CARI Captures Issue 747: Iran war raises export of Malaysian and Indonesian crude palm oil to multi-month highs

Captures has widened its scope to include news related to all the members of the Regional Comprehensive Economic Partnership (RCEP) agreement which was signed towards the end of 2020. Besides the ASEAN Member States, this includes Australia, New Zealand, China, Japan, and South Korea. The other weekly newsletters under CARI, China-ASEAN Monitor and Mekong Monitor will also be consolidated into the Captures newsletter. We hope this new version of Captures will serve you better and look forward to providing a curation of stories relevant to ASEAN and its trading partners.

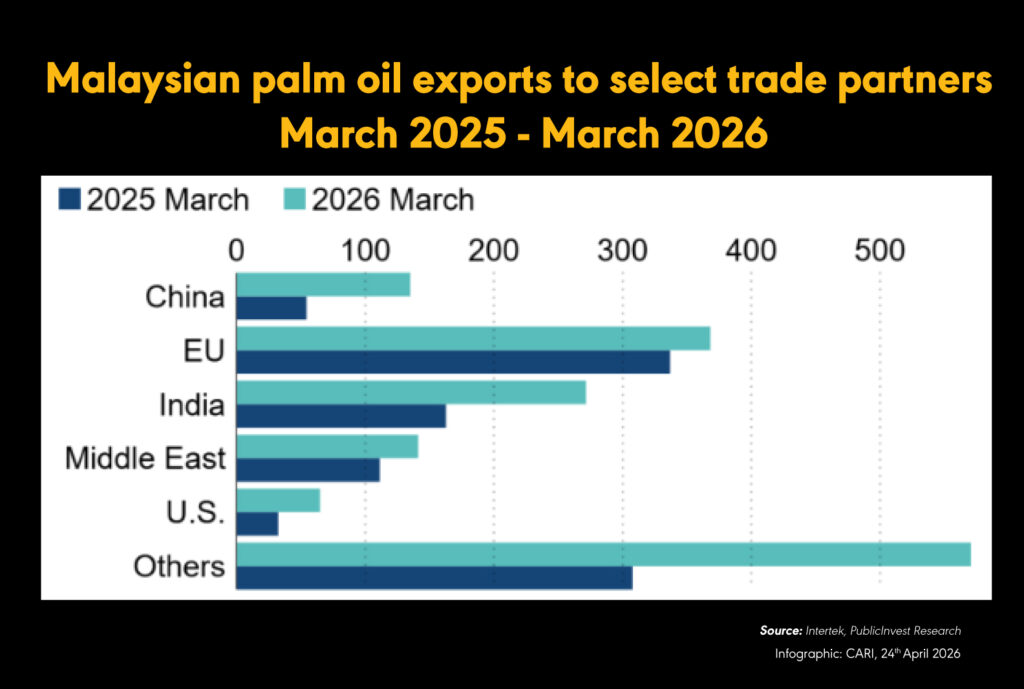

MALAYSIA, INDONESIA

Iran war raises export of Malaysian and Indonesian crude palm oil to multi-month highs

(20 April 2026) Demand for crude palm oil (CPO) has increased due to the Iran war, prompting stockpiling and lifting Malaysian and Indonesian exports to multi-month highs while raising supply concerns. CPO prices are under near-term upward pressure, supported by inventory build-ups and higher crude oil prices boosting biofuel demand. Malaysian palm oil futures reached their highest level since December 2024 in April following the conflict. Malaysia’s CPO exports rose 41% month on month in March to 1.6 million metric tons, the highest since October 2025, with strong demand from China, the Middle East, the U.S. and the EU. Exports to the Middle East surged 547.2% to 280,000 metric tons, while shipments to China and the U.S. rose 132.6% to 233,000 metric tons and 210.5% to 169,000 metric tons respectively. The EU remained the largest buyer, accounting for 23.4% or 963,000 metric tons of Malaysia’s exports from January to March 2026. Indonesia’s palm oil exports increased 36.26% year on year to 4.54 million tons in January–February. Rising fertiliser costs, up about 50% due to supply disruptions, are leading smallholders to reduce planting and fertiliser use, with potential production declines flagged by industry groups. Weather risks, including a 50%–60% probability of El Nino between July and September, could reduce fresh fruit bunch output by up to 16% and CPO production by up to 14% in subsequent years. Ageing plantations in Malaysia, with 35% of trees projected to be 19 years or older by next year, add to supply constraints. Indonesia plans to raise its biodiesel blending mandate to B50 from 01 July, potentially diverting 1.5 million tons of CPO from exports.

