CARI Captures Issue 745: Viet Nam’s GDP slows to 7.8% year-on-year in Q1 2026 amidst energy crisis

Captures has widened its scope to include news related to all the members of the Regional Comprehensive Economic Partnership (RCEP) agreement which was signed towards the end of 2020. Besides the ASEAN Member States, this includes Australia, New Zealand, China, Japan, and South Korea. The other weekly newsletters under CARI, China-ASEAN Monitor and Mekong Monitor will also be consolidated into the Captures newsletter. We hope this new version of Captures will serve you better and look forward to providing a curation of stories relevant to ASEAN and its trading partners.

VIET NAM

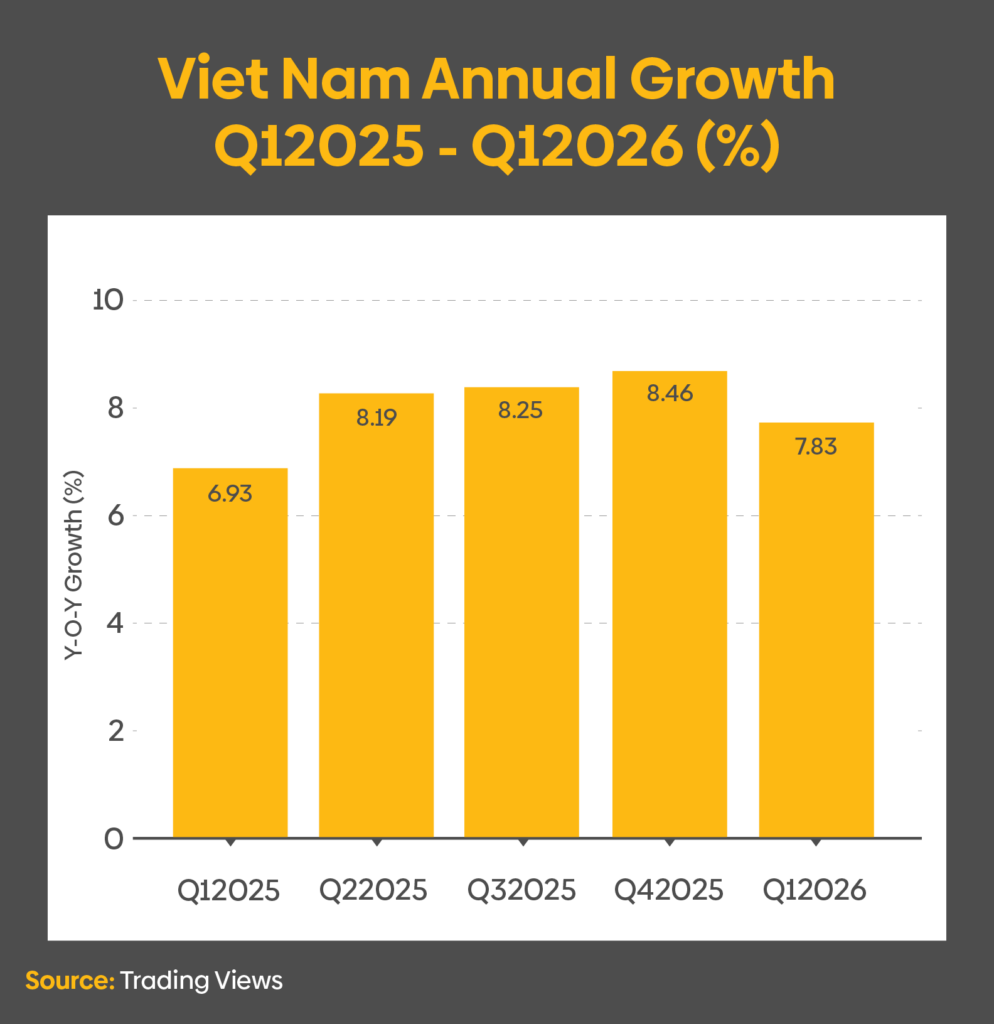

Viet Nam’s GDP slows to 7.8% year-on-year in Q1 2026 amidst energy crisis

(06 April 2026) Viet Nam’s GDP grew 7.8% year on year in Q1 2026, exceeding the 7.1% recorded in Q1 2025 but below both the 9.1% quarterly target and the 8.46% achieved in Q4 2025, according to the National Statistics Office. Achieving the government’s full-year target of at least 10% growth would require quarterly expansion of 10.5% in Q2, 10.6% in Q3, and 10.74% in Q4, contingent on stabilisation of Middle East conflict and energy prices. The global energy crisis significantly impacted performance, with Viet Nam importing over 80% of crude oil from the Persian Gulf and facing sharp fuel cost increases. March CPI rose 4.65% year on year, the fastest pace in five years, driven by gasoline prices rising 29.72%, diesel 57.03%, kerosene 62.35%, and gas 5.56%. It is believed that inflation could increase by an additional 1–2 percentage points, challenging the government’s 4.5% cap. Energy reliability emerged as a key investment constraint, with investors now requiring verified power allocation, grid upgrades, and infrastructure timelines before committing capital. The government introduced measures including a 10% electricity consumption reduction target until July, tax cuts on energy products, increased rooftop solar adoption, and expanded work-from-home policies. FDI disbursement reached USD 5.41 billion, up 9% and the highest Q1 level since 2022, while pledges and share purchases rose 43% to USD 15.2 billion. Imports increased 27% to USD 126.6 billion, with nearly 40% sourced from China, widening the trade deficit with China by 34% to USD 33.3 billion. Exports rose 19% to USD 122.9 billion, including USD 39 billion to the United States, resulting in a trade surplus with the U.S. of USD 33.9 billion, up 24%. Export activity accelerated ahead of U.S. tariff adjustments, following the replacement of a 20% tariff with a temporary 10% global tariff for 150 days. Executives identified energy supply, land reform, and U.S. trade policy as key determinants for investment flows in the second half of 2026.

VIET NAM

Pham Duc An appointed as governor of State Bank of Vietnam

