CARI Captures Issue 734: Indonesia’s fiscal deficit reaches 2.92% of GDP in 2025, highest level in two decades

Captures has widened its scope to include news related to all the members of the Regional Comprehensive Economic Partnership (RCEP) agreement which was signed towards the end of 2020. Besides the ASEAN Member States, this includes Australia, New Zealand, China, Japan, and South Korea. The other weekly newsletters under CARI, China-ASEAN Monitor and Mekong Monitor will also be consolidated into the Captures newsletter. We hope this new version of Captures will serve you better and look forward to providing a curation of stories relevant to ASEAN and its trading partners.

INDONESIA

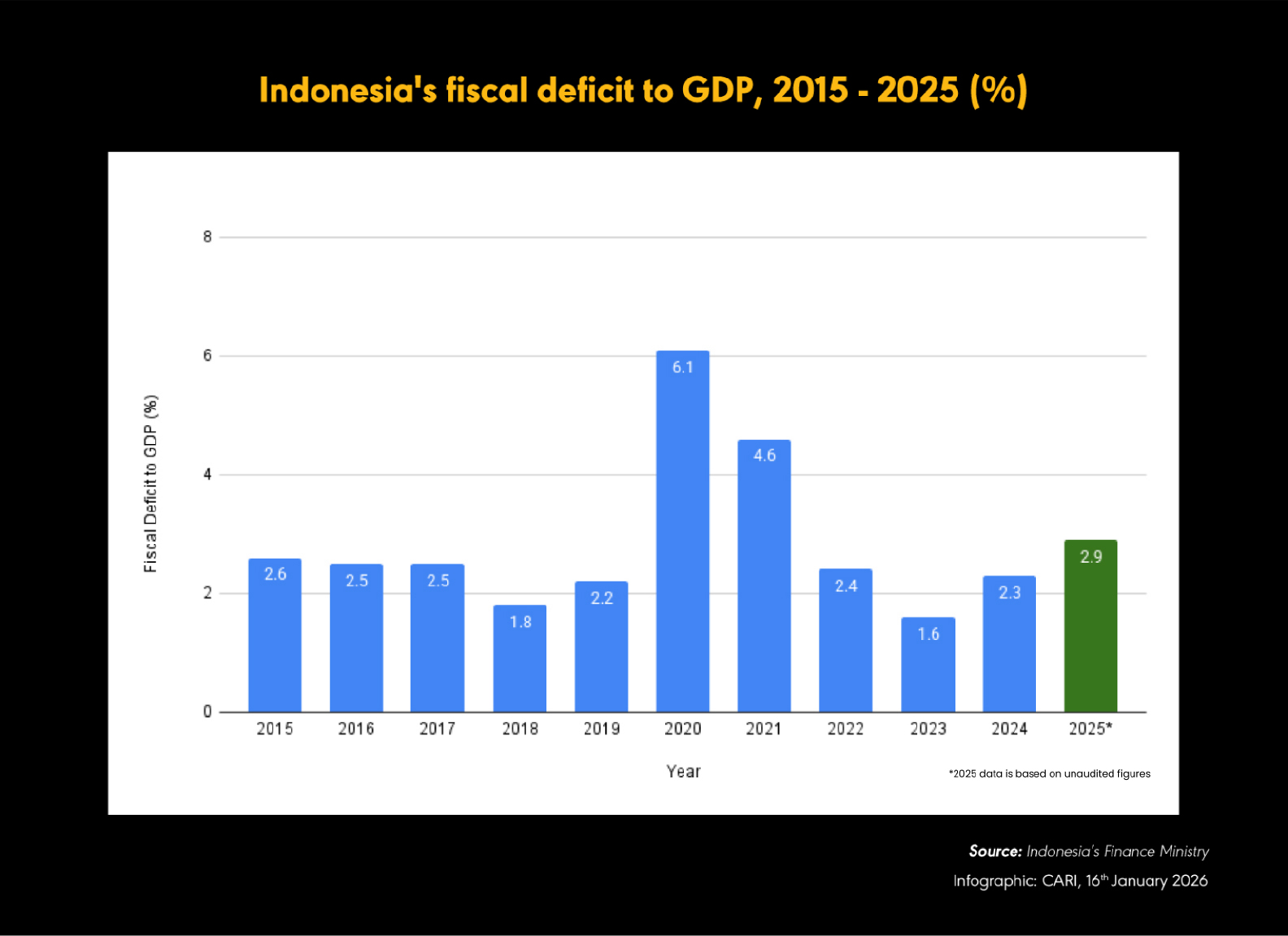

Indonesia’s fiscal deficit reaches 2.92% of GDP in 2025, highest level in two decades