VIET NAM

Viet Nam’s housing market shifts away from cash purchases towards mortgage financing

(21 April 2026) Viet Nam’s housing market is undergoing a structural shift towards mortgage financing as rising property prices and changing consumer behaviour make cash purchases less feasible. Home loan value reached VND 2 quadrillion by Q3 2025, up from VND 1.1 quadrillion in 2020, while mortgages increased from 8.7% of total credit in 2017 to 12.7% last year, according to JLL. Apartment prices rose 20%–30% nationwide in 2025, with Ho Chi Minh City averaging VND 111 million per square metre, implying around USD 210,000 for a 50-square metre unit. Housing affordability has deteriorated, with prices exceeding 19 times median income, driving reliance on bank lending. Mortgage products have expanded, with typical structures offering fixed rates around 8% for 2–3 years before shifting to floating rates of 12%–14%, and loan tenors ranging from 15 to 35 years or up to 50 years. Rising interest rates, now above 10%, have dampened credit demand and increased repayment burdens, with some borrowers facing payment increases of up to 50% after promotional periods expire. Property transactions declined 14% year on year in Q1 to 115,650 units, indicating a slowdown, although full-year 2025 sales rose 7.7% to 579,718 units. Credit growth concerns have intensified, with the State Bank of Vietnam setting a 15% target for 2026 after 17.87% growth in 2025, amid risks of bad debt. Fitch Ratings warned that rapid credit expansion could increase exposure to speculative lending and asset price inflation. Developers and banks are expanding financing incentives, including interest subsidies and preferential rates for buyers under 35, while authorities are considering measures such as taxes and caps on second-home mortgages. Mortgage usage is estimated at 50%–70% among mid-market buyers in some projects, reflecting growing middle-class participation. Analysts describe the shift as a long-term trend despite short-term pressures from higher rates and external shocks, including the Middle East conflict.

MALAYSIA

Malaysian ringgit expected to continue strengthening in 2026

(20 April 2026) The Malaysian ringgit is projected by strategists to retest its year-to-date peak against the US dollar, with resistance identified at 3.88 compared with current levels near 3.95, following a recovery from a 4% decline in March linked to weakened global risk sentiment from the Iran war. Loomis Sayles & Co. and Deutsche Bank AG expect continued strengthening, with Loomis Sayles stating the currency could reach new 2026 highs supported by resilient growth, credible macroeconomic management, limited exposure to geopolitical flashpoints, and a diversified economy. Malaysia’s export strength and rising investment in its data centre sector, involving companies such as Oracle Corp., Amazon.com Inc., Alibaba Group Holding Ltd., and ByteDance Ltd., are key drivers of currency support. The economy expanded 5.5% in the first quarter, exceeding expectations and following 5.2% growth in 2024, with exports as a primary contributor. Investors are monitoring upcoming trade data for indications of any impact from the US-Iran conflict on export performance. Deutsche Bank highlighted Malaysia’s position as a net energy exporter, strong pre-conflict cyclical fundamentals, and exposure to global technology capital expenditure as supportive factors, forecasting the ringgit to trade in the 3.85 to 3.90 range. Oversea-Chinese Banking Corp. indicated support at 3.90 to 3.92, with potential for further gains if this range is breached. Analysts noted that growth momentum, elevated commodity prices, and sustained foreign inflows continue to underpin the currency outlook.

MALAYSIA

Economy expands 5.2% year-on-year in first quarter of 2026, moderating from fourth quarter of 2025

(17 April 2026) Malaysia’s economy expanded 5.3% year-on-year in the first quarter of 2026, according to advance estimates, moderating from 6.3% growth in the fourth quarter of 2025. Growth in the January to March period was driven by continued expansion in manufacturing, services and construction, although momentum slowed compared with the previous quarter. The mining and quarrying sector contracted by 1.1% due to lower crude oil and natural gas production. Malaysia’s Chief Statistician stated that the economy remains resilient despite rising global uncertainties and elevated oil prices linked to geopolitical tensions. Final first-quarter GDP data will be released on 15 May. Bank Negara Malaysia recently revised its 2026 growth forecast upward to a range of 4% to 5% from 4% to 4.5%, supported by household spending, exports and tourism. The economy grew 5.2% in 2025, exceeding expectations with record trade and approved investment levels. The central bank has warned that prolonged Middle East conflict could disrupt supply chains and increase fuel prices, posing risks to growth and inflation. Separate data showed consumer prices rose 1.7% year-on-year in March, in line with forecasts and up from 1.4% in the previous month.