(08 April 2026) Vietnam’s National Assembly appointed Pham Duc An, 56, as governor of the State Bank of Vietnam, replacing Nguyen Thi Hong, who will become vice chairwoman of the assembly for the 2026–2031 term. An, former chairman of Vietnam Bank for Agriculture and Rural Development and current chairman of Danang People’s Committee, assumes the role amid pressure to support a 10% growth target set by Party chief and President To Lam while containing inflation and maintaining financial stability. Vietnam’s credit-to-GDP ratio stands at 146%, with credit growth reaching 19% in 2025, limiting policy flexibility as credit expansion remains the primary growth lever. Inflation is rising, with consumer prices increasing 4.65% year on year in March, above the 4.5% target ceiling for 2026, driven partly by higher global energy prices linked to the Middle East conflict. The central bank has reduced its credit growth quota to 15% for 2026 and instructed banks to restrict lending to higher-risk sectors such as real estate. Liquidity conditions are tightening, with overnight interbank rates periodically reaching 7% as credit demand outpaces deposit growth, while banks raise interest rates to attract deposits. The leadership changes coincide with broader political consolidation, including the appointment of Ngo Van Tuan, 54, as finance minister and Le Minh Hung as prime minister. Market participants indicated limited adjustment time for the new governor, with expectations for immediate delivery on growth and stability objectives despite tightening financial conditions and external pressures including tariffs and energy price volatility.

ASEAN

ASEAN economies face increased risk of sovereign credit rating downgrades

(07 April 2026) Southeast Asian economies face increased risk of sovereign credit rating downgrades as fuel subsidies implemented to offset rising energy costs place pressure on fiscal balances and currencies. Indonesia maintained gasoline prices at IDR 10,000 per litre through subsidies, while the Philippines provided PHP 5,000 in cash support to transport drivers, and Viet Nam continued using a fuel price stabilisation fund, with Prime Minister Pham Minh Chinh planning expansion via a 2025 revenue increase. Thailand’s diesel subsidy programme pushed its oil fuel fund deficit to THB 42 billion, with potential borrowing of THB 20 billion raising concerns as public debt approaches 66% of GDP against a 70% legal ceiling. Indonesia’s Coordinating Minister estimated that oil at USD 97 per barrel would widen the fiscal deficit to 3.5% of GDP, exceeding the 3% legal cap, versus a prior 2.7% forecast. Credit outlooks for Indonesia were downgraded from stable to negative by Moody’s Ratings and Fitch Ratings amid concerns over fiscal discipline under President Prabowo Subianto’s spending plans, including free meals for 80 million people. The government is considering over IDR 100 trillion in budget cuts to contain the deficit. Currency depreciation has intensified, with the Philippine peso reaching a record low of PHP 60.748 per dollar and the Indonesian rupiah trading near IDR 17,000 per dollar, while Indonesia’s 10-year bond yields rose to around 6.9%, the highest since April 2025. Rising import costs due to weaker currencies are expected to feed inflation, potentially offsetting the intended stabilising effects of subsidies. Public unrest linked to fuel prices has emerged, including transport strikes in the Philippines and panic buying in Indonesia despite government assurances of stable pricing. The combination of elevated subsidies, weakening currencies and rising inflation creates a feedback loop that could further strain public finances and heighten downgrade risks.

