating it remains prepared to raise interest rates if required to achieve its mandates of price stability and full employment. The central bank said inflation remains too high and that it would assess the effects of previous rate increases and ongoing oil supply disruptions before making further policy changes. It warned that although the United States and Iran have reached an agreement to end the Iran conflict, the resolution remains at an early stage and disruptions to global oil supplies are likely to keep energy prices and inflation elevated. The RBA said prolonged global uncertainty could also weaken economic growth in Australia and its major trading partners. Australia’s economy expanded 2.5% year-on-year in the first quarter, below expectations and unchanged from the previous quarter, while quarterly GDP growth slowed to 0.3% from 0.9% in the previous quarter and below the 0.5% forecast. Annual inflation eased to 4.2% in April but remained above the RBA’s 2%–3% target range. The central bank said higher fuel prices are contributing directly to inflation and are increasingly feeding through into the prices of other goods and services, suggesting inflation is likely to remain elevated for some time. Following the decision, the S&P/ASX 200 edged lower, and the Australian dollar weakened 0.3% against the US dollar to 0.705.

|

15 participating countries |

20 chapters |

2.2 billion |

US$26.2 trillion |

28% |

| ASEAN member states, Australia, China, Japan, South Korea, New Zealand | trade in goods and services, investment, intellectual property, e-commerce, competition, SMEs, economic and technical cooperation, and government procurement | combined population, 30% world’s population | combined GDP, 30% global GDP | global trade (based on 2019 figures) |