THAILAND

Thailand mulls lifting public debt ceiling to enable additional borrowing

(20 April 2026) Thailand’s government is considering lifting its voluntary public debt ceiling to 75% of GDP from 70% to enable additional borrowing of about THB 1 trillion baht (approximately USD 30–31 billion), according to officials from the finance ministry and Prime Minister Anutin Charnvirakul’s office. The proposal, which remains under discussion and requires approval from the fiscal and monetary policy committee chaired by Anutin, is one of several options to address economic pressures from global energy shocks. The structure and allocation of the potential new borrowing have not been finalised. Separately, the government is preparing an emergency decree to raise up to THB 500 billion baht. Thailand’s Finance Minister indicated openness to increasing the debt limit if funds are directed towards investments that strengthen fiscal resilience. Government measures already announced include cash transfers to low-income groups, transport subsidies, and concessional loans for SMEs. A government spokesman stated that all funding options are being evaluated, but declined to confirm the debt ceiling increase. The policy shift reflects pressure on Thailand, a net energy importer, to create fiscal space amid rising costs linked to the Iran war, with inflation risks and weaker growth outlook. Economists have reduced growth forecasts as higher fuel prices weigh on consumption, exports, and tourism.

VIET NAM

Vingroup commences construction of high-speed rail line in northern Viet Nam

(13 April 2026) Vingroup has commenced construction of a high-speed rail line in northern Viet Nam as part of a planned USD 5.6 billion network, targeting a reduction in travel time from Hanoi to key northern destinations from about two hours to 23–30 minutes. The project aims to connect Hanoi with Bac Ninh, Hai Phong and Quang Ninh by end-2028, covering 120 km with trains operating at speeds of up to 350 km/h. Siemens Mobility will supply trains, infrastructure and services under a turnkey arrangement, alongside an agreed technology transfer programme. Vingroup confirmed the northern system would become Viet Nam’s first inter-regional bullet train if completed on schedule, although land clearance costs are excluded from the stated budget. The initiative follows Vingroup’s December withdrawal from the 1,541-km, USD 68 billion North–South high-speed rail project to focus on other developments. Its subsidiary VinSpeed is also targeting completion of a separate high-speed line linking Ho Chi Minh City to Can Gio by late 2028. The northern route will improve connectivity to Hai Phong, where Vingroup’s EV unit VinFast operates a production hub. Siemens Mobility cited extensive operational scale and safety performance alongside the planned technology transfer. The launch coincides with the start of a new five-year National Assembly term. Separately, Viet Nam’s president To Lam is scheduled to visit China to discuss a border rail partnership.

THE PHILIPPINES

The Philippines calls for support for job creation and climate financing at G-24 meeting

(19 April 2026) The Philippines called for expanded global support for job creation, financing and climate resilience at the G-24 Ministers’ and Governors’ Meeting on 14 April, citing increasing pressure on developing economies from geopolitical tensions and climate risks. The Philippines’ Finance Secretary stated that overlapping global challenges are constraining fiscal space and limiting countries’ capacity to respond. He urged scaled-up and more flexible financing, including budget support and emergency funding mechanisms, to help absorb external shocks while maintaining social services and development programmes. He also advocated stronger mobilisation of private capital to increase investment in infrastructure, energy transition and digital services to support employment and growth. He highlighted the need to strengthen human capital development to ensure economic reforms deliver quality jobs and improved livelihoods. He emphasised enhancing climate and disaster resilience, particularly for vulnerable countries such as the Philippines, through better access to climate financing and technical assistance. He called for deeper multilateral cooperation to reinforce the global financial system and support inclusive and sustainable development.