THAILAND

Thailand plans broad economic and administrative reforms to boost growth

(06 April 2026) Thailand’s government plans broad economic and administrative reforms under a draft policy statement to be delivered by the prime minister, targeting faster growth and reduced business costs through technology adoption. The draft prioritises support for small and medium-sized enterprises, improved access to finance and investment in artificial intelligence, semiconductors and clean energy. It proposes fast-tracking an omnibus law within 2026 to remove outdated regulations and introducing a “super license” within 180 days to digitise state services and reduce bureaucracy. The government also intends to deploy big data and AI in agriculture to better align supply and demand, increase farmer income and boost food exports. Education reforms will focus on online access, job skills and AI-related training, alongside healthcare reform, social security updates and expanded support for an ageing population. Security measures include stricter drug controls, action against transnational crime and a review of free-visa entry rules. Tourism policy will shift towards flexible visas to encourage longer stays. Foreign tourist arrivals declined 2.3% year on year to 9.17 million between 01 January and 29 March. A leading business group forecasts 32 million arrivals in 2026, below the pre-pandemic level of nearly 40 million. The same group revised its 2026 GDP growth forecast down to 1.2%–1.6% from 1.6%–2.0%, compared with 2.4% growth recorded in 2025.

THAILAND

Thailand announces tighter control on crude palm oil exports and bottled palm oil prices

(06 April 2026) Thailand’s Commerce Ministry announced tighter controls on crude palm oil exports and bottled palm oil prices effective 07 April, in response to rising biodiesel demand linked to higher global fuel prices driven by the Middle East conflict. Under an order published in the Royal Gazette on 05 April, exporters must obtain prior government approval, providing details on destination, volume and pricing, with each permit valid for 30 days and requiring invoice submission within three days of shipment. The order, dated 03 April and signed by the Internal Trade Department’s director-general, will remain in force for one year. The ministry stated that the measures, alongside maintenance of energy reserves, will not affect farmers, who will continue to receive government protection. Thailand, the world’s third-largest palm oil producer, is forecast to produce 21.87 million tonnes of palm oil and 3.94 million tonnes of crude palm oil in 2026, according to the Office of Agricultural Economics. The policy aims to manage domestic supply and prices amid increased energy-linked demand pressures.

INDONESIA

Foreign exchange reserves decline for third consecutive month in March 2026

(08 April 2026) Indonesia’s foreign-exchange reserves declined for a third consecutive month in March, falling by USD 3.7 billion to USD 148.2 billion, the lowest level since July 2024, as Bank Indonesia intensified market intervention to stabilise the rupiah and the government met external debt obligations. Reserves have decreased by USD 8.3 billion in the first quarter of 2026. The rupiah weakened 1.3% in March amid higher oil import costs linked to the Middle East conflict and renewed concerns over fiscal pressures, prompting the central bank to prioritise exchange rate stability through continued intervention. A temporary US-Iran ceasefire contributed to a rebound in the currency, with the rupiah recording its strongest gain in seven months against the US dollar. Indonesia’s reserves remain sufficient to cover 5.8 months of imports and foreign debt servicing, which the central bank stated supports external sector resilience and financial stability. However, ongoing risks from elevated oil prices are expected to sustain pressure on the state budget and current account balance. Market expectations indicate Bank Indonesia is likely to maintain its policy interest rate unchanged for the remainder of 2026.

INDONESIA

Bank Indonesia indicates that scope for interest rate cuts is narrowing due to global developments

(08 April 2026) Bank Indonesia governor Perry Warjiyo stated that the scope for further interest rate cuts is narrowing due to global developments, signalling a recalibration of monetary policy to prioritise financial market stability. The central bank maintained its benchmark BI rate at 4.75% in March and indicated that the “room for reduction” is likely to shrink in the coming months. Policy adjustments will include increased issuance of rupiah-denominated securities (SRBI) to attract capital inflows while ensuring sufficient banking system liquidity to support lending. Bank Indonesia removed guidance on potential future rate cuts in its latest policy statement, reflecting the impact of the Middle East conflict, which has contributed to rupiah depreciation to record lows. The central bank had previously reduced rates by a cumulative 150 basis points between September 2024 and September 2025. Earlier expectations of continued monetary easing to support growth have been revised due to external pressures affecting currency stability.