(08 January 2026) Indonesia’s fiscal deficit reached IDR 695.1 trillion, equivalent to USD 41.4 billion or 2.92% of gross domestic product, in 2025, marking the highest level in at least two decades outside the pandemic years. Indonesia’s finance minister disclosed the unaudited figures, noting that the outcome exceeded the original target of 2.53% and the revised target of 2.78%. Bloomberg data show the ratio was the highest since 2005, excluding 2020 and 2021. The finance minister stated that spending was maintained to support economic expansion amid global uncertainty while keeping the deficit below the legal 3% cap. State expenditure rose 2.7% year on year to IDR 3,451.4 trillion, while state revenue declined 3.3% to IDR 2,756.3 trillion. Tax collection reached only about 90% of the government’s target. He cited higher tax refunds linked to weaker business profits in the trade and mining sectors, fiscal incentives for consumers, and lower oil, coal and nickel prices reducing non-tax revenue. Analysts highlighted risks to fiscal sustainability under the new finance minister, with Credit Agricole CIB expecting the deficit ratio to remain within 2.8% to 3% in coming years. Following the data release, the rupiah recorded a small loss against the US dollar, the 10-year government bond yield was unchanged, and equities reversed earlier gains. Analysts warned that a persistently high deficit could pressure the rupiah towards 16,900 per dollar and lift benchmark yields to as high as 6.2%.

INDONESIA

Authorities target 16 to 17.6 million foreign tourist arrivals in 2026

(13 January 2026) Indonesia’s government has set a target of 16 to 17.6 million foreign tourist arrivals in 2026. The government is targeting tourism foreign exchange earnings of between IDR 22 billion and IDR 24.7 billion. Tourism’s contribution to gross domestic product is projected to increase to between 4.5% and 4.7%. Agreed strategies include accelerating infrastructure development and improving connectivity between new and existing airports. Joint programmes between central and regional governments will be implemented in priority tourism destinations. Entry access for foreign tourists will be simplified through an evaluation of visa policies, with proposed changes to be reported to the President. Governance reforms will focus on digitalisation through integrated licensing systems and strengthened safety standards supported by tourism insurance. Government-borne income tax incentives for tourism workers will be provided in 2025 and 2026. As of the third quarter of 2025, tourism contributed 3.96% to GDP, generated USD 13.82 billion in foreign exchange earnings, and supported 25.91 million jobs. Total foreign tourist arrivals reached 13.98 million as of November 2025, with average spending per visitor at USD 1,259, led by visitors from Malaysia, Australia, Singapore, and China.

INDONESIA

Indonesia sells USD 2.7 billion worth of US-dollar-denominated bonds

(12 January 2026) Indonesia sold USD 2.7 billion of US-dollar-denominated bonds, marking the first such issuance by an Asian sovereign this year amid record global debt issuance at the start of 2026. The offering comprised three tranches with maturities ranging from five to 30 years. The longest tranche was a USD 500 million note maturing in 2056, priced to yield 5.5% after initial price guidance of around 5.8%. The issuance comes as the administration of President Prabowo Subianto seeks to finance a widening fiscal gap that risks breaching the statutory budget deficit cap of 3% of gross domestic product in 2026. Indonesia’s budget deficit reached 2.92% of GDP last year, the highest level in at least 20 years. For this year, the government has set a deficit target of 2.68% of GDP. Total net bond issuance, including domestic and foreign currency debt, is budgeted at IDR 799.5 trillion, equivalent to USD 47.4 billion. Citigroup revised its 2026 budget deficit forecast for Indonesia to 3.5% of GDP from 2.7%, citing expectations of accelerated spending on a free-meals programme and increased transfers to regional governments.