RCEP Monitor

SOUTH KOREA, INDIA

India and South Korea agree to double bilateral trade to USD 50 billion by 2030

(21 April 2026) India and South Korea agreed to expand economic cooperation across energy, critical minerals, shipbuilding, semiconductors and steel, with a target to double bilateral trade to USD 50 billion by 2030 from about USD 27 billion currently. The countries will resume and accelerate negotiations to upgrade their 2010 trade agreement, focusing on balancing trade and improving market access, including easing non-tariff barriers and rules of origin. South Korean President Lee Jae Myung, on an eight-year first state visit to India, held talks with Prime Minister Narendra Modi and was accompanied by around 200 business representatives. Both sides established a new ministerial-level economic cooperation committee and agreed to strengthen collaboration in nuclear power, clean energy, trade and investment. Energy security cooperation will be prioritised amid supply disruptions linked to the Iran war, including coordination on key inputs such as naphtha. The trade ministers of both countries agreed to fast-track trade pact discussions and expand cooperation in industry, green energy and digital trade. A joint business forum highlighted potential synergies between India’s AI capabilities and South Korea’s manufacturing sector, alongside new opportunities in shipbuilding. POSCO Holdings announced plans to invest about USD 1.09 billion by end-2031 in a joint venture with JSW to build a 6-million-ton-per-annum steel plant in Odisha. South Korea recorded a USD 12.8 billion trade surplus with India last year, with exports of USD 19.2 billion and imports of USD 6.4 billion, underscoring India’s concerns over trade imbalance.

NEW ZEALAND

Annual inflation remains unchanged at 3.1% in Q1, above central bank’s target range

(21 April 2026) New Zealand’s annual inflation remained unchanged at 3.1% in Q1, exceeding expectations of 2.9% and staying above the Reserve Bank of New Zealand’s 1%–3% target range. The consumer price index rose 0.9% quarter on quarter, compared with forecasts of 0.8%. Financial markets reacted with the New Zealand dollar rising 0.4% to USD 0.5916 and two-year swap rates increasing 5 basis points to 3.3951%. Interest rate swaps now indicate a 42% probability of a 25 basis point rate hike in May, up from below 30% previously, against the current 2.25% cash rate. The RBNZ had forecast 3% inflation for the quarter, with expectations of a rise to 4.2% in Q2 driven by higher oil prices linked to the Middle East conflict. Electricity prices, up 12.5%, were the largest contributor to inflation and accounted for more than a tenth of the annual increase, marking the third consecutive quarter as the main driver. ANZ noted the data showed no progress on non-tradable inflation and could raise concerns about inflation expectations, although it provided limited new insight into persistence. The central bank has signalled readiness to tighten policy if inflation accelerates further, while warning that the conflict may increase inflationary pressures and weigh on growth.

AUSTRALIA, CHINA

China approves more export licenses for Australian beef facilities

(21 April 2026) China approved export licences for eight additional Australian beef facilities, including six cold stores and two abattoirs such as Thomas Foods International in South Australia, according to the General Administration of Customs of China. It also upgraded 13 existing Australian abattoir licences to allow exports of chilled beef, increasing total new or enhanced licences to 15 and more than doubling prior capacity for chilled exports. Australia exported 272,940 tonnes of beef to China in 2025. The approvals come despite China imposing a 205,000-tonne import quota on Australian beef this year, after which a 55% tariff applies, with the quota expected to be filled by mid-June. Analysts noted the timing as inconsistent with existing trade restrictions. Global AgriTrends indicated the licence changes enable greater chilled beef exports and may reflect supply constraints in China. China’s agriculture ministry confirmed foot-and-mouth disease outbreaks in Xinjiang and Gansu in March, affecting 142 of 513 cattle in one location and 77 of 5,716 cattle in another, with containment measures implemented. Reports of broader outbreaks and reduced access to US beef were cited as possible factors tightening domestic supply. The Australian government stated the expanded access reflects recognition of product quality and safety. Industry participants noted increased demand but did not confirm links to disease outbreaks, while highlighting broader food security concerns amid global uncertainty.

|

15 participating countries |

20 chapters |

2.2 billion |

US$26.2 trillion |

28% |

| ASEAN member states, Australia, China, Japan, South Korea, New Zealand | trade in goods and services, investment, intellectual property, e-commerce, competition, SMEs, economic and technical cooperation, and government procurement | combined population, 30% world’s population | combined GDP, 30% global GDP | global trade (based on 2019 figures) |