RCEP Monitor

SOUTH KOREA

Household lending rises by KRW 0.5 trillion month-on-month at end-March 2026

(08 April 2026) South Korean household lending rose by KRW 0.5 trillion month on month to KRW 1,172.8 trillion at end-March, marking the first increase in four months, according to Bank of Korea data. The rebound was driven by growth in credit loans for stock investments, offsetting government measures aimed at limiting housing-related borrowing. Mortgage lending remained flat in March following a KRW 0.3 trillion increase in February. Other household loans, including credit lines and commercial real estate-backed lending, increased by KRW 0.5 trillion over the same period. Housing market activity showed volatility, with apartment transactions at 42,000 in December, 48,000 in January and 41,000 in February. The Bank of Korea maintained its benchmark interest rate at 2.50% after previous cumulative cuts of 25 basis points in February and May 2025 and in October and November 2024. Corporate lending increased by KRW 7.8 trillion to KRW 1,387 trillion, with loans to large companies rising by KRW 3.4 trillion and lending to small firms up KRW 4.5 trillion.

CHINA

Rebound in Chinese demand for LNG not expected to occur

(08 April 2026) Expectations for a rebound in China’s liquefied natural gas demand are weakening despite a Middle East ceasefire, as supply disruptions and higher prices persist. Chinese LNG imports fell 11% to 68.4 million tonnes last year, with BloombergNEF forecasting a further decline to 62.3 million tonnes in 2026, while Rystad Energy projects a modest increase to 70 million tonnes. Gas demand had already weakened, with apparent consumption down 0.9% in the first two months of 2026, extending declines seen in 2025. Forecasts assume LNG shipments from Qatar via the Strait of Hormuz will resume in April, but analysts indicate this will not offset structural supply damage from Iranian strikes. The destruction of two LNG trains in Qatar is expected to remove 12.5 million tonnes of annual capacity for three to five years, affecting a supplier that previously accounted for roughly one quarter of China’s LNG imports. China is expected to reduce reliance on Persian Gulf supply, increasing use of domestic production, pipeline gas from Russia and Central Asia, and substitutes such as coal and renewables. Alternative supply contracts outside the Gulf are estimated to cover demand for up to four months, after which China may increase imports from the United States despite tariffs. LNG prices rose sharply, with Asian spot benchmarks nearly doubling to about USD 20 per mmBtu in March, while China’s domestic-equivalent market increased 44% to around USD 15 per mmBtu. Industrial users have reduced operations, coastal power plants are limiting gas consumption, and importers are capping retail prices, further reducing LNG competitiveness. Higher price volatility is expected to constrain gas power utilisation relative to other energy sources.

NEW ZEALAND

Central bank keeps official cash rate on hold as fuel prices surge

(08 April 2026) New Zealand’s central bank held its official cash rate at 2.25%, the lowest level since mid-2022, with the Monetary Policy Committee signalling it will look through near-term inflation driven by higher fuel prices following the Middle East conflict. The decision, reached by consensus, maintains policy flexibility, with the committee indicating gradual rate increases may follow if inflation proves temporary, but warning that persistent second-round effects or rising medium-term expectations would require prompt tightening. The central bank expects inflation to rise to 4.2% in Q2 and remain above the 1–3% target range through 2026, with some economists projecting a peak above 4.5% by mid-year. Higher fuel costs are expected to feed into transport and food prices, while weak demand and spare capacity may limit broader price pass-through. Economic activity is slowing, with business feedback indicating weaker conditions in March and some forecasts pointing to a contraction in Q2 GDP. The New Zealand dollar was largely unchanged following the decision at around 58.03 US cents. The policy stance reflects uncertainty following a tentative US-Iran ceasefire, with oil prices having fallen below USD 100 per barrel after prior volatility.

|

15 participating countries |

20 chapters |

2.2 billion |

US$26.2 trillion |

28% |

| ASEAN member states, Australia, China, Japan, South Korea, New Zealand | trade in goods and services, investment, intellectual property, e-commerce, competition, SMEs, economic and technical cooperation, and government procurement | combined population, 30% world’s population | combined GDP, 30% global GDP | global trade (based on 2019 figures) |