THE PHILIPPINES

Peso weakens to record low of 59.38 per US dollar in early January 2026

(13 January 2026) The Philippine peso weakened to a record low of 59.38 per US dollar in early January before partially recovering, with authorities signalling tolerance for further depreciation and limited intervention. The peso has fallen more than 3% since July following President Ferdinand Marcos Jr.’s disclosure of alleged misuse of flood infrastructure funds, which triggered investigations, mass protests and foreign investor withdrawals. Foreign investors recorded net equity outflows of USD 220 million between 29 July and 09 January, accounting for over 40% of local stock market turnover. The Bangko Sentral ng Pilipinas stated that business confidence and domestic growth prospects weakened amid concerns over public infrastructure spending. Expectations of further monetary easing have also weighed on the currency, with the central bank having cut rates by 200 basis points since August 2024 and signalling a possible additional cut this year. The government lowered its 2026 growth target to 5%–6% from 6%–7%, while other institutions also revised forecasts lower. Additional pressures include a 19% US tariff on Philippine goods imposed in August, weaker factory activity, and softer investment and services export inflows. Remittance inflows reached a record USD 34.5 billion in 2024 and were expected to rise to USD 35.5 billion, with a weaker peso boosting local purchasing power and household consumption, which accounts for about two-thirds of GDP. Currency depreciation could also support business-process outsourcing employment, which totals nearly 2 million workers, and improve export competitiveness, potentially narrowing a monthly trade deficit averaging USD 3 billion to USD 4 billion. Conversely, peso weakness raises import costs and inflation risks, particularly for fuel, machinery, electronics and food. The Department of Budget and Management estimates that every one-peso depreciation could generate an additional 9.3 billion pesos in tax revenue in 2026.

THAILAND

Exports forecast to grow by 2% to 4% in 2026, supported by expansion in electronics sector

(13 January 2026) Thailand’s exports are forecast to grow by 2% to 4% in 2026, according to the Thai National Shippers’ Council (TNSC), supported by potential expansion in the electronics sector. The chairman of the TNSC said the outlook reflects resilience despite subdued global demand linked partly to US tariff measures and a high comparison base after double-digit export growth last year. The council stated that electronics shipments retain growth capacity and are expected to benefit from increased foreign investment. Food and processed agricultural products are continuing to access new markets with strong demand for Thai goods. Automotive parts and vehicles are also expected to expand in selected niche segments. The council estimated that total exports grew by more than 9% last year, driven by accelerated import demand from key trading partners during the first three quarters.

CAMBODIA, UNITED STATES, CHINA

Phnom Penh seeking to reduce reliance on China amidst US tariff threats

(14 January 2026) Cambodia is seeking to reduce its economic reliance on China, its largest foreign investor, donor and trading partner. China accounts for more than half of total investment into Cambodia and is the largest source of raw materials for its export-oriented manufacturing sector. Phnom Penh has reassessed this dependence following US trade actions, after President Donald Trump initially threatened 49% tariffs on Cambodian goods, later reduced to 19%. Cambodia’s deputy prime minister said this prompted a strategy to avoid reliance on any single country and to avoid taking sides in the US-China rivalry. Cambodia is diversifying its investor base by targeting capital from the US, Europe and Brazil, and has conducted recent investment roadshows in the US, Canada, Japan and South Korea. The government is also seeking to diversify export markets beyond the US, which currently absorbs 40% of Cambodia’s exports, mainly footwear and sportswear. Policy focus has intensified on reducing dependence on Chinese inputs amid expectations of stricter US rules of origin and potential levies of up to 40% on goods deemed transshipped from China. Cambodian officials said Cambodia expects changes in US requirements on component sourcing thresholds. They added that bilateral relations with the US have improved following clarification over the Ream naval base. Cambodia and China have denied hosting Chinese naval forces at Ream, and Phnom Penh cited recent port calls by Vietnamese and Japanese warships, with a US warship expected this year. The US government did not comment.

LAO PDR

Economic conditions in Laos showing signs of recovery as market activities normalise

(14 January) Economic conditions in Laos are showing signs of recovery, with market activity normalising and price pressures linked to exchange rate volatility easing in several areas. Traders at Lao Market on 450 Year Road in Vientiane reported a return to typical customer volumes as food purchasing patterns stabilise. Earlier inflation led to sharp increases in meat, fish, poultry and vegetable prices, driven mainly by higher vendor input costs across the country. Traders indicated that these cost pressures have moderated, allowing trade conditions to improve. Market activity in urban and community areas has become more vibrant, supporting a gradual recovery in small businesses and the trade and services sectors. Employment opportunities and household income sources are expanding, particularly in agriculture, small-scale commerce, services and tourism-related activities. The government is continuing economic stabilisation measures, including promoting domestic production, import substitution, support for small and medium-sized enterprises and stronger economic management. Despite improvements, the cost of living remains elevated and high prices for some essential goods continue to strain household budgets. Public confidence is nevertheless improving, with households reporting greater adaptability and optimism.

RCEP Monitor

AUSTRALIA

Household spending rises 1% month-on-month in November, exceeding forecast

(12 January 2026) Australian household spending rose 1% month on month in November, exceeding the 0.6% forecast. Spending increased 6.3% year on year, also above expectations, with average annual spending up 4.6% so far in 2025 compared with 3% in 2024. The ABS reported that services spending rose 1.2%, driven by major events such as concerts and sporting fixtures, which lifted expenditure on catering, transport, recreation and cultural activities. Goods and services spending continued the momentum seen in October, with services spending 7.8% higher than November 2024 and goods spending up 4.9% year on year. The strongest monthly increases were recorded in furnishings and household equipment, followed by clothing and footwear, and recreation and culture. Goods spending growth was supported by Black Friday sales, particularly in clothing, footwear, furnishings and electronics. Private consumption accounts for more than half of GDP, increasing the relevance of the data for monetary policy. The Australian dollar held gains as markets maintained expectations of a Reserve Bank of Australia rate hike by mid-year. The RBA cut rates by 75 basis points last year to 3.6%, but the bank’s governor has indicated the next move may be a hike after inflation exceeded the 2–3% target range.

AUSTRALIA

Consumer sentiment weakens in January mainly due to interest rate expectations

(13 November 2026) Australian consumer sentiment weakened in January, with the Westpac Banking Corp index falling 1.7 per cent to 92.9 points, indicating pessimists again outnumbered optimists. The decline was attributed primarily to shifting interest rate expectations, with nearly two-thirds of surveyed consumers now expecting mortgage rates to rise over the next 12 months, more than double the proportion in September. The Reserve Bank of Australia has held the cash rate at 3.6% since August but has highlighted ongoing inflation pressures alongside a tight labour market. The governor has signalled that further easing is unlikely in the near term and that the next policy move could be a rate increase. The survey followed official data showing household spending rose faster than expected in November, supported by higher services expenditure and pre-Christmas retail discounting. Market expectations are increasingly aligned with a rate hike by mid-year, although economist forecasts remain mixed. Commonwealth Bank of Australia and National Australia Bank anticipate at least one rate rise this year, while Bank of America expects rates to remain unchanged. The RBA’s next policy decision will follow its 2–3 February meeting, informed by December employment figures and fourth-quarter inflation data due in late January. All components of the Westpac survey remained below the neutral 100 level, marking only the second instance since October 2024 where pessimism outweighed optimism across all sub-indexes.

NEW ZEALAND

Filled jobs in November mark highest employment level since March 2026

(14 January 2026) New Zealand employment increased again in November, with filled jobs rising by 6,569 or 0.3% month on month to 2.35 million, according to Statistics New Zealand. This marked the highest level since March and followed a trough in July at a two-and-a-half-year low. The November outcome represented the third increase in four months and indicated a return to job growth in the final quarter of 2025 after five quarters of contraction or stagnation. Westpac reported that worker confidence rose to its highest level since early 2024 in the fourth quarter. It’s suggested that the unemployment rate may have peaked at 5.3% in the third quarter, the highest level in five years. Business sentiment has improved after being weakened by the 2024 recession and uncertainty following US trade policies announced in mid-2025. The New Zealand Institute of Economic Research survey showed sentiment at its highest level in almost 12 years. The survey also recorded the first quarterly increase in hiring in two years, with a net 22% of firms planning to increase staff numbers in the three months to March. Employment gains are supporting expectations that the economic recovery can be sustained following GDP growth of 1.1% in the September quarter. Economic conditions have been supported by monetary easing, with the Reserve Bank lowering the Official Cash Rate to 2.25% in November. This brought total rate cuts to 325 basis points since August 2024.

|

15 participating countries |

20 chapters |

2.2 billion |

US$26.2 trillion |

28% |

| ASEAN member states, Australia, China, Japan, South Korea, New Zealand | trade in goods and services, investment, intellectual property, e-commerce, competition, SMEs, economic and technical cooperation, and government procurement | combined population, 30% world’s population | combined GDP, 30% global GDP | global trade (based on 2019 figures) |